In today’s fast-evolving tech landscape, DocuSign, Inc. and ServiceTitan, Inc. stand out as innovative leaders in software applications. Both companies serve distinct but overlapping markets by leveraging technology to streamline business operations—DocuSign focuses on digital agreements, while ServiceTitan optimizes field service management. This article will explore their growth strategies and market potential to help you decide which company is the more compelling investment opportunity in 2026.

Table of contents

Companies Overview

I will begin the comparison between DocuSign and ServiceTitan by providing an overview of these two companies and their main differences.

DocuSign Overview

DocuSign, Inc. is a technology company specializing in electronic signature software and digital agreement solutions. With a market cap of 11.4B USD and 6,838 employees, it offers a comprehensive suite of products including AI-driven contract lifecycle management and remote online notarization. Headquartered in San Francisco, DocuSign serves enterprise, commercial, and small businesses globally.

ServiceTitan Overview

ServiceTitan, Inc. operates in the software application industry focused on field service management for residential and commercial infrastructure. Founded in 2008 and based in Glendale, California, ServiceTitan employs 3,049 people and has a market cap of 8.5B USD. It provides software to streamline installation, maintenance, and service operations for various trades.

Key similarities and differences

Both DocuSign and ServiceTitan operate in the software application sector targeting B2B customers with cloud-based solutions. DocuSign centers on digital agreements and contract automation, while ServiceTitan focuses on field service management software. DocuSign has a larger workforce and market cap, reflecting its broader product scope and international reach compared to ServiceTitan’s specialized service niche.

Income Statement Comparison

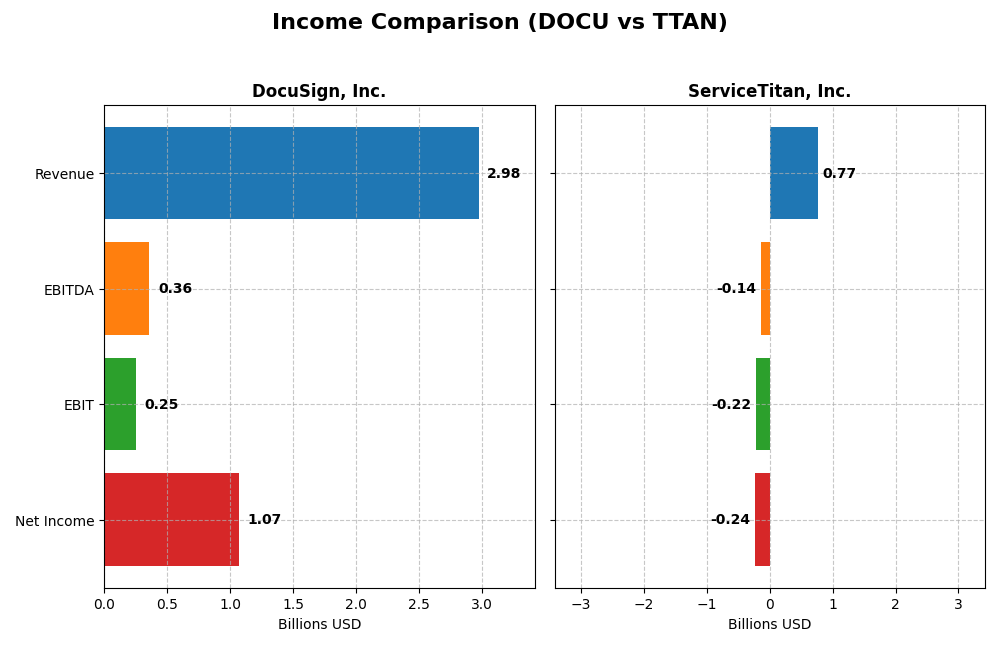

The table below presents a clear comparison of key income statement metrics for DocuSign, Inc. and ServiceTitan, Inc. for the fiscal year 2025.

| Metric | DocuSign, Inc. (DOCU) | ServiceTitan, Inc. (TTAN) |

|---|---|---|

| Market Cap | 11.36B | 8.50B |

| Revenue | 2.98B | 772M |

| EBITDA | 357M | -141M |

| EBIT | 249M | -221M |

| Net Income | 1.07B | -239M |

| EPS | 5.23 | -8.53 |

| Fiscal Year | 2025 | 2025 |

Income Statement Interpretations

DocuSign, Inc.

DocuSign’s revenue more than doubled from 2021 to 2025, reaching 3B in 2025, with net income turning strongly positive at 1.07B that year. Gross margins remained high at 79.1%, reflecting operational efficiency. The 2025 fiscal year showed solid growth: revenue rose 7.8%, EBIT surged 148%, and net margin expanded impressively, indicating improved profitability and cost control.

ServiceTitan, Inc.

ServiceTitan’s revenue grew steadily from 468M in 2023 to 772M in 2025, a 65% overall increase. However, net income remained negative, with a bottom line loss of 360M in 2025, despite a slight improvement in net margin. Gross margin was favorable at 64.9%, yet EBIT margin stayed deeply negative at -28.7%, signaling ongoing challenges in controlling expenses relative to revenue growth.

Which one has the stronger fundamentals?

DocuSign demonstrates stronger fundamentals with consistent revenue and net income growth, high gross and net margins, and positive EBIT margin, reflecting operational efficiency and profitability. ServiceTitan shows solid top-line growth but struggles with persistent losses and negative EBIT margin, indicating less mature financial performance and higher operational risks.

Financial Ratios Comparison

Below is a comparison of key financial ratios for DocuSign, Inc. and ServiceTitan, Inc. based on their most recent fiscal year data ending January 31, 2025.

| Ratios | DocuSign, Inc. (DOCU) | ServiceTitan, Inc. (TTAN) |

|---|---|---|

| ROE | 53.3% | -16.4% |

| ROIC | 9.1% | -14.1% |

| P/E | 18.5 | -18.1 |

| P/B | 9.87 | 2.98 |

| Current Ratio | 0.81 | 3.74 |

| Quick Ratio | 0.81 | 3.74 |

| D/E (Debt-to-Equity) | 0.06 | 0.11 |

| Debt-to-Assets | 3.1% | 9.4% |

| Interest Coverage | 129.0 | -14.8 |

| Asset Turnover | 0.74 | 0.44 |

| Fixed Asset Turnover | 7.28 | 9.57 |

| Payout Ratio | 0 | 0 |

| Dividend Yield | 0 | 0 |

Interpretation of the Ratios

DocuSign, Inc.

DocuSign shows a slightly favorable profile, with strong net margin (35.87%) and ROE (53.32%), indicating efficient profitability and shareholder returns. However, the low current ratio (0.81) and high price-to-book ratio (9.87) raise liquidity and valuation concerns. The company does not pay dividends, likely reinvesting earnings to support growth, consistent with its tech sector profile.

ServiceTitan, Inc.

ServiceTitan’s ratios are slightly unfavorable overall, suffering from negative profitability measures such as net margin (-30.98%) and ROE (-16.44%). While liquidity appears strong with a high current ratio (3.74) and low debt levels, negative interest coverage and asset turnover reflect operational challenges. The company also does not pay dividends, possibly focusing resources on expansion and R&D.

Which one has the best ratios?

Comparing both, DocuSign exhibits stronger profitability and shareholder return ratios, though it faces liquidity and valuation issues. ServiceTitan demonstrates weaker profit metrics and operational efficiency despite better liquidity. Thus, DocuSign holds a more favorable ratio profile, while ServiceTitan’s ratios suggest higher risk and challenges.

Strategic Positioning

This section compares the strategic positioning of DocuSign and ServiceTitan, including market position, key segments, and exposure to technological disruption:

DocuSign, Inc.

- Leading e-signature software provider facing competition in software applications.

- Revenue mainly from subscription services and professional services driving growth.

- Incorporates AI-driven contract lifecycle management and digital notarization technology.

ServiceTitan, Inc.

- Field service software provider with competitive pressures in residential and commercial sectors.

- Revenue primarily from platform and subscription services focused on field service management.

- Technology focused on infrastructure service operations without explicit AI disruption noted.

DocuSign, Inc. vs ServiceTitan, Inc. Positioning

DocuSign operates with a diversified portfolio of digital agreement and workflow products, leveraging AI technologies, while ServiceTitan concentrates on field service software platforms. DocuSign’s broader product base contrasts with ServiceTitan’s specialized market focus and smaller employee base.

Which has the best competitive advantage?

Both companies are currently shedding value relative to their cost of capital; DocuSign shows a growing ROIC trend indicating slight favorability, whereas ServiceTitan’s stable profitability is rated unfavorable, reflecting a weaker competitive moat.

Stock Comparison

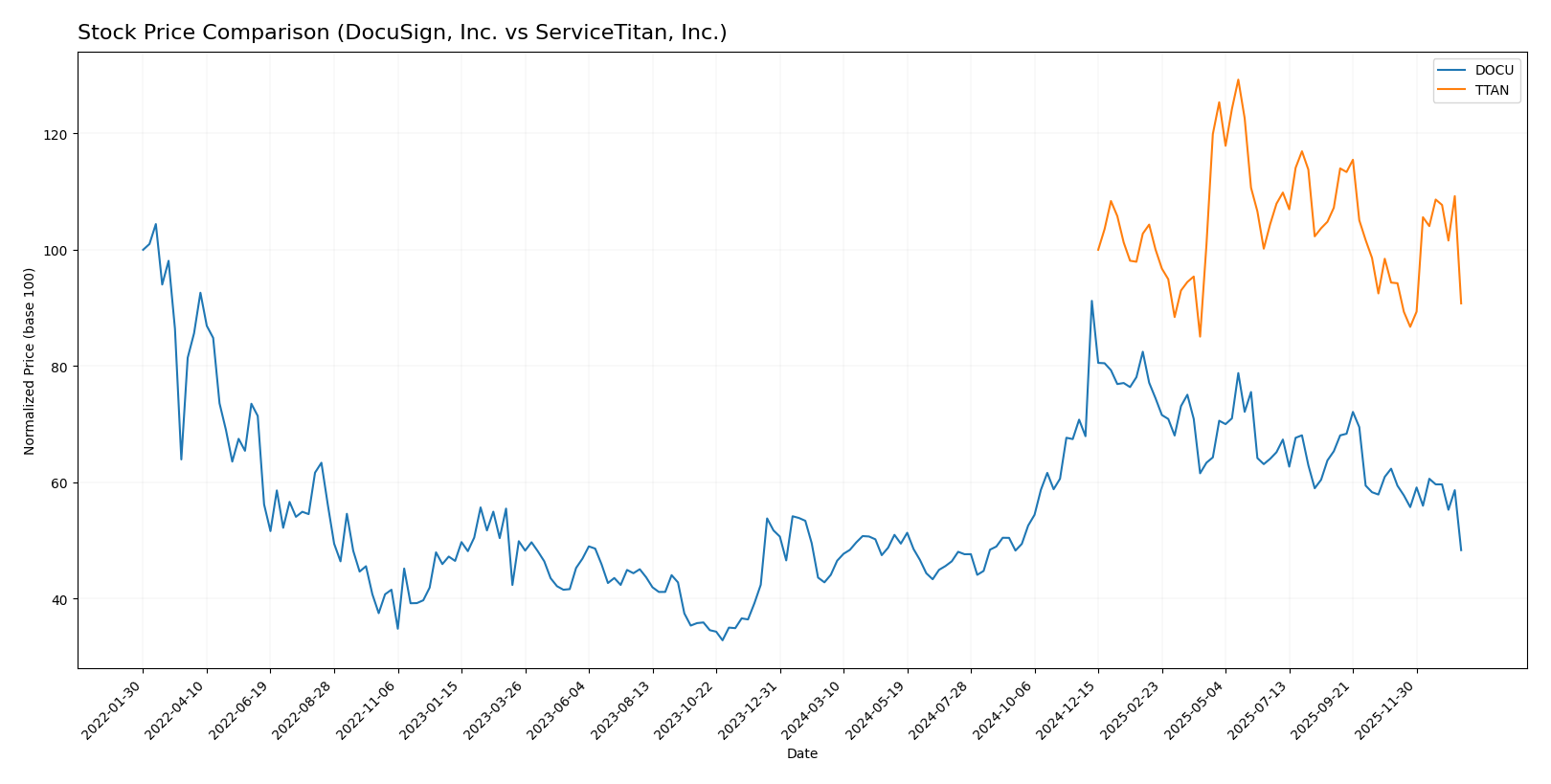

The stock price chart captures key price movements and trading dynamics for DocuSign, Inc. (DOCU) and ServiceTitan, Inc. (TTAN) over the past 12 months, highlighting distinct bullish and bearish trends.

Trend Analysis

DocuSign, Inc. (DOCU) exhibited a bullish trend over the past year with a 9.63% price increase, though the trend shows deceleration. The price ranged from a low of 50.84 to a high of 106.99, with volatility at 12.98%.

ServiceTitan, Inc. (TTAN) followed a bearish trend with a 9.22% decline in price over the same period, accompanied by accelerating downward momentum. Its price fluctuated between 85.07 and 129.26, with a volatility measure of 9.86%.

Comparing both stocks, DOCU delivered the highest market performance with positive growth, while TTAN experienced a notable decline in value over the past year.

Target Prices

The current analyst consensus for target prices shows optimistic upside potential for both DocuSign, Inc. and ServiceTitan, Inc.

| Company | Target High | Target Low | Consensus |

|---|---|---|---|

| DocuSign, Inc. | 88 | 70 | 76.86 |

| ServiceTitan, Inc. | 145 | 117 | 132.44 |

Analysts expect DocuSign’s price to rise from $56.71 to around $77 on average, and ServiceTitan’s from $90.78 to about $132, indicating notable growth potential for both stocks.

Analyst Opinions Comparison

This section compares analysts’ ratings and grades for DocuSign, Inc. and ServiceTitan, Inc.:

Rating Comparison

DocuSign, Inc. Rating

- Rating: B+ indicating a very favorable outlook.

- Discounted Cash Flow Score: 5, classified as very favorable.

- ROE Score: 4, considered favorable.

- ROA Score: 4, favorable assessment.

- Debt To Equity Score: 3, moderate financial risk.

- Overall Score: 3, moderate rating overall.

ServiceTitan, Inc. Rating

- Rating: C- with a very favorable status noted.

- Discounted Cash Flow Score: 1, very unfavorable.

- ROE Score: 1, very unfavorable.

- ROA Score: 1, very unfavorable.

- Debt To Equity Score: 3, moderate financial risk.

- Overall Score: 1, very unfavorable overall rating.

Which one is the best rated?

Based on the provided data, DocuSign shows stronger financial scores and a higher overall rating than ServiceTitan. DocuSign excels particularly in discounted cash flow, ROE, and ROA, while ServiceTitan’s scores are mostly very unfavorable except for debt to equity.

Scores Comparison

Here is a comparison of the Altman Z-Score and Piotroski Score for DocuSign, Inc. and ServiceTitan, Inc.:

DocuSign, Inc. Scores

- Altman Z-Score: 4.43, indicating a safe zone

- Piotroski Score: 5, assessed as average strength

ServiceTitan, Inc. Scores

- Altman Z-Score: 15.74, indicating a safe zone

- Piotroski Score: 6, assessed as average strength

Which company has the best scores?

ServiceTitan has a higher Altman Z-Score (15.74 vs. 4.43) and a slightly higher Piotroski Score (6 vs. 5) than DocuSign. Both companies are in the safe zone with average Piotroski strength.

Grades Comparison

The following is a comparison of the recent grades and consensus ratings for DocuSign, Inc. and ServiceTitan, Inc.:

DocuSign, Inc. Grades

This table summarizes the recent grades assigned to DocuSign, Inc. by reputable grading companies.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| RBC Capital | Maintain | Sector Perform | 2026-01-05 |

| Evercore ISI Group | Maintain | In Line | 2025-12-05 |

| UBS | Maintain | Neutral | 2025-12-05 |

| Wells Fargo | Maintain | Equal Weight | 2025-12-05 |

| Piper Sandler | Maintain | Neutral | 2025-12-05 |

| RBC Capital | Maintain | Sector Perform | 2025-12-05 |

| JP Morgan | Maintain | Neutral | 2025-12-05 |

| B of A Securities | Maintain | Neutral | 2025-12-05 |

| Needham | Maintain | Hold | 2025-12-05 |

| Baird | Maintain | Neutral | 2025-12-05 |

DocuSign’s grades consistently reflect a hold or neutral stance, indicating a cautious outlook among analysts.

ServiceTitan, Inc. Grades

The following table shows recent reliable grades assigned to ServiceTitan, Inc. by recognized grading companies.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Piper Sandler | Maintain | Overweight | 2025-12-05 |

| BMO Capital | Maintain | Outperform | 2025-12-05 |

| TD Cowen | Maintain | Buy | 2025-12-05 |

| Morgan Stanley | Maintain | Equal Weight | 2025-12-05 |

| BMO Capital | Maintain | Outperform | 2025-11-20 |

| Wells Fargo | Maintain | Overweight | 2025-09-19 |

| Stifel | Maintain | Buy | 2025-09-19 |

| Piper Sandler | Maintain | Overweight | 2025-09-19 |

| Canaccord Genuity | Maintain | Buy | 2025-09-19 |

| Citigroup | Maintain | Neutral | 2025-09-09 |

ServiceTitan’s grades predominantly indicate buy or outperform ratings, reflecting a more positive analyst sentiment.

Which company has the best grades?

ServiceTitan, Inc. has received consistently stronger grades than DocuSign, Inc., with more buy and outperform ratings versus DocuSign’s neutral and hold recommendations. This difference may influence investors’ perceptions of growth potential and risk profiles.

Strengths and Weaknesses

Below is a comparison table summarizing the key strengths and weaknesses of DocuSign, Inc. (DOCU) and ServiceTitan, Inc. (TTAN) based on their latest financial and operational data.

| Criterion | DocuSign, Inc. (DOCU) | ServiceTitan, Inc. (TTAN) |

|---|---|---|

| Diversification | Moderate; mainly subscription-based with professional services contributing <$75M annually | Moderate; platform revenue and subscription revenue split roughly 57%/43% |

| Profitability | High net margin (35.9%) and ROE (53.3%); slightly favorable overall ratios | Negative net margin (-31%) and ROE (-16.4%); profitability currently unfavorable |

| Innovation | Strong innovation indicated by growing ROIC trend (+167.8%) but currently shedding value | Neutral ROIC trend with value destruction; innovation impact unclear |

| Global presence | Well-established global footprint as leader in e-signature services | Primarily focused on North American trades services market |

| Market Share | Leading position in digital agreement management | Growing market share in service management software but profitability issues |

Key takeaways: DocuSign shows strong profitability and a growing return on invested capital, signaling improving value creation despite some valuation concerns. ServiceTitan, while expanding its platform revenue, faces challenges with negative profitability and value destruction, warranting cautious assessment for investors.

Risk Analysis

Below is a comparative summary of key risks for DocuSign, Inc. (DOCU) and ServiceTitan, Inc. (TTAN) as of 2025.

| Metric | DocuSign, Inc. (DOCU) | ServiceTitan, Inc. (TTAN) |

|---|---|---|

| Market Risk | Moderate (Beta ~0.99) | Low to Negative (Beta ~-0.85) |

| Debt level | Low (Debt/Equity 0.06) | Low (Debt/Equity 0.11) |

| Regulatory Risk | Moderate (Tech and data privacy regulations) | Moderate (Industry-specific compliance) |

| Operational Risk | Moderate (Complex software solutions) | Moderate to High (Field service operations) |

| Environmental Risk | Low (Software sector) | Low (Service software) |

| Geopolitical Risk | Moderate (US and global markets) | Moderate (US focused) |

In 2025, the most impactful risks for DocuSign revolve around regulatory compliance and market competition, while ServiceTitan faces operational challenges and negative profitability, increasing its financial risk despite low debt. Investors should closely monitor ServiceTitan’s path to profitability and DocuSign’s ability to sustain growth amid evolving data privacy laws.

Which Stock to Choose?

DocuSign, Inc. (DOCU) shows a favorable income evolution with strong net margin growth of 35.87% and a 7.78% revenue increase in 2025. Its financial ratios are slightly favorable, highlighting robust profitability (ROE at 53.32%) and low debt (D/E 0.06), supported by a very favorable B+ rating.

ServiceTitan, Inc. (TTAN) presents a mixed income picture, with a favorable 25.64% revenue growth but an unfavorable net margin of -30.98%. Financial ratios lean slightly unfavorable due to negative returns (ROE -16.44%) despite moderate debt levels (D/E 0.11). Its overall rating is C-, categorized as very unfavorable.

From an investor perspective, DOCU’s slightly favorable financial ratios, strong profitability, and very favorable rating suggest it might appeal to those seeking quality and income growth. By contrast, TTAN’s unfavorable ratios and rating could indicate higher risk, possibly suiting risk-tolerant investors focused on growth potential despite current losses.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of DocuSign, Inc. and ServiceTitan, Inc. to enhance your investment decisions: