Home > Analyses > Healthcare > Zimmer Biomet Holdings, Inc.

Zimmer Biomet reshapes lives by restoring mobility through cutting-edge musculoskeletal solutions. It leads the medical devices sector with flagship products like knee and hip implants, spine devices, and advanced surgical tools. Renowned for innovation and quality, Zimmer Biomet influences global orthopedic care standards. As healthcare demands evolve, I question whether its fundamentals still justify its valuation and growth prospects in a competitive, innovation-driven market.

Table of contents

Business Model & Company Overview

Zimmer Biomet Holdings, Inc., founded in 1927 and headquartered in Warsaw, Indiana, leads the musculoskeletal healthcare sector. The company integrates orthopaedic reconstructive products, spine solutions, and dental implants into a unified ecosystem. This ecosystem addresses complex bone and joint disorders with precision, supporting surgeons and healthcare providers worldwide.

Zimmer Biomet’s revenue engine balances advanced medical devices, surgical instruments, and regenerative products. Its footprint spans the Americas, Europe, the Middle East, Africa, and Asia Pacific, enabling broad market access. The company’s competitive advantage lies in its innovation pipeline and global reach, securing a durable economic moat in orthopaedic device manufacturing.

Financial Performance & Fundamental Metrics

I analyze Zimmer Biomet Holdings, Inc.’s income statement, key financial ratios, and dividend payout policy to assess its core financial health and shareholder value.

Income Statement

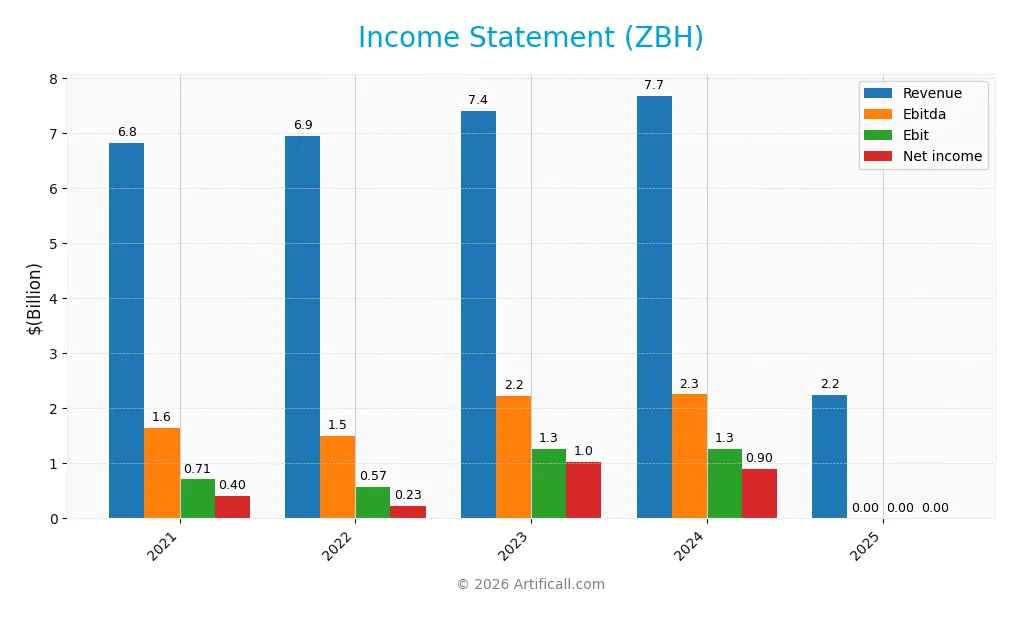

The table summarizes Zimmer Biomet Holdings, Inc.’s key income statement figures over the past five fiscal years, highlighting revenue growth and profitability trends.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 6.83B | 6.94B | 7.39B | 7.68B | 8.23B |

| Cost of Revenue | 1.96B | 2.02B | 2.08B | 2.19B | 3.16B |

| Operating Expenses | 4.01B | 4.22B | 4.03B | 4.20B | 3.71B |

| Gross Profit | 4.87B | 4.92B | 5.31B | 5.49B | 5.07B |

| EBITDA | 1.65B | 1.49B | 2.22B | 2.25B | 2.22B |

| EBIT | 707M | 568M | 1.27B | 1.25B | 1.12B |

| Interest Expense | 208M | 165M | 201M | 218M | 293M |

| Net Income | 402M | 231M | 1.02B | 904M | 705M |

| EPS | 1.93 | 1.10 | 4.91 | 4.45 | 3.56 |

| Filing Date | 2022-02-25 | 2023-02-24 | 2024-02-23 | 2025-02-25 | 2026-02-20 |

Income Statement Evolution

Zimmer Biomet’s revenue grew 20.6% from 2021 to 2025, reaching $8.23B in 2025. Net income surged 75.6% over the same period, hitting $705M in 2025. However, recent growth slowed with a 7.2% revenue rise but a 27.2% net margin decline in 2025. Gross margin contracted, signaling margin pressure despite overall expansion.

Is the Income Statement Favorable?

In 2025, Zimmer Biomet shows a favorable income statement with a 61.6% gross margin and 13.7% EBIT margin. Interest expense remains contained at 3.6% of revenue, supporting profitability. Yet, EBIT and net income declined year-over-year, reflecting margin compression. Despite this, the company’s fundamentals remain solid with long-term growth in earnings per share and net margin.

Financial Ratios

The table below presents key financial ratios for Zimmer Biomet Holdings, Inc. over the last five fiscal years:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 5.9% | 3.3% | 13.8% | 11.8% | 8.6% |

| ROE | 3.2% | 1.9% | 8.2% | 7.2% | 5.6% |

| ROIC | 3.6% | 2.6% | 6.3% | 5.7% | 5.5% |

| P/E | 64.0 | 115.5 | 24.8 | 23.7 | 25.2 |

| P/B | 2.03 | 2.22 | 2.04 | 1.72 | 1.40 |

| Current Ratio | 1.41 | 1.88 | 1.61 | 1.91 | 1.98 |

| Quick Ratio | 0.79 | 0.97 | 0.78 | 0.99 | 1.10 |

| D/E | 0.56 | 0.47 | 0.46 | 0.50 | 0.59 |

| Debt-to-Assets | 30.1% | 27.0% | 26.8% | 29.0% | 32.6% |

| Interest Coverage | 4.1x | 4.2x | 6.4x | 5.9x | 4.7x |

| Asset Turnover | 0.29 | 0.33 | 0.34 | 0.36 | 0.36 |

| Fixed Asset Turnover | 3.72 | 3.71 | 3.59 | 3.75 | 3.73 |

| Dividend Yield | 0.78% | 0.75% | 0.79% | 0.91% | 1.07% |

Evolution of Financial Ratios

Return on Equity (ROE) declined steadily from 8.2% in 2023 to 5.5% in 2025, signaling reduced profitability. The Current Ratio improved from 1.61 to 1.98, indicating stronger liquidity. Debt-to-Equity Ratio rose moderately from 0.46 to 0.59, reflecting a cautious increase in leverage while profitability showed signs of weakening.

Are the Financial Ratios Favorable?

In 2025, Zimmer Biomet’s liquidity ratios, including Current (1.98) and Quick (1.1), remain favorable, supporting short-term financial health. Profitability metrics like ROE (5.5%) and Net Margin (8.6%) appear neutral to unfavorable, below industry benchmarks. Leverage stands neutral with debt-to-equity at 0.59. Asset turnover is unfavorable at 0.36, signaling efficiency challenges. Overall, ratios are slightly favorable but warrant careful monitoring.

Shareholder Return Policy

Zimmer Biomet Holdings, Inc. maintains a consistent dividend policy with a payout ratio around 27% and a dividend yield near 1.07% in 2025. The company supplements dividends with share buybacks, supported by strong free cash flow coverage, indicating disciplined capital allocation.

This approach balances shareholder returns with investment capacity. The moderate payout and buybacks signal sustainable distributions aligned with long-term value creation. Risks include potential pressure if earnings decline, but current cash flow metrics suggest prudent management.

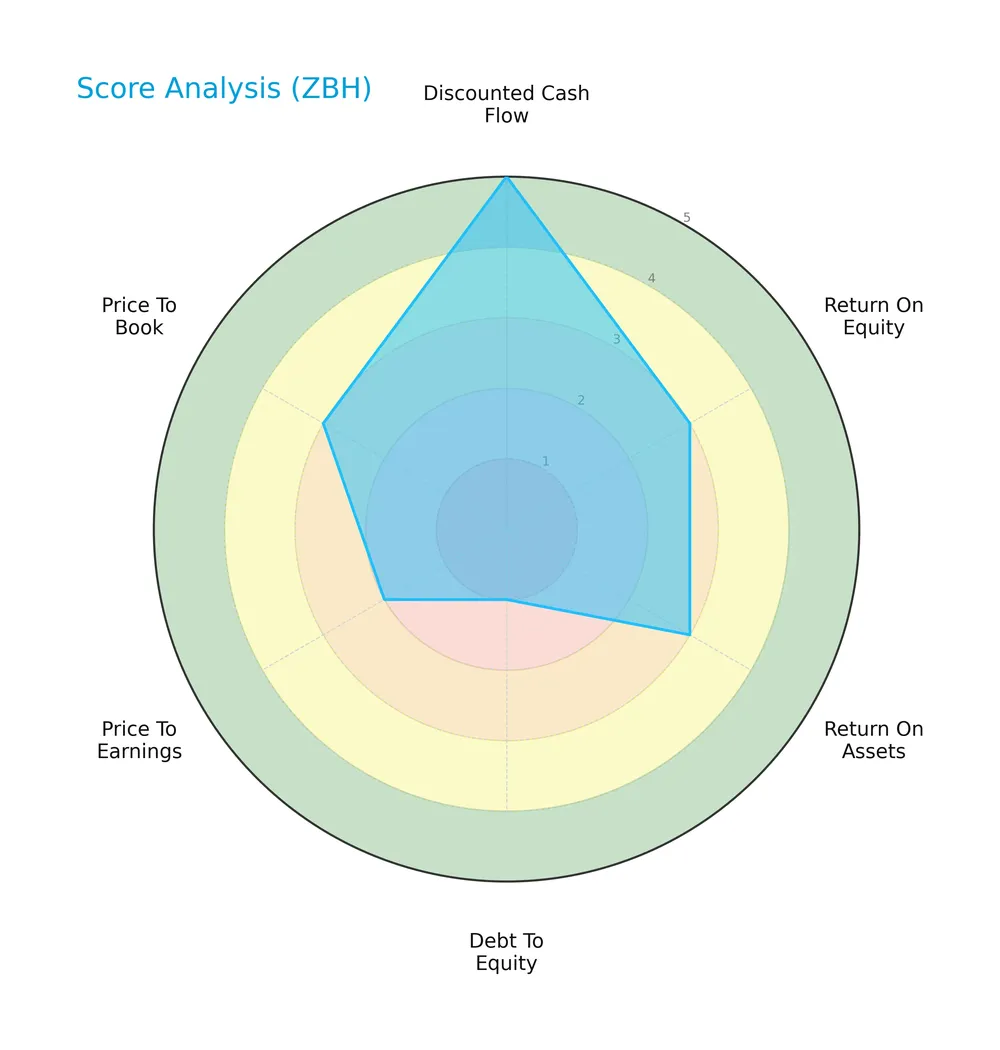

Score analysis

The radar chart below illustrates Zimmer Biomet Holdings, Inc.’s key financial scores across valuation, profitability, and leverage metrics:

Discounted Cash Flow scores very favorably at 5, indicating solid valuation support. Profitability metrics, ROE and ROA, both hold moderate scores of 3. Debt-to-Equity and P/E ratios are weak at 2, signaling leverage and valuation concerns. The Price-to-Book ratio scores favorably at 4.

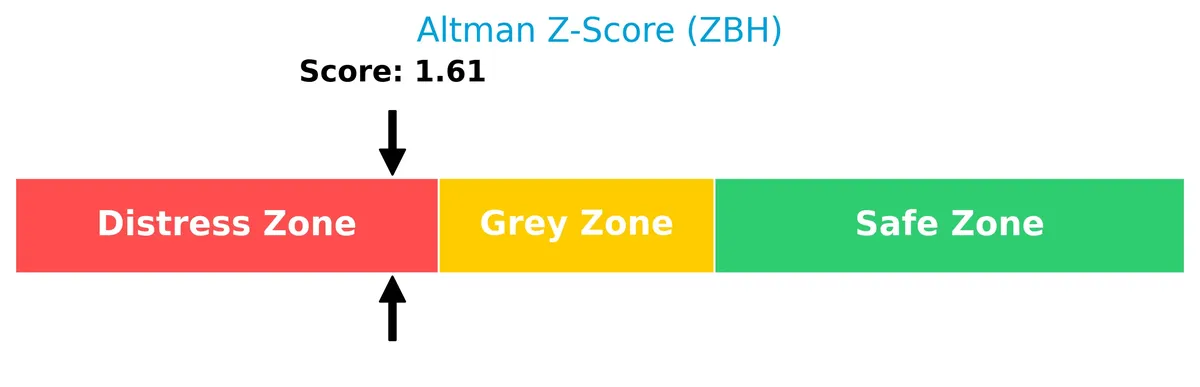

Analysis of the company’s bankruptcy risk

Zimmer Biomet’s Altman Z-Score places it in the grey zone, suggesting moderate bankruptcy risk and some financial uncertainty:

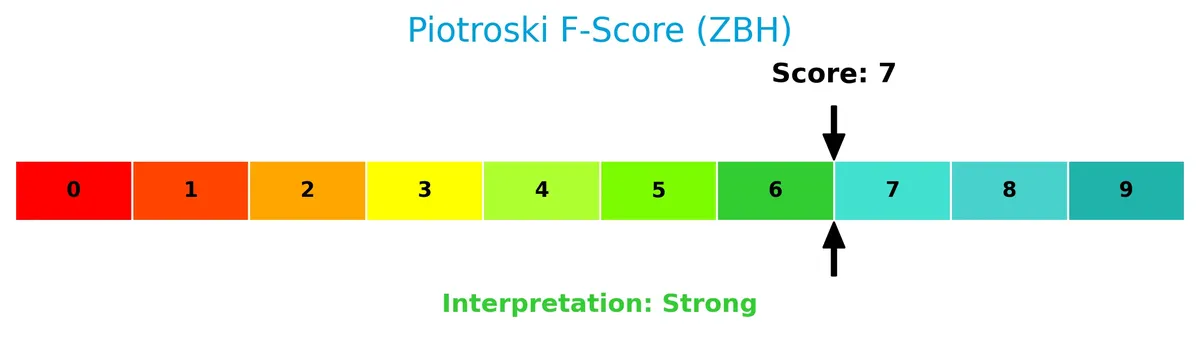

Is the company in good financial health?

The Piotroski Score diagram highlights Zimmer Biomet’s financial strength based on nine key accounting criteria:

A score of 7 classifies the company as strong, reflecting solid profitability, liquidity, and operational efficiency. This suggests Zimmer Biomet maintains good financial health relative to investment benchmarks.

Competitive Landscape & Sector Positioning

This sector analysis explores Zimmer Biomet Holdings, Inc.’s strategic positioning, revenue segments, and key products. I will assess whether the company holds a competitive advantage over its main competitors.

Strategic Positioning

Zimmer Biomet strategically diversifies across orthopaedic product lines—hips, knees, and S.E.T.—with stable growth. Geographically, it maintains broad exposure in the Americas (5.1B), EMEA (1.8B), and Asia Pacific (1.3B), balancing regional risks and growth opportunities.

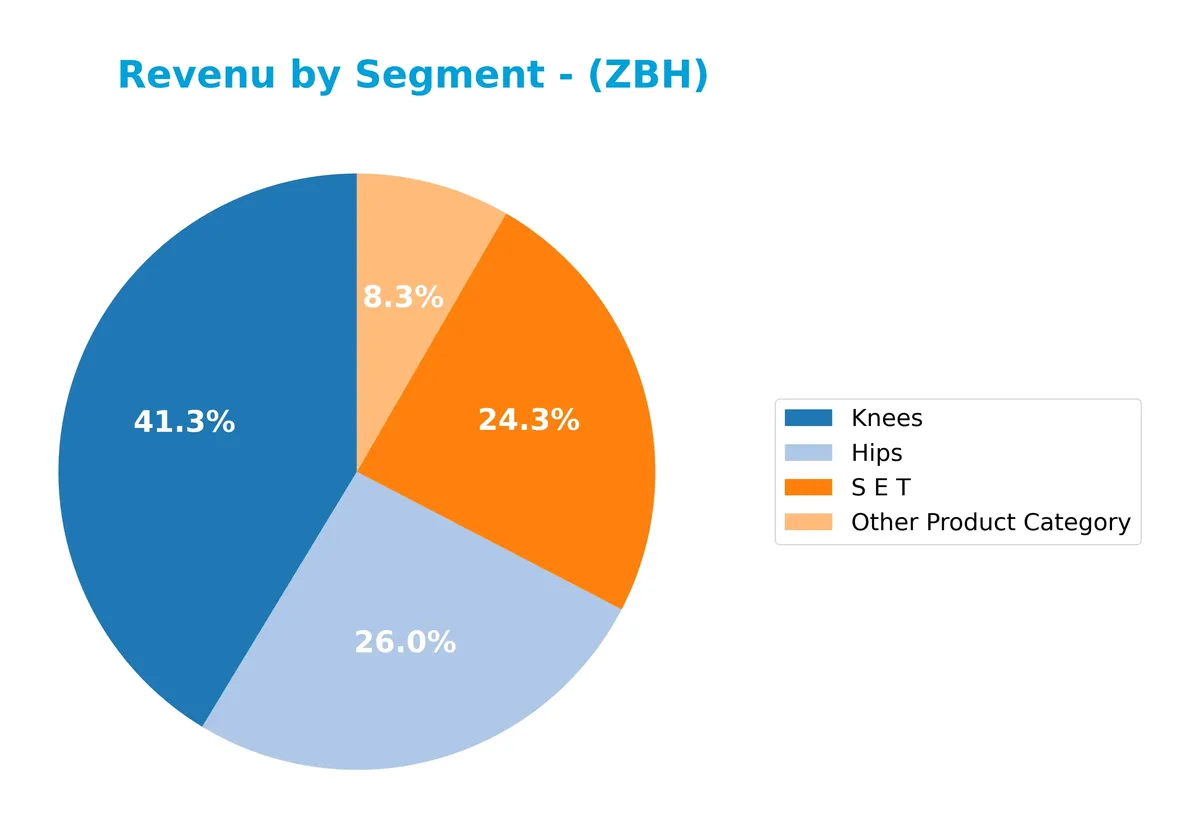

Revenue by Segment

The pie chart presents Zimmer Biomet Holdings, Inc.’s revenue distribution by product segments for the fiscal year 2025, showing the relative contribution of Hips, Knees, and S E T.

In 2025, Knees dominate Zimmer Biomet’s revenue at 3.3B, followed by S E T at 2.15B, and Hips at 2.09B. The steady growth in Knees and S E T reflects strong demand and product innovation. Hips also show a consistent rise. This concentration emphasizes orthopedic implants as the core business, with no segment showing alarming volatility or risk concentration in the latest year.

Key Products & Brands

Zimmer Biomet’s key products and brands focus on musculoskeletal healthcare solutions, spanning multiple specialized categories:

| Product | Description |

|---|---|

| Hips | Orthopaedic reconstructive products designed for hip joint repair and replacement. |

| Knees | Orthopaedic reconstructive products focused on knee joint repair and replacement. |

| S E T | Sports medicine, biologics, foot and ankle, extremities, and trauma products. |

| Other Product Category | Includes spine products, face and skull reconstruction, chest fixation, dental implants, surgical instruments, robotics, and bone cement. |

Zimmer Biomet offers a diversified portfolio centered on orthopaedic and reconstructive devices. Its products serve surgeons and healthcare providers treating bone and joint disorders worldwide.

Main Competitors

Zimmer Biomet Holdings, Inc. faces 10 main competitors in the Medical Devices industry. Here are the top 10 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| Abbott Laboratories | 216B |

| Boston Scientific Corporation | 140B |

| Stryker Corporation | 133B |

| Medtronic plc | 123B |

| Edwards Lifesciences Corporation | 50B |

| DexCom, Inc. | 26B |

| STERIS plc | 25B |

| Insulet Corporation | 20B |

| Zimmer Biomet Holdings, Inc. | 18B |

| Align Technology, Inc. | 11B |

Zimmer Biomet ranks 9th among its peers with a market cap just 9.05% that of Abbott Laboratories, the sector leader. The company sits below both the average market cap of the top 10 (76B) and the sector median (38B). It maintains a narrow 1.7% gap above its closest competitor, Insulet Corporation.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does ZBH have a competitive advantage?

Zimmer Biomet Holdings shows a slightly unfavorable moat as its ROIC falls below WACC, indicating value destruction despite improving profitability. This suggests challenges in sustaining long-term economic profits.

The company’s broad product range and geographic presence across the Americas, EMEA, and Asia Pacific create growth opportunities. Continued expansion into new markets and product innovation offer potential to strengthen its competitive position.

SWOT Analysis

This SWOT analysis identifies Zimmer Biomet Holdings, Inc.’s key strategic factors to guide investment decisions.

Strengths

- strong global presence with diversified regional revenue

- favorable gross and EBIT margins (61.6%, 13.7%)

- robust long-term revenue and net income growth

Weaknesses

- recent declines in gross profit and net margin growth

- ROE at 5.55% below industry standards

- slight value destruction indicated by ROIC below WACC

Opportunities

- expanding demand in Asia Pacific and EMEA markets

- growth potential in robotic and surgical solutions

- aging populations driving orthopedic device need

Threats

- intense competition in medical devices sector

- pricing pressure impacting margins

- regulatory and reimbursement risks in key markets

Zimmer Biomet’s solid fundamentals and geographic reach provide a strong base. However, recent profitability erosion and ROE weakness require strategic focus on innovation and operational efficiency.

Stock Price Action Analysis

The upcoming weekly chart illustrates Zimmer Biomet Holdings, Inc.’s stock price movement over the past 12 months, highlighting key fluctuations and trend shifts:

Trend Analysis

Over the past 12 months, ZBH’s stock declined by 25.18%, confirming a bearish trend with accelerating downside momentum. The price ranged from a high of 131.98 to a low of 86.6, exhibiting significant volatility with a standard deviation of 9.56. A recent 2.5-month period shows a modest 4.74% recovery.

Volume Analysis

Trading volumes over the last three months show a slight seller dominance, with buyer volume at 48.18%. Volume is increasing overall, indicating heightened market participation despite neutral buyer behavior. This suggests cautious sentiment with no clear conviction shift among investors.

Target Prices

Analysts set a target price consensus that reflects moderate upside potential for Zimmer Biomet Holdings, Inc.

| Target Low | Target High | Consensus |

|---|---|---|

| 89 | 130 | 107.82 |

The target range suggests cautious optimism, with the average price pointing to a roughly 10-15% gain from current levels. This outlook aligns with sector recovery trends but warrants monitoring for execution risks.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section reviews Zimmer Biomet Holdings, Inc.’s analyst ratings and consumer feedback to gauge market sentiment.

Stock Grades

Here are the latest verified analyst grades for Zimmer Biomet Holdings, Inc., reflecting recent recommendations and revisions:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Barclays | Maintain | Underweight | 2026-02-12 |

| Citigroup | Maintain | Neutral | 2026-02-11 |

| Wells Fargo | Maintain | Equal Weight | 2026-02-11 |

| Needham | Maintain | Hold | 2026-02-10 |

| BTIG | Maintain | Buy | 2026-02-10 |

| UBS | Maintain | Sell | 2026-01-28 |

| Bernstein | Maintain | Market Perform | 2026-01-09 |

| BTIG | Maintain | Buy | 2026-01-08 |

| Evercore ISI Group | Upgrade | Outperform | 2026-01-05 |

| Baird | Downgrade | Neutral | 2025-12-16 |

The consensus trend shows a balanced mix of Buy and Hold ratings, with a few Sell assessments. Upgrades and downgrades suggest ongoing debate about Zimmer Biomet’s near-term prospects.

Consumer Opinions

Zimmer Biomet Holdings, Inc. sparks strong reactions from its customers, reflecting its critical role in medical devices.

| Positive Reviews | Negative Reviews |

|---|---|

| High-quality implants with excellent durability. | Customer service response times can be slow. |

| Products improve patient mobility significantly. | Some pricing concerns for smaller practices. |

| Reliable and innovative surgical solutions. | Occasional delays in product delivery. |

Overall, consumers praise Zimmer Biomet for durable, effective implants and innovative solutions. However, service speed and pricing remain common concerns, suggesting room for operational improvements.

Risk Analysis

Below is a summary table outlining the key risks facing Zimmer Biomet Holdings, Inc., including their likelihood and potential impact:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Financial Health | Altman Z-score in grey zone (1.80) signals moderate bankruptcy risk amid mixed profitability. | Medium | High |

| Valuation | Elevated P/E ratio (25.25) suggests possible overvaluation relative to sector benchmarks. | Medium | Medium |

| Operational | Low asset turnover (0.36) indicates inefficiencies in using assets to generate sales. | Medium | Medium |

| Leverage | Debt-to-equity ratio (0.59) is neutral but combined with moderate interest coverage (3.84). | Medium | Medium |

| Market Volatility | Beta of 0.61 implies lower sensitivity to market swings but potential lag in bull markets. | Low | Low |

The most pressing risk stems from Zimmer Biomet’s Altman Z-score hovering just above distress territory, signaling potential financial strain. Coupled with a relatively high P/E ratio, this raises concerns about valuation and future earnings sustainability. Operational inefficiencies and moderate leverage require close monitoring amid evolving healthcare demands in 2026.

Should You Buy Zimmer Biomet Holdings, Inc.?

Zimmer Biomet appears to exhibit improving profitability amid a slightly unfavorable moat, suggesting value destruction despite rising returns. Its leverage profile could be seen as substantial, with a moderate overall rating of B+ reflecting a cautious yet potentially rewarding financial position.

Strength & Efficiency Pillars

Zimmer Biomet Holdings, Inc. shows operational resilience with a gross margin of 61.62% and a net margin of 8.57%, both favorable metrics. The company maintains a neutral ROIC of 5.48% closely aligned with its WACC of 5.59%, indicating it currently neither creates nor destroys significant value. Despite shedding value relative to capital costs, Zimmer Biomet’s growing ROIC trend (+54%) suggests improving profitability. Its Piotroski score of 7 confirms strong financial health in profitability and efficiency measures.

Weaknesses and Drawbacks

Zimmer Biomet sits in the Altman Z-Score grey zone at 1.80, signaling moderate bankruptcy risk. This caution tempers the otherwise favorable operational metrics. Its price-to-earnings ratio of 25.25 is elevated, implying a premium valuation that could limit upside. Debt-to-equity stands at 0.59, a neutral leverage level but requiring close monitoring. Recent bearish price trends (-25.18% over one year) and seller dominance (51.82% buyers overall but only 48.18% recently) add short-term market pressure and volatility risks.

Our Final Verdict about Zimmer Biomet Holdings, Inc.

Zimmer Biomet’s profile may appear cautiously optimistic. Despite moderate solvency concerns reflected by its Altman Z-Score in the grey zone, improving profitability and a strong Piotroski score suggest operational strength. However, recent bearish momentum and valuation premiums might warrant a wait-and-see approach for a more favorable entry. The company could offer potential upside but remains exposed to financial and market uncertainties.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Decoding Zimmer Biomet Holdings Inc (ZBH): A Strategic SWOT Insi – GuruFocus (Feb 21, 2026)

- There May Be Reason For Hope In Zimmer Biomet Holdings’ (NYSE:ZBH) Disappointing Earnings – Yahoo Finance (Feb 17, 2026)

- ZBH Investor Alert: Hagens Berman Investigates Zimmer Biomet (ZBH) Over Alleged Emerging Market Failures and “Inconsistent” Execution – PR Newswire (Feb 18, 2026)

- Vanguard Group Inc. Acquires 39,929 Shares of Zimmer Biomet Holdings, Inc. $ZBH – MarketBeat (Feb 20, 2026)

- 3 Reasons to Avoid ZBH and 1 Stock to Buy Instead – Finviz (Feb 19, 2026)

For more information about Zimmer Biomet Holdings, Inc., please visit the official website: zimmerbiomet.com