Home > Analyses > Healthcare > West Pharmaceutical Services, Inc.

West Pharmaceutical Services, Inc. revolutionizes how injectable drugs reach patients safely and effectively. It dominates the medical instruments sector with innovative containment and delivery solutions, including advanced stoppers, seals, and self-injection devices. Renowned for quality and cutting-edge technology, West supports pharmaceutical giants globally. As healthcare demands evolve, I explore whether West’s solid fundamentals still justify its premium valuation and growth prospects in this competitive landscape.

Table of contents

Business Model & Company Overview

West Pharmaceutical Services, Inc., founded in 1923 and headquartered in Exton, Pennsylvania, dominates the medical instruments and supplies sector. It delivers a cohesive ecosystem of containment and delivery systems for injectable drugs, integrating stoppers, seals, and advanced administration technologies. This focus on injectable drug safety and precision forms the core of its competitive edge across global healthcare markets.

The company’s revenue engine balances proprietary products with contract-manufactured devices, serving pharmaceutical and medical device firms worldwide. Its footprint spans the Americas, Europe, the Middle East, Africa, and Asia Pacific. West’s economic moat lies in its integrated solutions—combining high-quality components with regulatory expertise and after-sales support—making it a cornerstone in shaping the future of injectable drug delivery.

Financial Performance & Fundamental Metrics

I analyze West Pharmaceutical Services, Inc.’s income statement, key financial ratios, and dividend payout policy to assess its core financial health and shareholder value.

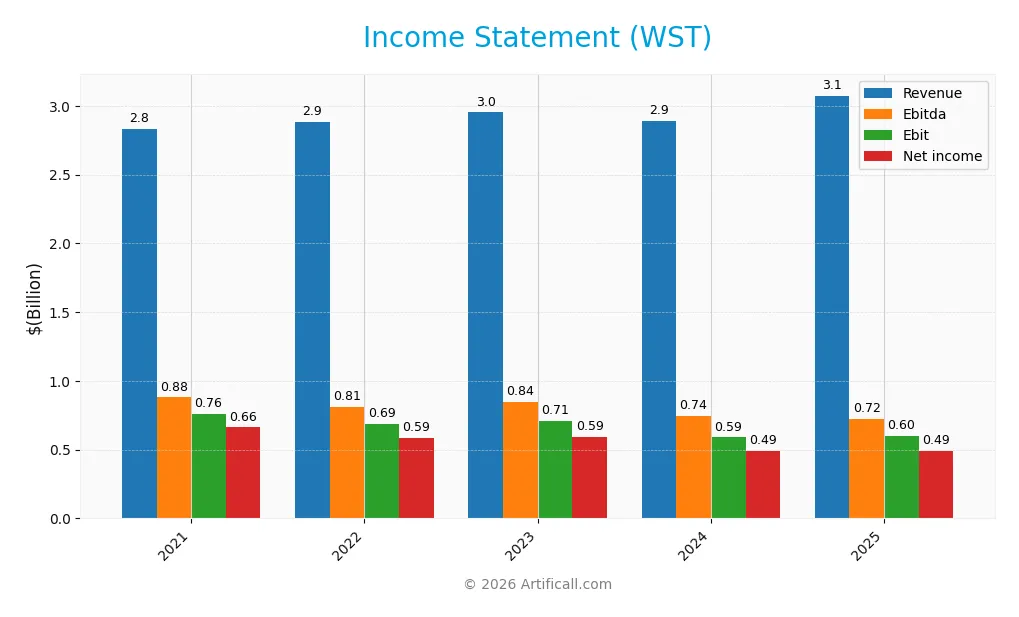

Income Statement

The table below presents West Pharmaceutical Services, Inc.’s key income statement figures for fiscal years 2021 through 2025 in USD.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 2.83B | 2.89B | 2.95B | 2.89B | 3.07B |

| Cost of Revenue | 1.66B | 1.75B | 1.82B | 1.89B | 1.97B |

| Operating Expenses | 415M | 375M | 422M | 408M | 486M |

| Gross Profit | 1.17B | 1.14B | 1.13B | 1.00B | 1.10B |

| EBITDA | 880M | 808M | 844M | 744M | 724M |

| EBIT | 757M | 688M | 707M | 588M | 599M |

| Interest Expense | 8.5M | 7.6M | 8.8M | 2.9M | 0.6M |

| Net Income | 662M | 586M | 593M | 493M | 494M |

| EPS | 8.90 | 7.88 | 7.99 | 6.75 | 6.83 |

| Filing Date | 2022-02-22 | 2023-02-21 | 2024-02-20 | 2025-02-18 | 2026-02-17 |

Income Statement Evolution

West Pharmaceutical Services reported steady revenue growth from 2021 to 2025, rising 8.6% overall. Net income, however, declined sharply by 25.4% in the same period. Margins show mixed trends: gross margin remained favorable at 35.9%, while net margin contracted by over 31%, signaling margin pressure despite revenue gains.

Is the Income Statement Favorable?

In 2025, West posted $3.07B revenue, up 6.3% year-over-year, with gross profit growing 10.1%. Operating expenses grew at the same pace as revenue, slightly eroding EBIT growth to 1.8%. The net margin slipped 5.7% to 16.1%, reflecting rising costs despite minimal interest expense. Overall, fundamentals appear favorable, supported by strong gross and EBIT margins, but margin compression warrants caution.

Financial Ratios

The following table presents key financial ratios for West Pharmaceutical Services, Inc. over the last five fiscal years:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 23% | 20% | 20% | 17% | 16% |

| ROE | 28% | 22% | 21% | 18% | 16% |

| ROIC | 24% | 20% | 18% | 16% | 14% |

| P/E | 53 | 30 | 44 | 49 | 40 |

| P/B | 15 | 7 | 9 | 9 | 6 |

| Current Ratio | 2.9 | 3.7 | 2.9 | 2.8 | 3.0 |

| Quick Ratio | 2.3 | 2.9 | 2.2 | 2.1 | 2.3 |

| D/E | 0.14 | 0.12 | 0.11 | 0.11 | 0.13 |

| Debt-to-Assets | 10% | 9% | 8% | 8% | 10% |

| Interest Coverage | 89 | 100 | 81 | 205 | 1029 |

| Asset Turnover | 0.85 | 0.80 | 0.77 | 0.79 | 0.72 |

| Fixed Asset Turnover | 2.51 | 2.29 | 1.95 | 1.72 | 0 |

| Dividend Yield | 0.15% | 0.31% | 0.22% | 0.25% | 0.31% |

Evolution of Financial Ratios

West Pharmaceutical’s Return on Equity (ROE) declined from 28.3% in 2021 to 15.5% in 2025, indicating reduced profitability. The Current Ratio fluctuated but remained above 2.7, peaking at 3.7 in 2022 and settling at 3.0 in 2025, suggesting stable liquidity. Debt-to-Equity remained low and stable, near 0.13, reflecting consistent conservative leverage.

Are the Financial Ratios Fovorable?

In 2025, West Pharmaceutical shows favorable profitability with a 16.1% net margin and 15.5% ROE, outperforming average sector returns. Liquidity ratios present mixed signals: a strong quick ratio (2.34) but an unfavorable current ratio (3.02) possibly due to high inventory levels. Leverage is low and favorable at 0.13 debt-to-equity. Market valuation ratios like P/E (40.3) and P/B (6.26) appear stretched, posing valuation concerns. Overall, the financial ratios are slightly favorable with prudent leverage and solid profitability tempered by valuation and liquidity nuances.

Shareholder Return Policy

West Pharmaceutical Services, Inc. pays dividends with a payout ratio around 12%, and dividend per share has steadily increased to $0.85 in 2025. The annual dividend yield remains low, near 0.3%, while share buybacks complement distributions, supported by strong free cash flow coverage.

This measured approach balances returning capital with reinvestment, aiming for sustainable long-term value. The moderate payout ratio and free cash flow backing reduce risk of unsustainable payouts, while buybacks provide flexibility to enhance shareholder returns without excessive leverage.

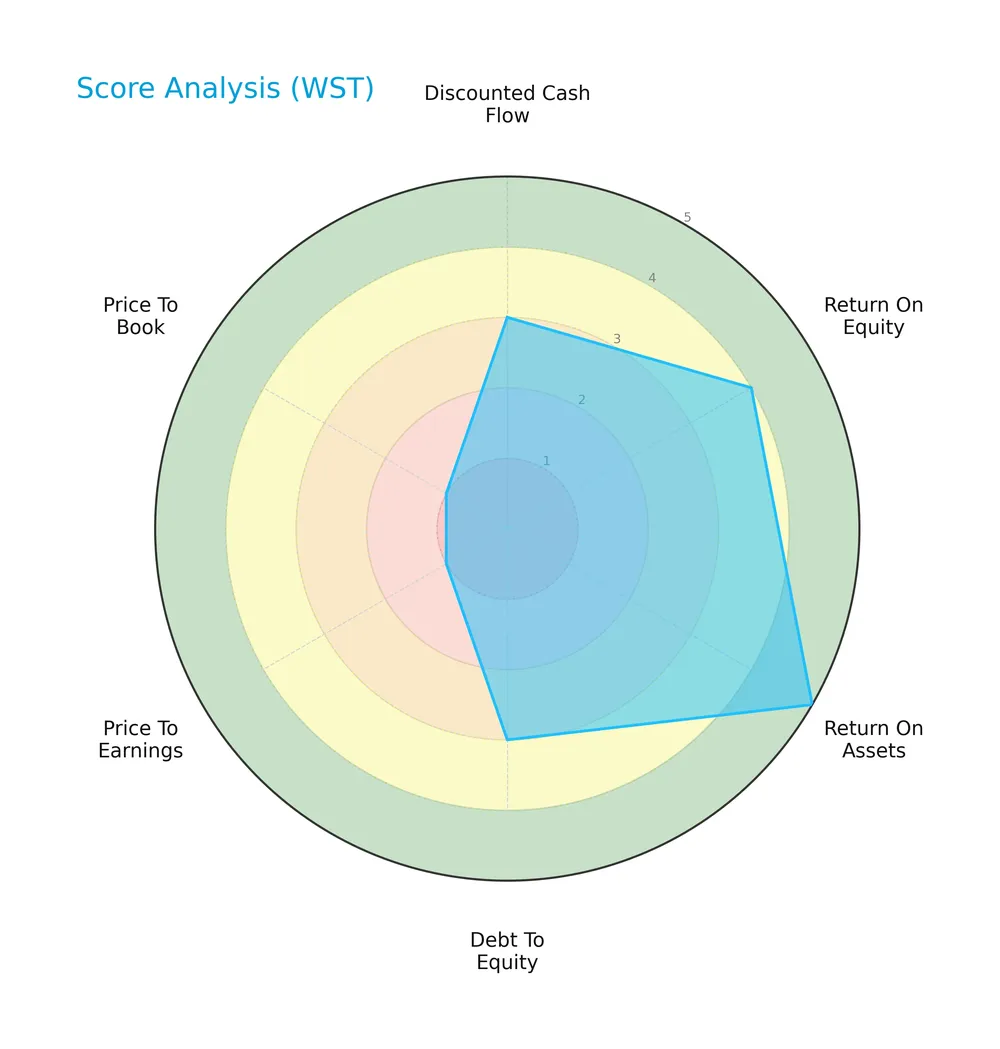

Score analysis

Here is a detailed view of West Pharmaceutical Services’ key financial scores represented in the radar chart:

West Pharmaceutical Services scores moderately on DCF and debt-to-equity, with favorable ROE and very favorable ROA. However, valuation metrics like P/E and P/B are very unfavorable, indicating potential market pricing concerns.

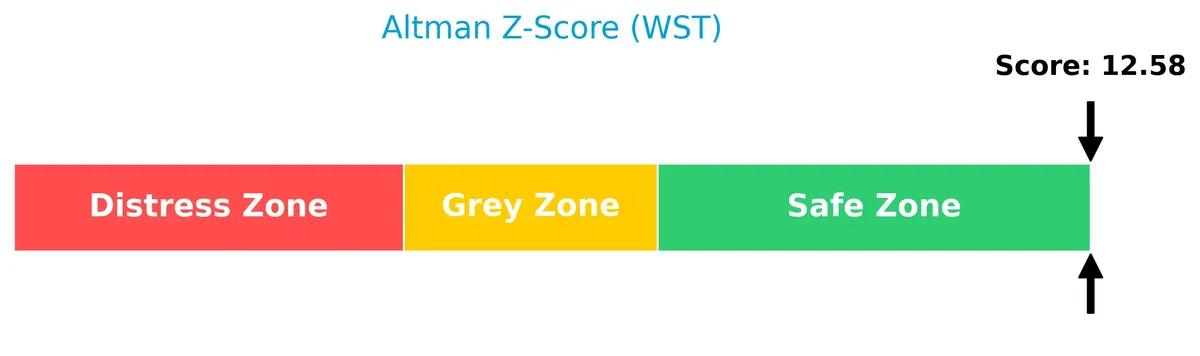

Analysis of the company’s bankruptcy risk

West Pharmaceutical Services’ Altman Z-Score places it well within the safe zone, signaling a very low bankruptcy risk:

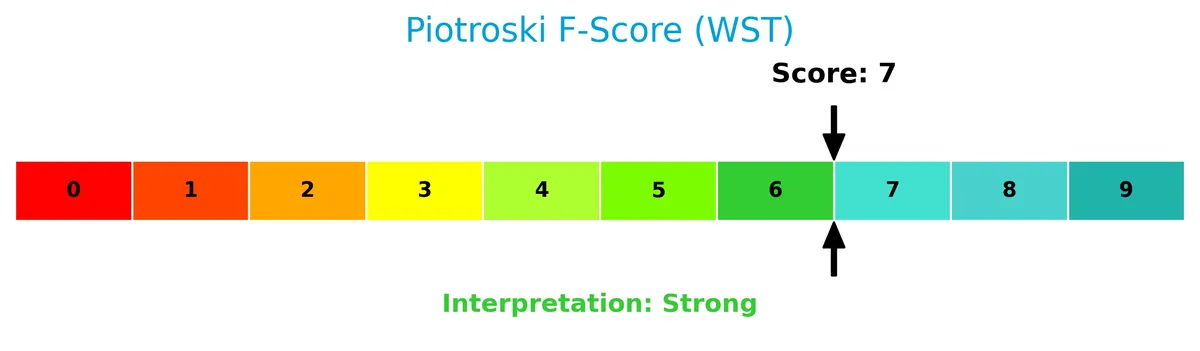

Is the company in good financial health?

The Piotroski Score diagram highlights West Pharmaceutical Services’ strong financial condition based on nine key criteria:

A score of 7 reflects strong financial health, suggesting robust profitability, liquidity, and operational efficiency, positioning the company favorably relative to peers.

Competitive Landscape & Sector Positioning

This section examines West Pharmaceutical Services, Inc.’s strategic positioning and revenue breakdown within the medical instruments sector. I will analyze its key products and main competitors. I also aim to assess whether West holds a competitive advantage over its rivals.

Strategic Positioning

West Pharmaceutical Services maintains a concentrated product portfolio focused on proprietary injectable drug packaging and contract-manufactured delivery systems. Its geographic exposure spans the Americas, Europe, Middle East, Africa, and Asia Pacific, with the U.S. generating the largest revenue share, followed by diverse European markets.

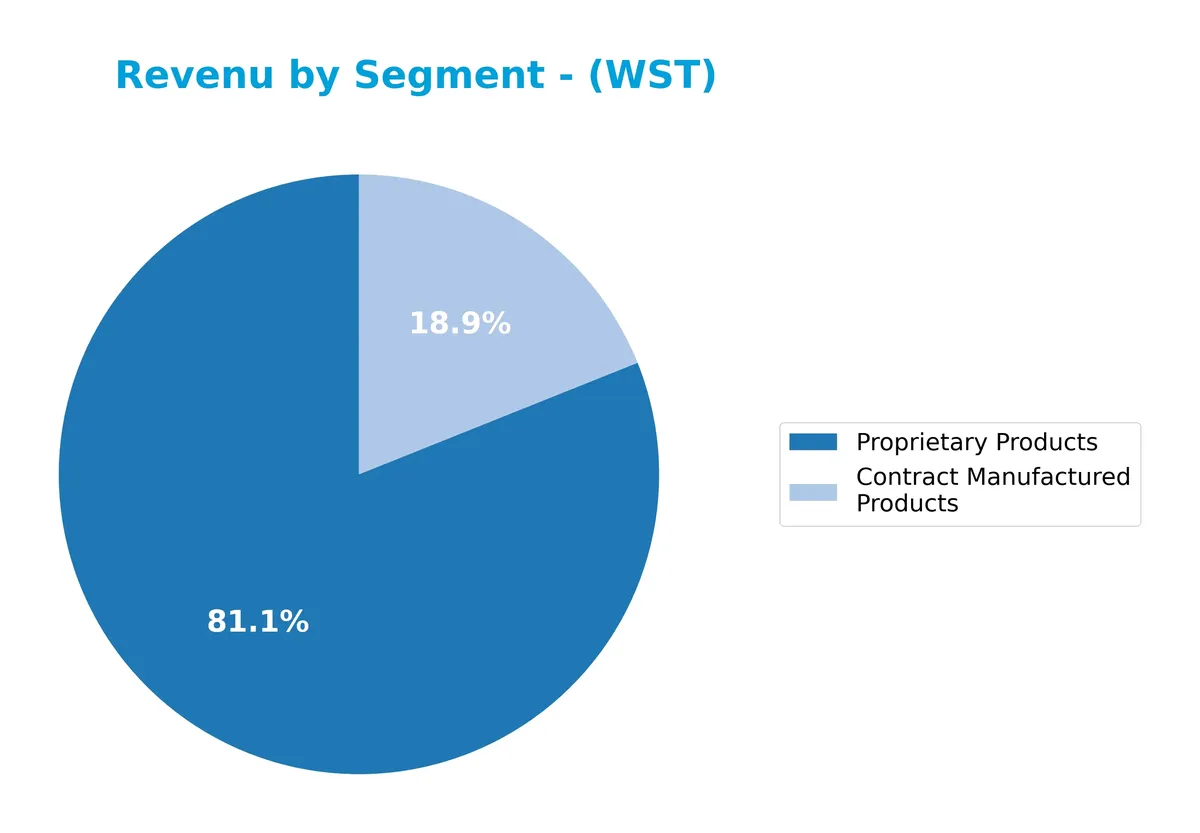

Revenue by Segment

This pie chart displays West Pharmaceutical Services, Inc.’s revenue breakdown by segment for the fiscal year 2025, highlighting the relative contribution of each business line.

In 2025, Proprietary Products dominate with $2.5B, reflecting steady growth since 2021. Contract Manufactured Products contribute $582M, showing a consistent but slower increase. The business increasingly relies on Proprietary Products, indicating concentration risk, but also a strong moat in innovative offerings. Contract Manufacturing remains a stable secondary revenue source, supporting diversification. The trend suggests acceleration in proprietary innovation driving revenue expansion.

Key Products & Brands

The following table presents West Pharmaceutical Services’ main product lines and brand descriptions:

| Product | Description |

|---|---|

| Proprietary Products | Stoppers, seals, syringe and cartridge components, administration systems, films, coatings, and drug containment solutions. |

| Contract Manufactured Products | Design, manufacture, and assembly of devices for surgical, diagnostic, ophthalmic, injectable, and other drug delivery systems. |

West Pharmaceutical Services focuses on proprietary components for injectable drug packaging and contract manufacturing of medical devices. Proprietary Products generate a substantially larger revenue share, reflecting strong specialization in containment and delivery systems.

Main Competitors

There are 8 competitors in total, with the table listing the top 8 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| Intuitive Surgical, Inc. | 201B |

| Becton, Dickinson and Company | 56B |

| ResMed Inc. | 36B |

| West Pharmaceutical Services, Inc. | 20B |

| Hologic, Inc. | 16.6B |

| The Cooper Companies, Inc. | 16.1B |

| Baxter International Inc. | 10B |

| AptarGroup, Inc. | 8.1B |

West Pharmaceutical Services, Inc. ranks 4th among its competitors. Its market cap is 8.7% of the sector leader, Intuitive Surgical, Inc. The company sits below both the average market cap of the top 10 (45.4B) and the median market cap in the sector (18.3B). It maintains a significant 105% gap above its closest competitor.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does WST have a competitive advantage?

West Pharmaceutical Services, Inc. demonstrates a competitive advantage by consistently generating returns on invested capital (ROIC) above its weighted average cost of capital (WACC), indicating value creation. However, the company’s ROIC trend is declining, signaling a reduction in profitability over recent years.

Looking ahead, West’s broad geographic footprint and diversified product segments offer growth opportunities in injectable drug delivery and advanced packaging solutions. Expansion in proprietary products and contract manufacturing across multiple regions supports a positive future outlook amid evolving healthcare demands.

SWOT Analysis

This SWOT analysis distills West Pharmaceutical Services’ strategic position by highlighting internal strengths and weaknesses alongside external opportunities and risks.

Strengths

- Strong market leadership in injectable drug containment

- Solid profitability with 16% net margin

- Low leverage with debt-to-assets under 10%

Weaknesses

- Declining ROIC trend signals weakening profitability

- High valuation multiples (PE 40.3, PB 6.3)

- Net income and EPS have declined over 5 years

Opportunities

- Growing global demand for injectable pharmaceuticals

- Expansion in emerging markets beyond US and Europe

- Innovation in drug delivery technologies and self-injection devices

Threats

- Intense competition in medical instruments sector

- Regulatory risks in healthcare markets

- Currency and geopolitical risks in global operations

West Pharmaceutical Services displays robust fundamentals and a defensible market position. However, rising valuations and profitability erosion warrant caution. Strategic focus on innovation and geographic expansion is critical to sustain growth amid sector headwinds.

Stock Price Action Analysis

The weekly stock chart of West Pharmaceutical Services, Inc. illustrates its price movement and volatility over the past 100 weeks:

Trend Analysis

Over the past 12 months, West Pharmaceutical’s stock declined by 38.54%, signaling a bearish trend. The stock reached a high of 395.71 and a low of 201.9, with decelerating downside momentum. Volatility remains elevated, evidenced by a 49.43 standard deviation.

Volume Analysis

Trading volume is increasing, with buyer and seller volumes nearly balanced at 50.02% and 49.98%, respectively. In the recent three-month period, buyers have a slight edge at 51.16%, indicating neutral buyer sentiment and stable market participation.

Target Prices

Analysts set a strong target consensus for West Pharmaceutical Services, reflecting confidence in its growth potential.

| Target Low | Target High | Consensus |

|---|---|---|

| 265 | 340 | 304.43 |

The target range suggests upside potential of 10–20% from current levels, indicating positive analyst sentiment on West’s strategic positioning.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section examines West Pharmaceutical Services, Inc.’s analyst ratings and consumer feedback to gauge market sentiment.

Stock Grades

Here is a summary of recent stock grades from reputable analysts covering West Pharmaceutical Services, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Barclays | Maintain | Equal Weight | 2026-02-13 |

| Evercore ISI Group | Maintain | Outperform | 2026-02-03 |

| Barclays | Maintain | Equal Weight | 2025-10-27 |

| Keybanc | Maintain | Overweight | 2025-10-24 |

| UBS | Maintain | Buy | 2025-10-24 |

| Evercore ISI Group | Maintain | Outperform | 2025-10-23 |

| Barclays | Maintain | Equal Weight | 2025-10-02 |

| Evercore ISI Group | Maintain | Outperform | 2025-07-25 |

| UBS | Maintain | Buy | 2025-07-25 |

| Barclays | Maintain | Equal Weight | 2025-07-25 |

The grades consistently show a stable outlook with Barclays favoring a neutral stance, while Evercore ISI and UBS lean positive. The consensus remains a Buy, reflecting moderate optimism among analysts.

Consumer Opinions

Consumers express a mix of admiration and frustration toward West Pharmaceutical Services, Inc., reflecting its complex market position.

| Positive Reviews | Negative Reviews |

|---|---|

| High product quality and reliability | Price points are often higher than competitors |

| Excellent customer service and support | Delivery delays create operational headaches |

| Innovative packaging solutions that enhance product safety | Limited customization options in some product lines |

Overall, consumers consistently praise West’s product quality and customer service. However, pricing and delivery issues emerge as common concerns, signaling areas for operational improvements.

Risk Analysis

Below is a summary table of key risks facing West Pharmaceutical Services, Inc. as of 2026:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Valuation Risk | Elevated P/E of 40.3 and P/B of 6.26 signal potential overvaluation relative to sector norms. | High | High |

| Market Volatility | Beta at 1.19 indicates stock price moves more than the market, increasing downside risk. | Medium | Medium |

| Operational Risk | Zero fixed asset turnover suggests potential inefficiencies in asset utilization. | Medium | Medium |

| Dividend Risk | Low dividend yield of 0.31% may deter income-focused investors amid market alternatives. | Medium | Low |

| Leverage Risk | Low debt-to-equity ratio (0.13) and strong interest coverage reduce financial distress risk. | Low | Low |

The most significant risks stem from valuation concerns and market volatility. West’s high price multiples make it vulnerable to multiple contraction if growth slows. The beta above 1 reflects amplified sensitivity to market swings, demanding cautious position sizing. Encouragingly, the company’s strong balance sheet and safe Altman Z-score mitigate bankruptcy risk. However, the lack of fixed asset utilization efficiency warrants monitoring.

Should You Buy West Pharmaceutical Services, Inc.?

West Pharmaceutical Services, Inc. appears to be a profitable company with a slightly favorable competitive moat, indicated by value creation despite declining ROIC. Its debt profile is manageable, supported by strong liquidity ratios. Overall, it suggests a solid B rating with moderate risks to consider.

Strength & Efficiency Pillars

West Pharmaceutical Services, Inc. posts a robust net margin of 16.06% and a return on equity of 15.54%, signaling solid profitability. Its return on invested capital (ROIC) stands at 13.53%, comfortably above the weighted average cost of capital (WACC) at 9.1%, confirming the company as a value creator. The interest expense is negligible at 0.02%, and a strong Piotroski score of 7 supports operational strength. Despite a declining ROIC trend, the firm maintains efficiency and value creation in a challenging sector.

Weaknesses and Drawbacks

Valuation metrics present concerns: a high price-to-earnings ratio of 40.29 and price-to-book ratio of 6.26 suggest an expensive equity relative to earnings and book value. The current ratio at 3.02, though seemingly strong, is flagged unfavorable here due to potential liquidity management issues in context. Dividend yield is low at 0.31%, limiting income appeal. The bearish overall stock trend with a -38.54% price change and decelerating momentum signals market pressure and investor caution.

Our Final Verdict about West Pharmaceutical Services, Inc.

West Pharmaceutical Services may appear attractive for long-term exposure given its value-creating profile and operational strength. However, the bearish price trend and elevated valuation ratios suggest a wait-and-see approach to identify a more favorable entry point. The financial health is solid with an Altman Z-Score of 12.58 in the safe zone, mitigating solvency risks but not eliminating short-term market headwinds.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- West Announces Quarterly Dividend and Share Repurchase Program – PR Newswire (Feb 17, 2026)

- Why West Pharmaceutical Services (WST) is a Top Growth Stock for the Long-Term – Yahoo Finance (Feb 17, 2026)

- West Pharmaceutical announces up to $1B share repurchase program – MSN (Feb 17, 2026)

- West Pharmaceutical clears $1B for stock buybacks and a May dividend – Stock Titan (Feb 17, 2026)

- West Pharmaceutical Services, Inc. Declares Regular Quarterly Dividend on Common Stock, Payable on May 6, 2026 – marketscreener.com (Feb 17, 2026)

For more information about West Pharmaceutical Services, Inc., please visit the official website: westpharma.com