Home > Analyses > Energy > Valero Energy Corporation

Valero Energy powers millions of vehicles daily, shaping global transportation and energy markets. It commands industry leadership with 15 refineries and a robust portfolio spanning conventional fuels, renewable diesel, and ethanol. Known for operational excellence and innovation, Valero balances traditional energy with cleaner solutions. As energy dynamics evolve, I question whether Valero’s strong asset base and diversified segments still justify its current valuation and growth outlook.

Table of contents

Business Model & Company Overview

Valero Energy Corporation, founded in 1980 and headquartered in San Antonio, Texas, stands as a leading force in Oil & Gas Refining & Marketing. With a portfolio that integrates refining, renewable diesel, and ethanol production, Valero delivers a cohesive energy ecosystem. The company operates 15 refineries and 12 ethanol plants, positioning itself as a dominant supplier of transportation fuels and petrochemicals across North America and beyond.

Valero’s revenue engine balances conventional fuels with growing renewable segments, leveraging its extensive logistics network to serve wholesale and retail markets under multiple brands. Its footprint spans the Americas, Europe, and Asia, reinforcing a robust global presence. The company’s economic moat lies in its integrated refining capacity and diversified product mix, securing its role as a pivotal energy provider shaping the industry’s future.

Financial Performance & Fundamental Metrics

I analyze Valero Energy Corporation’s income statement, key financial ratios, and dividend payout policy to assess its operational efficiency and shareholder value.

Income Statement

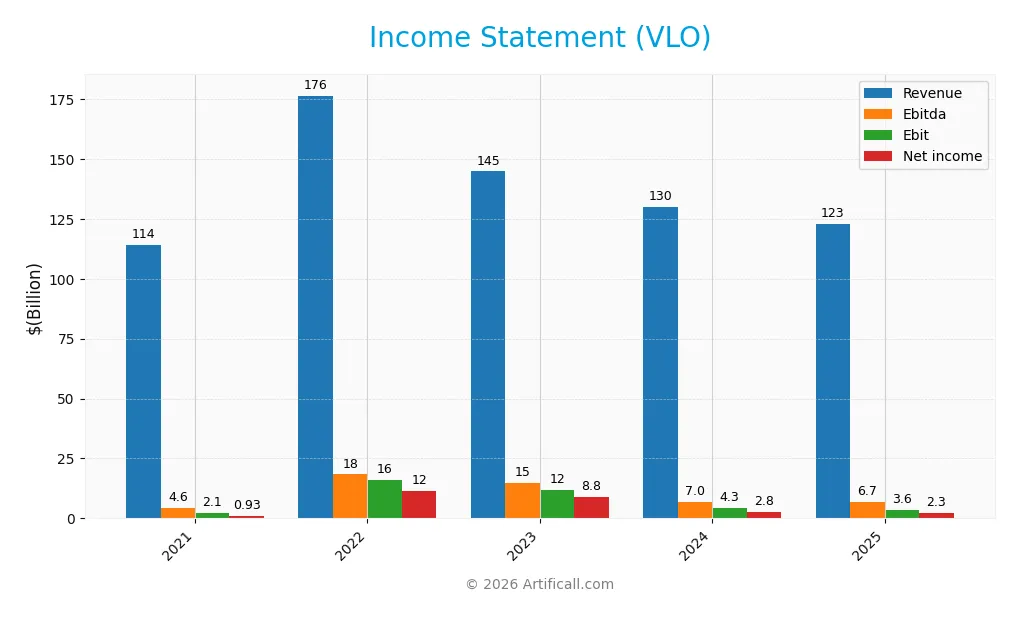

The table below presents Valero Energy Corporation’s key income statement figures for fiscal years 2021 through 2025, reflecting revenue, expenses, profits, and earnings per share.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 114B | 176B | 145B | 130B | 123B |

| Cost of Revenue | 111B | 160B | 132B | 125B | 117B |

| Operating Expenses | 952M | 1.06B | 1.03B | 1.01B | 1.06B |

| Gross Profit | 3.08B | 16.75B | 12.89B | 4.76B | 5.37B |

| EBITDA | 4.55B | 18.34B | 14.66B | 7.03B | 6.72B |

| EBIT | 2.15B | 15.87B | 11.96B | 4.25B | 3.56B |

| Interest Expense | 603M | 562M | 592M | 556M | 556M |

| Net Income | 930M | 11.53B | 8.81B | 2.77B | 2.35B |

| EPS | 2.27 | 29.08 | 24.95 | 8.58 | 7.57 |

| Filing Date | 2022-02-22 | 2023-02-23 | 2024-02-22 | 2025-02-26 | 2026-02-25 |

Income Statement Evolution

Valero’s revenue declined by 5.5% in 2025, reversing prior growth. Despite this, gross profit increased 12.8%, signaling margin improvement. Net income fell 10.3%, reflecting pressure on profitability. Margins remained stable overall, with a gross margin near 4.4% and a net margin around 1.9%, indicating consistent operational efficiency amid revenue fluctuations.

Is the Income Statement Favorable?

In 2025, Valero reported $123B revenue and $2.35B net income, with EPS at $7.57. Operating expenses and interest costs remained well controlled, supporting a favorable interest expense ratio of 0.45%. However, declines in revenue, EBIT (-16.3%), and net margin suggest near-term challenges. The fundamentals appear neutral, balancing solid margin management against shrinking top-line and bottom-line results.

Financial Ratios

The table below summarizes key financial ratios for Valero Energy Corporation (VLO) over the last five fiscal years, providing insight into profitability, leverage, liquidity, valuation, and efficiency:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 0.82% | 6.54% | 6.10% | 2.13% | 1.91% |

| ROE | 5.05% | 48.93% | 33.53% | 11.30% | 9.90% |

| ROIC | 4.17% | 27.09% | 19.20% | 6.67% | 9.38% |

| P/E | 32.87 | 4.35 | 5.19 | 14.25 | 21.42 |

| P/B | 1.66 | 2.13 | 1.74 | 1.61 | 2.12 |

| Current Ratio | 1.26 | 1.38 | 1.56 | 1.53 | 3.37 |

| Quick Ratio | 0.88 | 1.00 | 1.11 | 1.03 | 2.83 |

| D/E | 0.82 | 0.54 | 0.48 | 0.47 | 0.45 |

| Debt-to-Assets | 26.13% | 20.86% | 20.04% | 19.19% | 22.35% |

| Interest Coverage | 3.53 | 27.92 | 20.03 | 6.75 | 7.76 |

| Asset Turnover | 1.97 | 2.89 | 2.30 | 2.16 | 2.58 |

| Fixed Asset Turnover | 3.55 | 5.50 | 4.62 | — | — |

| Dividend Yield | 5.24% | 3.12% | 3.16% | 3.51% | 2.79% |

Note: Fixed Asset Turnover is unavailable for 2024 and 2025.

Evolution of Financial Ratios

Return on Equity (ROE) declined sharply from 48.9% in 2022 to 9.9% in 2025, signaling lower profitability. The Current Ratio increased markedly to 3.37 in 2025, indicating improved liquidity. Meanwhile, the Debt-to-Equity Ratio decreased from 0.82 in 2021 to 0.45 in 2025, reflecting reduced leverage and a more conservative capital structure.

Are the Financial Ratios Favorable?

In 2025, profitability ratios such as net margin (1.91%) and ROE (9.9%) appear unfavorable, though ROIC (9.38%) is neutral relative to the 6.55% WACC. Liquidity shows mixed signals; the high current ratio (3.37) is unfavorable, but the quick ratio (2.83) is favorable. Leverage metrics, including debt-to-equity (0.45) and interest coverage (6.4), are favorable. Overall, half of the key ratios are favorable, suggesting a slightly favorable financial profile.

Shareholder Return Policy

Valero Energy Corporation maintains a dividend payout ratio near 60%, with a dividend per share rising steadily to $4.55 in 2025, yielding approximately 2.8%. The company supports dividends through robust free cash flow and also engages in share buybacks.

This disciplined distribution balances shareholder returns and capital needs, suggesting a sustainable approach to value creation. The payout aligns with earnings and cash flow, reducing risk of unsustainable payouts or excessive buybacks.

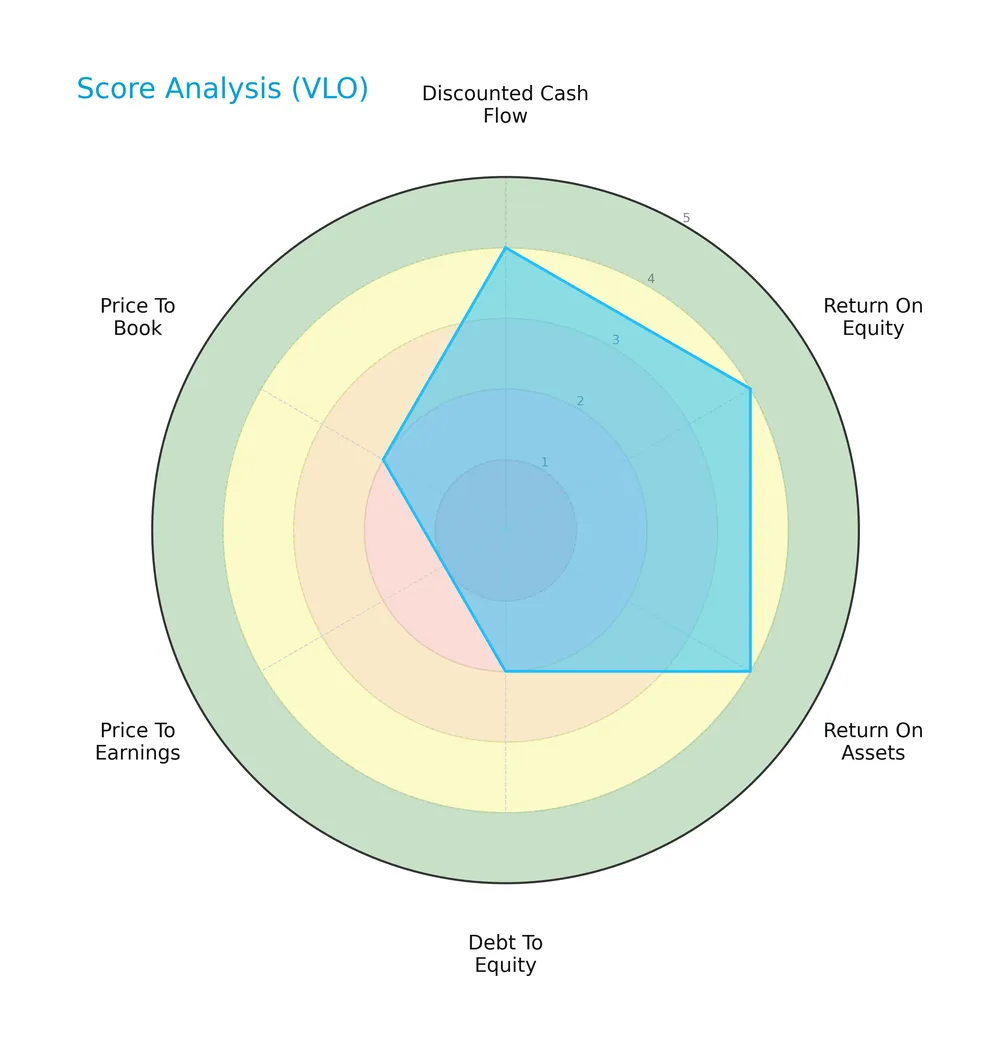

Score analysis

The radar chart below summarizes key financial scores evaluating Valero Energy Corporation’s performance and valuation metrics:

Valero scores favorably in discounted cash flow, return on equity, and return on assets, each at 4. Debt-to-equity and price-to-book ratios are unfavorable at 2, while the price-to-earnings score is very unfavorable at 1. Overall, the company presents a moderate score of 3.

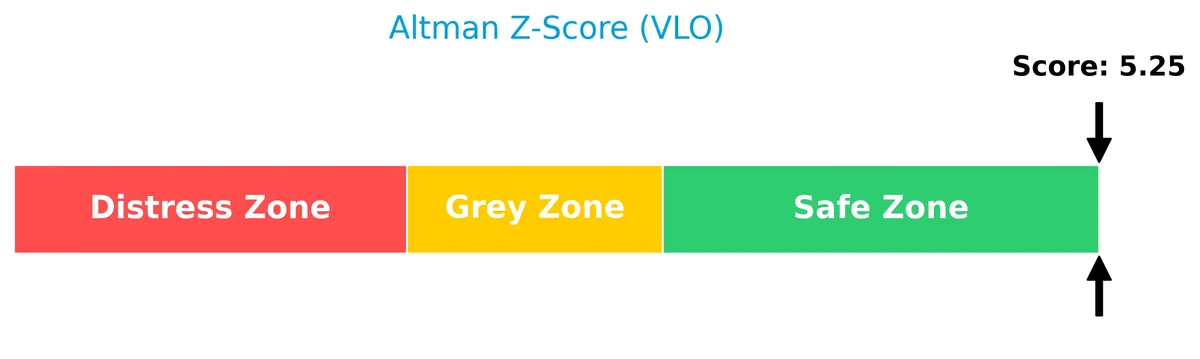

Analysis of the company’s bankruptcy risk

Valero’s Altman Z-Score places it firmly in the safe zone, indicating low bankruptcy risk and strong financial stability:

Is the company in good financial health?

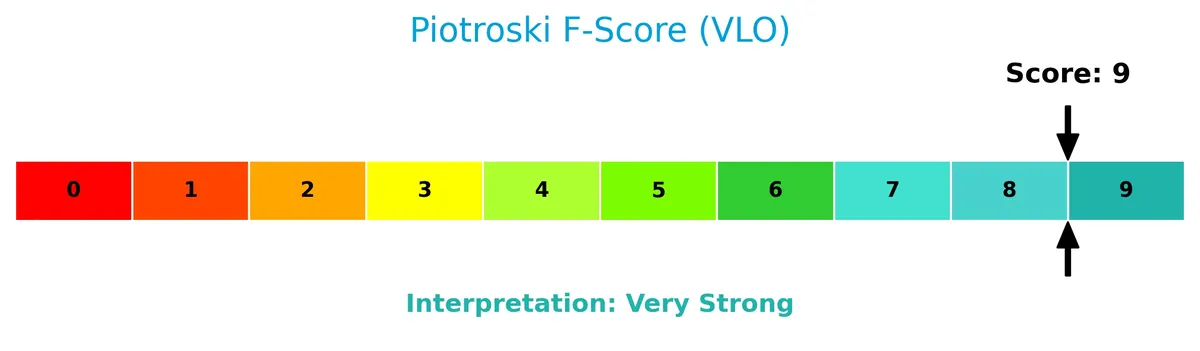

The Piotroski diagram highlights Valero’s exceptionally strong financial health with a top score:

With a Piotroski score of 9, Valero demonstrates robust profitability, efficient capital allocation, and solid balance sheet management, signaling very strong financial health.

Competitive Landscape & Sector Positioning

This analysis examines Valero Energy Corporation’s sector positioning, revenue segments, and product portfolio. I will assess its competitive advantages relative to main industry rivals.

Strategic Positioning

Valero Energy Corporation maintains a diversified product portfolio across refining, renewable diesel, and ethanol, with refining dominating revenue at $116B in 2025. Geographically, it balances exposure mainly in the US ($88B), UK/Ireland ($16B), Canada ($8B), and other countries ($5.7B), reflecting a broad international footprint.

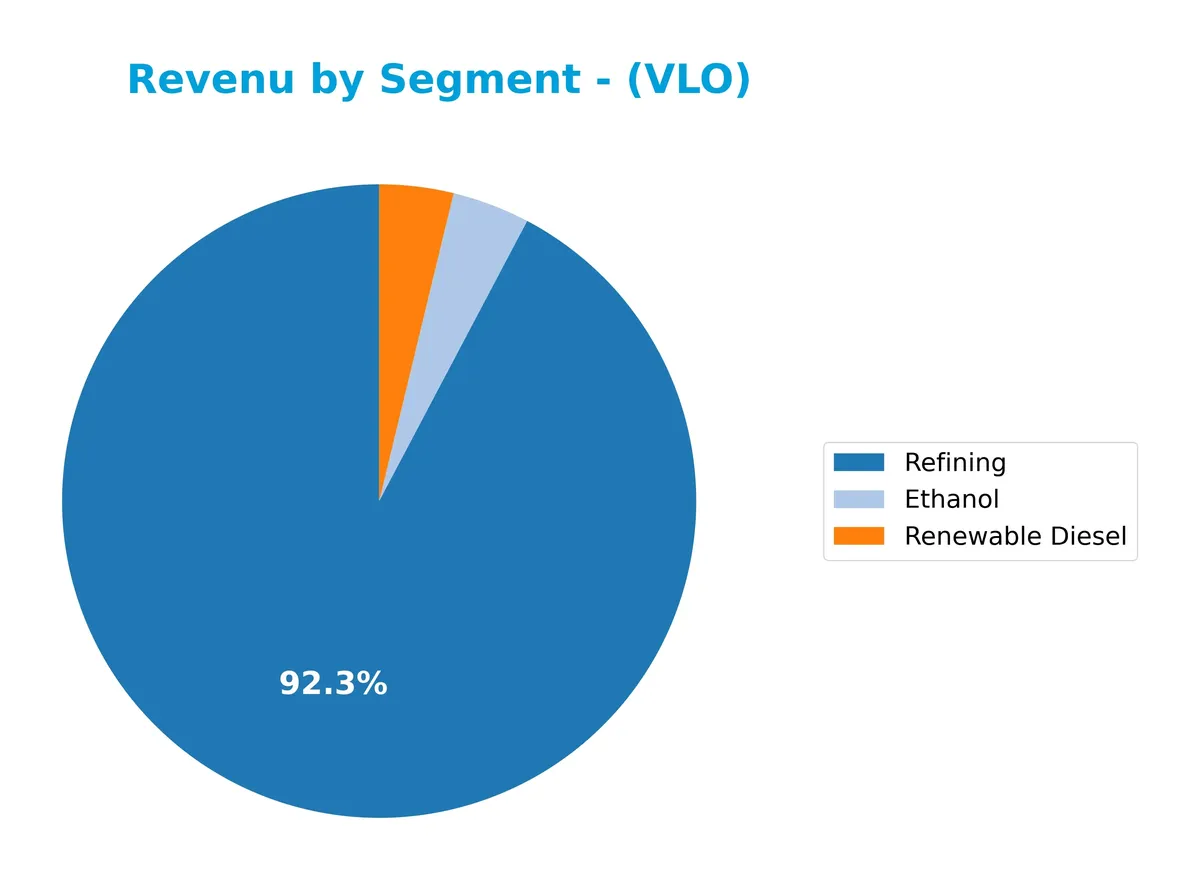

Revenue by Segment

This pie chart illustrates Valero Energy Corporation’s revenue distribution across key segments for the full fiscal year 2025, providing insight into the company’s business drivers.

Refining dominates Valero’s revenue with 116B in 2025, down from 168B in 2022, signaling a notable contraction in this core segment. Ethanol and Renewable Diesel generate 5B each, showing relative stability but limited scale compared to refining. The recent slowdown in refining revenue raises concentration risk, underscoring the need to monitor diversification efforts closely.

Key Products & Brands

The following table details Valero Energy Corporation’s main products and brands across its operations:

| Product | Description |

|---|---|

| Refining | Produces conventional, premium, reformulated gasolines, diesel fuels including CARB diesel, jet fuels, asphalts, petrochemicals, and lubricants. Operates 15 refineries with 3.2M barrels/day capacity. |

| Renewable Diesel | Processes animal fats, used cooking oils, and inedible corn oils into renewable diesel through dedicated plants. |

| Ethanol | Manufactures ethanol and co-products like dry distiller grains, syrup, and inedible corn oil mainly for animal feed. Operates 12 ethanol plants with 1.6B gallons/year capacity. |

| Retail Brands | Markets refined products via ~7,000 outlets under Valero, Beacon, Diamond Shamrock, Shamrock, Ultramar, and Texaco brands. |

| Logistics Assets | Owns and operates pipelines, terminals, tanks, marine docks, and truck rack bays supporting crude oil and refined product distribution. |

Valero’s product portfolio spans traditional and renewable fuels, leveraging a broad refining base and multiple fuel brands. Its integration into logistics and ethanol production enhances supply chain control and market reach.

Main Competitors

There are 3 competitors in the Oil & Gas Refining & Marketing industry. The table below lists the top 3 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| Phillips 66 | 52.6B |

| Valero Energy Corporation | 51.6B |

| Marathon Petroleum Corporation | 49.6B |

Valero Energy Corporation ranks 2nd among its competitors. Its market cap is about 18% smaller than the leader, Phillips 66. Valero stands above both the average market cap of the top 10 and the median market cap in the sector. It remains roughly 15% behind Phillips 66, showing a moderate gap with the closest rival.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does Valero Energy Corporation have a competitive advantage?

Valero demonstrates a clear competitive advantage, evidenced by a ROIC exceeding its WACC by 2.83%, indicating consistent value creation. Its ROIC growth of 125% over five years confirms a very favorable moat and sustained profitability.

Looking ahead, Valero’s diversified operations across refining, renewable diesel, and ethanol position it well to capture emerging market opportunities. Expansion in renewable fuels and international sales should support future growth amid evolving energy demands.

SWOT Analysis

This SWOT analysis highlights Valero Energy Corporation’s core competitive position and risks to inform strategic decisions.

Strengths

- strong refining capacity with 3.2M bpd throughput

- diversified product portfolio including renewable diesel and ethanol

- solid liquidity position with quick ratio at 2.83

Weaknesses

- recent revenue decline of 5.54%

- net margin low at 1.91%

- unfavorable trends in EBIT and EPS growth

Opportunities

- expanding renewable diesel market

- potential to increase U.S. and international market share

- rising demand for low-sulfur fuels

Threats

- volatile oil prices impacting margins

- regulatory risks in carbon emissions

- intense competition in refining sector

Valero’s strengths in scale and product diversification provide a solid base, but margin pressure and recent revenue setbacks require cautious capital allocation. Growth in renewables offers a strategic pivot to enhance resilience.

Stock Price Action Analysis

The weekly stock chart for Valero Energy Corporation (VLO) highlights price movement and volatility over the past 100 weeks:

Trend Analysis

Over the past two years, VLO’s stock price increased by 8.86%, indicating a bullish trend. The trend exhibits acceleration with a high volatility level (21.22% std deviation). The price ranged between a low of 104.69 and a high of 202.68, reflecting strong upward momentum.

Volume Analysis

Trading volume totals 1.73B shares, with buyers accounting for 54.84%. Volume has been decreasing recently, suggesting waning market participation. Buyer dominance remains neutral at 51.45% during the last three months, indicating balanced investor sentiment without clear directional conviction.

Target Prices

Analysts set a clear target consensus for Valero Energy Corporation, reflecting cautious optimism.

| Target Low | Target High | Consensus |

|---|---|---|

| 162 | 220 | 190.22 |

The target range spans from 162 to 220, with a consensus near 190, indicating moderate upside potential balanced by sector volatility.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section examines Valero Energy Corporation’s recent analyst ratings alongside consumer feedback and sentiment trends.

Stock Grades

Here is the latest consensus and individual grades for Valero Energy Corporation from established financial institutions:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Citigroup | Maintain | Neutral | 2026-02-09 |

| Morgan Stanley | Maintain | Equal Weight | 2026-01-30 |

| Piper Sandler | Maintain | Overweight | 2026-01-30 |

| Morgan Stanley | Maintain | Equal Weight | 2026-01-27 |

| Piper Sandler | Maintain | Overweight | 2026-01-08 |

| JP Morgan | Maintain | Overweight | 2026-01-08 |

| Mizuho | Downgrade | Neutral | 2025-12-12 |

| B of A Securities | Downgrade | Neutral | 2025-12-11 |

| Barclays | Maintain | Overweight | 2025-11-17 |

| Piper Sandler | Maintain | Overweight | 2025-11-14 |

The grades show a stable bias toward maintaining overweight or equal weight ratings, with some downgrades from outperform and buy to neutral in late 2025. The consensus remains a buy, reflecting moderate confidence amid cautious adjustments.

Consumer Opinions

Valero Energy Corporation’s consumer sentiment reveals a mix of appreciation and concern, reflecting its complex market position.

| Positive Reviews | Negative Reviews |

|---|---|

| Reliable fuel quality praised by frequent buyers. | Complaints about occasional price volatility. |

| Strong presence in multiple regions appreciated. | Some criticism on customer service responsiveness. |

| Efficient station locations noted for convenience. | Environmental impact concerns raised by some consumers. |

Overall, consumers value Valero for its dependable fuel and widespread accessibility. However, price fluctuations and service issues emerge as consistent pain points, alongside growing environmental scrutiny.

Risk Analysis

The following table summarizes key risks facing Valero Energy Corporation, including their likelihood and potential impact:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Market Volatility | Oil price fluctuations driven by geopolitical tensions and demand shifts | High | High |

| Regulatory Risks | Stricter environmental regulations on fossil fuels and emissions | Medium | High |

| Operational Risks | Refinery accidents or supply chain disruptions | Medium | Medium |

| Financial Risks | Debt levels and valuation concerns amid sector cyclicality | Low | Medium |

| Technological Risks | Transition to renewable energy reducing fossil fuel demand | Medium | Medium |

Valero’s strongest risk remains oil price volatility, which directly impacts margins. Recent geopolitical instability has caused sharp price swings. Regulatory pressure on carbon emissions also threatens refining profitability. While Valero’s robust Altman Z-score (5.25) confirms financial stability, its unfavorable price-to-earnings ratio warns of valuation risks. Prudence requires monitoring energy policy and market cycles closely.

Should You Buy Valero Energy Corporation?

Valero Energy Corporation appears to be delivering robust profitability and strong value creation supported by a durable competitive moat with growing ROIC. Despite an unfavorable leverage profile, its overall B rating and safe Altman Z-Score suggest a favorable financial health outlook.

Strength & Efficiency Pillars

Valero Energy Corporation delivers solid operational efficiency with a net margin of 1.91% and ROE of 9.9%, albeit both flagged as unfavorable. Crucially, its ROIC stands at 9.38%, comfortably above the WACC of 6.55%, confirming Valero as a value creator. This gap signals effective capital allocation and sustained value generation. The firm’s Piotroski score of 9 reinforces its strong financial health. Additionally, favorable metrics like a quick ratio of 2.83 and interest coverage of 6.4x indicate operational resilience.

Weaknesses and Drawbacks

Valero’s valuation metrics raise concerns; a P/E of 21.42 and P/B of 2.12 suggest a neutral to slightly rich pricing, limiting margin for error. The current ratio at 3.37, deemed unfavorable, signals potential liquidity inefficiencies despite a manageable debt-to-equity ratio of 0.45. Moreover, revenue declined by 5.54% last year, and net margin shrank by 10.26%, reflecting profitability pressures. While buyer dominance at 51.45% is neutral, decreasing volume could herald reduced market interest or liquidity risks.

Our Final Verdict about Valero Energy Corporation

Valero’s fundamentals appear attractive for long-term exposure, supported by a strong financial health profile and value-creating capital returns. The stock’s bullish overall trend and recent neutral buyer behavior suggest cautious optimism. Investors might consider Valero for portfolio inclusion, but should remain attentive to near-term market dynamics and earnings volatility. This profile suggests measured confidence rather than an outright endorsement.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Valero Energy Corporation (VLO) Is a Trending Stock: Facts to Know Before Betting on It – Yahoo Finance (Feb 25, 2026)

- Valero Energy Corporation (VLO) Is Gaining Attention: Key Information to Consider Before Investing – Bitget (Feb 25, 2026)

- X Square Capital LLC Sells 8,096 Shares of Valero Energy Corporation $VLO – MarketBeat (Feb 23, 2026)

- VALERO ENERGY CORP/TX SEC 10-K Report – TradingView (Feb 25, 2026)

- Valero Energy (VLO): A Refining Giant With Earnings Momentum and Global Reach – Insider Monkey (Feb 25, 2026)

For more information about Valero Energy Corporation, please visit the official website: valero.com