Home > Analyses > Healthcare > Universal Health Services, Inc.

Universal Health Services transforms healthcare delivery across the United States and beyond. It operates a vast network of acute care hospitals and behavioral health facilities, serving millions with critical medical and mental health services. Renowned for integrating innovation and quality, UHS stands as a pillar in medical care facilities. As healthcare demands evolve, I ask whether UHS’s operational strength and market position still justify its valuation and growth prospects in 2026.

Table of contents

Business Model & Company Overview

Universal Health Services, Inc., founded in 1978 and headquartered in King of Prussia, PA, commands a dominant position in the Medical – Care Facilities sector. With 363 inpatient and 40 outpatient facilities across 39 states, Washington, D.C., Puerto Rico, and the UK, it delivers an integrated ecosystem of acute care hospitals and behavioral health services. This network supports a wide range of medical specialties from surgery to oncology and behavioral health, reflecting a comprehensive healthcare mission.

The company’s revenue engine balances inpatient acute care and behavioral health services, supplemented by commercial health insurance and centralized management services. Its footprint spans key global markets, enabling scale efficiencies and cross-segment synergies. Universal Health Services’ extensive network and integrated offerings create a formidable economic moat, shaping the future of healthcare delivery through scale and specialization.

Financial Performance & Fundamental Metrics

I analyze Universal Health Services, Inc.’s income statement, key financial ratios, and dividend payout policy to assess its core financial health and shareholder value.

Income Statement

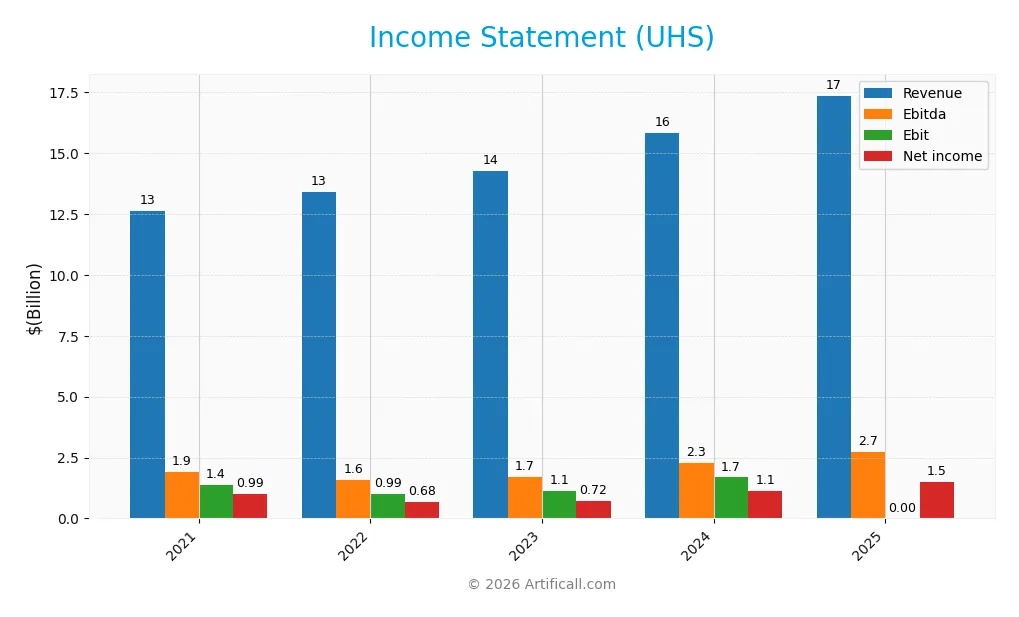

Below is the Income Statement for Universal Health Services, Inc. (UHS) covering fiscal years 2021 through 2025. The figures are reported in USD and show key profitability metrics.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 12.64B | 13.40B | 14.28B | 15.83B | 17.36B |

| Cost of Revenue | 1.43B | 1.47B | 1.53B | 1.59B | 0 |

| Operating Expenses | 9.85B | 10.92B | 11.57B | 12.56B | 0 |

| Gross Profit | 11.21B | 11.93B | 12.75B | 14.24B | 0 |

| EBITDA | 1.91B | 1.58B | 1.71B | 2.27B | 2.72B |

| EBIT | 1.38B | 993M | 1.14B | 1.68B | 0 |

| Interest Expense | 85M | 127M | 207M | 188M | 156M |

| Net Income | 992M | 676M | 718M | 1.14B | 1.49B |

| EPS | 11.99 | 9.23 | 10.35 | 17.16 | 23.42 |

| Filing Date | 2022-02-24 | 2023-02-27 | 2024-02-27 | 2025-02-26 | 2026-02-25 |

Income Statement Evolution

Universal Health Services’ revenue grew steadily from 12.6B in 2021 to 17.4B in 2025, marking a 37% rise over five years. Net income increased 50%, reaching 1.49B in 2025. Margins showed mixed trends: while net margin improved to 8.57%, gross profit and EBIT margins declined sharply in the latest year, signaling margin pressure despite top-line growth.

Is the Income Statement Favorable?

The 2025 income statement reveals favorable fundamentals overall. Revenue growth of 9.7% outpaced operating expense increases, supporting margin expansion. Interest expense remained low at 0.9% of revenue, a positive for profitability. However, the disappearance of reported gross profit and EBIT figures is concerning, indicating possible reporting changes or accounting shifts. Despite this, net margin and EPS growth suggest solid bottom-line performance.

Financial Ratios

The table below presents key financial ratios for Universal Health Services, Inc. (UHS) from 2021 to 2025, reflecting profitability, liquidity, leverage, efficiency, and dividend metrics:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 7.8% | 5.0% | 5.0% | 7.2% | 8.6% |

| ROE | 16.3% | 11.4% | 11.7% | 17.1% | 20.3% |

| ROIC | 9.3% | 6.5% | 7.4% | 10.6% | 11.7% |

| P/E | 10.8 | 15.2 | 14.7 | 10.5 | 9.3 |

| P/B | 1.76 | 1.74 | 1.72 | 1.79 | 1.89 |

| Current Ratio | 1.14 | 1.33 | 1.40 | 1.27 | 1.05 |

| Quick Ratio | 1.04 | 1.21 | 1.29 | 1.17 | 1.05 |

| D/E | 0.75 | 0.89 | 0.87 | 0.74 | 0.70 |

| Debt-to-Assets | 34.8% | 39.1% | 38.4% | 34.2% | 33.3% |

| Interest Coverage | 16.0x | 7.9x | 5.7x | 9.0x | 12.8x |

| Asset Turnover | 0.97 | 0.99 | 1.02 | 1.09 | 1.12 |

| Fixed Asset Turnover | 2.03 | 2.10 | 2.18 | 2.26 | 46.40 |

| Dividend Yield | 0.62% | 0.57% | 0.53% | 0.45% | 0.37% |

Evolution of Financial Ratios

Return on Equity (ROE) improved steadily, reaching 20.29% in 2025, indicating stronger profitability. The Current Ratio declined from 1.40 in 2023 to 1.05 in 2025, showing reduced liquidity. Debt-to-Equity Ratio eased slightly from 0.87 in 2023 to 0.70 in 2025, suggesting moderate deleveraging. Profit margins stabilized around 8.6%, reflecting consistent earnings quality.

Are the Financial Ratios Favorable?

In 2025, profitability metrics like ROE and ROIC outperformed the weighted average cost of capital (7.84%), signaling value creation. Liquidity ratios remain neutral to favorable, though Current Ratio is relatively low. Leverage ratios are moderate, with Debt-to-Equity at 0.7 and Debt-to-Assets at 33%. Market multiples, including P/E at 9.31, appear attractive. Interest coverage is a notable weakness, and dividend yield is low, tempering the overall slightly favorable rating.

Shareholder Return Policy

Universal Health Services, Inc. maintains a low dividend payout ratio around 3-8%, with dividends per share steadily near $0.80 and a modest yield below 0.7%. The company supports returns with share buybacks, balancing distributions with free cash flow coverage exceeding 1.7x in recent years.

This policy reflects prudent capital allocation, avoiding excessive payouts amid moderate profit margins and leverage. The combination of dividends and buybacks aligns with sustainable long-term shareholder value creation, maintaining flexibility to invest while rewarding investors conservatively.

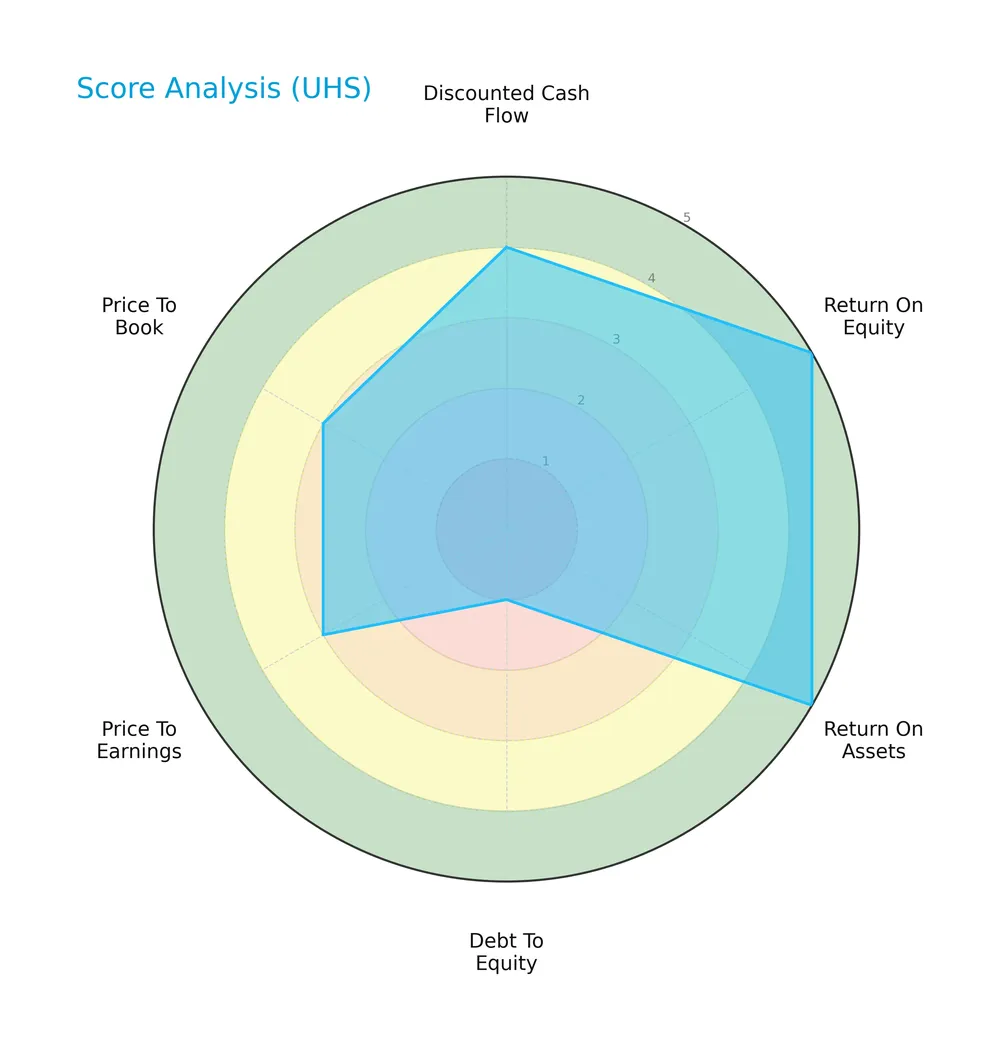

Score analysis

Here is a radar chart summarizing Universal Health Services, Inc.’s key financial scores:

The company scores very favorably on return on equity and assets, indicating strong profitability. Discounted cash flow also rates favorably. However, the debt-to-equity score is very unfavorable, signaling high leverage risk. Price-to-earnings and price-to-book ratios are moderate.

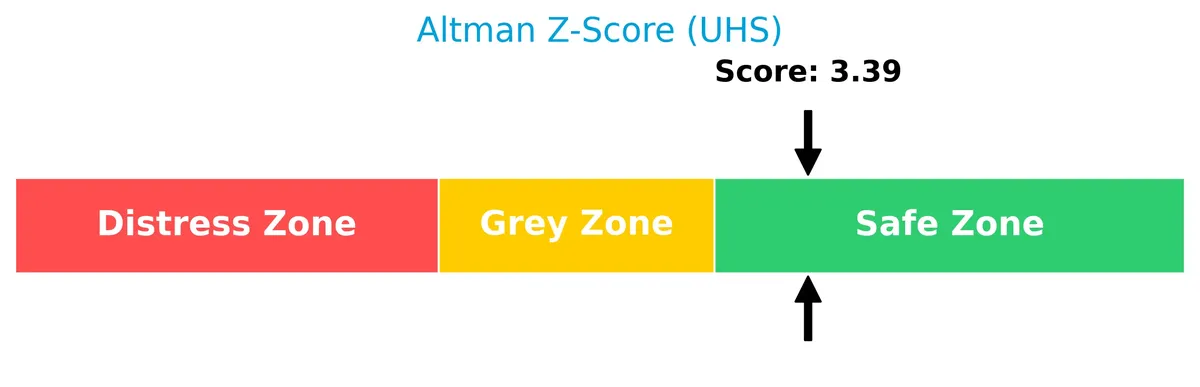

Analysis of the company’s bankruptcy risk

Universal Health Services, Inc. currently resides in the safe zone according to its Altman Z-Score, indicating low bankruptcy risk:

Is the company in good financial health?

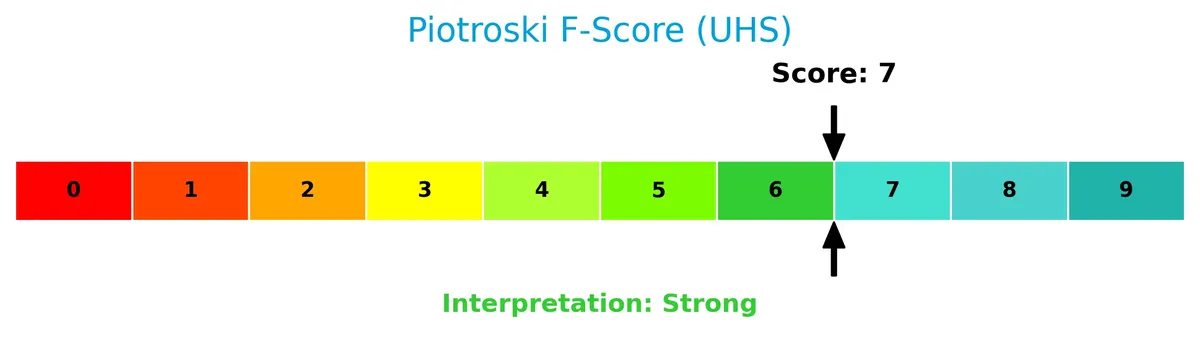

The Piotroski Score diagram illustrates the company’s financial strength based on nine key criteria:

With a score of 7, the company is classified as strong, reflecting solid profitability, efficiency, and financial stability relative to peers.

Competitive Landscape & Sector Positioning

This analysis covers Universal Health Services, Inc.’s strategic positioning, revenue segments, key products, and main competitors. I will evaluate whether the company holds a competitive advantage over its industry peers.

Strategic Positioning

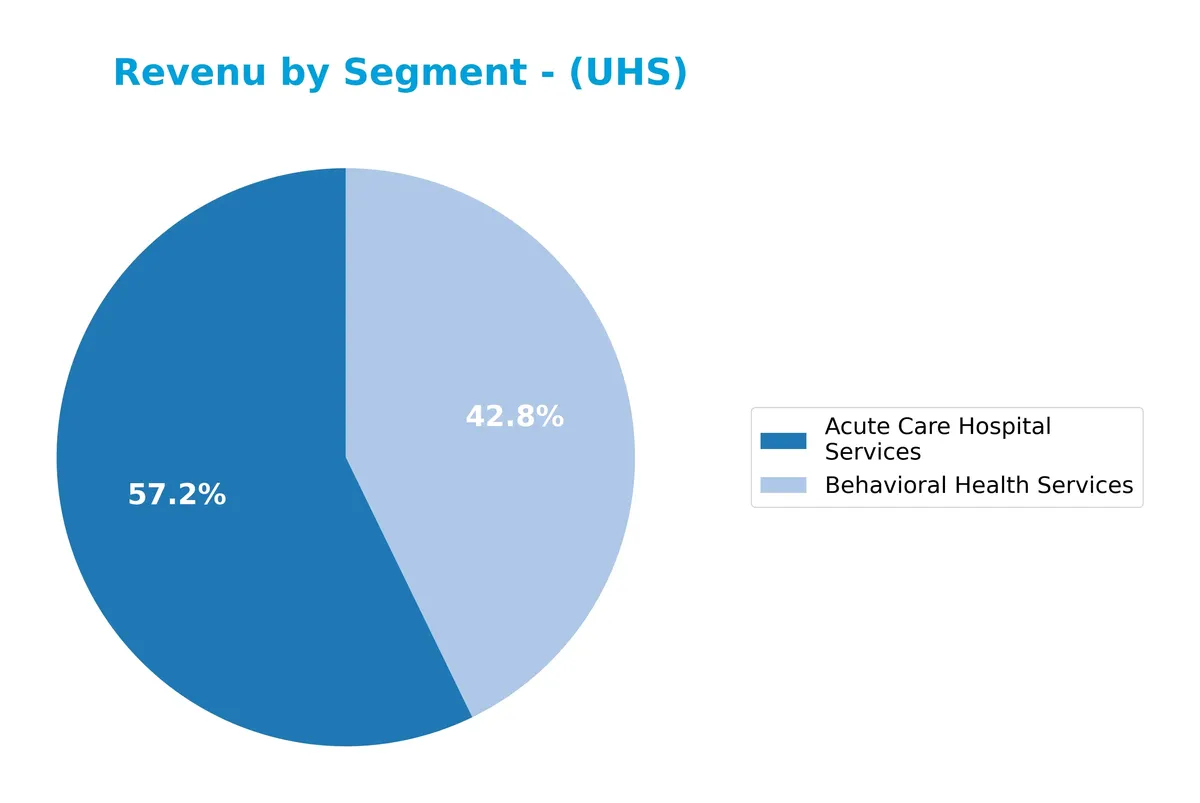

Universal Health Services, Inc. concentrates on healthcare with dual segments: Acute Care Hospital Services (approx. $9.9B in 2025) and Behavioral Health Services ($7.4B). It operates 403 facilities across 39 US states, D.C., UK, and Puerto Rico, combining geographic reach with focused service lines.

Revenue by Segment

The pie chart illustrates Universal Health Services, Inc.’s revenue distribution by segment for fiscal year 2025, highlighting the relative contribution of acute care and behavioral health services.

In 2025, Acute Care Hospital Services drove the business with $9.9B in revenue, outpacing Behavioral Health Services at $7.4B. Both segments show steady growth over recent years, reflecting consistent demand and operational scale. The concentration in these two segments suggests a focused business model, with acute care maintaining a clear leadership role and behavioral health expanding steadily, mitigating concentration risk.

Key Products & Brands

Universal Health Services, Inc. generates revenue primarily from two healthcare service segments:

| Product | Description |

|---|---|

| Acute Care Hospital Services | Operates hospitals offering surgery, internal medicine, emergency, radiology, oncology, pediatrics, pharmacy, and more. |

| Behavioral Health Services | Provides behavioral health care facilities and related services focused on mental health treatment and support. |

Universal Health Services focuses on acute and behavioral health care. Acute Care dominates revenue with comprehensive hospital services. Behavioral Health grows steadily, reflecting rising demand for mental health solutions. These segments define UHS’s core market presence.

Main Competitors

There are 4 competitors in the sector; the table below lists the top 4 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| HCA Healthcare, Inc. | 114B |

| Universal Health Services, Inc. | 14B |

| Solventum Corporation | 14B |

| DaVita Inc. | 8B |

Universal Health Services ranks 2nd among its 4 competitors. Its market cap is 13% of the leader, HCA Healthcare. UHS sits below the average market cap of the top 10 in the sector but above the sector median. The company enjoys a 668% market cap gap to the leader, showing a significant scale difference with its closest rival.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does UHS have a competitive advantage?

Universal Health Services, Inc. presents a very favorable competitive advantage. The company consistently generates an ROIC 3.8% above its WACC, signaling efficient capital use and value creation over 2021-2025.

Looking ahead, UHS’s extensive network of 363 inpatient and 40 outpatient facilities across multiple regions offers growth opportunities. Expansion in behavioral health services and specialized care may further enhance its market position.

SWOT Analysis

This analysis highlights Universal Health Services, Inc.’s core strengths, weaknesses, opportunities, and threats to guide strategic decisions.

Strengths

- strong ROIC exceeding WACC

- diversified acute and behavioral health services

- steady revenue and net income growth

Weaknesses

- unfavorable gross and EBIT margins

- moderate current ratio at 1.05

- low dividend yield

Opportunities

- expanding behavioral health segment

- increasing healthcare demand post-pandemic

- technology integration for operational efficiency

Threats

- regulatory changes in healthcare

- rising operational costs

- competitive pressure in care facilities

Universal Health Services demonstrates robust value creation with growing profitability. However, margin pressures and liquidity metrics warrant caution. Strategic focus on expanding behavioral health and operational efficiencies can mitigate risks from regulatory and cost challenges.

Stock Price Action Analysis

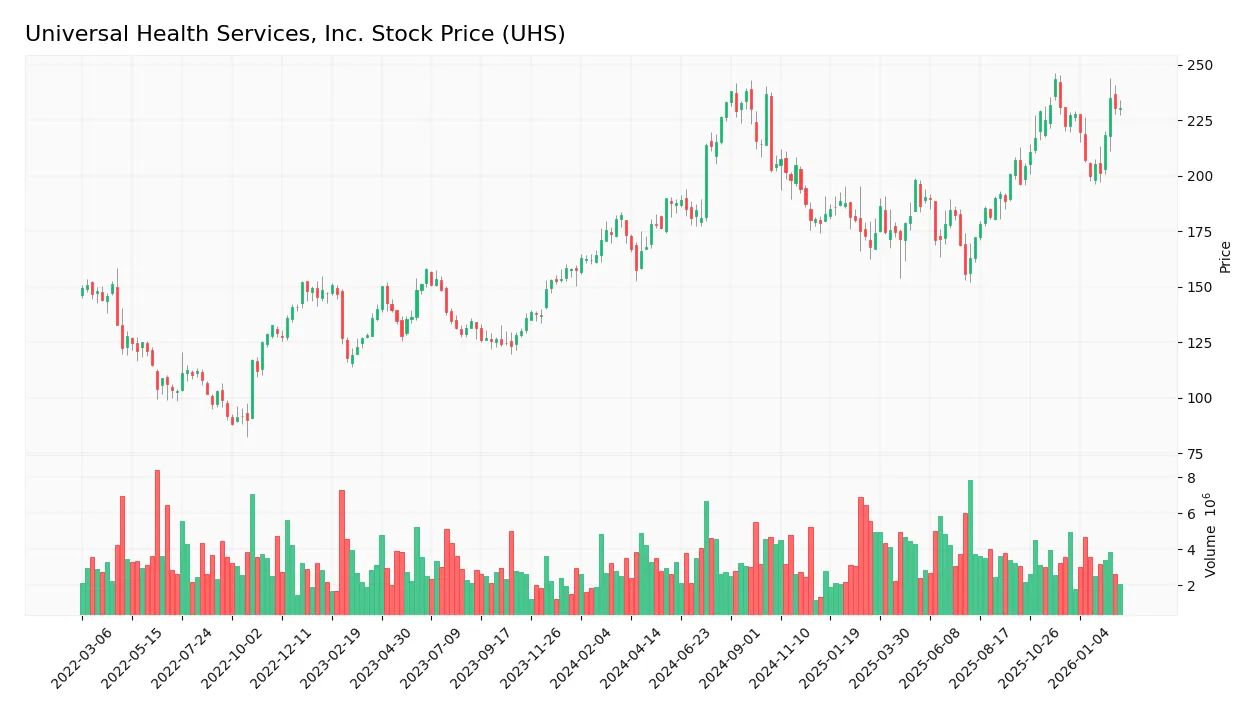

The following weekly stock chart illustrates Universal Health Services, Inc. (UHS) price movements over the past 100 weeks:

Trend Analysis

Over the past 12 months, UHS stock gained 33.04%, showing a bullish trend with accelerated momentum. The price ranged from a low of 155.6 to a high of 243.63, supported by a high volatility level of 22.05%. Recent three-month data reveals a 3.65% rise with steady slope of 0.52, confirming continued positive momentum.

Volume Analysis

Trading volume is increasing, with 53.41% buyer dominance over the full period. However, the recent three months show slight seller dominance at 52.59%, indicating neutral buyer behavior. This suggests cautious investor sentiment with balanced market participation amid rising volumes.

Target Prices

Analysts set a firm target consensus for Universal Health Services, Inc., reflecting positive growth expectations.

| Target Low | Target High | Consensus |

|---|---|---|

| 219 | 274 | 245.67 |

The target range suggests analysts anticipate a 10-15% upside from current levels, signaling confidence in UHS’s operational resilience and market positioning.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section examines Universal Health Services, Inc.’s analyst ratings and consumer feedback to assess market sentiment.

Stock Grades

Here are the latest verified analyst grades for Universal Health Services, Inc. (UHS) from recognized financial institutions:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Barclays | Maintain | Overweight | 2026-01-22 |

| TD Cowen | Maintain | Buy | 2026-01-07 |

| Wells Fargo | Downgrade | Equal Weight | 2026-01-07 |

| Guggenheim | Maintain | Buy | 2025-12-02 |

| Wells Fargo | Maintain | Overweight | 2025-11-13 |

| RBC Capital | Maintain | Sector Perform | 2025-10-30 |

| Cantor Fitzgerald | Maintain | Neutral | 2025-10-29 |

| Guggenheim | Maintain | Buy | 2025-10-29 |

| UBS | Maintain | Buy | 2025-10-29 |

| Barclays | Maintain | Overweight | 2025-10-28 |

The consensus reflects a stable outlook with a majority maintaining buy or overweight ratings. Notably, Wells Fargo’s recent downgrade to equal weight signals some caution amid generally positive sentiment.

Consumer Opinions

Universal Health Services, Inc. evokes a mix of respect and frustration among its patients and clients.

| Positive Reviews | Negative Reviews |

|---|---|

| Staff are compassionate and attentive. | Long wait times in emergency departments. |

| Facilities are clean and well-maintained. | Billing processes can be confusing and slow. |

| High-quality care with experienced physicians. | Communication gaps between departments reported. |

Overall, consumers praise UHS for its compassionate care and clean facilities. However, recurrent complaints about wait times and billing issues indicate operational areas needing urgent improvement.

Risk Analysis

Below is a summary table presenting key risks for Universal Health Services, Inc., highlighting likelihood and potential impact:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Financial Leverage | High debt-to-equity ratio signals financial strain risk | Medium | High |

| Interest Coverage | Zero interest coverage ratio indicates risk of default | High | High |

| Regulatory Changes | Healthcare regulations could tighten, increasing costs | Medium | Medium |

| Operational Risks | Managing 400+ facilities across geographies is complex | Medium | Medium |

| Market Volatility | Beta above 1.2 exposes stock to amplified market swings | High | Medium |

| Dividend Yield | Low yield reduces appeal to income-focused investors | Low | Low |

Interest coverage at 0.0 is a glaring red flag, raising concerns about debt servicing ability despite a safe Altman Z-score of 3.39. The company’s debt-to-equity ratio of 0.7 is neutral but warrants monitoring given the healthcare sector’s capital intensity. Market volatility remains a risk with beta at 1.27. These financial vulnerabilities contrast with strong profitability metrics like 20.3% ROE, underscoring the need for cautious portfolio allocation.

Should You Buy Universal Health Services, Inc.?

Universal Health Services, Inc. appears to be a robust value creator with a very favorable moat supported by growing ROIC well above WACC. Despite substantial leverage concerns, its financial health is rated A-, suggesting operational efficiency but caution regarding debt.

Strength & Efficiency Pillars

Universal Health Services, Inc. demonstrates solid profitability with a net margin of 8.57% and a return on equity of 20.29%. Its return on invested capital (ROIC) stands at 11.66%, comfortably exceeding the weighted average cost of capital (WACC) of 7.84%. This differential confirms the company as a clear value creator. Additionally, a strong Piotroski score of 7 and growing ROIC trend underscore a sustainable competitive advantage and effective capital allocation.

Weaknesses and Drawbacks

The company maintains a neutral debt-to-equity ratio of 0.7, but its interest coverage ratio is alarmingly unfavorable at 0.0, signaling potential challenges in servicing debt. Although the price-to-earnings ratio of 9.31 is favorable, the moderate price-to-book ratio of 1.89 and a slim current ratio of 1.05 suggest limited liquidity buffers. Recent seller dominance at 52.59% in the short term also introduces some market pressure and uncertainty.

Our Final Verdict about Universal Health Services, Inc.

Universal Health Services presents a fundamentally strong profile with value creation and robust profitability. Its bullish long-term trend, paired with a safe Altman Z-score of 3.39, signals financial stability. However, recent neutral buyer behavior advises a cautious wait-and-see for a more favorable entry, as market dynamics may temporarily weigh on price momentum. Overall, the profile may appear attractive for investors with a medium to long-term horizon.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Universal Health Services misses quarterly profit estimates on lower medical care demand – Reuters (Feb 25, 2026)

- UNIVERSAL HEALTH SERVICES, INC. ANNOUNCES FINANCIAL RESULTS FOR THE THREE AND TWELVE-MONTH PERIODS ENDED DECEMBER 31, 2025 AND OPERATING RESULTS FORECAST FOR THE FULL YEAR OF 2026 – Yahoo Finance (Feb 25, 2026)

- Decoding Universal Health Services Inc (UHS): A Strategic SWOT I – GuruFocus (Feb 26, 2026)

- Universal Health Services (NYSE:UHS) Misses Q4 CY2025 Sales Expectations – Bitget (Feb 25, 2026)

- Universal Health Services: Q4 Earnings Snapshot – morning-times.com (Feb 25, 2026)

For more information about Universal Health Services, Inc., please visit the official website: uhs.com