Home > Analyses > Healthcare > UnitedHealth Group Incorporated

UnitedHealth Group shapes how millions access healthcare daily, blending insurance with cutting-edge health services. It dominates the medical insurance sector through its UnitedHealthcare plans and the innovative Optum platforms, which streamline care delivery and pharmacy management. Renowned for operational scale and technological integration, it consistently sets industry standards. As healthcare demands evolve, I question whether UnitedHealth’s robust fundamentals still justify its lofty valuation and support sustainable growth ahead.

Table of contents

Business Model & Company Overview

UnitedHealth Group Incorporated, founded in 1977 and headquartered in Eden Prairie, MN, stands as a titan in the healthcare plans industry. With 400K employees, it integrates four segments—UnitedHealthcare, Optum Health, Optum Insight, and OptumRx—into a cohesive ecosystem delivering broad health benefit plans and specialized care services. This diversified health care approach addresses needs from individual consumers to large employers and government programs, positioning UnitedHealth as a dominant force in U.S. healthcare.

The company’s revenue engine balances consumer-oriented health plans with advanced software and pharmacy care services. UnitedHealthcare leads with insurance coverage, while Optum segments drive value through care delivery, data analytics, and pharmacy management across the Americas, Europe, and Asia. This blend of recurring services and technology solutions fuels steady growth and underpins UnitedHealth’s wide economic moat, securing its role as a future shaper of healthcare.

Financial Performance & Fundamental Metrics

I analyze UnitedHealth Group Incorporated’s income statement, key financial ratios, and dividend payout policy to assess its profitability and capital allocation efficiency.

Income Statement

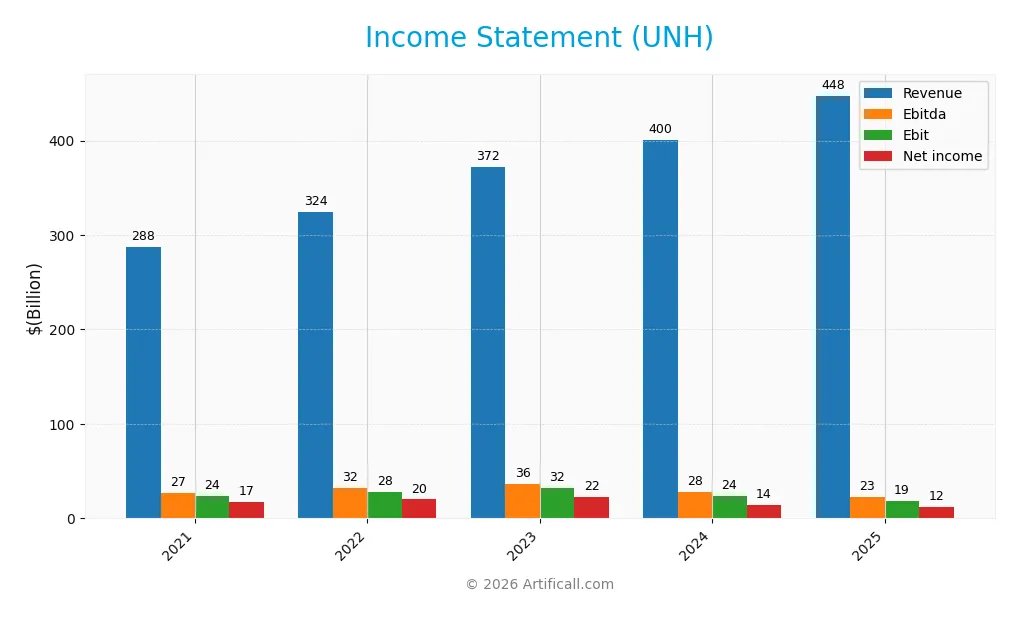

The table below summarizes UnitedHealth Group Incorporated’s key income statement figures for the fiscal years 2021 through 2025, showing trends in revenue, profitability, and earnings per share.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 288B | 324B | 372B | 400B | 448B |

| Cost of Revenue | 218B | 245B | 281B | 311B | 365B |

| Operating Expenses | 46B | 51B | 59B | 57B | 64B |

| Gross Profit | 70B | 80B | 91B | 89B | 83B |

| EBITDA | 27B | 32B | 36B | 28B | 23B |

| EBIT | 24B | 28B | 32B | 24B | 19B |

| Interest Expense | 1.7B | 2.1B | 3.2B | 3.9B | 4.0B |

| Net Income | 17B | 20B | 22B | 14B | 12B |

| EPS | 18.33 | 21.54 | 24.12 | 15.64 | 13.23 |

| Filing Date | 2022-02-15 | 2023-02-24 | 2023-12-31 | 2025-02-27 | 2026-03-02 |

Income Statement Evolution

UnitedHealth’s revenue grew steadily from 287.6B in 2021 to 447.6B in 2025, a 55.6% increase. However, net income declined 30.3% over the same period, falling to 12.1B in 2025. Margins weakened, with gross profit and net margin contracting, signaling rising costs and pressure on profitability despite top-line expansion.

Is the Income Statement Favorable?

The 2025 income statement shows mixed fundamentals. Revenue growth of 11.8% is favorable, but gross profit decreased 7.3%, and EBIT dropped 22%. Net margin shrank to 2.7%, reflecting cost pressures. Interest expense remains low at 0.9% of revenue, a positive factor. Overall, the statement’s risks outweigh strengths, yielding an unfavorable assessment.

Financial Ratios

The table below presents key financial ratios for UnitedHealth Group Incorporated (UNH) over the last five fiscal years:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 6.0% | 6.2% | 6.0% | 3.6% | 2.7% |

| ROE | 24.1% | 25.9% | 25.2% | 15.5% | 12.0% |

| ROIC | 13.9% | 14.0% | 14.3% | 12.3% | 8.2% |

| P/E | 27.4 | 24.6 | 21.8 | 32.6 | 24.9 |

| P/B | 6.6 | 6.4 | 5.5 | 5.1 | 3.0 |

| Current Ratio | 0.79 | 0.77 | 0.79 | 0.83 | 0.79 |

| Quick Ratio | 0.79 | 0.77 | 0.79 | 0.83 | 0.79 |

| D/E | 0.64 | 0.74 | 0.76 | 0.83 | 0.78 |

| Debt-to-Assets | 21.7% | 23.5% | 24.6% | 25.8% | 25.3% |

| Interest Coverage | 14.4x | 13.6x | 10.0x | 8.3x | 4.7x |

| Asset Turnover | 1.36 | 1.32 | 1.36 | 1.34 | 1.45 |

| Fixed Asset Turnover | 32.1 | 32.0 | 32.5 | 37.9 | 0.0 |

| Dividend Yield | 1.1% | 1.2% | 1.4% | 1.6% | 2.6% |

Evolution of Financial Ratios

UnitedHealth’s Return on Equity (ROE) declined from 25.2% in 2023 to 12.1% in 2025, indicating reduced profitability. The Current Ratio hovered below 1.0, signaling consistent liquidity pressure. Debt-to-Equity Ratio rose slightly to 0.78 in 2025, reflecting stable but moderate leverage over the period.

Are the Financial Ratios Favorable?

In 2025, profitability ratios show mixed signals: ROE and ROIC are neutral, but net margin is unfavorable at 2.7%. Liquidity ratios, including Current and Quick Ratios around 0.79, are unfavorable, suggesting tight short-term resources. Leverage is neutral with a Debt-to-Equity near 0.78, while asset turnover and dividend yield rates are favorable. Overall, the ratios lean slightly unfavorable.

Shareholder Return Policy

UnitedHealth Group pays dividends consistently, with a payout ratio rising to 65.7% in 2025 and dividend yield at 2.64%. Dividend payments remain well-covered by free cash flow, supported by moderate share buybacks, reflecting disciplined capital allocation.

This payout level and buyback activity align with sustainable shareholder value creation. The company balances rewarding investors and retaining cash for growth, avoiding risks of over-distribution or excessive leverage.

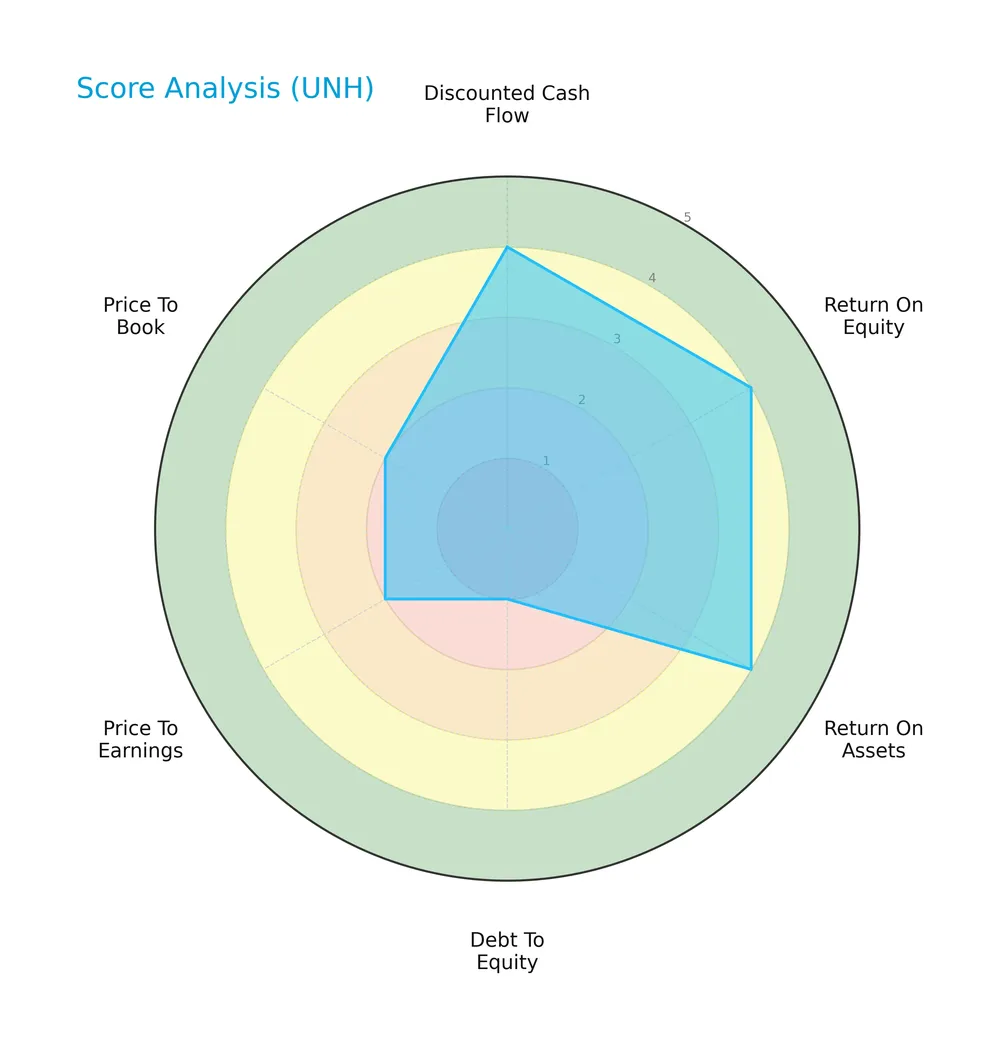

Score analysis

The following radar chart illustrates UnitedHealth Group’s key financial scores across valuation, profitability, and leverage metrics:

UnitedHealth excels in discounted cash flow, return on equity, and return on assets, each scoring 4, indicating strong profitability and value creation. However, its debt-to-equity score is very unfavorable at 1, signaling high leverage risk. Price-to-earnings and price-to-book scores are both unfavorable at 2, reflecting valuation concerns.

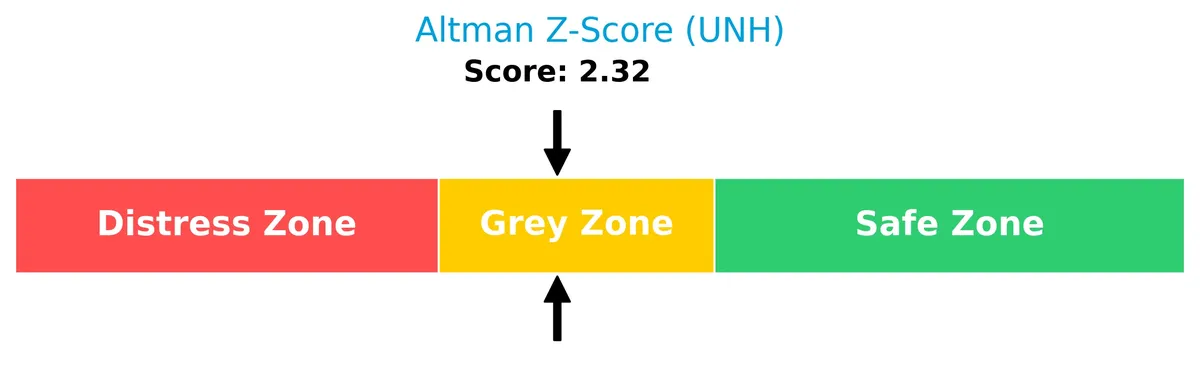

Analysis of the company’s bankruptcy risk

UnitedHealth’s Altman Z-Score places it in the grey zone, signaling a moderate risk of financial distress and potential bankruptcy:

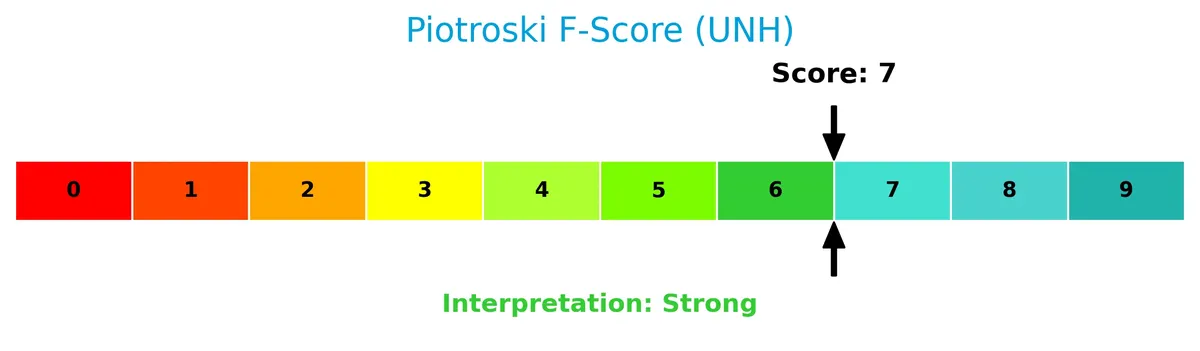

Is the company in good financial health?

This Piotroski diagram highlights UnitedHealth’s solid financial strength based on nine fundamental criteria:

With a strong Piotroski score of 7, the company demonstrates robust profitability, liquidity, and operating efficiency, supporting its status as financially sound despite some leverage concerns.

Competitive Landscape & Sector Positioning

This sector analysis examines UnitedHealth Group’s strategic positioning, revenue segments, key products, and main competitors. I will assess whether UnitedHealth Group holds a competitive advantage over its industry peers.

Strategic Positioning

UnitedHealth Group operates a diversified portfolio across healthcare plans, pharmacy services, and health technology. UnitedHealthcare dominates with $332B revenue in 2025, complemented by Optum segments spanning care delivery, data analytics, and pharmacy, reflecting a broad product mix within the U.S. market.

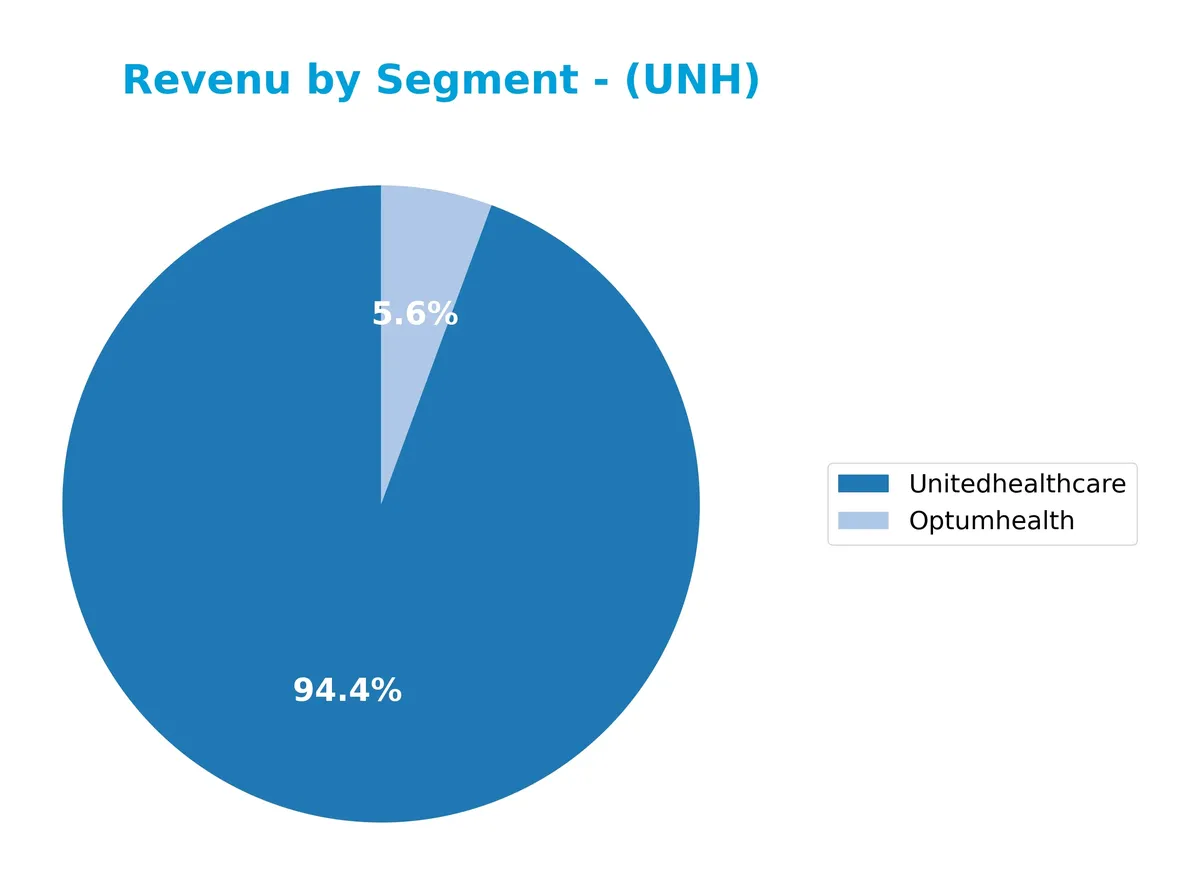

Revenue by Segment

This pie chart illustrates UnitedHealth Group’s revenue distribution by segment for the full fiscal year 2025, highlighting the relative size of its core business units.

UnitedHealthcare dominates with $332B revenue, nearly 17x larger than Optumhealth at $19.8B in 2025. The data reveals a consolidation in reporting, focusing on these two segments, reflecting a strategic simplification. Historically, Optum segments grew rapidly, but 2025 shows a sharp decline in Optum revenue reporting, signaling potential segment reclassification or concentration risk around UnitedHealthcare. This shift demands careful monitoring for future diversification impacts.

Key Products & Brands

The table below lists UnitedHealth Group’s main products and brands, along with their core descriptions:

| Product | Description |

|---|---|

| UnitedHealthcare | Offers health benefit plans and services for employers, individuals, Medicaid, and specialized services for older adults. |

| OptumHealth | Provides care delivery, health management services, consumer engagement, and financial services to individuals and entities. |

| OptumInsight | Supplies software, advisory consulting, and managed services to hospitals, physicians, health plans, and governments. |

| OptumRx | Delivers pharmacy care services including retail, home delivery, specialty pharmacy, and drug therapy management programs. |

UnitedHealth Group operates through these four segments, combining health benefits with care delivery and data-driven solutions. UnitedHealthcare remains the largest revenue contributor by far.

Main Competitors

The Healthcare sector includes 7 main competitors, with the table listing the top 7 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| UnitedHealth Group Incorporated | 305B |

| CVS Health Corporation | 102B |

| Elevance Health Inc. | 79B |

| Cigna Corporation | 75B |

| Humana Inc. | 32B |

| Centene Corporation | 21B |

| Molina Healthcare, Inc. | 9.7B |

UnitedHealth Group ranks first among its 7 competitors by a wide margin. Its market cap is 88% of the top leader benchmark, placing it well Above both the average market cap of the top 10 peers (88.8B) and the median sector cap (74.6B). The gap with the next competitor, CVS Health, is substantial, reinforcing UnitedHealth’s dominant position.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does UNH have a competitive advantage?

UnitedHealth Group demonstrates a competitive advantage by creating value with a ROIC exceeding its WACC by 3%, indicating efficient capital use despite a declining profitability trend. Its diversified business model spans healthcare plans, care delivery, pharmacy services, and data analytics, strengthening its market position.

Looking ahead, UNH’s opportunities lie in expanding its Optum segments, which integrate technology and healthcare services, targeting evolving consumer needs and healthcare innovation. These efforts could support growth amid healthcare sector complexities and increasing demand for value-based care.

SWOT Analysis

This SWOT analysis highlights UnitedHealth Group’s strategic position by assessing internal capabilities and external challenges.

Strengths

- diversified healthcare segments

- strong market cap of $267B

- favorable WACC at 5.21%

Weaknesses

- declining ROIC trend

- unfavorable net margin of 2.69%

- weak liquidity ratios (current ratio 0.79)

Opportunities

- expanding healthcare demand

- growth in pharmacy services

- digital health innovation

Threats

- regulatory changes

- rising healthcare costs

- intense competition in healthcare plans

UnitedHealth’s robust market presence and diversified services create a solid foundation. However, margin pressure and liquidity constraints require careful capital management. The company must leverage growth opportunities while mitigating regulatory and cost risks to sustain its competitive moat.

Stock Price Action Analysis

The following weekly chart illustrates UnitedHealth Group Incorporated’s stock price movement over the last 100 weeks, highlighting key price levels and volatility:

Trend Analysis

Over the past 12 months, UNH’s stock price declined by 32.85%, confirming a bearish trend. The price dropped from a high of 615.81 to a low of 237.77, with decelerating downward momentum. Volatility remains elevated, with a standard deviation of 114.31, indicating significant price fluctuation during the period.

Volume Analysis

Trading volume has increased overall, totaling 4.42B shares, with sellers slightly outpacing buyers at 50.63%. In the recent three months, seller dominance intensified to 56.53% amid rising volume. This suggests cautious investor sentiment and heightened selling pressure in the near term.

Target Prices

Analysts project a target price consensus reflecting moderate growth potential for UnitedHealth Group Incorporated.

| Target Low | Target High | Consensus |

|---|---|---|

| 327 | 444 | 385.38 |

The target prices suggest a balanced outlook, with upside near 444 and downside around 327. The consensus at 385.38 indicates steady confidence in UNH’s performance.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section examines analyst ratings and consumer feedback to provide insights into UnitedHealth Group Incorporated’s market perception.

Stock Grades

Here are the latest verified analyst grades for UnitedHealth Group Incorporated from recognized firms:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Mizuho | Maintain | Outperform | 2026-02-05 |

| JP Morgan | Maintain | Overweight | 2026-02-02 |

| Truist Securities | Maintain | Buy | 2026-02-02 |

| Barclays | Maintain | Overweight | 2026-01-30 |

| Wells Fargo | Maintain | Overweight | 2026-01-30 |

| Oppenheimer | Maintain | Outperform | 2026-01-28 |

| RBC Capital | Maintain | Outperform | 2026-01-28 |

| Leerink Partners | Maintain | Outperform | 2026-01-28 |

| Jefferies | Maintain | Buy | 2026-01-28 |

| UBS | Maintain | Buy | 2026-01-28 |

The consensus shows a strong preference for buying UnitedHealth Group, with most analysts maintaining positive ratings such as Buy, Overweight, or Outperform. No recent downgrades or negative shifts appear, indicating stable confidence in the stock’s prospects.

Consumer Opinions

UnitedHealth Group consistently earns praise for its customer service and comprehensive healthcare plans, yet some users express frustration over billing complexities.

| Positive Reviews | Negative Reviews |

|---|---|

| “Excellent coverage options and easy claims process.” | “Confusing billing statements and unexpected charges.” |

| “Responsive customer support that resolves issues quickly.” | “Long wait times on customer service calls.” |

| “Wide network of providers and good prescription benefits.” | “Premiums have increased significantly in recent years.” |

Overall, consumers appreciate UnitedHealth’s extensive provider network and support quality. However, billing transparency and premium hikes remain persistent pain points.

Risk Analysis

Below is a summary table presenting UnitedHealth Group’s key risk categories, their likelihood, and potential impact:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Financial Liquidity | Current and quick ratios below 1 signal tight short-term liquidity. | High | Moderate |

| Valuation | Elevated price-to-book ratio (3.0) suggests overvaluation risk. | Medium | Moderate |

| Profitability | Low net margin (2.69%) indicates pressure on earnings quality. | Medium | High |

| Debt Management | Debt-to-equity concerns reflected in very unfavorable score. | Medium | Moderate |

| Market Volatility | Low beta (0.415) reduces sensitivity to market swings. | Low | Low |

| Bankruptcy Risk | Altman Z-Score in grey zone (2.32) signals moderate financial distress risk. | Medium | High |

The most pressing risks are UnitedHealth’s weak liquidity ratios and below-par net margin, which constrain operational flexibility. Its Altman Z-Score in the grey zone adds caution, reflecting moderate bankruptcy risk despite a strong Piotroski score. Investors should watch valuation multiples and debt levels closely.

Should You Buy UnitedHealth Group Incorporated?

UnitedHealth Group appears to be a robust value creator with a slightly favorable moat, evidenced by positive but declining ROIC relative to WACC. Despite a manageable leverage profile, its overall B rating suggests moderate financial strength balanced by some valuation concerns.

Strength & Efficiency Pillars

UnitedHealth Group Incorporated demonstrates operational resilience with an ROIC of 8.23% surpassing its WACC of 5.21%, confirming it as a value creator. Despite a modest net margin of 2.69% and a neutral ROE of 12.05%, the company benefits from favorable interest expense at 0.89% and solid asset turnover at 1.45. These metrics reflect efficient capital deployment amid a challenging industry environment. Historically in healthcare, maintaining ROIC above WACC signals sustainable competitive advantages, a critical moat in this sector.

Weaknesses and Drawbacks

The company remains in the Altman Z-Score grey zone at 2.32, indicating moderate bankruptcy risk and warranting caution. Valuation metrics pose concerns: a P/B ratio of 3.0 signals potential overvaluation relative to book value, while a neutral P/E of 24.92 suggests fair but not compelling pricing. Liquidity is weak with a current ratio of 0.79, below the safety threshold of 1, heightening short-term financial risk. Additionally, recent seller dominance (56.53% sellers) and a bearish price trend (-32.85% over the longer term) create immediate market pressure.

Our Final Verdict about UnitedHealth Group Incorporated

UnitedHealth Group Incorporated’s long-term fundamentals suggest value creation, but the Altman Z-Score’s grey zone status and weakening profitability trends inject uncertainty. Despite solid operational metrics, current market pressure and liquidity risks imply a wait-and-see approach may be prudent. This profile might appear suitable for investors with a tolerance for moderate risk, but it may not be ideal for conservative capital seeking stability.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Where is UnitedHealth Group Incorporated (UNH) Headed? – Yahoo Finance (Feb 28, 2026)

- Decoding UnitedHealth Group Inc (UNH): A Strategic SWOT Insight – GuruFocus (Mar 03, 2026)

- UnitedHealth Group (NYSE: UNH) files shelf to register multiple securities – Stock Titan (Mar 02, 2026)

- UnitedHealth stock price ticks up after hours as UNH files shelf, 10-K and accounting shake-up – TechStock² (Mar 03, 2026)

- UnitedHealth Group Incorporated $UNH Shares Sold by River Wealth Advisors LLC – MarketBeat (Mar 02, 2026)

For more information about UnitedHealth Group Incorporated, please visit the official website: unitedhealthgroup.com