Home > Analyses > Consumer Defensive > The Magnum Ice Cream Company N.V.

Magnum Ice Cream transforms everyday indulgence into a global craving. As a dominant force in packaged foods, it commands market respect with premium ice cream offerings known for rich flavor and innovative recipes. The company’s strong brand loyalty and expansive reach underpin its leadership in the consumer defensive sector. Yet, with its recent market debut, I ask: do Magnum’s fundamentals justify its current valuation and growth outlook in a competitive landscape?

Table of contents

Business Model & Company Overview

The Magnum Ice Cream Company N.V., headquartered in Amsterdam, stands as a dominant player in the packaged foods sector. Founded recently before its 2025 IPO, it leverages a cohesive ecosystem centered on premium ice cream products. The company employs over 18,500 people, underscoring its significant scale and commitment to quality within the consumer defensive industry.

Its revenue engine balances product innovation with strong market penetration across the Americas, Europe, and Asia. Magnum combines its core ice cream offerings with strategic distribution channels, creating a resilient stream of sales in diverse global markets. This competitive advantage fortifies its economic moat, positioning the firm to shape the future of premium frozen treats worldwide.

Financial Performance & Fundamental Metrics

I analyze The Magnum Ice Cream Company N.V.’s income statement, key financial ratios, and dividend payout policy to assess its core financial health and shareholder value.

Income Statement

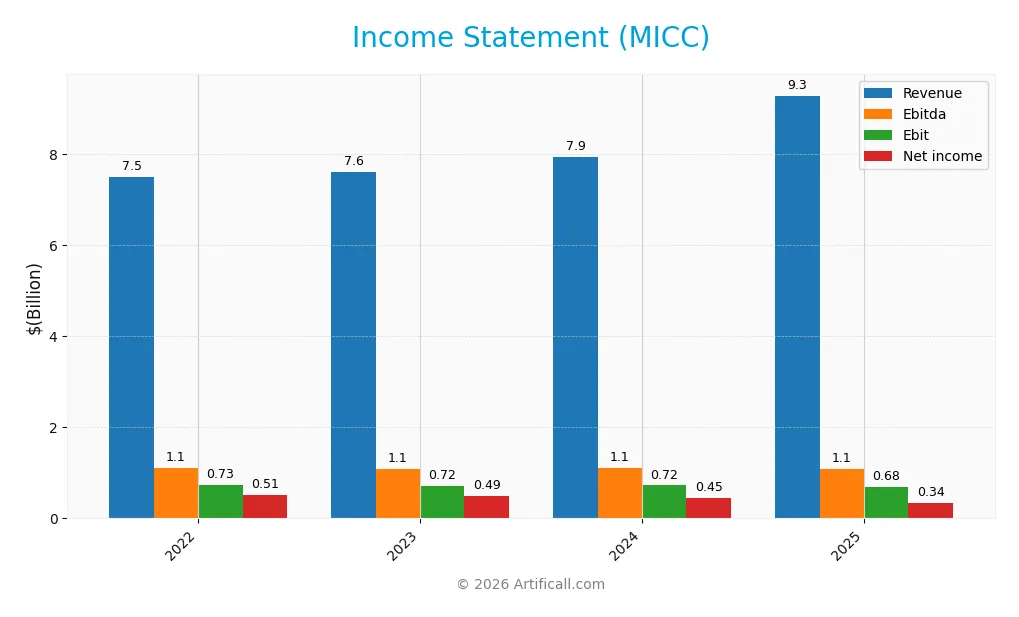

The following table summarizes The Magnum Ice Cream Company N.V.’s annual income statement figures for fiscal years 2022 through 2025, reported in respective currencies.

| 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|

| Revenue | 7.51B EUR | 7.62B EUR | 7.95B EUR | 9.29B USD |

| Cost of Revenue | 4.94B EUR | 5.02B EUR | 5.17B EUR | 0 USD |

| Operating Expenses | 1.83B EUR | 1.85B EUR | 2.04B EUR | 8.59B USD |

| Gross Profit | 2.57B EUR | 2.60B EUR | 2.77B EUR | 9.29B USD |

| EBITDA | 1.10B EUR | 1.08B EUR | 1.10B EUR | 1.08B USD |

| EBIT | 729M EUR | 722M EUR | 725M EUR | 682M USD |

| Interest Expense | 29M EUR | 10M EUR | 142M EUR | 163M USD |

| Net Income | 509M EUR | 492M EUR | 450M EUR | 344M USD |

| EPS | 0.83 | 0.80 | 0.74 | 0.56 |

| Filing Date | 2022-12-31 | 2023-12-31 | 2024-12-31 | 2026-03-18 |

Income Statement Evolution

Between 2022 and 2025, revenue grew by 23.8%, showing steady top-line expansion. However, net income declined by 32.4%, reflecting margin compression. Gross margin improved to a favorable 100%, but EBIT and net margins weakened, indicating increased operating and other expenses eroded profitability despite revenue gains.

Is the Income Statement Favorable?

In 2025, revenue surged 16.9% year-over-year, yet EBIT dropped 5.9%, and net margin fell to 3.7%, signaling profitability pressures. Operating expenses rose proportionally with revenue, an unfavorable trend. Interest expense remains low and favorable, but overall fundamentals appear challenged, with declining net income and EPS growth weighing on earnings quality.

Financial Ratios

The following table summarizes key financial ratios for The Magnum Ice Cream Company N.V. over the last five fiscal years:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 0% | 6.78% | 6.46% | 5.66% | 3.70% |

| ROE | 0% | 26.06% | 19.60% | 16.20% | 46.88% |

| ROIC | 0% | 19.65% | 15.65% | 16.42% | 9.17% |

| P/E | 0 | 17.95 | 18.57 | 20.30 | 28.11 |

| P/B | 0 | 4.68 | 3.64 | 3.29 | 13.18 |

| Current Ratio | 0.68 | 0.81 | 0.77 | 0.80 | 1.02 |

| Quick Ratio | 0.26 | 0.32 | 0.31 | 0.35 | 0.74 |

| D/E | 0.12 | 0.10 | 0.08 | 0.07 | 0.17 |

| Debt-to-Assets | 4.33% | 3.96% | 3.74% | 3.41% | 1.40% |

| Interest Coverage | 0 | 25.41 | 74.20 | 5.18 | 4.31 |

| Asset Turnover | 0 | 1.58 | 1.44 | 1.44 | 1.06 |

| Fixed Asset Turnover | 0 | 3.34 | 3.41 | 3.37 | 3.43 |

| Dividend Yield | 0% | 0% | 0% | 0.12% | 1.01% |

Evolution of Financial Ratios

Return on Equity (ROE) surged dramatically, reaching 46.88% in 2025 from near zero in 2021, indicating a sharp improvement in profitability. The Current Ratio showed a gradual increase, moving from 0.68 in 2021 to 1.02 in 2025, reflecting enhanced short-term liquidity. Debt-to-Equity Ratio declined from 0.12 in 2021 to 0.17 in 2025, suggesting stable leverage with a slight uptick in debt usage.

Are the Financial Ratios Favorable?

In 2025, ROE stands out as highly favorable, supported by a WACC below ROIC, highlighting efficient capital allocation. Liquidity ratios like Current Ratio are neutral, but the Quick Ratio is unfavorable, indicating potential short-term liquidity constraints. Valuation multiples such as P/E and P/B are unfavorable, suggesting market premium or overvaluation. Debt metrics remain favorable, with low debt-to-assets and manageable interest coverage. Overall, the ratio profile is slightly favorable but warrants caution on valuation and liquidity.

Shareholder Return Policy

The Magnum Ice Cream Company N.V. pays dividends with a 28% payout ratio and a 1.01% annual yield, supported by a modest dividend per share increase. Share buybacks are not explicitly reported, and free cash flow covers only 3% of operating cash flow, indicating limited distribution flexibility.

This payout aligns with sustainable value creation given the company’s positive net margin and cash flow, though the low free cash flow coverage flags potential risks if operating performance weakens. The policy balances shareholder returns with prudent capital retention for operational stability.

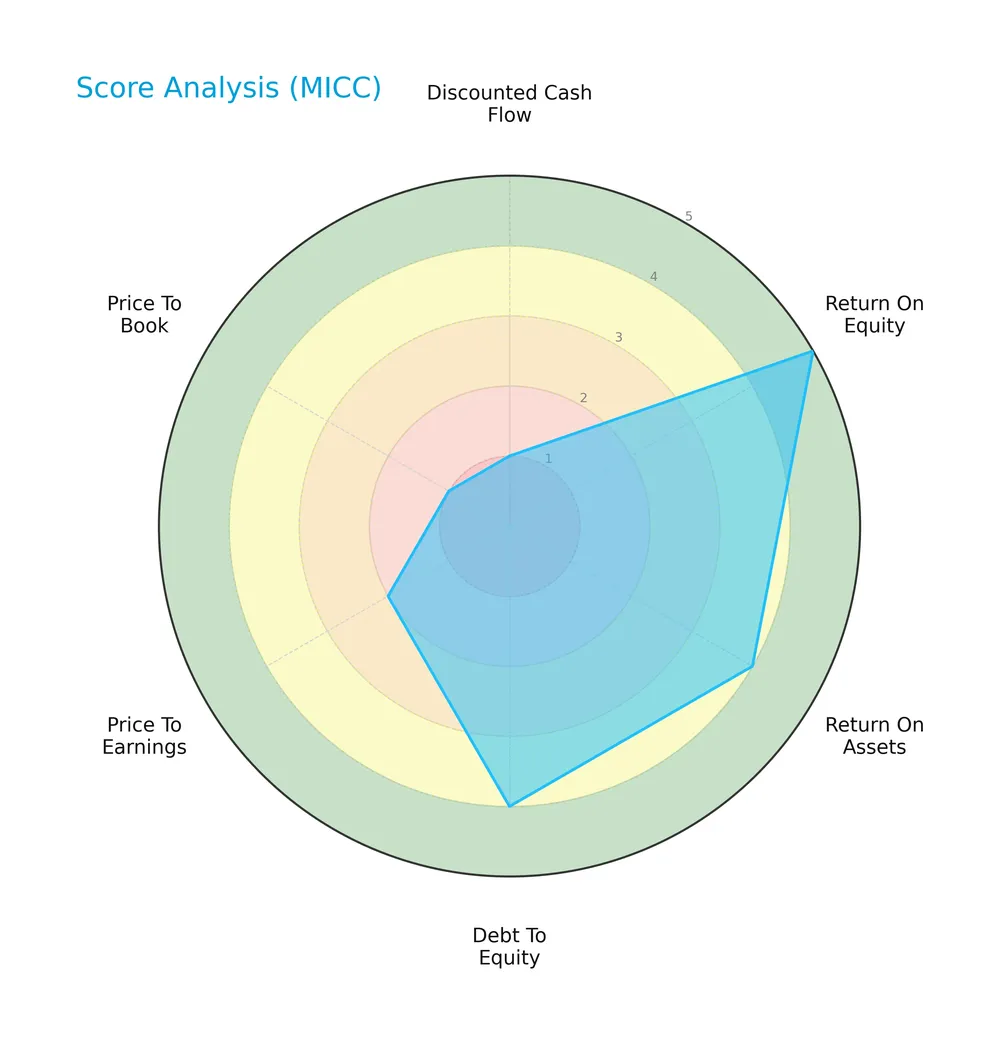

Score analysis

The following radar chart illustrates key valuation and financial performance scores for The Magnum Ice Cream Company N.V.:

The company shows strong returns on equity (5) and assets (4), alongside a favorable debt-to-equity score (4). However, its discounted cash flow (1), price-to-earnings (2), and price-to-book (1) scores remain weak, reflecting valuation concerns.

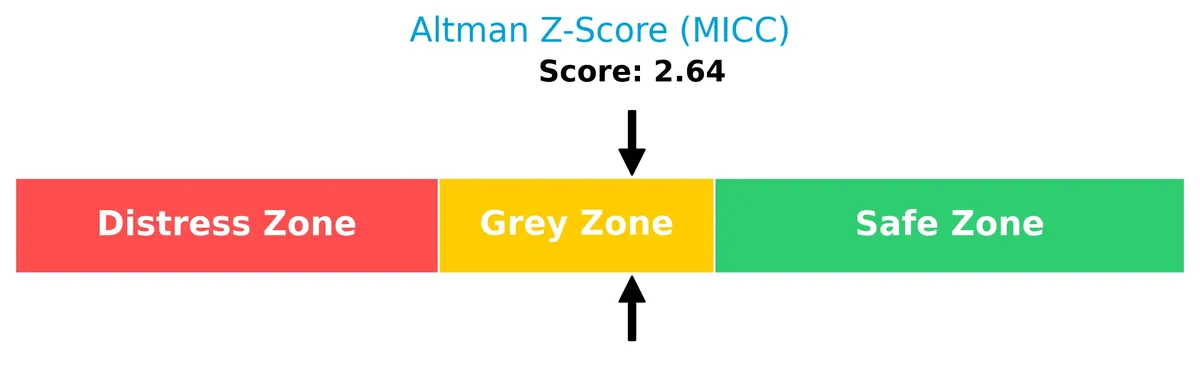

Analysis of the company’s bankruptcy risk

The Altman Z-Score places the company in the grey zone, indicating a moderate risk of bankruptcy and financial uncertainty:

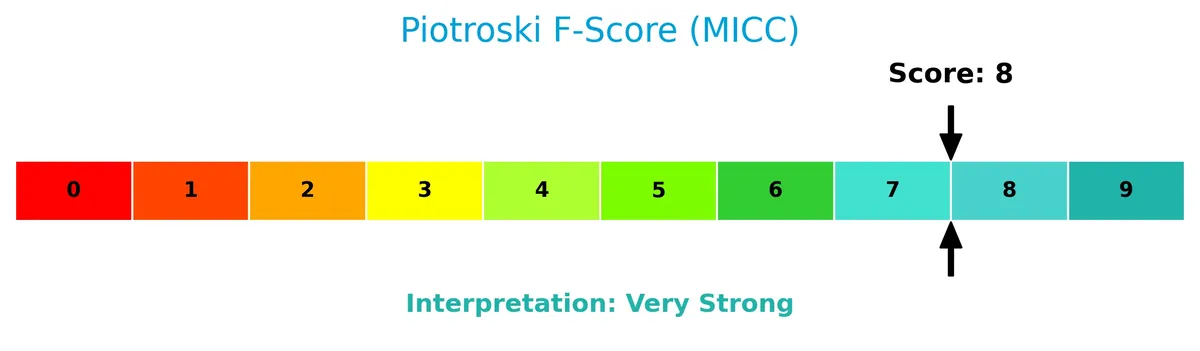

Is the company in good financial health?

The Piotroski Score diagram highlights the company’s solid financial condition and operational efficiency:

With a Piotroski Score of 8, The Magnum Ice Cream Company exhibits very strong financial health, signaling robust profitability and prudent capital management.

Competitive Landscape & Sector Positioning

This analysis explores The Magnum Ice Cream Company N.V.’s positioning within the packaged foods sector. It examines strategic placement, revenue streams, and key competitors. I will assess whether the company holds a distinct competitive advantage in its market.

Strategic Positioning

The Magnum Ice Cream Company N.V. concentrates its product focus exclusively on ice cream within the packaged foods sector. Geographically, it generates over 73% of its 7.7B USD revenue from outside the United States, signaling a predominantly international market exposure.

Key Products & Brands

The Magnum Ice Cream Company N.V. offers a focused portfolio of ice cream products, including its flagship brand:

| Product | Description |

|---|---|

| Magnum Ice Cream | Premium ice cream bars known for rich flavors and a thick chocolate coating. |

Magnum dominates the company’s portfolio, emphasizing premium quality in the ice cream segment. This singular focus reflects the company’s strategy within the packaged foods industry.

Main Competitors

The sector includes 11 competitors, with the table showing the top 10 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| JBS N.V. | 32B |

| The Kraft Heinz Company | 29B |

| General Mills, Inc. | 25B |

| McCormick & Company, Incorporated | 18B |

| Hormel Foods Corporation | 13B |

| The J. M. Smucker Company | 10.3B |

| The Magnum Ice Cream Company N.V. | 9.7B |

| Pilgrim’s Pride Corporation | 9.3B |

| Conagra Brands, Inc. | 8.3B |

| Campbell Soup Company | 8.3B |

The Magnum Ice Cream Company ranks 7th among 11 competitors. Its market cap stands at 28% of the leader JBS N.V. The company is below both the average market cap of the top 10 (16.2B) and the sector median (10.3B). It maintains a 15.1% gap from its nearest competitor above, The J. M. Smucker Company.

Does MICC have a competitive advantage?

The Magnum Ice Cream Company N.V. presents a competitive advantage, as it consistently creates value with a ROIC 2.9% above its WACC, indicating stable profitability. This favorable moat suggests efficient capital allocation despite neutral ROIC growth over recent years.

Looking ahead, MICC’s strong presence in the U.S. and other countries supports expansion opportunities. The company’s focus on the ice cream sector positions it well to capitalize on new product innovation and market penetration in consumer defensive packaged foods.

Comparisons with competitors

Check out how we compare the company to its competitors:

SWOT Analysis

This SWOT analysis highlights The Magnum Ice Cream Company N.V.’s key strategic factors shaping its competitive position and growth prospects.

Strengths

- strong ROE at 46.9%

- favorable debt metrics with low leverage

- stable competitive moat with ROIC > WACC

Weaknesses

- declining net margin and EPS growth

- high P/E and P/B ratios indicate overvaluation

- weak liquidity with quick ratio below 1

Opportunities

- expanding international revenue base

- rising packaged foods demand globally

- potential margin improvement through cost control

Threats

- intense competition in consumer defensive sector

- margin pressure from rising operating expenses

- market volatility affecting stock valuation

Overall, Magnum leverages a solid competitive moat and strong equity returns but faces margin erosion and valuation concerns. The company must focus on operational efficiency and prudent capital allocation to sustain growth and defend its premium positioning.

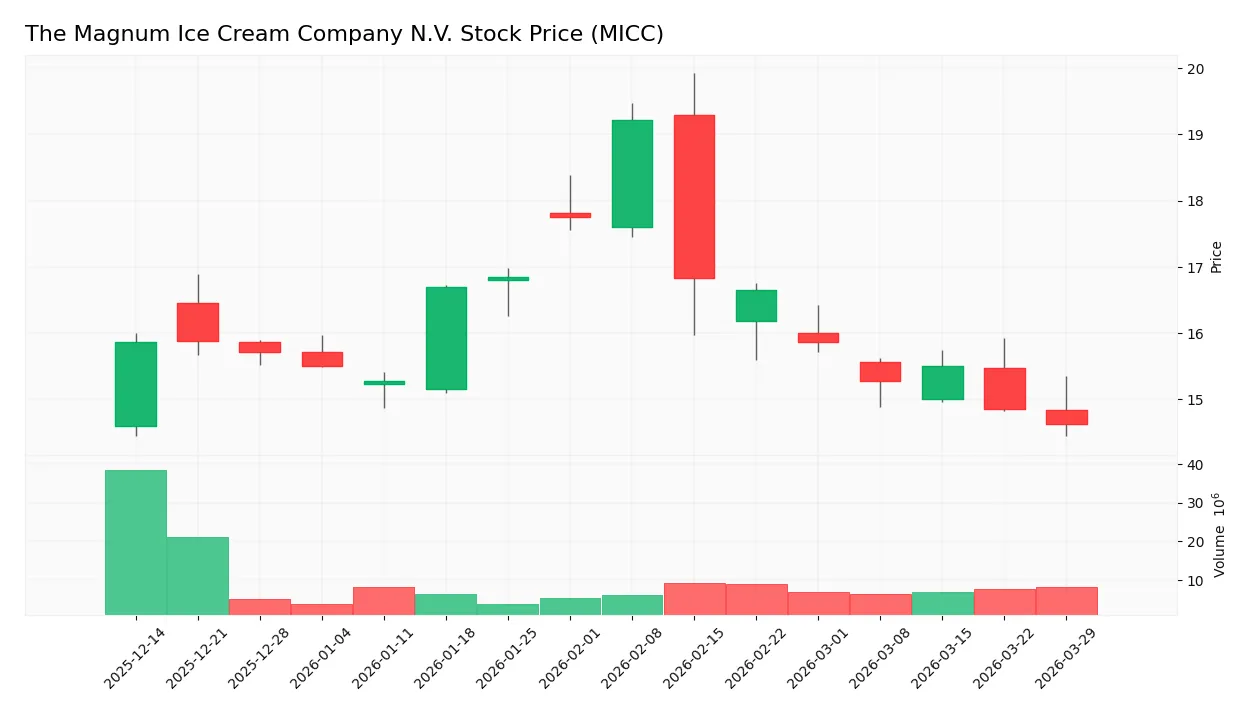

Stock Price Action Analysis

The weekly chart below illustrates The Magnum Ice Cream Company N.V.’s stock price movement over the past 12 months:

Trend Analysis

Over the past 12 months, MICC’s stock price declined by 7.81%, establishing a bearish trend with decelerating downward momentum. The stock traded between a high of 19.22 and a low of 14.63. Recent three-month data shows a continued bearish trend with a 4.25% drop and a slope of -0.19.

Volume Analysis

Trading volume over the last three months shows seller dominance with 56M shares sold versus 29M bought. Total volume is decreasing, indicating waning market participation and cautious investor sentiment amid the ongoing downtrend.

Target Prices

Analysts show a unified target price for The Magnum Ice Cream Company N.V.

| Target Low | Target High | Consensus |

|---|---|---|

| 16 | 16 | 16 |

The single target price of 16 reflects strong analyst confidence and a clear valuation expectation.

Analyst & Consumer Opinions

This section examines recent analyst ratings and consumer feedback on The Magnum Ice Cream Company N.V. (MICC) to gauge market sentiment.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Stock Grades

No verified stock grades were available from recognized analysts for The Magnum Ice Cream Company N.V. Investors must rely on other fundamental and market data to assess its position.

Consumer Opinions

Consumer sentiment around The Magnum Ice Cream Company N.V. (MICC) reflects a passionate customer base with clear praise and pointed critiques.

| Positive Reviews | Negative Reviews |

|---|---|

| “Exceptional flavor variety and quality.” | “Pricing feels high compared to competitors.” |

| “Consistently creamy texture in every bite.” | “Limited availability in some regions.” |

| “Innovative seasonal flavors keep me coming back.” | “Packaging could be more eco-friendly.” |

Overall, consumers praise MICC for superior taste and innovation, which builds strong brand loyalty. However, pricing and distribution limitations pose notable challenges to broader market penetration.

Risk Analysis

Below is a summary of key risks facing The Magnum Ice Cream Company N.V., focusing on likelihood and impact:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Financial Health | Altman Z-Score in grey zone signals moderate bankruptcy risk | Medium | High |

| Valuation | High P/E (28.11) and P/B (13.18) ratios indicate overvaluation risk | High | Medium |

| Liquidity | Quick ratio at 0.74 suggests weak immediate liquidity | Medium | Medium |

| Profitability | Low net margin (3.7%) despite strong ROE (46.88%) | Medium | Medium |

| Market Volatility | Moderate trading volume below average reflects potential liquidity risk | Medium | Low |

The Altman Z-score places MICC in a moderate financial distress zone, warranting caution. Valuation metrics remain stretched relative to industry norms. Liquidity concerns arise from a suboptimal quick ratio, potentially limiting flexibility. Despite a very strong Piotroski score, these risks highlight the need for vigilance given the company’s recent IPO status.

Should You Buy The Magnum Ice Cream Company N.V.?

The Magnum Ice Cream Company N.V. appears to be a profitable business with a durable competitive moat, evidenced by stable ROIC exceeding WACC. While its leverage profile seems manageable, valuation metrics suggest caution. Overall, the company could be seen as a solid B-rated investment candidate.

Strength & Efficiency Pillars

The Magnum Ice Cream Company N.V. maintains solid operational efficiency with a gross margin at a perfect 100.0% and a favorable return on equity of 46.88%. Its return on invested capital (ROIC) stands at 9.17%, comfortably exceeding its weighted average cost of capital (WACC) of 6.31%, indicating the company is a clear value creator. Despite a modest net margin of 3.7%, the firm demonstrates stable profitability and a competitive advantage, supported by favorable asset turnover ratios of 1.06 and fixed asset turnover of 3.43.

Weaknesses and Drawbacks

The company’s Altman Z-Score of 2.64 places it in the grey zone, signaling moderate financial distress risk, which warrants caution. Valuation metrics also raise concerns: a high price-to-earnings (P/E) ratio of 28.11 and a steep price-to-book (P/B) ratio of 13.18 suggest the stock trades at a significant premium. Liquidity indicators are mixed with a borderline current ratio of 1.02 and a weak quick ratio of 0.74, which could pressure short-term solvency. Furthermore, recent seller dominance at 65.97% signals market hesitancy that may weigh on near-term performance.

Our Final Verdict about The Magnum Ice Cream Company N.V.

The company exhibits a fundamentally sound value creation model and strong profitability metrics. However, the grey zone Altman Z-Score and elevated valuation multiples introduce notable risk. Despite stable operational strengths, recent bearish technical trends and seller dominance suggest a cautious stance. This profile may appear attractive for long-term exposure but might warrant a wait-and-see approach for a more favorable entry point given current market pressures.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Goldman Sachs downgrades Magnum Ice Cream Company (MICC) to sell from neutral – here’s why – MSN (Mar 27, 2026)

- Magnum Ice Cream (MICC) senior managers report routine share dealings – Stock Titan (Mar 24, 2026)

- We Think You Can Look Beyond Magnum Ice Cream’s (AMS:MICC) Lackluster Earnings – Yahoo Finance (Mar 26, 2026)

- There May Be Reason For Hope In Magnum Ice Cream’s (AMS:MICC) Disappointing Earnings – simplywall.st (Mar 27, 2026)

- Ben & Jerry’s Foundation joins lawsuit challenging The Magnum Ice Cream Company – Reuters (Mar 23, 2026)

For more information about The Magnum Ice Cream Company N.V., please visit the official website: corporate.magnumicecream.com