Home > Analyses > Technology > SoundHound AI, Inc.

SoundHound AI transforms how people interact with technology through its cutting-edge voice AI platform. Its Houndify suite powers conversational voice assistants that elevate customer experiences across industries. Known for innovation and robust voice recognition technology, the company shapes the future of natural language interfaces. As SoundHound navigates rapid market evolution, I ask: do its fundamentals still justify its current valuation and long-term growth potential?

Table of contents

Business Model & Company Overview

SoundHound AI, Inc., founded in Santa Clara, California, commands a leading position in the voice artificial intelligence space. Its core mission revolves around creating a seamless conversational ecosystem through the Houndify platform. This platform integrates automatic speech recognition, natural language understanding, and embedded voice solutions into a cohesive suite that empowers businesses across industries to enhance customer interaction.

The company’s revenue engine balances software licensing and recurring services tied to its Houndify tools. It leverages strategic exposure across the Americas, Europe, and Asia, enabling global brands to embed conversational AI into their offerings. SoundHound’s competitive advantage lies in its proprietary voice AI technology, which builds a durable economic moat and shapes the future of human–machine interaction.

Financial Performance & Fundamental Metrics

I analyze SoundHound AI, Inc.’s income statement, key financial ratios, and dividend payout policy to assess its financial health and shareholder value.

Income Statement

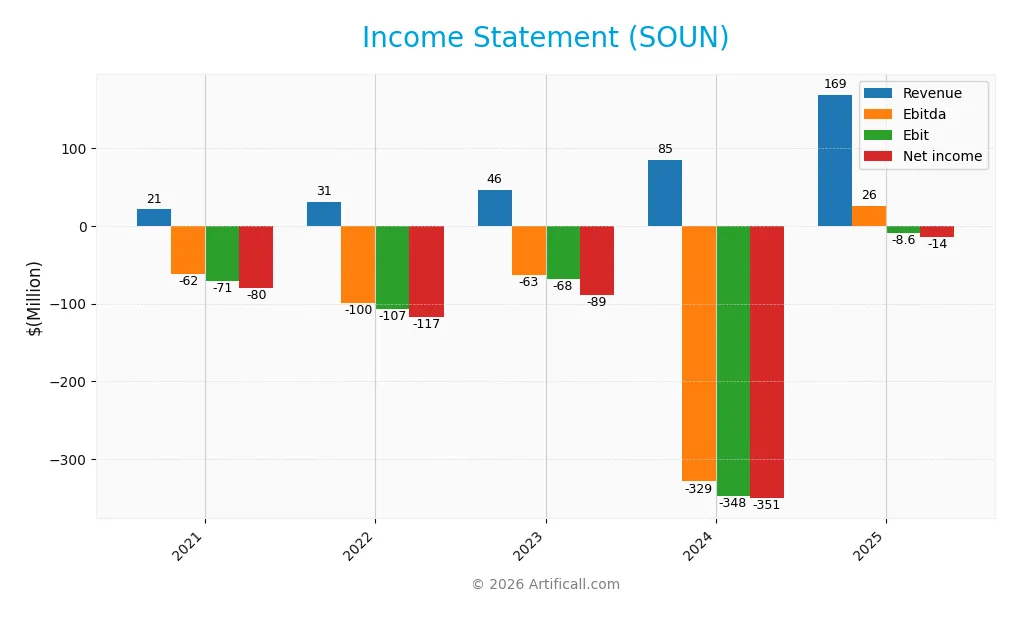

The following table presents SoundHound AI, Inc.’s annual income statement figures for fiscal years 2021 through 2025, highlighting key profitability and expense metrics.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 21.2M | 31.1M | 45.9M | 84.7M | 169.0M |

| Cost of Revenue | 6.6M | 9.6M | 11.3M | 43.3M | 97.4M |

| Operating Expenses | 79.9M | 127.2M | 103.2M | 382.7M | 94.8M |

| Gross Profit | 14.6M | 21.5M | 34.6M | 41.4M | 71.6M |

| EBITDA | -61.7M | -99.7M | -62.6M | -329.1M | 25.5M |

| EBIT | -70.7M | -107.0M | -68.3M | -347.8M | -8.6M |

| Interest Expense | 8.3M | 6.9M | 16.7M | 12.2M | 0.7M |

| Net Income | -79.5M | -116.7M | -88.9M | -350.7M | -14.0M |

| EPS | -0.40 | -0.74 | -0.40 | -1.04 | -0.03 |

| Filing Date | 2022-03-09 | 2023-03-28 | 2024-03-01 | 2025-03-11 | 2026-03-02 |

Income Statement Evolution

SoundHound AI, Inc. shows strong revenue growth, nearly 7x from 2021 to 2025, with a 99% increase in 2025 alone. Gross margin improved to 42.4%, reflecting better cost control. Despite growth, net income remains negative, though losses narrowed significantly. EBIT margin remains negative at -5.1%, indicating ongoing operational challenges.

Is the Income Statement Favorable?

In 2025, fundamentals show improvement with revenue at $169M and gross profit of $71.5M. Operating expenses grew proportionally, but EBITDA turned positive at $25.5M. Net margin is still negative at -8.3%, driven by operating losses and tax expenses. Interest costs remain low at 0.4%, supporting financial stability. Overall, the income statement trends positively but reflects ongoing profitability risks.

Financial Ratios

The following table summarizes key financial ratios for SoundHound AI, Inc. over recent fiscal years:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | -3.75% | -3.75% | -1.94% | -4.14% | -8.29% |

| ROE | 0.23% | 3.19% | -3.16% | -1.92% | -3.02% |

| ROIC | -2.52% | -5.41% | -0.53% | -0.68% | -3.76% |

| P/E | -18.86 | -2.39 | -5.47 | -19.15 | -288.59 |

| P/B | -4.37 | -7.62 | 17.26 | 36.76 | 8.72 |

| Current Ratio | 0.31 | 0.46 | 4.69 | 3.77 | 4.59 |

| Quick Ratio | 0.31 | 0.46 | 4.69 | 3.77 | 4.59 |

| D/E | -0.21 | -1.21 | 3.20 | 0.02 | 0.01 |

| Debt-to-Assets | 149.01% | 116.16% | 59.66% | 0.79% | 0.61% |

| Interest Coverage | -7.83 | -15.33 | -4.10 | -28.05 | -34.73 |

| Asset Turnover | 0.43 | 0.82 | 0.30 | 0.15 | 0.25 |

| Fixed Asset Turnover | 1.29 | 2.69 | 6.82 | 14.28 | 25.14 |

| Dividend Yield | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% |

Evolution of Financial Ratios

From 2021 to 2025, SoundHound AI’s Return on Equity (ROE) remained negative, showing persistent unprofitability. The Current Ratio improved significantly, rising from below 1 to 4.59 by 2025, indicating better short-term liquidity. The Debt-to-Equity Ratio sharply decreased, reaching a minimal 0.01 in 2025, reflecting a substantial reduction in leverage.

Are the Financial Ratios Favorable?

In 2025, profitability ratios such as net margin (-8.29%) and ROE (-3.02%) remain unfavorable, highlighting ongoing losses. Liquidity is mixed: a high Current Ratio (4.59) is flagged unfavorable, while Quick Ratio is favorable. Low leverage metrics, including a 0.01 Debt-to-Equity ratio, are positive. However, poor interest coverage (-12.84) and low asset turnover (0.25) weigh on efficiency. Overall, 64% of ratios are unfavorable.

Shareholder Return Policy

SoundHound AI, Inc. does not pay dividends due to consistent net losses and negative operating cash flows. The company prioritizes reinvestment, likely focusing on growth and R&D given its negative profitability and zero dividend payout ratio.

The firm does not engage in share buybacks. This approach aligns with a growth phase strategy aimed at long-term value creation rather than immediate shareholder returns. However, sustained negative margins and cash flow deficits remain risks to future distribution policies.

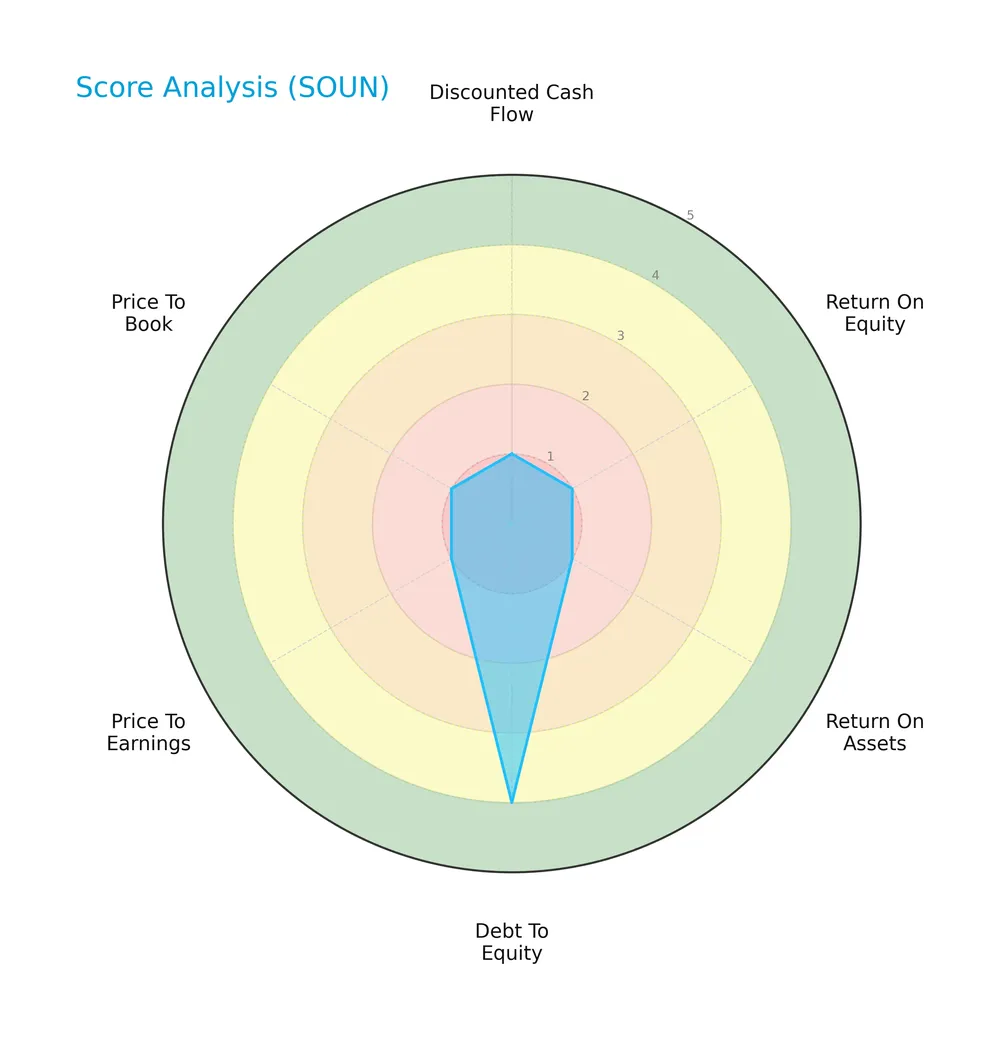

Score analysis

The following radar chart displays key financial scores for SoundHound AI, Inc., illustrating its current valuation and profitability metrics:

SoundHound AI shows very unfavorable scores in discounted cash flow, return on equity, return on assets, price-to-earnings, and price-to-book, each scoring 1. Its debt-to-equity score stands out favorably at 4, indicating relatively conservative leverage.

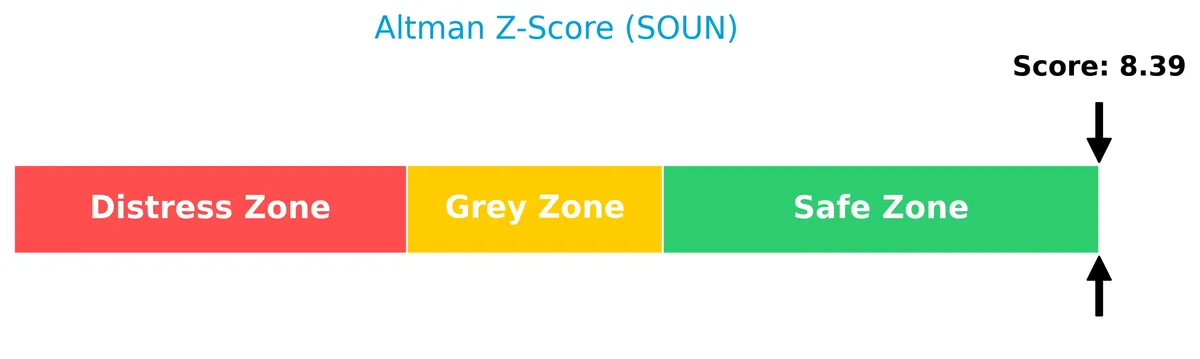

Analysis of the company’s bankruptcy risk

SoundHound AI’s Altman Z-Score places it well within the safe zone, indicating a very low risk of bankruptcy:

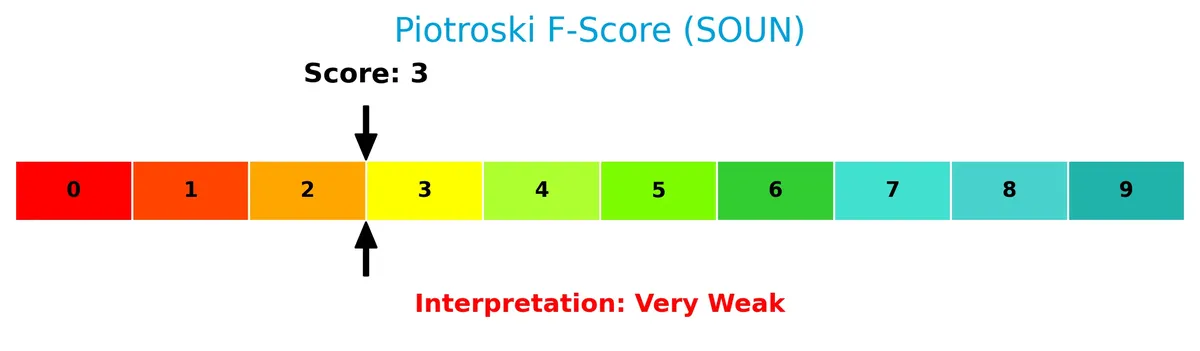

Is the company in good financial health?

This Piotroski diagram highlights the company’s financial strength based on nine fundamental criteria:

With a Piotroski Score of 3, SoundHound AI ranks as very weak in financial health, signaling challenges in profitability, efficiency, or liquidity despite a strong balance sheet.

Competitive Landscape & Sector Positioning

This section examines SoundHound AI, Inc.’s strategic positioning, revenue by segment, key products, main competitors, and competitive advantages. I will assess whether SoundHound AI holds a competitive advantage over its industry peers.

Strategic Positioning

SoundHound AI concentrates on software applications with a clear focus on voice AI platforms. Its product portfolio centers on hosted services, licensing, and professional services, showing significant growth in hosted services. Geographically, it diversifies revenue with dominant exposure in the US and expanding presence in Korea, France, and other markets.

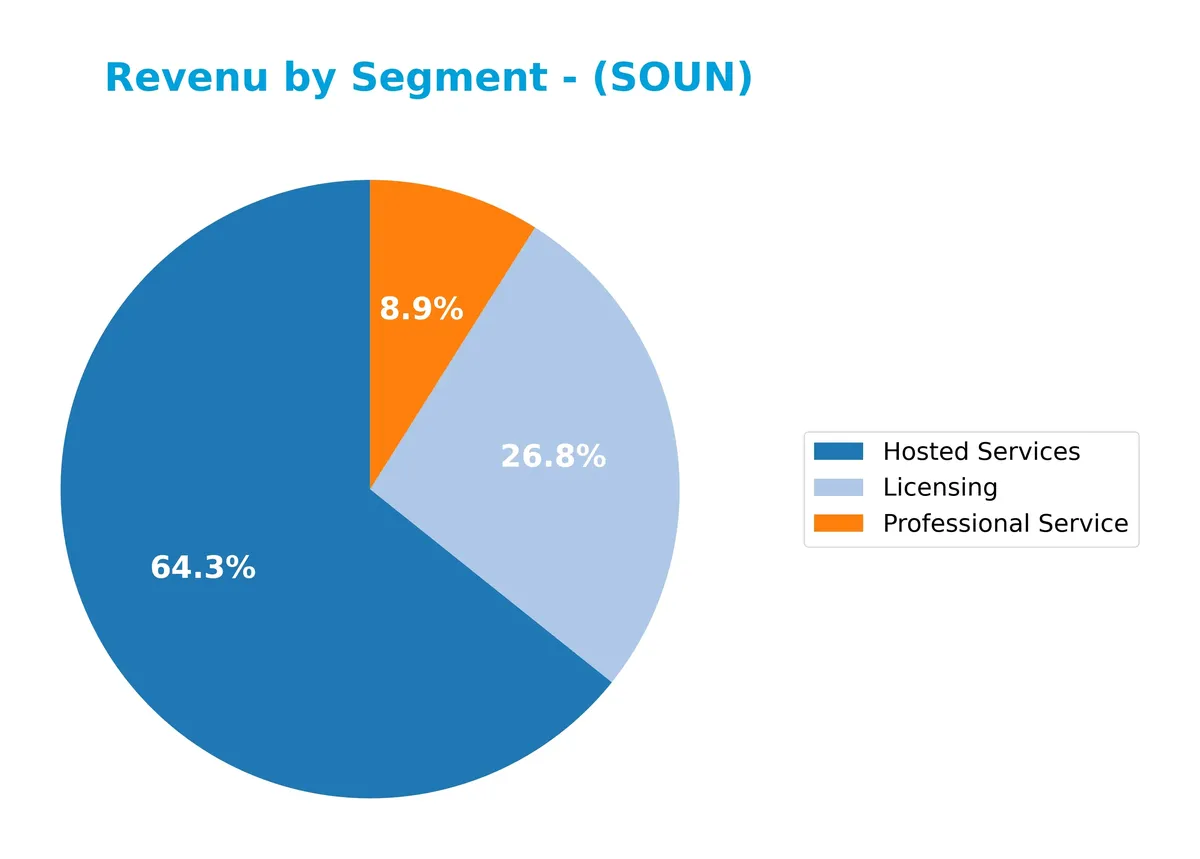

Revenue by Segment

This pie chart displays SoundHound AI, Inc.’s revenue breakdown by segment for fiscal year 2025, highlighting Hosted Services, Licensing, and Professional Service contributions.

Hosted Services dominate SoundHound’s revenue, reaching $108M in 2025, nearly doubling from $57M in 2024. Licensing and Professional Service grew more modestly to $45M and $15M, respectively. The rapid acceleration in Hosted Services signals strong demand for scalable cloud offerings, but reliance on this segment raises concentration risk if market dynamics shift. Licensing’s rebound after a dip in 2024 reflects renewed contract wins.

Key Products & Brands

The following table outlines SoundHound AI’s main products and brands with their core functionalities:

| Product | Description |

|---|---|

| Houndify Platform | An independent voice AI platform offering tools like automatic speech recognition, natural language understanding, wake words, custom domains, text-to-speech, and embedded voice solutions. |

| Hosted Services | Cloud-based voice AI services enabling businesses to integrate conversational experiences for customers. |

| Licensing | License agreements allowing clients to use SoundHound’s voice AI technology within their own products. |

| Professional Service | Customized support and implementation services to help clients deploy and optimize voice AI solutions. |

SoundHound AI’s product suite centers on voice AI technology, with the Houndify platform as the core. Revenue growth in Hosted Services shows expanding adoption, while Licensing and Professional Services complement the technology deployment.

Main Competitors

SoundHound AI, Inc. faces competition from 33 companies in its sector. The table below lists the top 10 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| Salesforce, Inc. | 242.5B |

| Shopify Inc. | 209.6B |

| AppLovin Corporation | 209.0B |

| Intuit Inc. | 175.2B |

| Uber Technologies, Inc. | 172.2B |

| ServiceNow, Inc. | 153.0B |

| Cadence Design Systems, Inc. | 84.5B |

| Snowflake Inc. | 73.4B |

| Autodesk, Inc. | 61.2B |

| Workday, Inc. | 54.9B |

SoundHound AI ranks 29th among 33 competitors, with a market cap just 1.49% of the sector leader, Salesforce. The company sits well below the average 143.6B market cap of the top 10 and the sector median of 18.8B. It holds a significant 106.9% gap above its nearest competitor, highlighting a steep climb to higher tiers.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does SoundHound AI have a competitive advantage?

SoundHound AI currently lacks a strong competitive advantage, as it is shedding value with a ROIC significantly below its WACC. However, its profitability is improving, indicating some operational progress.

Looking ahead, SoundHound AI plans to expand its voice AI platform across industries, leveraging growth in conversational voice assistants and new international markets like the United States and Korea to capture emerging opportunities.

SWOT Analysis

This analysis highlights SoundHound AI’s core strengths, weaknesses, opportunities, and threats to guide strategic focus.

Strengths

- Rapid revenue growth (696.9% over 5 years)

- Strong gross margin (42.4%)

- Low debt levels (D/E 0.01)

Weaknesses

- Negative net margin (-8.3%)

- ROIC below WACC (-3.8% vs 17.2%)

- Weak profitability metrics (negative ROE and interest coverage)

Opportunities

- Expansion in US market with $108M revenue in 2025

- Growing demand for voice AI across industries

- Increasing international sales (notably Korea and France)

Threats

- High beta (2.88) implies stock volatility

- Intense competition in AI software

- Profitability challenges may limit scaling

SoundHound AI shows impressive top-line growth and solid gross margins but struggles with profitability and capital efficiency. The company must leverage its market expansion opportunities while addressing operational inefficiencies to avoid margin pressure and sustain value creation.

Stock Price Action Analysis

The weekly stock chart below displays SoundHound AI, Inc.’s price movements over the past 12 months, highlighting key highs and lows alongside recent volatility and trend shifts:

Trend Analysis

Over the past year, SOUN’s stock price rose 96.8%, reflecting a strong bullish trend with decelerating momentum. The price ranged from a low of 3.55 to a high of 23.95. In the recent 11 weeks, the price dropped 21.78%, showing a short-term bearish trend with low volatility.

Volume Analysis

In the last three months, trading volume increased but showed slight seller dominance with buyers at 43.57%. This shift from the overall buyer-driven market suggests waning investor confidence and increased selling pressure in recent weeks.

Target Prices

Analysts set a target price consensus for SoundHound AI, Inc. indicating moderate upside potential.

| Target Low | Target High | Consensus |

|---|---|---|

| 11 | 15 | 13.33 |

The consensus target of 13.33 suggests analysts expect a modest appreciation from current levels, with a reasonable range of 11 to 15.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section examines analyst ratings and consumer feedback to provide a balanced view of SoundHound AI, Inc.’s market perception.

Stock Grades

The latest analyst grades for SoundHound AI, Inc. reveal a consistent positive outlook from leading firms:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| HC Wainwright & Co. | Maintain | Buy | 2026-03-02 |

| Piper Sandler | Maintain | Neutral | 2026-02-27 |

| Piper Sandler | Maintain | Neutral | 2026-01-05 |

| Cantor Fitzgerald | Upgrade | Overweight | 2025-12-12 |

| DA Davidson | Maintain | Buy | 2025-11-18 |

| Piper Sandler | Maintain | Neutral | 2025-11-07 |

| HC Wainwright & Co. | Maintain | Buy | 2025-10-16 |

| HC Wainwright & Co. | Maintain | Buy | 2025-09-17 |

| Wedbush | Maintain | Outperform | 2025-09-11 |

| DA Davidson | Maintain | Buy | 2025-09-10 |

The consensus favors a Buy rating, with multiple firms maintaining positive stances and Cantor Fitzgerald notably upgrading to Overweight. Neutral ratings from Piper Sandler offer some caution but no outright negative assessments.

Consumer Opinions

SoundHound AI, Inc. inspires a mix of enthusiasm and caution among its users.

| Positive Reviews | Negative Reviews |

|---|---|

| “Excellent voice recognition accuracy and speed.” | “App occasionally misinterprets commands.” |

| “Innovative AI features set it apart from competitors.” | “User interface feels cluttered and complex.” |

| “Reliable integration with smart home devices.” | “Customer support response times are slow.” |

Consumers consistently praise SoundHound AI’s accuracy and innovation. However, interface complexity and support delays remain notable pain points. This feedback suggests strong product potential tempered by execution risks.

Risk Analysis

Below is a table summarizing key risks facing SoundHound AI, Inc., highlighting their likelihood and potential impact:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Profitability | Negative net margin (-8.29%) signals ongoing losses and weak earnings power. | High | High |

| Financial Health | Low Piotroski score (3) indicates weak financial strength and operational risks. | High | Medium |

| Valuation | Elevated price-to-book ratio (8.72) suggests possible overvaluation risk. | Medium | Medium |

| Leverage & Debt | Very low debt (D/E 0.01) reduces financial distress risk but limits leverage benefits. | Low | Low |

| Liquidity | Strong current and quick ratios (4.59) indicate good short-term liquidity. | Low | Low |

| Earnings Quality | Negative return on equity (-3.02%) and return on invested capital (-3.76%) imply inefficient capital use. | High | High |

| Market Volatility | High beta (2.88) exposes the stock to significant price swings in volatile markets. | High | Medium |

| Interest Coverage | Negative interest coverage (-12.84) raises concerns over ability to service debt if borrowing rises. | Medium | High |

SoundHound’s greatest risks stem from persistent unprofitability and weak capital returns amid a highly volatile market environment. Despite a strong Altman Z-Score indicating low bankruptcy risk, poor operational metrics and valuation multiples warn of underlying financial fragility. Investors must weigh these factors carefully given the company’s early-stage growth profile and competitive technology sector.

Should You Buy SoundHound AI, Inc.?

SoundHound AI appears to be improving profitability with a growing ROIC, yet it continues to shed value, suggesting a slightly unfavorable moat. Despite manageable leverage and a safe Altman Z-score, its overall rating remains a cautious C-, reflecting operational challenges.

Strength & Efficiency Pillars

SoundHound AI, Inc. shows strong operational efficiency with a gross margin of 42.36%, reflecting solid core profitability. Despite a negative ROIC of -3.76% trailing a WACC of 17.21%, the company’s EBIT margin of -5.09% and net margin of -8.29% highlight ongoing challenges in translating revenue into profit. Its negligible debt-to-equity ratio of 0.01 signals cautious financial leverage. The Altman Z-Score of 8.39 places SoundHound comfortably in the safe zone, indicating strong solvency despite current profitability issues.

Weaknesses and Drawbacks

Although SoundHound’s solvency is secure, its financial profile reveals notable weaknesses. The ROE at -3.02% and negative net margin underline persistent unprofitability. A high price-to-book ratio of 8.72 suggests the stock trades at a premium, raising valuation concerns. The interest coverage ratio is -12.84, indicating insufficient earnings to cover interest expenses, a red flag for creditors. Recently, seller dominance at 56.43% signals short-term market pressure that may suppress near-term price appreciation.

Our Final Verdict about SoundHound AI, Inc.

SoundHound AI’s long-term fundamentals appear mixed. The company benefits from a strong solvency base and rapid revenue growth but struggles with consistent profitability and market valuation pressures. Despite a bullish overall trend, recent seller dominance suggests caution. This profile might appeal to investors with a higher risk tolerance, but conservative capital could find the current setup too speculative pending improved earnings and market sentiment.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- SoundHound AI, Inc. (SOUN) Reports Q4 Loss, Beats Revenue Estimates – Nasdaq (Feb 26, 2026)

- SoundHound AI Reports Record Annual Revenue of $169 Million, Up Nearly 100%, Forecasts Strong Growth – GlobeNewswire (Feb 26, 2026)

- SoundHound AI (NASDAQ:SOUN) Shares Gap Down on Analyst Downgrade – MarketBeat (Mar 02, 2026)

- Earnings call transcript: SoundHound AI beats Q4 2025 EPS forecast, stock rises – Investing.com (Feb 26, 2026)

- What Analysts Are Saying About SoundHound AI Stock – Benzinga (Mar 02, 2026)

For more information about SoundHound AI, Inc., please visit the official website: soundhound.com