Home > Analyses > Real Estate > SBA Communications Corporation

SBA Communications powers the wireless world by owning and operating critical communication towers across the Americas and South Africa. It dominates the specialty REIT sector with a vast portfolio that supports leading wireless providers through long-term site leases. Renowned for innovation and operational excellence, SBA shapes how millions connect daily. As 5G and beyond expand demand, I ask: does SBA’s financial strength and growth outlook still justify its premium valuation?

Table of contents

Business Model & Company Overview

SBA Communications Corporation, founded in 1999 and based in Boca Raton, FL, stands as a leading owner and operator of wireless communications infrastructure. Its ecosystem centers on multi-tenant communication sites, enabling wireless service providers to expand coverage efficiently. With 1,720 employees, SBA dominates the specialty REIT industry across the Americas and South Africa, delivering critical backbone support for mobile networks.

The company’s revenue engine balances long-term site leasing with site development services, creating stable, recurring cash flows. SBA’s strategic footprint spans North, Central, South America, and South Africa, allowing it to capitalize on global wireless growth trends. Its competitive advantage lies in scale, diversified markets, and high barriers to entry, securing its role as a keystone in the wireless infrastructure sector.

Financial Performance & Fundamental Metrics

I will analyze SBA Communications Corporation’s income statement, key financial ratios, and dividend payout policy to assess its core financial health and shareholder returns.

Income Statement

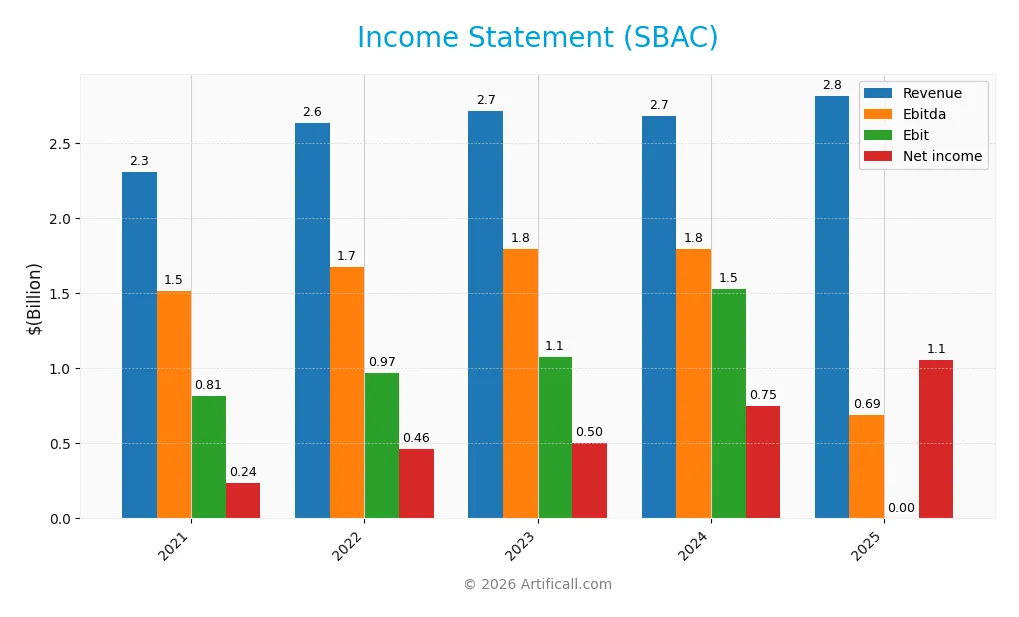

This table summarizes SBA Communications Corporation’s key income statement metrics over the last five fiscal years.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 2.31B | 2.63B | 2.71B | 2.68B | 2.82B |

| Cost of Revenue | 573M | 695M | 634M | 608M | 0 |

| Operating Expenses | 953M | 1.01B | 1.15B | 636M | 1.47B |

| Gross Profit | 1.74B | 1.94B | 2.08B | 2.07B | 0 |

| EBITDA | 1.51B | 1.68B | 1.79B | 1.79B | 690M |

| EBIT | 814M | 968M | 1.08B | 1.53B | 0 |

| Interest Expense | 0 | 0 | 0 | 0 | -468M |

| Net Income | 238M | 461M | 502M | 750M | 1.05B |

| EPS | 2.17 | 4.27 | 4.64 | 6.96 | 9.83 |

| Filing Date | 2022-03-01 | 2023-03-01 | 2024-02-28 | 2025-02-26 | 2026-02-26 |

Income Statement Evolution

Between 2021 and 2025, SBA Communications’ revenue rose 22% to 2.82B, showing steady top-line growth. Net income surged over 340%, reaching 1.05B in 2025, driven by improved net margins. However, gross profit and EBIT margins fell sharply in 2025, indicating margin compression despite higher revenue. Operating expenses grew in line with revenue, maintaining cost discipline.

Is the Income Statement Favorable?

The 2025 income statement reflects a favorable financial position overall. Net margin expanded to 37.4%, supported by a significant reduction in interest expense as a percentage of revenue. Earnings per share jumped 41%, underlining strong profitability gains. Yet, the absence of reported gross profit and EBIT values signals caution. Investors should note mixed margin trends alongside solid bottom-line growth.

Financial Ratios

The following table summarizes key financial ratios for SBA Communications Corporation from 2021 to 2025, providing a snapshot of profitability, valuation, liquidity, leverage, and efficiency:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 10.3% | 17.5% | 18.5% | 28.0% | 37.4% |

| ROE | -4.5% | -8.7% | -9.7% | -14.7% | -21.7% |

| ROIC | 7.8% | 8.0% | 8.6% | 12.6% | 12.1% |

| P/E | 182 | 66 | 55 | 29 | 20 |

| P/B | -8.18 | -5.81 | -5.34 | -4.31 | -4.27 |

| Current Ratio | 1.00 | 0.69 | 0.36 | 1.10 | 0.29 |

| Quick Ratio | 1.00 | 0.69 | 0.36 | 1.10 | 0.29 |

| D/E | -2.75 | -2.88 | -2.80 | -3.08 | -0.90 |

| Debt-to-Assets | 148% | 143% | 142% | 138% | 38% |

| Interest Coverage | 0 | 0 | 0 | 0 | -2.87 |

| Asset Turnover | 0.24 | 0.25 | 0.27 | 0.23 | 0.24 |

| Fixed Asset Turnover | 0.40 | 0.40 | 0.42 | 0.42 | 0.39 |

| Dividend Yield | 0.59% | 1.00% | 1.34% | 1.93% | 2.31% |

Evolution of Financial Ratios

SBA Communications Corporation’s Return on Equity (ROE) has declined significantly, reaching -21.71% in 2025, signaling deteriorating shareholder returns. The Current Ratio sharply dropped from above 1.0 in 2024 to 0.29 in 2025, indicating weakening liquidity. Meanwhile, the Debt-to-Equity ratio remained negative and favorable, reflecting the company’s unusual capital structure and leverage position.

Are the Financial Ratios Fovorable?

In 2025, SBA exhibits mixed financial health. Profitability shows strength with a net margin of 37.43% and ROIC at 12.06%, both favorable versus the 6.91% WACC. Liquidity ratios are weak, with current and quick ratios at 0.29, raising red flags. Leverage is favorable with a negative debt-to-equity ratio, but asset turnover and interest coverage are unfavorable. Dividend yield at 2.31% is positive. Overall, ratios are neutral, balancing strengths and risks.

Shareholder Return Policy

SBA Communications maintains a consistent dividend payout, with a 2025 payout ratio near 45% and a dividend yield around 2.3%. Dividends per share have steadily increased from $2.28 in 2021 to $4.47 in 2025, supported by solid free cash flow coverage.

The company also engages in share buybacks, complementing its dividend strategy. This balanced approach suggests a focus on sustainable long-term shareholder value, though investors should monitor leverage and cash ratios as potential risks.

Score analysis

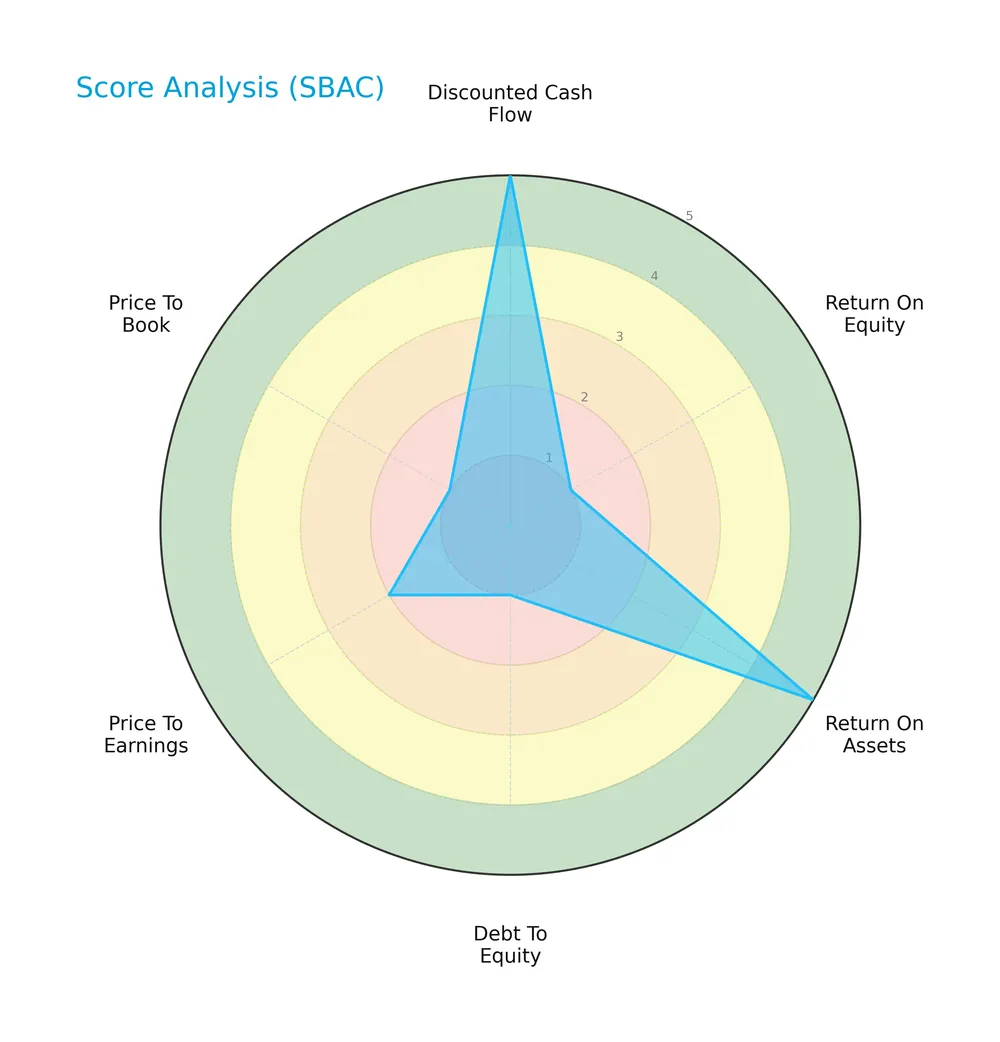

Here is a radar chart illustrating key valuation and financial performance scores for SBA Communications Corporation:

The company scores very favorably in discounted cash flow and return on assets, signaling strong cash generation and asset efficiency. However, it shows significant weakness in return on equity, debt-to-equity, price-to-earnings, and price-to-book metrics, highlighting risks in profitability and valuation.

Analysis of the company’s bankruptcy risk

The Altman Z-Score places SBA Communications in the distress zone, indicating a high probability of financial distress and potential bankruptcy risk:

Is the company in good financial health?

The Piotroski Score diagram presents SBA Communications’ financial strength assessment:

With a score of 6, SBA Communications demonstrates average financial health, suggesting moderate strength but room for improvement in profitability, leverage, and liquidity factors.

Competitive Landscape & Sector Positioning

This analysis explores SBA Communications Corporation’s role within the REIT – Specialty sector. I will evaluate its strategic positioning, revenue streams, and key competitors. Next, I will determine whether SBA Communications holds a competitive advantage over its rivals.

Strategic Positioning

SBA Communications concentrates on wireless infrastructure, generating most revenue from domestic site leasing (1.86B in 2024) with significant international exposure (665M) and a smaller, stable site development segment (153M). This reflects a focused product portfolio with geographic diversification across the Americas and South Africa.

Revenue by Segment

The pie chart illustrates SBA Communications Corporation’s revenue distribution across key segments for the fiscal year 2024. It highlights the relative contribution of domestic and international site leasing alongside site development construction.

Domestic Site Leasing dominates SBA’s revenue at $1.86B in 2024, reflecting steady growth since 2011. International Site Leasing contributes $665M, showing moderate expansion but slight recent volatility. Site Development Construction has declined to $153M, signaling a strategic shift away from this lower-margin segment. The concentration in leasing revenue underscores SBA’s focus on stable, recurring cash flows amid sector cyclical pressures.

Key Products & Brands

The table below outlines SBA Communications Corporation’s primary products and brands with brief descriptions:

| Product | Description |

|---|---|

| Domestic Site Leasing | Leasing antenna space on multi-tenant communication sites across the United States to wireless providers under long-term contracts. |

| International Site Leasing | Leasing antenna space in international markets including Central and South America, and South Africa. |

| Site Development Construction | Providing site development and construction services for wireless communications infrastructure. |

SBA Communications generates most revenue from leasing antenna space domestically and internationally. Site development construction complements the leasing business, supporting infrastructure expansion. These offerings position SBA as a key wireless infrastructure provider in multiple regions.

Main Competitors

There are 6 main competitors in the Real Estate REIT – Specialty sector; the table lists the top 6 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| American Tower Corporation | 81.8B |

| Equinix, Inc. | 74.5B |

| Crown Castle Inc. | 38.6B |

| Iron Mountain Incorporated | 24.6B |

| SBA Communications Corporation | 20.7B |

| Weyerhaeuser Company | 17.2B |

SBA Communications ranks 5th among its 6 competitors. Its market cap is 25.0% of the leader, American Tower. SBA is below both the average market cap of the top 10 (43B) and the sector median (31.6B). The company is 20.15% smaller than the next competitor above, Iron Mountain, indicating a moderate gap in scale.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does SBA Communications have a competitive advantage?

SBA Communications demonstrates a strong competitive advantage, evidenced by a very favorable moat rating and a ROIC exceeding its WACC by over 5%. The company efficiently uses invested capital and sustains growing profitability.

Looking ahead, SBA plans to expand its wireless infrastructure footprint across the Americas and South Africa, capitalizing on long-term site leasing contracts and potential new development services. This positions SBA well to capture future industry growth opportunities.

SWOT Analysis

This SWOT analysis highlights SBA Communications Corporation’s core strengths and challenges to guide strategic positioning.

Strengths

- Leading wireless infrastructure owner in Americas and South Africa

- Strong net margin at 37.4%

- Growing ROIC indicating value creation

Weaknesses

- Very low current and quick ratios (0.29) signaling liquidity risk

- Negative ROE and weak interest coverage

- Asset turnover below industry norms

Opportunities

- Expanding wireless demand and 5G rollout

- Long-term lease contracts provide stable cash flows

- Potential growth in site development services

Threats

- Rising interest rates increasing debt costs

- Competitive pressure from new infrastructure providers

- Regulatory changes impacting lease agreements

SBA Communications shows a solid competitive moat with high profitability and growth in invested capital returns. However, liquidity challenges and leverage risks require cautious financial management. The company should leverage its market leadership to capitalize on wireless expansion while addressing its balance sheet vulnerabilities.

Stock Price Action Analysis

The weekly stock chart of SBA Communications Corporation shows price movements and volatility over the past 100 weeks:

Trend Analysis

Over the past 12 months, SBAC’s stock price declined by 9.95%, indicating a bearish trend with accelerating downward momentum. The price ranged between a high of 247.47 and a low of 180.74. Volatility is elevated, with a standard deviation of 17.29, signaling significant price fluctuations.

Volume Analysis

In the last three months, trading volume increased but remains seller-driven, with sellers accounting for over 69% of activity. Buyer dominance dropped to 30.51%, suggesting cautious investor sentiment and persistent selling pressure despite rising market participation.

Target Prices

Analysts set a robust target consensus for SBA Communications Corporation.

| Target Low | Target High | Consensus |

|---|---|---|

| 205 | 260 | 224.8 |

The target range from 205 to 260 signals strong confidence in SBA’s growth potential. The consensus price of 224.8 suggests a favorable upside compared to current levels.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section presents a detailed review of SBA Communications Corporation’s analyst ratings and consumer feedback.

Stock Grades

Here are the latest verified stock grades from reputable financial institutions for SBA Communications Corporation (SBAC):

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| UBS | Maintain | Buy | 2026-01-20 |

| Scotiabank | Maintain | Sector Perform | 2026-01-14 |

| JP Morgan | Maintain | Neutral | 2026-01-12 |

| Wells Fargo | Maintain | Equal Weight | 2025-12-16 |

| Barclays | Maintain | Overweight | 2025-12-01 |

| Barclays | Maintain | Overweight | 2025-11-17 |

| RBC Capital | Maintain | Outperform | 2025-11-10 |

| TD Cowen | Maintain | Buy | 2025-11-04 |

| BMO Capital | Maintain | Market Perform | 2025-11-04 |

| Wells Fargo | Maintain | Equal Weight | 2025-10-20 |

The consensus reveals a stable outlook with most firms maintaining positive ratings, predominantly “Buy” or equivalent. No downgrades or negative shifts appeared across these well-known analysts.

Consumer Opinions

SBA Communications Corporation enjoys a mixed but generally favorable reception from its user base, reflecting a solid reputation in wireless infrastructure.

| Positive Reviews | Negative Reviews |

|---|---|

| Reliable network performance across sites | Customer service response times lag |

| Strong infrastructure supporting 5G rollout | Occasional billing inaccuracies |

| Proactive maintenance reduces downtime | Limited transparency on pricing |

Consumers appreciate SBA’s robust infrastructure and reliability, crucial for network stability. However, concerns around customer support and billing indicate areas needing improvement for enhanced client trust.

Risk Analysis

Below is a summary table outlining key risks facing SBA Communications Corporation as of 2026:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Financial Health | Altman Z-Score indicates high bankruptcy risk (0.45, distress zone). | High | Very High |

| Liquidity | Critically low current and quick ratios (0.29), weak short-term liquidity. | High | High |

| Profitability | Negative return on equity (-21.7%) despite strong net margin (37.4%). | Medium | Medium |

| Leverage | Debt to equity score very unfavorable; leverage management is weak. | Medium | High |

| Operational Efficiency | Low asset turnover (0.24) and fixed asset turnover (0.39) suggest underutilization. | Medium | Medium |

| Interest Coverage | Interest coverage near zero, risking inability to service debt. | High | High |

The most pressing risks lie in SBA’s financial stability. The Altman Z-Score signals severe distress, implying elevated bankruptcy probability. Liquidity constraints compound this risk, with current and quick ratios well below healthy benchmarks. Negative ROE and poor interest coverage underline potential profitability and solvency challenges. These factors warrant cautious monitoring amid a challenging sector environment.

Should You Buy SBA Communications Corporation?

SBA Communications Corporation appears to be a company with a very favorable competitive moat supported by growing ROIC, suggesting strong value creation. However, its debt profile and profitability metrics show vulnerabilities, reflected in a moderate overall rating of B-.

Strength & Efficiency Pillars

SBA Communications Corporation exhibits strong operational margins, with a net margin of 37.43% indicating robust profitability. Its return on invested capital (ROIC) stands at 12.06%, comfortably exceeding its weighted average cost of capital (WACC) of 6.91%, confirming the company as a clear value creator. Despite a negative return on equity (-21.71%), the growing ROIC trend and favorable interest expense ratio (-16.62%) underscore operational efficiency and a sustainable competitive advantage.

Weaknesses and Drawbacks

The company is currently in financial distress, as reflected by an Altman Z-Score of 0.45, signaling a high bankruptcy risk. This solvency concern overshadows profitability strengths. Additionally, SBA Communications suffers from poor liquidity ratios, with a current ratio of 0.29, indicating potential short-term cash flow issues. Its market valuation shows mixed signals; a neutral P/E of 19.68 contrasts with an unusual negative P/B ratio (-4.27), raising questions about accounting or asset valuation. Seller dominance at 69.49% in recent trading adds near-term pressure.

Our Final Verdict about SBA Communications Corporation

Despite operational strengths and value creation, the company’s placement in the distress zone due to an Altman Z-Score of 0.45 makes its investment profile highly speculative. The solvency risk outweighs favorable margins and growth trends. Investors should approach with caution, as the financial health challenges imply that SBA Communications may be too risky for conservative capital at this stage.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- SBA Communications (SBAC) Q4 FFO and Revenues Miss Estimates – Yahoo Finance (Feb 26, 2026)

- SBA Communications Corporation Reports Fourth Quarter 2025 Results; Provides Full Year 2026 Outlook; and Declares Quarterly Cash Dividend – Stock Titan (Feb 26, 2026)

- SBA Communications Corporation Reports Fourth Quarter 2025 Results – TradingView (Feb 26, 2026)

- SBA Communications Corp (SBAC) Q4 2025 Earnings Call Highlights: – GuruFocus (Feb 27, 2026)

- SBA Communications Corp (NASDAQ:SBAC) Reports Mixed Q4 2025 Results, Misses AFFO Estimates – ChartMill (Feb 26, 2026)

For more information about SBA Communications Corporation, please visit the official website: sbasite.com