Home > Analyses > Technology > Rubrik, Inc.

Rubrik, Inc. revolutionizes how enterprises protect and recover their most critical data. Its cutting-edge software safeguards unstructured and cloud data across diverse sectors, from finance to healthcare. Known for its innovative cyber recovery and threat analytics solutions, Rubrik sets the industry standard in data security infrastructure. As the company navigates rapid growth and evolving cyber threats, I ask: do its fundamentals still support its ambitious market valuation and expansion prospects?

Table of contents

Business Model & Company Overview

Rubrik, Inc., founded in 2013 and headquartered in Palo Alto, California, stands as a leader in software infrastructure focused on data security. The company crafts a unified ecosystem of enterprise, cloud, and SaaS data protection solutions. Its mission centers on safeguarding unstructured data and enabling cyber recovery across diverse sectors, from finance to healthcare, reflecting a broad and vital market presence.

Rubrik generates revenue by blending software licenses with recurring cloud services, creating a resilient and scalable model. Its solutions hold traction in the Americas, Europe, and Asia, underscoring global reach. The company’s competitive advantage lies in integrating data threat analytics with robust protection, building a durable economic moat that influences the future of data security worldwide.

Financial Performance & Fundamental Metrics

I will analyze Rubrik, Inc.’s income statement, key financial ratios, and dividend payout policy to assess its operational efficiency and shareholder returns.

Income Statement

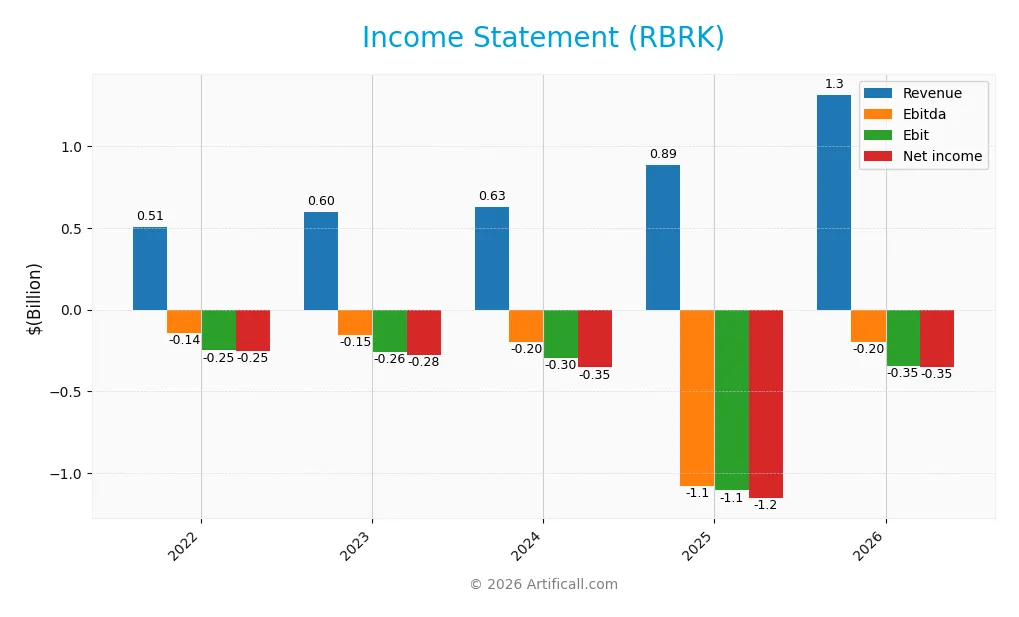

The table below summarizes Rubrik, Inc.’s annual income statement figures for 2022 through 2026, showing key profitability and expense metrics.

| 2022 | 2023 | 2024 | 2025 | 2026 | |

|---|---|---|---|---|---|

| Revenue | 506M | 600M | 628M | 887M | 1.32B |

| Cost of Revenue | 236M | 280M | 238M | 266M | 262M |

| Operating Expenses | 520M | 582M | 696M | 1.75B | 1.40B |

| Gross Profit | 270M | 320M | 390M | 621M | 1.05B |

| EBITDA | -145M | -154M | -196M | -1.08B | -198M |

| EBIT | -250M | -257M | -297M | -1.11B | -345M |

| Interest Expense | 0 | 12M | 30M | 41M | 17M |

| Net Income | -254M | -278M | -354M | -1.15B | -349M |

| EPS | -1.45 | -1.58 | -2.01 | -7.48 | -1.78 |

| Filing Date | 2022-01-31 | 2023-01-31 | 2024-01-31 | 2025-03-20 | 2026-03-19 |

Income Statement Evolution

Rubrik, Inc. shows strong revenue growth, up 160% from 2022 to 2026, with a 48% increase in the last year alone. Gross margins improved to 80.1%, reflecting efficient cost management. However, net income remains negative despite a 47% improvement in net margin, signaling ongoing profitability challenges. Operating expenses grew in line with revenue.

Is the Income Statement Favorable?

In 2026, Rubrik posted $1.32B revenue with a gross profit of $1.05B. Despite a favorable gross margin, the company reported a net loss of $349M, with a negative EBIT margin of -26.24%. Interest expense remains low at 1.31% of revenue. Overall, fundamentals show improving top-line growth but persistent bottom-line deficits, suggesting cautious interpretation of profitability trends.

Financial Ratios

The table below presents key financial ratios for Rubrik, Inc. over the past five fiscal years, offering a snapshot of profitability, liquidity, leverage, and valuation metrics:

| Ratios | 2022 | 2023 | 2024 | 2025 | 2026 |

|---|---|---|---|---|---|

| Net Margin | -50% | -46% | -56% | -130% | -27% |

| ROE | 243% | 75% | 50% | 209% | 67% |

| ROIC | -133% | -76% | -141% | -235% | -24% |

| P/E | -26 | -23 | -18 | -10 | -32 |

| P/B | -62 | -17 | -9 | -20 | -21 |

| Current Ratio | 0.98 | 1.17 | 0.84 | 1.13 | 1.69 |

| Quick Ratio | 0.97 | 1.14 | 0.83 | 1.13 | 1.69 |

| D/E | -0.32 | -0.58 | -0.44 | -0.63 | -2.18 |

| Debt-to-Assets | 6% | 28% | 35% | 25% | 41% |

| Interest Coverage | 0 | -22 | -10 | -27 | -20 |

| Asset Turnover | 0.98 | 0.78 | 0.72 | 0.62 | 0.48 |

| Fixed Asset Turnover | 7.7 | 7.2 | 8.1 | 16.7 | 15.7 |

| Dividend Yield | 0% | 0% | 0% | 0% | 0% |

Evolution of Financial Ratios

Return on Equity (ROE) improved significantly from 0.50% in 2024 to 67.14% in 2026, signaling enhanced shareholder profitability. The Current Ratio rose steadily from 0.84 to 1.69, indicating strengthening liquidity. Meanwhile, the Debt-to-Equity Ratio shifted negatively to -2.18, reflecting unusual capital structure dynamics with increased leverage or negative equity.

Are the Financial Ratios Favorable?

Profitability shows mixed signals with a strong ROE but a highly negative net margin of -26.5%. Liquidity ratios, including Current and Quick Ratios at 1.69, are favorable, suggesting sufficient short-term asset coverage. Leverage metrics appear favorable despite a high debt-to-assets ratio of 40.87%, considered neutral. Efficiency is weak with asset turnover at 0.48, and market multiples like P/E and P/B are favorable but reflect negative earnings and book value. Overall, the ratios lean favorable with notable risks.

Shareholder Return Policy

Rubrik, Inc. does not pay dividends, reflecting its negative net income and ongoing investment in growth and operations. The company does not engage in share buybacks either, indicating a focus on reinvesting cash flow into the business rather than returning capital to shareholders.

This strategy aligns with the typical profile of a high-growth firm prioritizing long-term value creation through expansion and development. However, the lack of shareholder distributions means investors must rely on capital appreciation, which depends on the company eventually achieving profitability and positive cash flow.

Score analysis

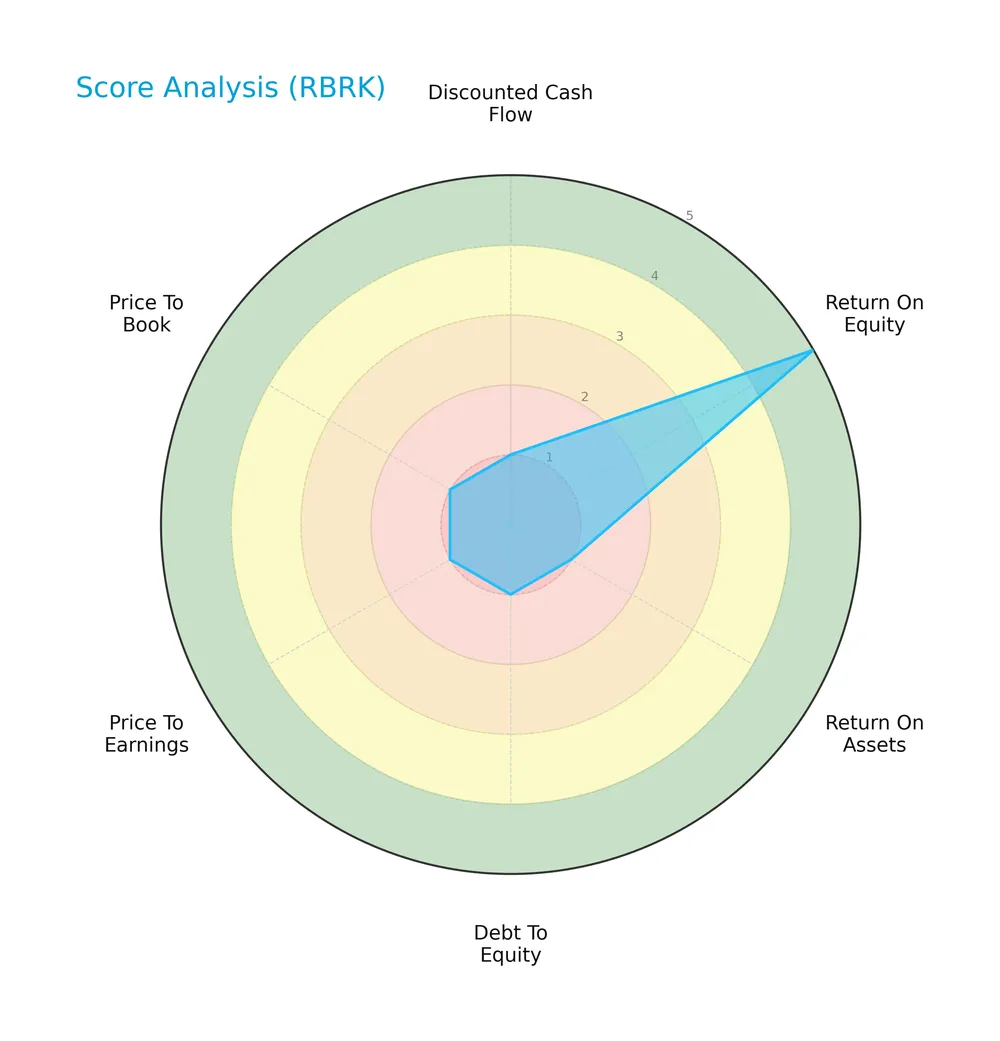

The following radar chart visualizes Rubrik, Inc.’s key financial scores across valuation and profitability metrics:

Rubrik’s scores reveal a stark contrast: a very favorable return on equity score of 5 stands against very unfavorable scores of 1 in discounted cash flow, return on assets, debt to equity, price to earnings, and price to book ratios, indicating uneven financial performance.

Analysis of the company’s bankruptcy risk

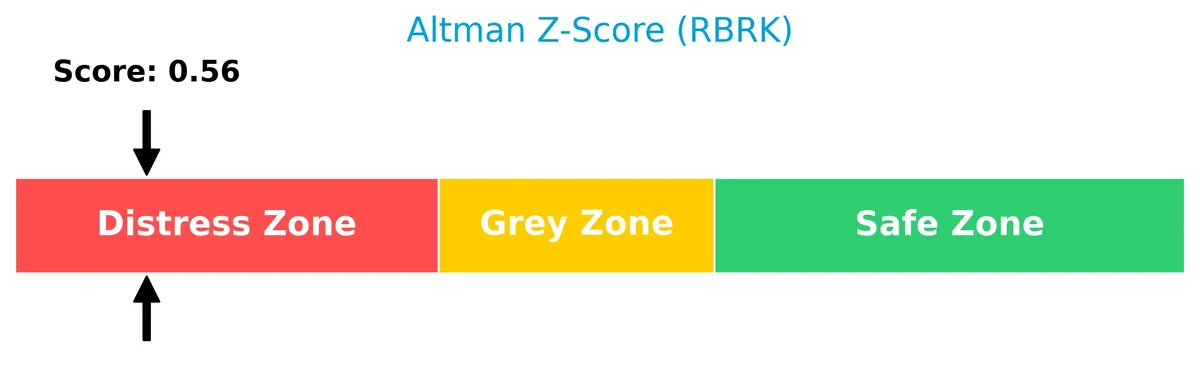

Rubrik’s Altman Z-Score places it firmly in the distress zone, signaling a high risk of bankruptcy based on key financial ratios:

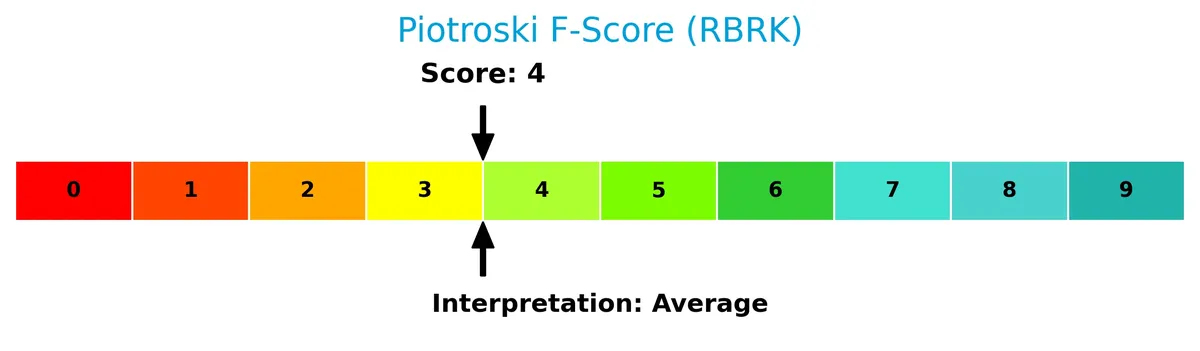

Is the company in good financial health?

The Piotroski Score diagram illustrates Rubrik’s moderate financial strength with a score of 4:

A Piotroski Score of 4 indicates average financial health, suggesting the company shows some positive financial traits but lacks robustness to be considered a strong investment based on this metric.

Competitive Landscape & Sector Positioning

This analysis explores Rubrik, Inc.’s strategic positioning within the software infrastructure sector. It reviews the company’s revenue by segment, key products, and main competitors. I will assess whether Rubrik holds a competitive advantage over its rivals.

Strategic Positioning

Rubrik concentrates on subscription-based data security services, with FY2026 subscription revenue at $1.26B versus $52M in other products. Geographically, it focuses heavily on the Americas ($952M), followed by EMEA ($313M) and Asia Pacific ($52M), reflecting a primarily regional exposure.

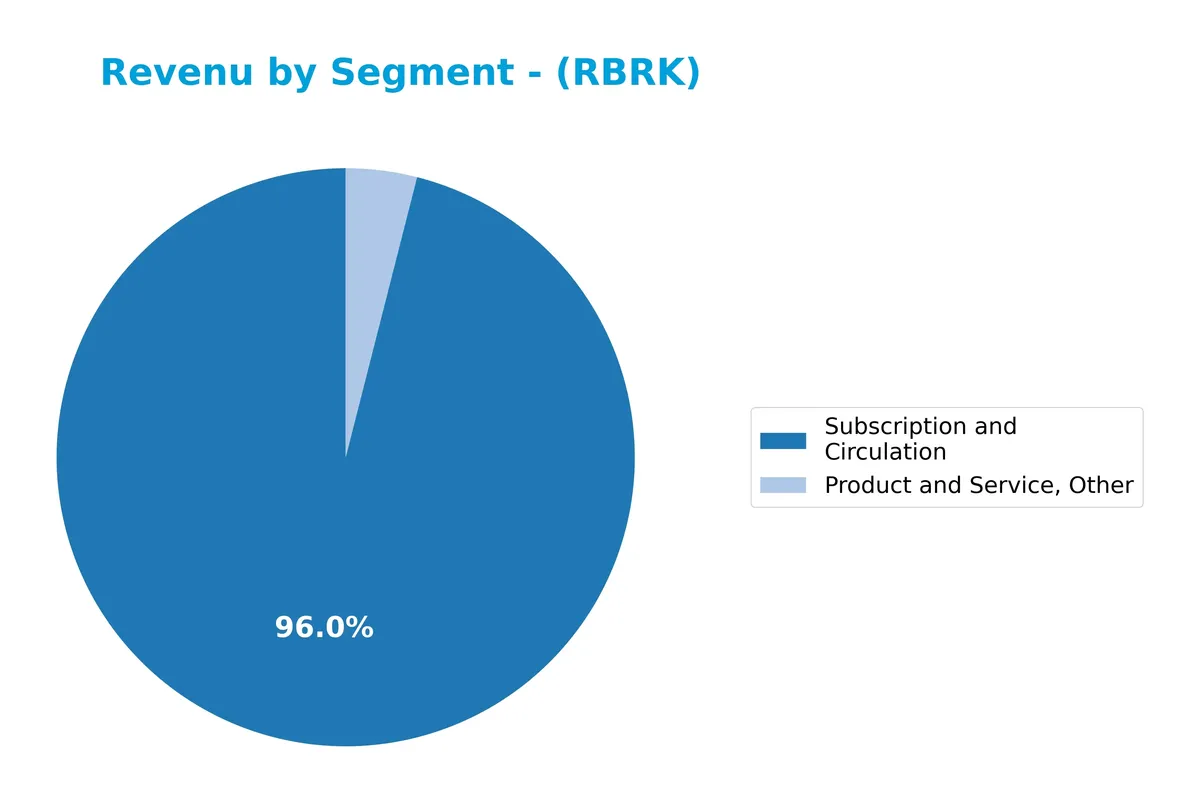

Revenue by Segment

The pie chart illustrates Rubrik, Inc.’s revenue distribution by segment for fiscal year 2026, highlighting the composition between Subscription and Circulation and Product and Service, Other.

Subscription and Circulation dominate Rubrik’s revenue with 1.26B in 2026, showing a strong growth from 829M in 2025. Product and Service, Other contributes modestly at 52M, up from 45M. Maintenance revenue was reported only in 2025 at 18M but not in 2026, indicating a possible consolidation or reclassification. The business leans heavily on subscription revenue, increasing concentration risk but also reflecting a successful shift to recurring revenue models.

Key Products & Brands

Rubrik’s revenue primarily comes from subscription services and diverse product offerings as detailed below:

| Product | Description |

|---|---|

| Subscription and Circulation | Recurring revenue from enterprise data protection, cloud, SaaS data security, and cyber recovery solutions. |

| Product and Service, Other | One-time sales including software licenses and other service-related offerings. |

| Maintenance | Support and update services provided post-sale to ensure product performance and customer satisfaction. |

Rubrik generates most revenue from subscriptions, reflecting strong recurring cash flow. Product sales and maintenance services complement this base, supporting client retention and ongoing service delivery.

Main Competitors

There are 32 competitors in the Technology sector, with the table below listing the top 10 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| Microsoft Corporation | 3.5T |

| Oracle Corporation | 553B |

| Palantir Technologies Inc. | 383B |

| Adobe Inc. | 140B |

| Palo Alto Networks, Inc. | 120B |

| CrowdStrike Holdings, Inc. | 113B |

| Synopsys, Inc. | 92B |

| Cloudflare, Inc. | 69B |

| Fortinet, Inc. | 59B |

| Block, Inc. | 40B |

Rubrik, Inc. ranks 19th among 32 competitors, with a market cap just 0.26% of Microsoft’s. It sits below both the average market cap of the top 10 (508B) and the sector median (19B). The 74% gap to its nearest competitor above highlights a significant scale difference.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does Rubrik have a competitive advantage?

Rubrik currently lacks a strong competitive advantage, as its ROIC remains below WACC, indicating value destruction despite improving profitability. This places the company in a slightly unfavorable moat position compared to industry benchmarks.

The firm shows promising growth with expanding revenues across Americas, EMEA, and Asia Pacific markets. Its focus on data security and cyber recovery solutions positions it well for future opportunities in evolving enterprise and cloud environments.

SWOT Analysis

This analysis highlights Rubrik’s key internal strengths and weaknesses alongside external opportunities and threats to guide strategic decisions.

Strengths

- Strong revenue growth of 48% YoY

- High gross margin at 80%

- Solid market presence in data security

Weaknesses

- Negative net margin at -26.5%

- ROIC below WACC, indicating value destruction

- Low Altman Z-score signals financial distress

Opportunities

- Expanding demand for cloud and SaaS data protection

- Growing cybersecurity threats increase market potential

- Geographic revenue growth in Americas and EMEA

Threats

- Intense competition in software infrastructure

- Rapid technology changes require constant innovation

- Financial distress risk limits investment capacity

Rubrik enjoys robust growth and market positioning but struggles with profitability and financial health. The company must leverage growth opportunities while aggressively managing costs and financial risks to build sustainable value.

Stock Price Action Analysis

The weekly stock chart below illustrates Rubrik, Inc.’s price movements over the past 100 weeks, highlighting key volatility and trend shifts:

Trend Analysis

Over the past 100 weeks, Rubrik’s stock price rose 39.63%, signaling a bullish trend. However, recent data from January to March 2026 shows a 35.19% decline, indicating a short-term bearish trend. The overall trend decelerated despite high volatility (20.51% std deviation). The stock peaked at 97.91 and bottomed at 28.65.

Volume Analysis

Trading volume is increasing, with sellers dominating the recent period (only 20.1% buyer dominance). From January to March 2026, seller volume reached 193M versus buyer volume of 49M, implying bearish investor sentiment and heightened selling pressure.

Target Prices

Analysts set a consensus target price signaling moderate upside potential for Rubrik, Inc.

| Target Low | Target High | Consensus |

|---|---|---|

| 70 | 113 | 94.71 |

The target range shows a cautious optimism with a consensus near $95, reflecting expectations of steady growth balanced against sector volatility.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section examines analyst ratings and consumer feedback to provide a balanced view of Rubrik, Inc.’s market perception.

Stock Grades

Here are the latest verified stock grades from leading financial institutions for Rubrik, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Citigroup | Maintain | Buy | 2026-03-16 |

| Cantor Fitzgerald | Maintain | Overweight | 2026-03-13 |

| Piper Sandler | Maintain | Overweight | 2026-03-13 |

| Rosenblatt | Maintain | Buy | 2026-03-13 |

| Wells Fargo | Maintain | Overweight | 2026-03-13 |

| Guggenheim | Maintain | Buy | 2026-03-13 |

| Wedbush | Maintain | Outperform | 2026-03-13 |

| BMO Capital | Maintain | Outperform | 2026-03-13 |

| Cantor Fitzgerald | Maintain | Overweight | 2026-03-09 |

| Rosenblatt | Maintain | Buy | 2026-03-09 |

The consensus across reputable firms is clearly positive, with all maintaining buy, overweight, or outperform ratings. This consistency signals broad analyst confidence in Rubrik’s current trajectory.

Consumer Opinions

Consumer sentiment around Rubrik, Inc. reflects a mix of strong approval and notable concerns. Here’s what users are saying:

| Positive Reviews | Negative Reviews |

|---|---|

| “Rubrik’s data backup speed is impressive and reliable.” | “The pricing model feels expensive for smaller businesses.” |

| “Customer support responds quickly and resolves issues efficiently.” | “The user interface could be more intuitive for new users.” |

| “Integration with cloud services is seamless and well-executed.” | “Occasional bugs disrupt workflow during peak hours.” |

Overall, customers praise Rubrik for its performance and support but often cite cost and usability challenges. These weaknesses could hinder adoption among smaller clients despite strong technical capabilities.

Risk Analysis

Below is a detailed table outlining the key risks facing Rubrik, Inc., including their probability and potential impact:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Financial Distress | Altman Z-Score at 0.56 signals high bankruptcy risk. | High | Severe |

| Profitability | Negative net margin (-26.5%) indicates ongoing losses. | High | High |

| Capital Efficiency | Negative ROIC (-23.78%) below WACC (5.97%) erodes value. | High | High |

| Leverage | Debt-to-assets at 40.87% is moderate but interest coverage negative (-20.05). | Medium | High |

| Market Volatility | Share price range wide (44.75-103), beta low (0.46) suggests low market correlation but price swings. | Medium | Medium |

| Dividend Policy | No dividend yield may deter income-focused investors. | High | Medium |

The most pressing risks are financial distress and poor profitability. Rubrik’s Altman Z-Score firmly places it in the distress zone, increasing bankruptcy chances. Negative ROIC versus WACC signals value destruction despite a strong ROE, a red flag for capital allocation. Interest coverage is deeply negative, raising solvency concerns. These weaknesses overshadow moderate leverage and stable market beta. Investors must weigh Rubrik’s growth potential against these critical financial fragilities.

Should You Buy Rubrik, Inc.?

Rubrik appears to be shedding value despite a growing ROIC trend, suggesting improving profitability amid a slightly unfavorable moat. Supported by a manageable leverage profile, the overall rating is a cautious C, reflecting financial distress risk and average operational efficiency.

Strength & Efficiency Pillars

Rubrik, Inc. posts a robust gross margin of 80.1%, underscoring strong operational efficiency in its sector. The return on equity at 67.14% signals effective capital use and shareholder value generation. However, the company’s return on invested capital (ROIC) is -23.78%, well below its weighted average cost of capital (WACC) at 5.97%, indicating value destruction despite improving profitability trends. Given this, Rubrik cannot be classified as a value creator at present, reflecting ongoing challenges in converting investments into returns.

Weaknesses and Drawbacks

Rubrik is in financial distress, as evidenced by a perilously low Altman Z-Score of 0.56, which signals a high bankruptcy risk. This solvency concern eclipses other metrics. Leverage ratios show a favorable debt-to-equity at -2.18, but interest coverage is severely negative at -20.05, raising alarms about the company’s ability to service debt. Further, negative net margins (-26.5%) and unfavorable market valuation indicators (negative P/E and P/B ratios) compound risks. Recent seller dominance at 79.9% heightens short-term market pressure.

Our Final Verdict about Rubrik, Inc.

Despite operational strengths and a bullish long-term price trend, Rubrik’s severe solvency risk with an Altman Z-Score in the distress zone makes its profile highly speculative. The company’s value destruction and weak solvency metrics suggest it is too risky for conservative capital. Investors might consider waiting for clear signs of financial stabilization before evaluating long-term potential.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Rubrik (NYSE:RBRK) CFO Kiran Kumar Choudary Sells 122,613 Shares – MarketBeat (Mar 28, 2026)

- Analysts Offer Insights on Technology Companies: Intuit (INTU), Rubrik, Inc. Class A (RBRK) and Lumexa Imaging Holdings, Inc. (LMRI) – The Globe and Mail (Mar 28, 2026)

- Rubrik Inc (RBRK) Shares Gap Down to $45.7275 on Mar 27 – GuruFocus (Mar 27, 2026)

- Here’s why Rubrik, Inc. (RBRK) is a strong momentum stock – MSN (Mar 26, 2026)

- Vanguard disaggregates holdings; RBRK ownership reported as 0% (NYSE: RBRK) – Stock Titan (Mar 27, 2026)

For more information about Rubrik, Inc., please visit the official website: rubrik.com