Home > Analyses > Industrials > Pentair plc

Pentair transforms how water flows and purifies across homes, industries, and agriculture worldwide. Its market-leading solutions span residential pool equipment and advanced industrial fluid treatment, reflecting a commitment to innovation and quality. Pentair’s diverse brands and cutting-edge technologies have entrenched it as a vital player in water management. As water scarcity and infrastructure demands grow, I examine whether Pentair’s fundamentals support its current valuation and long-term growth prospects.

Table of contents

Business Model & Company Overview

Pentair plc, founded in 1966 and headquartered in London, UK, stands as a leading force in the industrial machinery sector. It crafts a comprehensive water solutions ecosystem spanning residential pools to complex industrial fluid systems. Through iconic brands like Everpure and Sta-Rite, it services diverse markets with a unified mission: delivering innovative, reliable water management technologies.

The company’s revenue engine balances durable hardware—pumps, valves, filtration systems—with specialized software and service components embedded in water treatment and flow technologies. Pentair sustains a strategic footprint across the Americas, Europe, and Asia, aligning global reach with local expertise. Its economic moat lies in proprietary membrane technologies and a broad product platform shaping the future of sustainable water management.

Financial Performance & Fundamental Metrics

I will analyze Pentair plc’s income statement, key financial ratios, and dividend payout policy to assess its core financial health and shareholder returns.

Income Statement

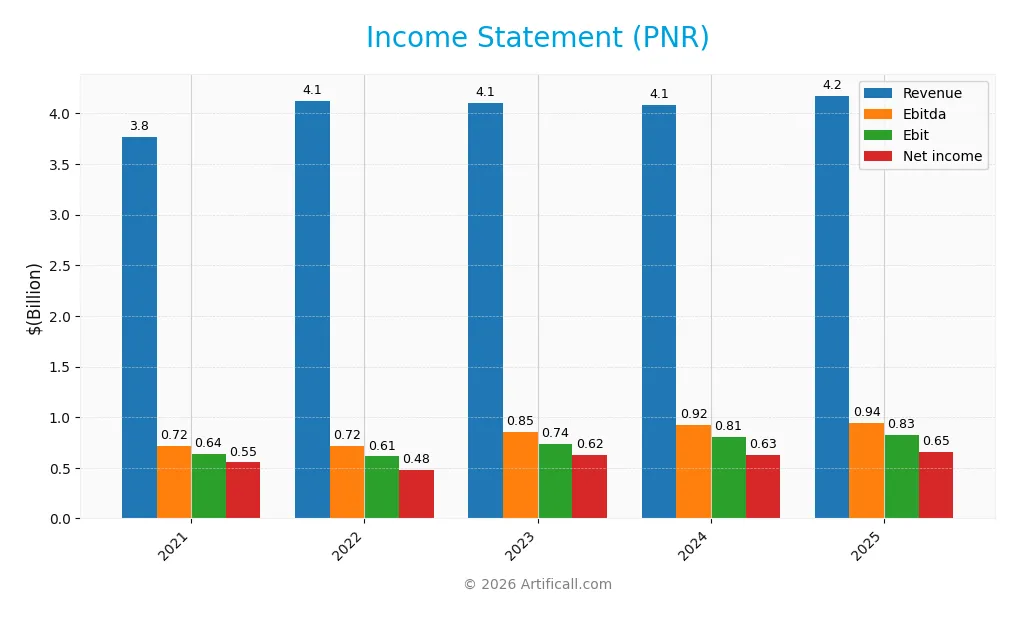

The table below summarizes Pentair plc’s key income statement figures for fiscal years 2021 through 2025, reported in USD.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 3.76B | 4.12B | 4.10B | 4.08B | 4.18B |

| Cost of Revenue | 2.45B | 2.76B | 2.59B | 2.48B | 2.49B |

| Operating Expenses | 682M | 769M | 780M | 795M | 833M |

| Gross Profit | 1.32B | 1.36B | 1.52B | 1.60B | 1.69B |

| EBITDA | 717M | 719M | 852M | 922M | 944M |

| EBIT | 639M | 612M | 737M | 808M | 826M |

| Interest Expense | 13M | 62M | 118M | 89M | 69M |

| Net Income | 553M | 481M | 623M | 625M | 654M |

| EPS | 3.34 | 2.92 | 3.77 | 3.78 | 3.99 |

| Filing Date | 2022-02-22 | 2023-02-21 | 2024-02-20 | 2025-02-25 | 2026-02-24 |

Income Statement Evolution

Pentair’s revenue grew modestly by 2.3% in 2025, slowing compared to the 10.9% growth over 2021-2025. Gross profit expanded 5.7%, lifting the gross margin to a favorable 40.5%. Operating expenses followed revenue growth, keeping EBIT margin stable near 19.8%. Net income rose by 2.2%, sustaining a healthy net margin around 15.7%.

Is the Income Statement Favorable?

In 2025, Pentair reported $4.18B revenue and $654M net income, reflecting solid fundamentals. Favorable margins—gross, EBIT, and net—indicate efficient cost control and profitability. Interest expense remains low at 1.66% of revenue. Despite modest revenue growth, EPS rose nearly 6%, signaling effective capital allocation and operating leverage. Overall, the income statement shows strength within a moderate growth environment.

Financial Ratios

The following table summarizes key financial ratios for Pentair plc over recent fiscal years, providing insight into profitability, liquidity, leverage, and valuation metrics:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 14.7% | 11.7% | 15.2% | 15.3% | 15.7% |

| ROE | 22.8% | 17.8% | 19.4% | 17.6% | 16.9% |

| ROIC | 15.2% | 9.7% | 13.1% | 12.5% | 12.5% |

| P/E | 21.9 | 15.4 | 19.3 | 26.9 | 26.1 |

| P/B | 5.0 | 2.7 | 3.7 | 4.7 | 4.4 |

| Current Ratio | 1.24 | 1.47 | 1.65 | 1.60 | 1.61 |

| Quick Ratio | 0.70 | 0.72 | 0.94 | 0.92 | 0.95 |

| D/E | 0.41 | 0.89 | 0.65 | 0.50 | 0.42 |

| Debt-to-Assets | 20.7% | 37.2% | 31.9% | 27.4% | 23.9% |

| Interest Coverage | 51.0 | 9.6 | 6.2 | 9.1 | 12.4 |

| Asset Turnover | 0.79 | 0.64 | 0.63 | 0.63 | 0.61 |

| Fixed Asset Turnover | 9.5 | 9.7 | 8.8 | 8.6 | 11.1 |

| Dividend Yield | 1.10% | 1.87% | 1.21% | 0.91% | 0.96% |

Evolution of Financial Ratios

Pentair’s Return on Equity (ROE) showed moderate fluctuations, peaking at 22.8% in 2021 before settling at 16.9% in 2025. The Current Ratio steadily improved from 1.24 in 2021 to 1.61 in 2025, indicating better liquidity. Debt-to-Equity declined from 0.65 in 2023 to 0.42 in 2025, reflecting a gradual reduction in leverage. Profitability margins remained stable with slight growth in net profit margin.

Are the Financial Ratios Favorable?

In 2025, Pentair’s profitability metrics such as ROE (16.9%) and net margin (15.66%) are favorable, outperforming typical industrial benchmarks. Liquidity is solid, supported by a Current Ratio of 1.61, while the Quick Ratio at 0.95 is neutral. Leverage is moderate, with a Debt-to-Equity of 0.42 and strong interest coverage near 12. Market valuation ratios like P/E (26.14) and P/B (4.42) appear stretched, indicating some caution despite an overall favorable financial profile.

Shareholder Return Policy

Pentair plc maintains a consistent dividend payout ratio near 25%, with dividends per share steadily rising from $0.80 in 2021 to $1.00 in 2025. The dividend yield hovers around 1%, supported by free cash flow coverage exceeding 90%, indicating prudent distribution levels.

The company also engages in share buybacks, complementing its dividend policy. This balanced approach reflects a focus on sustainable shareholder returns. However, investors should monitor potential risks from excessive repurchases amid fluctuating operating cash flow ratios.

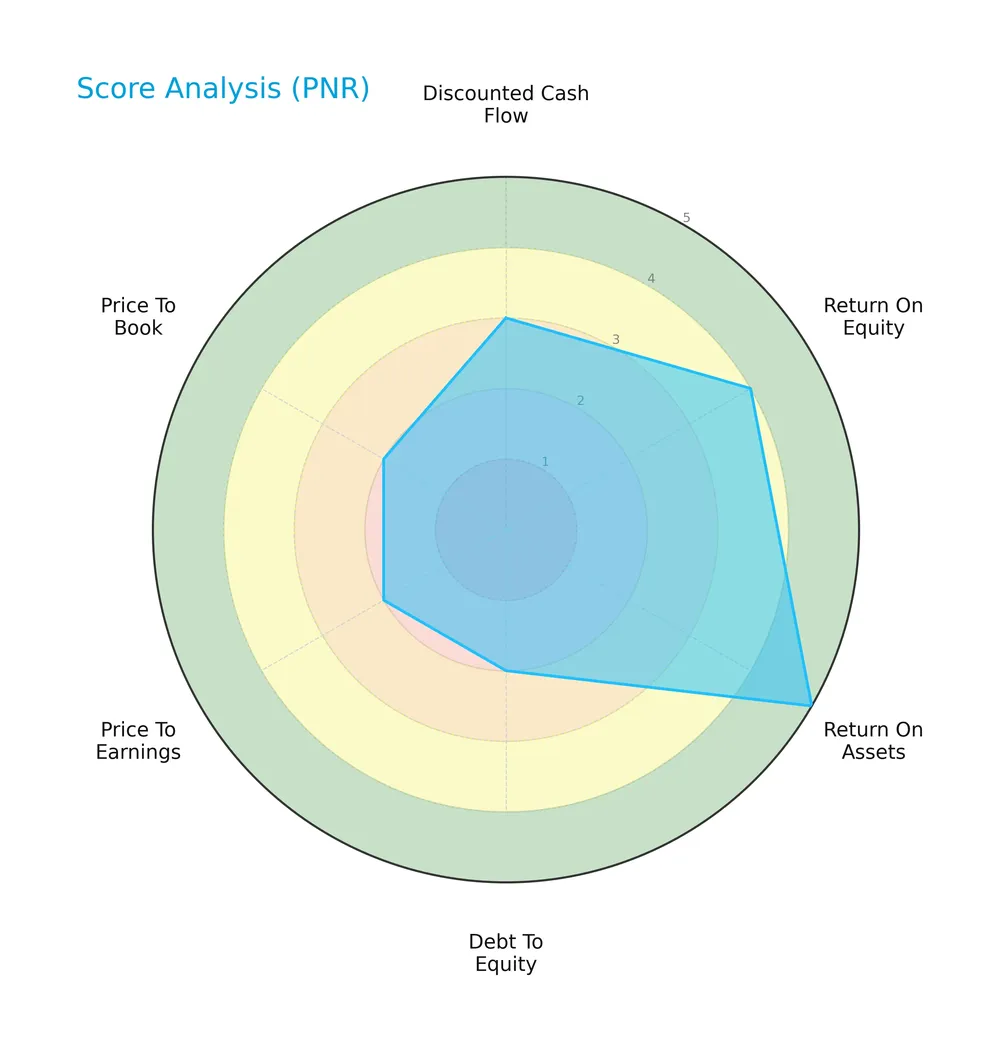

Score analysis

The following radar chart illustrates Pentair plc’s key financial metric scores for a comprehensive performance snapshot:

Pentair shows a very favorable return on assets score of 5 and a favorable return on equity score of 4. Its discounted cash flow and debt-to-equity scores are moderate at 3 each. Valuation metrics PE and PB scores are unfavorable at 2, reflecting potential market pricing concerns.

Analysis of the company’s bankruptcy risk

Pentair’s Altman Z-Score places it firmly in the safe zone, signaling a low bankruptcy risk and solid financial stability:

Is the company in good financial health?

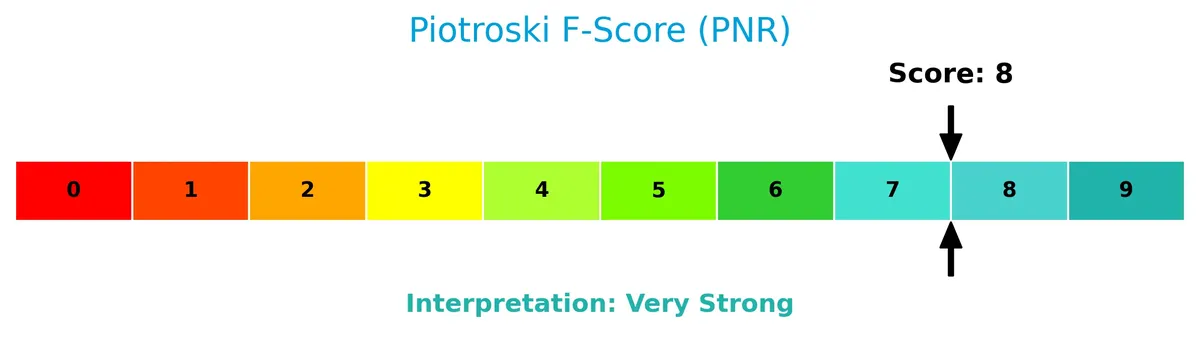

The Piotroski Score diagram highlights Pentair’s strong financial health with a score of 8 out of 9 points:

This very strong Piotroski Score indicates robust profitability, efficient asset use, and prudent leverage, suggesting Pentair maintains excellent financial strength.

Competitive Landscape & Sector Positioning

This analysis examines Pentair plc’s sector positioning, revenue segments, key products, and main competitors. I will assess whether Pentair holds a competitive advantage within the industrial machinery sector.

Strategic Positioning

Pentair plc maintains a diversified product portfolio across Consumer Solutions and Industrial & Flow Technologies, with roughly balanced revenue streams near $1.5B each in 2025. Geographically, it concentrates heavily in the U.S. ($2.94B), while also maintaining notable presence in Western Europe ($496M) and developing countries ($508M), reflecting moderate global diversification.

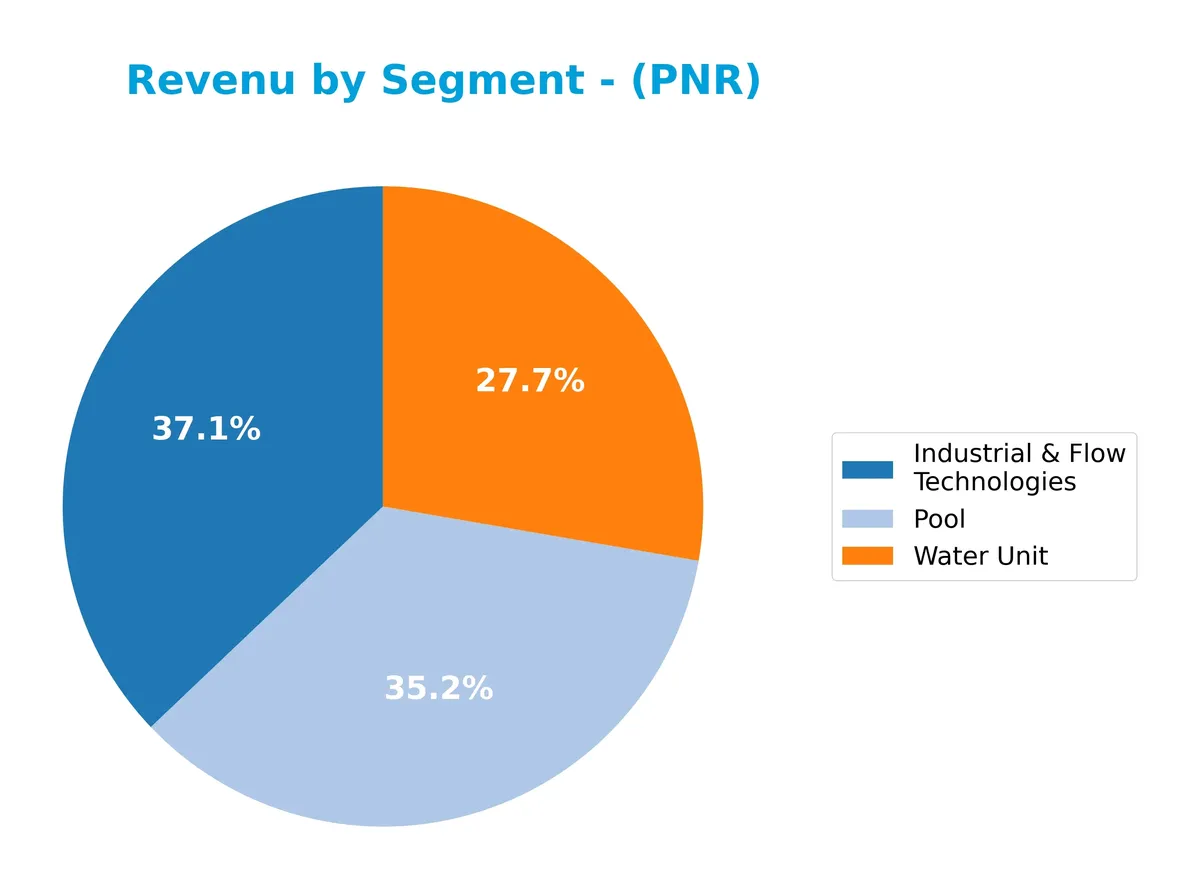

Revenue by Segment

This pie chart displays Pentair plc’s revenue distribution by segment for the fiscal year 2025, highlighting the contributions of all active business units.

In 2025, Pentair’s revenue is well balanced across three main segments: Industrial & Flow Technologies leads with $1.55B, closely followed by Pool at $1.56B, and Water Unit at $1.06B. The Pool segment showed a steady acceleration since 2023, while Industrial & Flow Technologies maintained consistent growth. Water Unit’s revenue slightly declined compared to 2024, signaling a potential shift or concentration risk in Pentair’s water-related offerings.

Key Products & Brands

The following table highlights Pentair plc’s main products and brands across its business segments:

| Product | Description |

|---|---|

| Consumer Solutions | Residential and commercial pool equipment and water treatment products, including pumps, filters, heaters. |

| Industrial & Flow Technologies | Fluid treatment products, pumps, valves, filtration systems, and gas recovery solutions for industrial use. |

| Pool Equipment & Accessories | Pool maintenance, repair, renovation, and construction equipment under brands like Kreepy Krauly, Sta-Rite. |

| Water Treatment Systems | Pressure tanks, control valves, activated carbon, filtration, softening, and point-of-use water systems. |

| Everpure | Water filtration products primarily for residential and commercial use. |

| Ken’s Beverage | Beverage filtration solutions. |

| Pleatco | Pool and spa filter cartridges and related accessories. |

| RainSoft | Water filtration and softening systems for residential applications. |

| Aurora, Berkeley, Codeline, Fairbanks-Nijhuis, Haffmans, Hydromatic, Hypro, Jung Pumpen, Myers, Shurflo, Südmo, X-Flow | Brands offering specialized pumps, valves, and filtration products for industrial and municipal water management. |

Pentair maintains a diverse product portfolio focused on water solutions and industrial fluid management. Its broad brand base supports both consumer and industrial markets worldwide.

Main Competitors

In the Industrials sector, 24 competitors exist, with the table below showing the top 10 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| Eaton Corporation plc | 127B |

| Parker-Hannifin Corporation | 114B |

| Howmet Aerospace Inc. | 85.2B |

| Emerson Electric Co. | 76.3B |

| Illinois Tool Works Inc. | 73B |

| Cummins Inc. | 71.9B |

| AMETEK, Inc. | 48.3B |

| Roper Technologies, Inc. | 46.8B |

| Rockwell Automation, Inc. | 44.8B |

| Symbotic Inc. | 35.9B |

Pentair plc ranks 15th among 24 competitors, with a market cap 13.25% that of the sector leader Eaton Corporation. It sits below both the average market cap of the top 10 competitors (72.4B) and the sector median (32.4B). Pentair maintains a significant 59.4% gap above its nearest competitor, highlighting a clear scale difference in the mid-tier segment.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does Pentair have a competitive advantage?

Pentair demonstrates a competitive advantage with a ROIC exceeding WACC by 3.6%, indicating consistent value creation. However, its ROIC trend shows a decline, reflecting weakening profitability over recent years. The company’s broad product portfolio in water solutions and industrial machinery supports its market position across diverse regions, notably the U.S. with $2.94B in 2025 revenue.

Looking ahead, Pentair’s opportunities lie in expanding its water treatment and filtration systems, leveraging brands like Everpure and Sta-Rite. Growth prospects also exist in emerging markets and new technological applications within industrial fluid management, potentially offsetting current challenges from declining ROIC trends.

SWOT Analysis

This SWOT analysis highlights Pentair plc’s key internal and external factors shaping its strategic outlook.

Strengths

- strong ROIC above WACC indicating value creation

- diversified global water solutions portfolio

- favorable profitability margins

Weaknesses

- declining ROIC trend signals eroding efficiency

- moderate revenue growth recently

- relatively high valuation multiples (PE, PB)

Opportunities

- expanding presence in developing markets

- rising global demand for water treatment

- innovation in advanced filtration technology

Threats

- competitive pressure in industrial machinery

- sensitivity to raw material price fluctuations

- regulatory risks in environmental standards

Pentair’s solid fundamentals and global footprint support steady value creation. However, management must address declining efficiency and high valuation risks to sustain growth. Growth in emerging markets and innovation remain critical strategic levers.

Stock Price Action Analysis

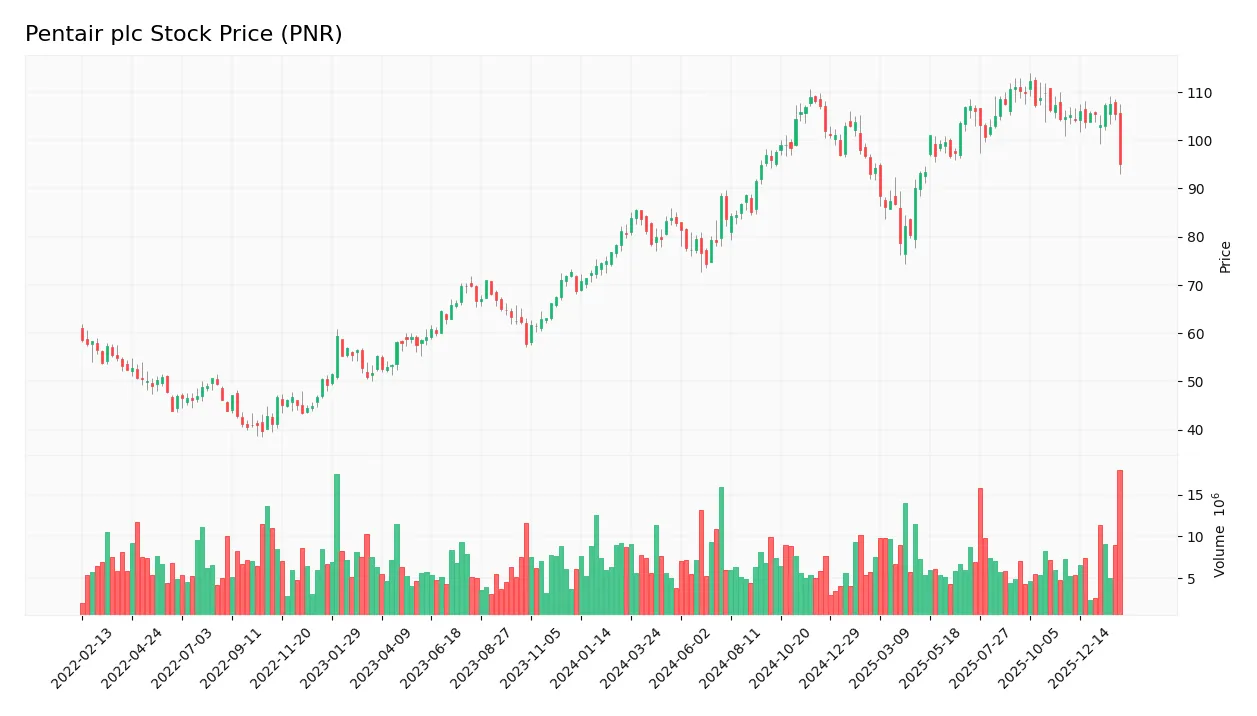

The weekly stock chart for Pentair plc (PNR) reveals price movements and key levels over the past 12 months:

Trend Analysis

Over the past 12 months, PNR’s stock price rose 23.17%, indicating a bullish trend with deceleration. The price ranged between 74.39 and 112.23, showing notable highs. Recent three-month data reveals a -2.91% decline, signaling a bearish short-term trend with mild negative slope and moderate volatility at 2.76.

Volume Analysis

In the last three months, trading volumes decreased, with sellers slightly dominating at 55.5% of activity. This seller-driven volume suggests cautious investor sentiment and reduced market participation compared to the broader yearly buyer dominance of 56.5%.

Target Prices

Analysts present a moderately bullish target consensus for Pentair plc.

| Target Low | Target High | Consensus |

|---|---|---|

| 90 | 135 | 118.56 |

The target range suggests upside potential near 13% from current levels, reflecting confidence in Pentair’s growth prospects and operational strength.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section examines the latest analyst ratings and consumer feedback regarding Pentair plc (PNR) to provide balanced insights.

Stock Grades

Here is a summary of recent verified stock grades for Pentair plc from leading financial institutions:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Citigroup | Maintain | Buy | 2026-02-04 |

| Oppenheimer | Maintain | Outperform | 2026-02-04 |

| JP Morgan | Maintain | Overweight | 2026-01-16 |

| Citigroup | Maintain | Buy | 2026-01-12 |

| BNP Paribas Exane | Downgrade | Underperform | 2026-01-07 |

| TD Cowen | Downgrade | Sell | 2026-01-05 |

| Jefferies | Upgrade | Buy | 2025-12-10 |

| Barclays | Downgrade | Equal Weight | 2025-12-04 |

| Oppenheimer | Maintain | Outperform | 2025-11-20 |

| UBS | Maintain | Buy | 2025-10-22 |

The overall trend shows a mix of buy and outperform ratings from top-tier firms, tempered by some recent downgrades to underperform and sell. This divergence suggests differing views on the stock’s near-term prospects amid broader market conditions.

Consumer Opinions

Pentair plc generates mixed but insightful consumer sentiment, reflecting its operational strengths and areas for improvement.

| Positive Reviews | Negative Reviews |

|---|---|

| Reliable water solutions with solid performance. | Customer service response times can lag. |

| Durable products that last over years. | Installation instructions are unclear. |

| Strong focus on sustainability efforts. | Pricing is higher compared to competitors. |

Overall, consumers praise Pentair’s product durability and commitment to sustainability. However, recurring complaints about customer service and pricing highlight areas where Pentair must improve to enhance customer satisfaction.

Risk Analysis

Below is a summary table outlining key risks facing Pentair plc, categorized by probability and impact:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Valuation Risk | Elevated P/E (26.14) and P/B (4.42) ratios suggest the stock may be overvalued. | Medium | High |

| Market Volatility | Beta of 1.22 indicates higher sensitivity to market swings than the Industrials sector average. | High | Medium |

| Liquidity Risk | Quick ratio near 1.0 signals tight short-term liquidity; potential vulnerability in downturns. | Medium | Medium |

| Competitive Pressure | Industrial machinery sector faces ongoing innovation and pricing pressures. | Medium | Medium |

| Dividend Yield Risk | Low dividend yield (0.96%) may deter income-focused investors amid rising rates. | High | Low |

| Debt and Interest Risk | Moderate debt-to-equity (0.42) with strong interest coverage (11.9x) reduces default risk. | Low | Low |

The primary risks for Pentair are valuation concerns and market volatility. The stock trades at premium multiples compared to sector averages, which could compress returns if growth slows. Additionally, a beta above 1.2 means Pentair’s shares may fall harder during market downturns. However, solid interest coverage and a safe Altman Z-Score (4.48) confirm financial stability, reducing bankruptcy risk. I remain cautious on valuation but recognize Pentair’s strong fundamentals and resilient balance sheet.

Should You Buy Pentair plc?

Pentair plc appears to be a moderately profitable company with a slightly favorable moat, reflecting value creation despite declining returns. Its leverage profile is manageable. Supported by a very favorable B+ rating, this analytical interpretation suggests a stable financial health with some operational efficiency risks.

Strength & Efficiency Pillars

Pentair plc exhibits solid profitability with a net margin of 15.66% and a return on equity of 16.9%. Its return on invested capital stands at 12.46%, comfortably above the weighted average cost of capital at 8.88%, confirming it as a value creator. The company maintains favorable operational efficiency, reflected in a strong EBIT margin of 19.78% and an interest expense ratio of only 1.66%, signaling effective cost control and capital allocation.

Weaknesses and Drawbacks

Despite operational strengths, Pentair faces valuation concerns with a price-to-earnings ratio of 26.14 and a price-to-book ratio of 4.42, both flagged as unfavorable. These elevated multiples suggest the stock trades at a premium, potentially limiting upside. Additionally, the recent trend shows seller dominance with buyers at 44.5%, indicating short-term market pressure. While leverage is moderately managed with a debt-to-equity ratio of 0.42 and a current ratio of 1.61, these metrics warrant monitoring amid valuation risks.

Our Final Verdict about Pentair plc

Pentair plc’s long-term fundamentals appear solid, supported by strong profitability and a robust Piotroski score of 8. However, despite a bullish overall trend, recent slight seller dominance suggests a cautious, wait-and-see stance for investors seeking optimal entry points. The premium valuation may constrain near-term gains, though the company’s ability to create value could make it appealing for patient, long-term exposure.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Decoding Pentair PLC (PNR): A Strategic SWOT Insight – GuruFocus (Feb 25, 2026)

- Pentair plc (NYSE:PNR) to Issue $0.27 Quarterly Dividend – MarketBeat (Feb 24, 2026)

- Pentair Announces Quarterly Cash Dividend of $0.27 – Business Wire (Feb 23, 2026)

- The Pentair plc (NYSE:PNR) Yearly Results Are Out And Analysts Have Published New Forecasts – Yahoo Finance (Feb 06, 2026)

- Lansforsakringar Fondforvaltning AB publ Purchases 19,467 Shares of Pentair plc $PNR – MarketBeat (Feb 24, 2026)

For more information about Pentair plc, please visit the official website: pentair.com