Home > Analyses > Technology > Onto Innovation Inc.

Onto Innovation shapes the semiconductor landscape by enabling precision in chip manufacturing that powers modern devices. The company leads with cutting-edge process control tools, including macro defect inspection, 3D optical metrology, and advanced lithography systems. Renowned for innovation and quality, Onto supports global semiconductor makers in boosting yield and efficiency. As the industry evolves rapidly, I ask: do Onto’s fundamentals still justify its premium valuation and growth prospects?

Table of contents

Business Model & Company Overview

Onto Innovation Inc., founded in 1940 and headquartered in Wilmington, Massachusetts, stands as a leading player in the semiconductors sector. The company delivers an integrated ecosystem of process control tools, including macro defect inspection, 2D/3D optical metrology, lithography systems, and analytical software. Its solutions serve a wide array of advanced device manufacturers, reinforcing its critical role in semiconductor and packaging technology.

Onto Innovation drives value through a balanced revenue engine combining hardware systems with recurring software licensing and spare parts sales. Its offerings span standalone tools and enterprise-wide software suites, addressing markets across the Americas, Europe, and Asia. This diversified presence, paired with proprietary technology, secures a durable economic moat and positions Onto Innovation to shape the semiconductor industry’s future.

Financial Performance & Fundamental Metrics

I analyze Onto Innovation Inc.’s income statement, key financial ratios, and dividend payout policy to assess its fiscal health and shareholder value potential.

Income Statement

The table below presents Onto Innovation Inc.’s key income statement figures for fiscal years 2021 through 2025, reported in USD.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 789M | 1.01B | 816M | 987M | 1.01B |

| Cost of Revenue | 360M | 466M | 396M | 472M | 505M |

| Operating Expenses | 273M | 303M | 304M | 328M | 367M |

| Gross Profit | 429M | 539M | 420M | 515M | 500M |

| EBITDA | 222M | 301M | 183M | 249M | 133M |

| EBIT | 156M | 237M | 116M | 187M | 133M |

| Interest Expense | 0 | 0 | 0 | 0 | 0 |

| Net Income | 142M | 223M | 121M | 202M | 137M |

| EPS | 2.89 | 4.52 | 2.47 | 4.09 | 2.78 |

| Filing Date | 2022-02-25 | 2023-02-24 | 2024-02-26 | 2025-02-25 | 2026-02-24 |

Income Statement Evolution

Onto Innovation’s revenue grew 27.4% from 2021 to 2025 but slowed to 1.8% in the last year. Gross profit declined 3% in 2025, reflecting margin pressure. EBIT and net income both fell sharply last year, by 29% and 33%, respectively. Margins weakened overall, with net margin down 24.6% over the period.

Is the Income Statement Favorable?

In 2025, Onto Innovation reported $1.01B revenue with a 13.6% net margin, both marked favorable metrics. However, net income dropped to $137M, down 33% year-over-year, signaling profitability challenges. Operating expenses grew faster than revenue, and EBIT margin contracted to 13.2%. Despite solid gross margin near 50%, fundamentals reflect a weakening income statement.

Financial Ratios

The following table summarizes key financial ratios for Onto Innovation Inc. over the last five fiscal years:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 18% | 22% | 15% | 20% | 14% |

| ROE | 10.0% | 14.0% | 7.0% | 10.5% | 6.5% |

| ROIC | 9.5% | 13.3% | 6.0% | 8.8% | 5.2% |

| P/E | 35.0 | 15.1 | 61.8 | 41.8 | 59.6 |

| P/B | 3.5 | 2.1 | 4.3 | 4.4 | 3.9 |

| Current Ratio | 6.1 | 7.1 | 8.7 | 8.7 | 5.8 |

| Quick Ratio | 4.6 | 5.0 | 6.5 | 7.0 | 4.4 |

| D/E | 0.01 | 0.01 | 0.01 | 0.01 | 0.00 |

| Debt-to-Assets | 1.1% | 1.2% | 1.0% | 0.7% | 0.0% |

| Interest Coverage | 0 | 0 | 0 | 0 | 0 |

| Asset Turnover | 0.48 | 0.56 | 0.43 | 0.47 | 0.42 |

| Fixed Asset Turnover | 9.6 | 10.9 | 6.7 | 7.2 | 7.9 |

| Dividend Yield | 0 | 0 | 0 | 0 | 0 |

Evolution of Financial Ratios

Return on Equity (ROE) declined from 14.0% in 2022 to 6.5% in 2025, signaling weakening profitability. The Current Ratio rose steadily, peaking at 8.7 in 2023 before settling at 5.8 in 2025, indicating strong but fluctuating liquidity. Debt-to-Equity Ratio remained near zero, reflecting minimal leverage and consistent financial conservatism.

Are the Financial Ratios Favorable?

In 2025, Onto Innovation shows mixed financial signals. Profitability is weak given ROE at 6.5%, below the 10.6% WACC, marking value destruction risk. Liquidity is uneven: a high Current Ratio of 5.79 contrasts with a favorable Quick Ratio of 4.43. Leverage remains low with zero debt, enhancing stability. Market valuation ratios, including P/E at 59.6 and P/B at 3.88, appear stretched. Overall, the ratios lean slightly unfavorable.

Shareholder Return Policy

Onto Innovation Inc. does not pay dividends, reflecting a strategic choice to reinvest earnings rather than distribute cash. The company maintains strong free cash flow and a robust balance sheet, with no debt and high liquidity ratios, supporting internal investment and potential growth initiatives.

While Onto Innovation does not engage in share buybacks, this approach aligns with its apparent focus on long-term value creation through reinvestment. The absence of dividends or buybacks suggests management prioritizes growth and capital allocation over immediate shareholder payouts, a stance consistent with sustaining future shareholder value.

Score analysis

The radar chart below illustrates Onto Innovation Inc.’s key financial scores across valuation, profitability, and leverage metrics:

Onto Innovation scores moderately on discounted cash flow and return on equity, with a favorable return on assets. However, debt-to-equity and price-to-earnings scores remain very unfavorable, signaling capital structure and valuation concerns. The price-to-book score is also unfavorable, reflecting potential market skepticism.

Analysis of the company’s bankruptcy risk

Onto Innovation’s Altman Z-Score places it securely in the safe zone, indicating a very low risk of bankruptcy:

Is the company in good financial health?

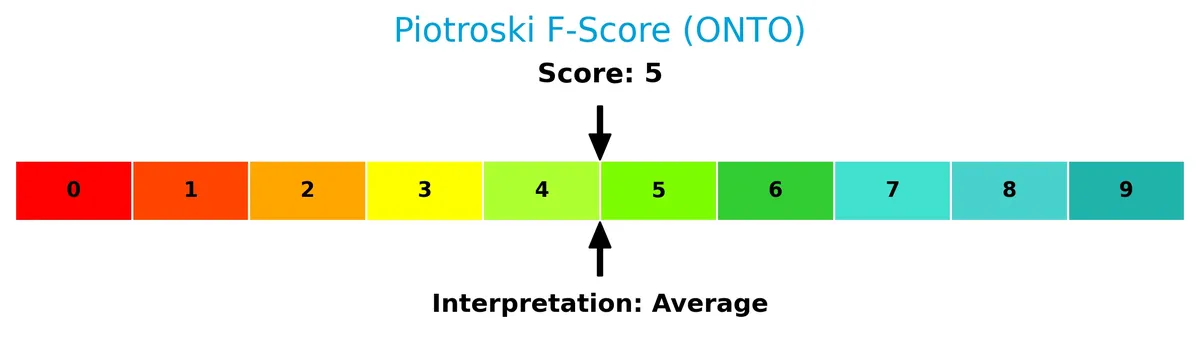

The Piotroski F-Score diagram provides insights into Onto Innovation’s financial strength and health status:

With a Piotroski score of 5, Onto Innovation demonstrates average financial health. This suggests moderate strength in profitability, leverage, and liquidity metrics, but with room for improvement compared to stronger firms.

Competitive Landscape & Sector Positioning

This section analyzes Onto Innovation Inc.’s strategic positioning within the semiconductor industry. It examines revenue by segment, key products, and main competitors. I will assess whether Onto Innovation holds a competitive advantage over its peers.

Strategic Positioning

Onto Innovation concentrates its revenue heavily in systems and software, generating over $847M in 2025, with smaller contributions from parts and services. Geographically, it diversifies across key semiconductor hubs, with significant exposure in Taiwan ($319M), Korea ($279M), and the US ($121M), reflecting a focused yet global footprint.

Revenue by Segment

The pie chart illustrates Onto Innovation Inc.’s revenue breakdown by segment for the fiscal year 2025, highlighting the relative contribution of parts, services, and systems/software.

In 2025, Systems and Software dominate with $848M, sustaining Onto’s tech-driven moat. Parts and Service revenues, $84M and $73M respectively, grow steadily, reflecting stable aftermarket and support demand. Despite slight year-to-year fluctuations, Systems revenue remains the core driver, signaling concentration risk but also strong technological leadership in semiconductor equipment. The recent year shows modest shifts, underscoring resilience amid market cyclicality.

Key Products & Brands

Onto Innovation’s main revenue streams and product lines are summarized in the table below:

| Product | Description |

|---|---|

| Systems and Software | Process control tools including macro defect inspection, 2D/3D optical metrology, lithography, and analytics software. |

| Parts | Spare parts supporting the maintenance and operation of equipment. |

| Services | Software licensing and device packaging, test, and analysis services for semiconductor manufacturing. |

Onto Innovation’s business primarily revolves around advanced measurement and process control systems. Systems and software dominate revenue, reflecting the company’s technological focus in semiconductors. Parts and services complement this core offering, supporting operational continuity.

Main Competitors

There are 38 competitors in the sector, with the table below listing the top 10 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| NVIDIA Corporation | 4.6T |

| Broadcom Inc. | 1.6T |

| Taiwan Semiconductor Manufacturing Company Limited | 1.6T |

| ASML Holding N.V. | 415B |

| Advanced Micro Devices, Inc. | 363B |

| Micron Technology, Inc. | 353B |

| Lam Research Corporation | 232B |

| Applied Materials, Inc. | 214B |

| QUALCOMM Incorporated | 185B |

| Intel Corporation | 173B |

Onto Innovation Inc. ranks 29th among 38 competitors. Its market cap is just 0.24% of NVIDIA’s, the sector leader. Onto Innovation sits below both the average market cap of the top 10 (975B) and the sector median (31B). It is approximately 14% behind its closest competitor above, highlighting a notable gap in scale.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does Onto Innovation Inc. have a competitive advantage?

Onto Innovation Inc. currently does not present a competitive advantage, as its return on invested capital (ROIC) falls significantly below its weighted average cost of capital (WACC). The company’s declining ROIC trend signals sustained value destruction and weakening profitability, a red flag in capital efficiency.

Looking ahead, Onto Innovation maintains a diversified global footprint in semiconductor process control and metrology, serving key markets like Taiwan, Korea, and the U.S. Its broad product portfolio and exposure to advanced packaging and lithography systems offer potential for growth in emerging semiconductor technologies.

SWOT Analysis

This SWOT analysis highlights Onto Innovation Inc.’s core strategic factors shaping its competitive position.

Strengths

- strong product portfolio in semiconductor process control

- zero debt structure

- favorable net margin of 13.6%

Weaknesses

- declining ROIC below WACC signals value destruction

- weak revenue growth recently at 1.8%

- high valuation multiples with PE near 60

Opportunities

- expanding semiconductor demand in Asia-Pacific

- growth in advanced packaging and metrology technologies

- potential to leverage software analytics for yield improvement

Threats

- intense competition in semiconductor tools sector

- geopolitical risks affecting China and Taiwan markets

- cyclicality and capital intensity of semiconductor industry

Onto Innovation benefits from a solid margin profile and debt-free balance sheet but faces headwinds from declining profitability and slow top-line growth. Strategic focus should be on innovation and geographic diversification to mitigate competitive and geopolitical risks.

Stock Price Action Analysis

The weekly stock price chart below illustrates Onto Innovation Inc.’s price movements over the past 12 months:

Trend Analysis

Over the past year, ONTO’s stock price rose 18.87%, signaling a bullish trend. The price shows acceleration, with a high of 233.14 and a low of 88.5. Volatility is elevated with a standard deviation of 44.18, reflecting notable price swings during this period.

Volume Analysis

Trading volumes are increasing, with buyers accounting for 56.42% of total volume, indicating buyer-driven activity. Recent months show slight buyer dominance at 57.21%, suggesting improving investor confidence and stronger market participation.

Target Prices

Analysts set a bullish consensus for Onto Innovation Inc., reflecting strong confidence in its growth prospects.

| Target Low | Target High | Consensus |

|---|---|---|

| 220 | 300 | 262.67 |

The target range from 220 to 300 signals optimism, with a consensus near 263, suggesting upside potential above current levels.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section examines grades and consumer feedback related to Onto Innovation Inc. (ONTO) to gauge market perception.

Stock Grades

Here are the latest verified stock grades for Onto Innovation Inc. from prominent analysts:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Needham | Maintain | Buy | 2026-02-20 |

| B. Riley Securities | Maintain | Buy | 2026-02-20 |

| Stifel | Maintain | Hold | 2026-02-20 |

| Evercore ISI Group | Maintain | Outperform | 2026-02-19 |

| Stifel | Maintain | Hold | 2026-02-18 |

| Cantor Fitzgerald | Upgrade | Overweight | 2026-02-17 |

| Needham | Maintain | Buy | 2026-01-20 |

| B. Riley Securities | Maintain | Buy | 2026-01-15 |

| Stifel | Maintain | Hold | 2026-01-14 |

| Needham | Maintain | Buy | 2026-01-06 |

The grades predominantly reflect a Buy consensus, with multiple firms maintaining positive outlooks. Notably, Cantor Fitzgerald upgraded from Neutral to Overweight, signaling increased confidence.

Consumer Opinions

Consumers express a mix of admiration and concern about Onto Innovation Inc., reflecting its innovative edge and service challenges.

| Positive Reviews | Negative Reviews |

|---|---|

| “Outstanding product quality and cutting-edge technology.” | “Customer support response times are frustratingly slow.” |

| “User-friendly interface enhances productivity significantly.” | “Pricing seems steep compared to competitors.” |

| “Reliable performance with minimal downtime reported.” | “Occasional software glitches disrupt workflow.” |

Overall, users praise Onto Innovation’s technology and reliability but frequently cite customer service delays and pricing as key pain points. This suggests strong product appeal tempered by service execution risks.

Risk Analysis

Below is a summary of key risks affecting Onto Innovation Inc., categorized by likelihood and potential impact:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Valuation Risk | High P/E of 59.6 suggests overvaluation relative to industry norms | High | High |

| Profitability | ROE at 6.5% lags WACC of 10.6%, indicating capital inefficiency | Medium | Medium |

| Liquidity | Elevated current ratio (5.79) may signal inefficient asset use | Medium | Low |

| Market Volatility | Beta of 1.48 implies above-market stock price fluctuations | High | Medium |

| Debt Risk | Zero debt and infinite interest coverage reduce financial risk | Low | Low |

| Financial Health | Piotroski score of 5 (average) shows mixed operational strength | Medium | Medium |

The most pressing risks are valuation and market volatility. Onto’s sky-high P/E ratio sharply exceeds the S&P 500 average near 20, raising a red flag for a correction. The stock’s beta of 1.48 also signals higher sensitivity to market swings. While liquidity appears strong, the abnormally high current ratio may reflect poor working capital allocation rather than strength. Notably, the company’s zero debt lowers bankruptcy risk, supported by a robust Altman Z-score in the safe zone at 26.2. However, middling profitability metrics highlight challenges in generating returns above the cost of capital, which investors must watch closely.

Should You Buy Onto Innovation Inc.?

Onto Innovation appears to be a company with manageable debt but a very unfavorable moat, as declining ROIC suggests value erosion. While profitability shows some operational efficiency, the overall B- rating reflects moderate financial strength with notable valuation risks.

Strength & Efficiency Pillars

Onto Innovation Inc. maintains solid operational efficiency, reflected by a robust gross margin of 49.72% and a net margin of 13.6%. The company delivers favorable EBIT margin at 13.22%, underscoring operational control. However, return on invested capital (ROIC) stands at 5.19%, below its weighted average cost of capital (WACC) at 10.6%, signaling value erosion rather than creation. Its zero debt load and infinite interest coverage further enhance financial flexibility, despite challenges in profitability metrics.

Weaknesses and Drawbacks

The company faces valuation headwinds, with a high price-to-earnings ratio of 59.58 and a price-to-book ratio of 3.88, indicating a premium valuation that may not be justified by earnings growth. The current ratio at 5.79, although seemingly strong, is flagged unfavorable, possibly reflecting inefficient asset use or liquidity mismanagement. Declining earnings per share and net margin growth over the last year add to concerns. Asset turnover at 0.42 also signals suboptimal asset utilization.

Our Final Verdict about Onto Innovation Inc.

Onto Innovation’s financial profile is mixed. It operates in a safe zone with an Altman Z-Score of 26.17, indicating no immediate bankruptcy risk. Despite a bullish overall stock trend and buyer dominance of 57.21% recently, the company’s value destruction and stretched valuation suggest caution. The profile might appear suitable for investors seeking long-term exposure but could warrant a wait-and-see approach given underlying profitability pressures and market premium.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Decoding Onto Innovation Inc (ONTO): A Strategic SWOT Insight – GuruFocus (Feb 25, 2026)

- The Bull Case For Onto Innovation (ONTO) Could Change Following Major Dragonfly Deal And AI Packaging Momentum – Learn Why – simplywall.st (Feb 25, 2026)

- Vanguard Group Inc. Boosts Stake in Onto Innovation Inc. $ONTO – MarketBeat (Feb 24, 2026)

- Onto Innovation (ONTO) Misses Q4 Earnings Estimates – Yahoo Finance (Feb 19, 2026)

- B. Riley Raises PT on Onto Innovation Inc. (ONTO) Stock – Insider Monkey (Feb 23, 2026)

For more information about Onto Innovation Inc., please visit the official website: ontoinnovation.com