Home > Analyses > Consumer Cyclical > Norwegian Cruise Line Holdings Ltd.

Norwegian Cruise Line Holdings transforms travel dreams into vivid realities across the globe’s most captivating waters. It commands a leading role in the cruise industry with its trio of distinct brands—Norwegian Cruise Line, Oceania Cruises, and Regent Seven Seas Cruises—renowned for innovation, luxury, and diverse itineraries. As the travel sector rebounds, I question whether NCLH’s current valuation reflects its growth trajectory and ability to navigate ongoing market volatility.

Table of contents

Business Model & Company Overview

Norwegian Cruise Line Holdings Ltd., founded in 1966 and headquartered in Miami, Florida, commands a dominant position in the travel services sector. It operates a cohesive ecosystem of cruise brands—Norwegian Cruise Line, Oceania Cruises, and Regent Seven Seas Cruises—offering diverse itineraries across the globe. With a fleet of 28 ships and approximately 59K berths, the company delivers immersive travel experiences spanning Scandinavia to the South Pacific.

The company’s revenue engine blends hardware—its robust cruise fleet—with software and recurring services like onboard sales and travel advisor distribution. Its strategic footprint spans North America, Europe, Asia-Pacific, and beyond, capturing diverse markets. This broad geographic reach, combined with a diversified product offering, fortifies Norwegian’s economic moat and shapes the future of global cruise travel.

Financial Performance & Fundamental Metrics

I will analyze Norwegian Cruise Line Holdings Ltd.’s income statement, key financial ratios, and dividend payout policy to assess its core financial health and shareholder returns.

Income Statement

The following table summarizes Norwegian Cruise Line Holdings Ltd.’s annual income statement figures from 2021 to 2025, expressed in USD.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 648M | 4.84B | 8.55B | 9.48B | 9.83B |

| Cost of Revenue | 1.61B | 4.27B | 5.47B | 5.69B | 5.64B |

| Operating Expenses | 1.59B | 2.13B | 2.15B | 2.33B | 1.55B |

| Gross Profit | -960M | 577M | 3.08B | 3.79B | 4.19B |

| EBITDA | -1.67B | -665M | 1.77B | 2.49B | 543M |

| EBIT | -2.43B | -1.48B | 891M | 1.52B | 0 |

| Interest Expense | 2.07B | 801M | 728M | 747M | 2.23B |

| Net Income | -4.51B | -2.27B | 166M | 910M | 423M |

| EPS | -12.33 | -5.41 | 0.39 | 2.09 | 0.94 |

| Filing Date | 2022-03-01 | 2023-02-28 | 2024-02-28 | 2025-02-27 | 2026-03-02 |

Income Statement Evolution

Norwegian Cruise Line Holdings Ltd. shows strong revenue growth of 3.7% from 2024 to 2025, continuing a robust five-year uptrend of 1417%. Gross profit expanded 10.5% last year, improving margins to a favorable 42.6%. However, EBIT margin dropped to zero, signaling cost pressures. Net margin remains stable at 4.3%, reflecting mixed profitability trends.

Is the Income Statement Favorable?

The 2025 income statement reveals solid top-line momentum with revenue nearing $9.8B. Gross margin strength offsets rising operating expenses, though EBIT stagnation raises concerns. Interest expense is well-managed at -22.7% of revenue, supporting financial stability. Net margin is neutral, with earnings per share down 52%, indicating near-term profit challenges despite favorable longer-term fundamentals.

Financial Ratios

The table below presents key financial ratios for Norwegian Cruise Line Holdings Ltd. over recent fiscal years, reflecting profitability, liquidity, leverage, efficiency, and dividend metrics:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | -695% | -469% | 1.94% | 9.60% | 4.31% |

| ROE | -185% | -3309% | 55.2% | 63.9% | 19.2% |

| ROIC | -16.1% | -10.7% | 6.12% | 9.43% | 8.69% |

| P/E | -1.68x | -2.26x | 51.2x | 12.3x | 24.0x |

| P/B | 3.12x | 74.9x | 28.3x | 7.86x | 4.60x |

| Current Ratio | 0.89 | 0.37 | 0.22 | 0.17 | 0.21 |

| Quick Ratio | 0.85 | 0.34 | 0.19 | 0.15 | 0.18 |

| D/E | 5.12x | 199x | 46.7x | 9.76x | 6.61x |

| Debt-to-Assets | 66.5% | 73.4% | 72.1% | 69.7% | 64.8% |

| Interest Coverage | -1.23x | -1.94x | 1.28x | 1.96x | -0.70x |

| Asset Turnover | 0.035x | 0.26x | 0.44x | 0.47x | 0.44x |

| Fixed Asset Turnover | 0.048x | 0.33x | 0.52x | 0.56x | 0.52x |

| Dividend Yield | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% |

Evolution of Financial Ratios

Norwegian Cruise Line’s Return on Equity (ROE) showed strong recovery, rising to 19.15% in 2025, reflecting improved profitability. The Current Ratio remained low around 0.21, signaling persistent liquidity challenges. Meanwhile, the Debt-to-Equity Ratio stayed elevated at 6.61, indicating sustained high leverage levels over the period.

Are the Financial Ratios Fovorable?

The 2025 financial ratios reveal mixed signals. Profitability is favorable on ROE and WACC but net margin is weak at 4.31%. Liquidity ratios, including Current and Quick Ratios, are unfavorable, highlighting short-term financial stress. Leverage metrics remain high with Debt-to-Equity and Debt-to-Assets ratios unfavorable. Market multiples such as P/E and P/B ratios are mostly neutral to unfavorable, resulting in an overall unfavorable financial health assessment.

Shareholder Return Policy

Norwegian Cruise Line Holdings Ltd. (NCLH) does not pay dividends, reflecting its reinvestment strategy amid recent negative and volatile free cash flow. The company also does not engage in share buybacks, focusing resources on capital expenditures exceeding operating cash flow.

This approach aligns with prioritizing growth and operational recovery over immediate returns. However, sustained negative free cash flow and high leverage pose risks to long-term value creation. The current policy supports reinvestment but requires careful monitoring for financial stability.

Score analysis

The following radar chart illustrates Norwegian Cruise Line Holdings Ltd.’s key financial scores across valuation, profitability, and leverage metrics:

The company shows a moderate discounted cash flow score and a very favorable return on equity. However, return on assets and price-to-earnings scores are unfavorable. Debt-to-equity and price-to-book scores rank very unfavorably, signaling capital structure concerns.

Analysis of the company’s bankruptcy risk

The Altman Z-Score places Norwegian Cruise Line Holdings Ltd. firmly in the distress zone, indicating a high risk of bankruptcy based on financial distress measures:

Is the company in good financial health?

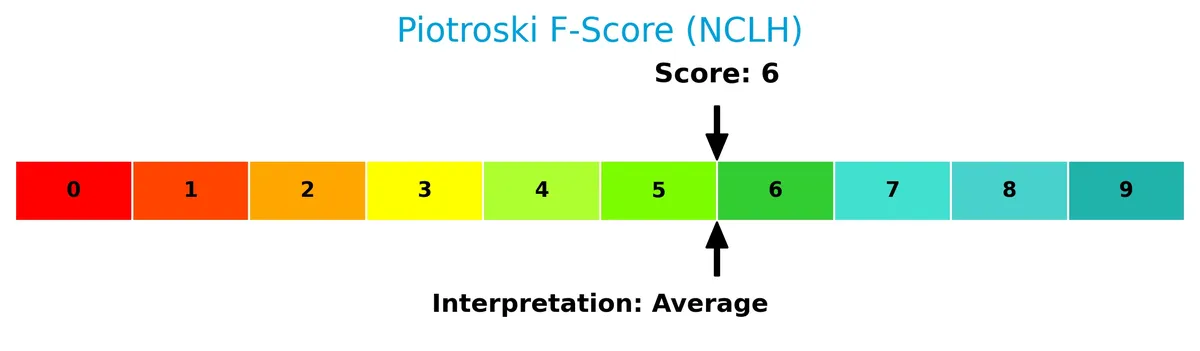

The Piotroski Score diagram highlights the company’s financial strength based on nine key accounting criteria:

A score of 6 suggests average financial health. This indicates some strengths but also areas requiring improvement to enhance overall stability.

Competitive Landscape & Sector Positioning

This sector analysis examines Norwegian Cruise Line Holdings Ltd.’s strategic positioning, revenue segments, key products, and main competitors. I will assess whether the company holds a competitive advantage over its peers in the travel services industry.

Strategic Positioning

Norwegian Cruise Line Holdings Ltd. maintains a diversified product portfolio with three cruise brands and itineraries spanning 3 to 180 days across North America, Europe, Asia-Pacific, and other regions. Revenue streams split between passenger tickets and onboard services reflect broad geographic exposure and service integration.

Revenue by Segment

This pie chart displays Norwegian Cruise Line Holdings Ltd.’s revenue breakdown by segment for the fiscal year 2025, highlighting the relative contribution of passenger ticket sales and onboard services.

Passenger ticket revenue dominates with $6.7B in 2025, reflecting strong demand for core cruise experiences. Onboard and other revenue, at $3.1B, shows steady growth, enhancing profitability through ancillary services. The business continues to rely heavily on passenger ticket sales, but the increasing onboard revenue signals successful capital allocation to diversify income streams and improve customer spend per cruise.

Key Products & Brands

The following table outlines Norwegian Cruise Line Holdings’ main revenue-generating products and their descriptions:

| Product | Description |

|---|---|

| Passenger ticket | Revenue from the sale of cruise tickets, covering itineraries from 3 to 180 days across global destinations. |

| Onboard and other | Income from onboard services including dining, entertainment, retail, and other ancillary offerings during cruises. |

Norwegian Cruise Line Holdings generates most revenue from passenger tickets, reflecting its core cruise operations. Onboard sales complement ticket income, enhancing overall profitability through ancillary services.

Main Competitors

The sector includes 5 competitors, with the following 5 top leaders ranked by market capitalization:

| Competitor | Market Cap. |

|---|---|

| Booking Holdings Inc. | 172B |

| Airbnb, Inc. | 82.3B |

| Royal Caribbean Cruises Ltd. | 77.2B |

| Expedia Group, Inc. | 33.1B |

| Norwegian Cruise Line Holdings Ltd. | 10.4B |

Norwegian Cruise Line Holdings Ltd. ranks 5th among its competitors. Its market cap is 5.88% of the leader, Booking Holdings Inc. The company stands below both the average market cap of the top 10 (75B) and the median market cap in the sector (77.2B). It trails Royal Caribbean by 228%, highlighting a significant gap with its closest rival.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does NCLH have a competitive advantage?

Norwegian Cruise Line Holdings Ltd. does not yet demonstrate a clear competitive advantage, as it currently sheds value with ROIC below WACC. However, its profitability shows a favorable upward trend.

The company’s diverse global footprint across North America, Europe, and Asia-Pacific offers growth opportunities. Continued expansion and new itineraries may enhance future competitive positioning.

SWOT Analysis

This SWOT analysis highlights Norwegian Cruise Line Holdings Ltd.’s key internal and external factors shaping its strategic outlook.

Strengths

- strong brand portfolio

- growing ROIC trend

- favorable gross profit growth

Weaknesses

- low liquidity ratios

- high debt leverage

- negative interest coverage

Opportunities

- expanding Asia-Pacific market

- increasing demand for luxury cruises

- digital sales channel growth

Threats

- economic sensitivity

- rising fuel costs

- geopolitical travel restrictions

Norwegian Cruise Line shows improving profitability but remains burdened by liquidity and leverage risks. Strategic focus on growth markets and operational efficiency is critical to mitigate external pressures.

Stock Price Action Analysis

The weekly stock chart below illustrates Norwegian Cruise Line Holdings Ltd.’s price movement over the past 12 months:

Trend Analysis

Over the past 12 months, NCLH’s stock price rose 24.82%, signaling a bullish trend. The price peaked at 28.35 and bottomed at 15.69, with volatility reflected by a 3.62 std deviation. The upward trend shows deceleration, indicating momentum is slowing.

Volume Analysis

Trading volume for the last three months is increasing, with buyers accounting for 58.71% of activity. The volume appears slightly buyer-driven, suggesting moderate investor confidence and steady market participation.

Target Prices

Analysts project a moderate upside for Norwegian Cruise Line Holdings Ltd., reflecting cautious optimism in the sector.

| Target Low | Target High | Consensus |

|---|---|---|

| 20 | 33 | 25.38 |

The target range suggests potential growth, but the spread indicates varied confidence levels among analysts. Overall, expectations remain cautiously positive.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section analyzes grades and consumer feedback related to Norwegian Cruise Line Holdings Ltd., ticker NCLH.

Stock Grades

The latest analyst grades for Norwegian Cruise Line Holdings Ltd. show a nuanced shift in sentiment across major firms:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| JP Morgan | Downgrade | Neutral | 2026-02-13 |

| Barclays | Downgrade | Equal Weight | 2026-02-11 |

| Stifel | Maintain | Buy | 2026-02-11 |

| JP Morgan | Maintain | Overweight | 2026-01-20 |

| Citigroup | Maintain | Buy | 2026-01-14 |

| Wells Fargo | Maintain | Overweight | 2026-01-13 |

| TD Cowen | Maintain | Buy | 2026-01-13 |

| B of A Securities | Maintain | Neutral | 2026-01-12 |

| Barclays | Maintain | Overweight | 2025-12-17 |

| Jefferies | Downgrade | Hold | 2025-12-15 |

Overall, the trend indicates a slight cooling from overweight and buy ratings toward more neutral and hold positions. This suggests some caution among analysts despite a majority consensus to buy.

Consumer Opinions

Consumers express mixed emotions about Norwegian Cruise Line Holdings Ltd. (NCLH), reflecting both enthusiasm and concern.

| Positive Reviews | Negative Reviews |

|---|---|

| “Exceptional onboard entertainment and amenities.” | “Cabin cleanliness was below expectations.” |

| “Friendly and attentive crew throughout the trip.” | “Frequent itinerary changes caused inconvenience.” |

| “Great value for the price paid.” | “Dining options felt limited and repetitive.” |

Overall, consumers praise NCLH for its engaging entertainment and service quality. However, recurring complaints about cabin upkeep and itinerary reliability suggest areas needing improvement.

Risk Analysis

The table below summarizes Norwegian Cruise Line Holdings Ltd.’s key risks, highlighting their likelihood and potential impact:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Financial Health | Extremely low current and quick ratios signal liquidity stress. | High | High |

| Leverage | Debt-to-assets ratio at 64.8% exposes vulnerability to interest hikes. | High | High |

| Profitability | Low net margin at 4.31% limits buffer against downturns. | Medium | Medium |

| Market Volatility | Beta of 2.04 shows high sensitivity to market swings. | High | Medium |

| Bankruptcy Risk | Altman Z-score at 0.31 places company in distress zone. | High | High |

| Dividend Policy | No dividend yield may deter income-focused investors. | Medium | Low |

| Operational Efficiency | Low asset turnover ratios indicate weak asset utilization. | Medium | Medium |

I emphasize financial distress risks. The Altman Z-score well below 1.8 signals a serious bankruptcy threat. High leverage compounds this risk, especially amid rising interest rates. Liquidity ratios below 0.3 are rare in this sector and raise red flags. Despite a favorable ROE, profitability and efficiency metrics lag peers. Investors must weigh these headwinds carefully.

Should You Buy Norwegian Cruise Line Holdings Ltd.?

Norwegian Cruise Line Holdings Ltd. appears to be improving profitability with a slightly favorable moat supported by growing ROIC, yet it carries a substantial leverage profile and weak liquidity. The overall B- rating suggests moderate operational efficiency but elevated financial risk.

Strength & Efficiency Pillars

Norwegian Cruise Line Holdings Ltd. exhibits operational resilience with a gross margin of 42.62%, signaling efficient core activities. The return on equity stands at a favorable 19.15%, reflecting solid shareholder returns. Its return on invested capital (8.69%) slightly exceeds its weighted average cost of capital (7.58%), positioning the company as a modest value creator. Despite a neutral net margin of 4.31%, the company’s growing ROIC trend underlines improving profitability, though it has not yet secured a sustainable competitive moat.

Weaknesses and Drawbacks

The company is in financial distress, with an Altman Z-Score of 0.31, well below the 1.8 threshold, indicating a high bankruptcy risk. This solvency concern overrides profitability metrics and signals acute risk for investors. Norwegian Cruise Line’s leverage profile is troubling, with a debt-to-equity ratio of 6.61 and a current ratio of 0.21, reflecting poor liquidity and heavy debt reliance. Valuation metrics also raise red flags: a price-to-book ratio of 4.6 marks an expensive premium, while the negative interest coverage ratio suggests difficulty servicing debt.

Our Final Verdict about Norwegian Cruise Line Holdings Ltd.

Despite operational strengths and a bullish long-term stock trend, Norwegian Cruise Line’s financial distress and elevated leverage render the investment profile highly speculative. The solvency risk captured by the distress-zone Altman Z-Score makes this stock too risky for conservative capital. Investors might cautiously monitor for structural improvements before considering exposure, as current liabilities and bankruptcy risk overshadow growth signals.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Norwegian Cruise Line: I’m Buying The Q4 Post-Earnings Pullback (NYSE:NCLH) – Seeking Alpha (Mar 02, 2026)

- Norwegian Cruise Line Holdings Ltd. Reports Earnings Results for the Full Year Ended December 31, 2025 – marketscreener.com (Mar 02, 2026)

- Why Is Norwegian Cruise Line Stock Sinking Monday? – Norwegian Cruise Line (NYSE:NCLH) – Benzinga (Mar 02, 2026)

- Decoding Norwegian Cruise Line Holdings Ltd (NCLH): A Strategic SWOT Insight – GuruFocus (Mar 03, 2026)

- Norwegian Cruise (NCLH) Loses 10.5% on Weak Earnings, Outlook – Finviz (Mar 03, 2026)

For more information about Norwegian Cruise Line Holdings Ltd., please visit the official website: nclhltd.com