Home > Analyses > Consumer Cyclical > International Paper Company

International Paper shapes daily life by delivering essential packaging solutions that protect and preserve goods worldwide. As a giant in the Packaging & Containers industry, it leads with innovative containerboards and cellulose fiber products that serve diverse markets from hygiene to construction. Known for quality and scale, it influences global supply chains profoundly. The key question now: does International Paper’s robust market presence still translate into compelling investment growth in 2026?

Table of contents

Business Model & Company Overview

International Paper Company, founded in 1898 and headquartered in Memphis, Tennessee, stands as a dominant player in the Packaging & Containers industry. With 65K employees, it operates a cohesive ecosystem spanning Industrial Packaging and Global Cellulose Fibers. Its core mission integrates containerboards and specialty pulps, serving diverse sectors from hygiene products to construction materials. This broad yet focused portfolio cements its leadership in sustainable packaging solutions worldwide.

The company’s revenue engine balances manufacturing containerboards with supplying specialty pulps, creating a resilient mix of product lines. It sells directly to end users and through distributors across the Americas, Europe, Asia, and beyond. International Paper’s strategic global footprint and integrated business model build a strong economic moat, positioning it to shape the future of packaging innovation.

Financial Performance & Fundamental Metrics

I analyze International Paper Company’s income statement, key financial ratios, and dividend payout policy to assess its core financial health and shareholder value.

Income Statement

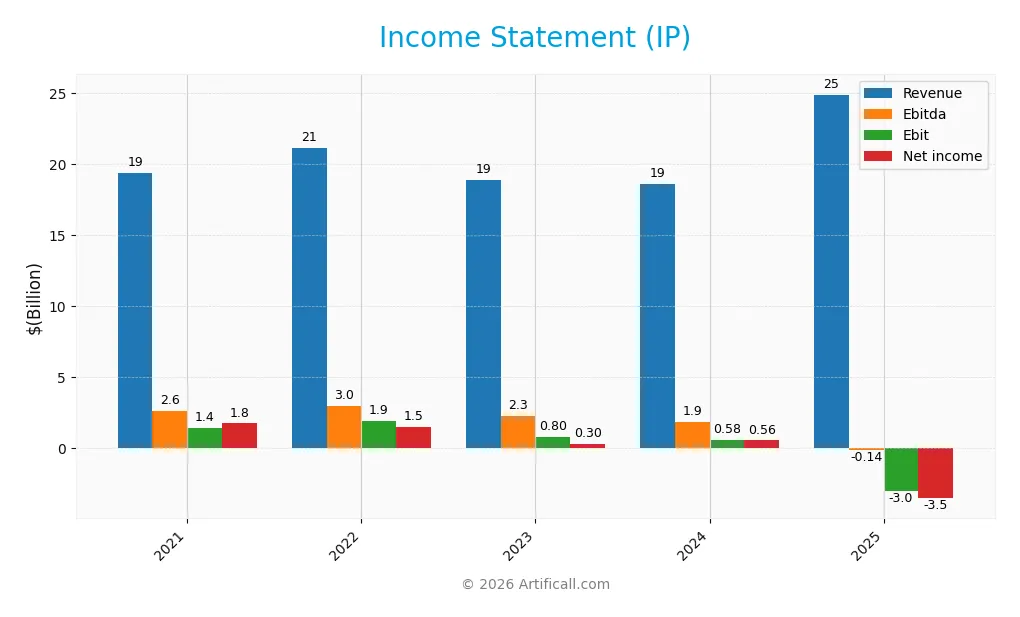

The table below summarizes International Paper Company’s key income statement figures for fiscal years 2021 through 2025, reported in USD.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 19.4B | 21.2B | 18.9B | 18.6B | 24.9B |

| Cost of Revenue | 13.8B | 15.1B | 15.1B | 13.4B | 17.5B |

| Operating Expenses | 4.1B | 4.3B | 2.7B | 4.8B | 10.2B |

| Gross Profit | 5.5B | 6.0B | 3.9B | 5.2B | 7.4B |

| EBITDA | 2.6B | 3.0B | 2.3B | 1.9B | -138M |

| EBIT | 1.4B | 1.9B | 803M | 577M | -2.98B |

| Interest Expense | 430M | 403M | 421M | 430M | 372M |

| Net Income | 1.75B | 1.50B | 302M | 557M | -3.52B |

| EPS | 4.50 | 4.14 | 0.83 | 1.60 | -6.71 |

| Filing Date | 2022-02-18 | 2023-02-17 | 2024-02-16 | 2025-02-21 | 2026-02-27 |

Income Statement Evolution

International Paper’s revenue increased 29% from 2021 to 2025, with a 34% jump in the last year. Gross profit rose 40% year-over-year, lifting gross margins to a favorable 29.5%. However, operating expenses grew proportionally, eroding EBIT margin to a negative 12%, while net income declined sharply, signaling margin compression and profitability challenges.

Is the Income Statement Favorable?

The 2025 income statement reveals significant stress. Despite strong revenue and gross profit growth, operating losses reached $2.82B, dragging net income down to -$3.52B and pushing net margin to -14.1%. Interest expense remains favorable at 1.49% of revenue, but negative EBIT and net margins highlight fundamental weaknesses. Overall, the income profile is unfavorable for investors seeking stable profits.

Financial Ratios

The following table summarizes key financial ratios for International Paper Company over recent fiscal years:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 9.0% | 7.1% | 1.6% | 3.0% | -14.1% |

| ROE | 19.3% | 17.7% | 3.6% | 6.8% | -23.7% |

| ROIC | 5.6% | 8.9% | 5.1% | 2.5% | -7.6% |

| P/E | 10.4 | 8.4 | 41.5 | 33.5 | -5.9 |

| P/B | 2.0 | 1.5 | 1.5 | 2.3 | 1.4 |

| Current Ratio | 1.71 | 1.35 | 1.67 | 1.51 | 1.28 |

| Quick Ratio | 1.27 | 0.97 | 1.19 | 1.09 | 1.02 |

| D/E | 0.64 | 0.69 | 0.71 | 0.72 | 0.73 |

| Debt-to-Assets | 23.0% | 24.5% | 25.4% | 25.7% | 28.5% |

| Interest Coverage | 3.4 | 4.4 | 2.8 | 1.1 | -7.6 |

| Asset Turnover | 0.77 | 0.88 | 0.81 | 0.82 | 0.66 |

| Fixed Asset Turnover | 1.79 | 1.95 | 1.78 | 1.85 | 1.64 |

| Dividend Yield | 4.3% | 5.3% | 5.1% | 3.4% | 4.7% |

Evolution of Financial Ratios

International Paper’s Return on Equity (ROE) declined sharply to -23.7% in 2025, reflecting deteriorated profitability. The Current Ratio decreased to 1.28, indicating reduced but still adequate liquidity. Debt-to-Equity remained stable around 0.73, showing consistent leverage. Profit margins worsened substantially, with net margin falling to -14.1%, signaling pressure on earnings.

Are the Financial Ratios Favorable?

In 2025, profitability ratios like ROE and net margin were unfavorable, undermining earnings quality. Liquidity ratios, particularly the quick ratio at 1.02, were favorable, supporting short-term obligations. Leverage measured by debt-to-assets at 28.5% was favorable, indicating moderate risk. Efficiency metrics such as asset turnover were neutral. Market valuation ratios and dividend yield remained favorable, leading to a slightly favorable overall ratios assessment.

Shareholder Return Policy

International Paper Company maintains a dividend policy despite reporting a net loss in 2025. The dividend payout ratio is negative at -28%, yet the company delivered a 4.7% dividend yield with a steady dividend per share near $1.85. Share buybacks are not explicitly mentioned.

The negative earnings and free cash flow coverage ratios suggest dividend sustainability risks. However, the consistent dividend and buyback approach implies a commitment to shareholder returns, though it may pressure long-term value if losses persist.

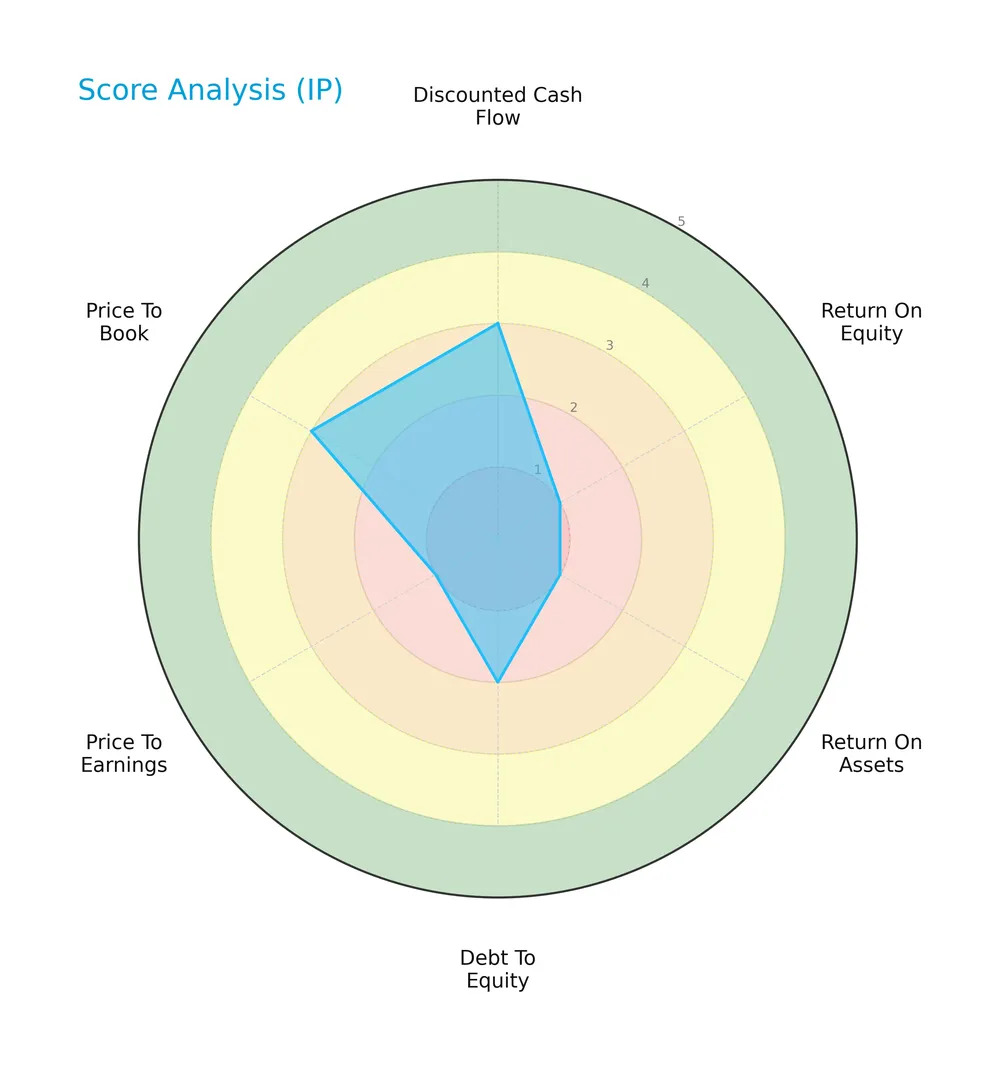

Score analysis

Here is a radar chart illustrating International Paper Company’s key financial scores for investor evaluation:

The company shows moderate strength in discounted cash flow and price-to-book metrics. However, its return on equity, return on assets, and price-to-earnings scores are very unfavorable, while debt-to-equity remains unfavorable, signaling financial challenges.

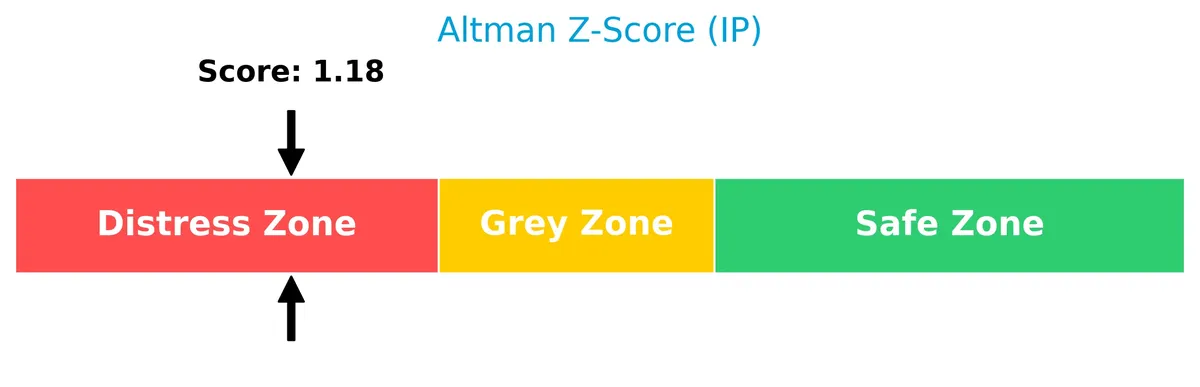

Analysis of the company’s bankruptcy risk

International Paper Company’s Altman Z-Score places it in the distress zone, indicating a high risk of bankruptcy:

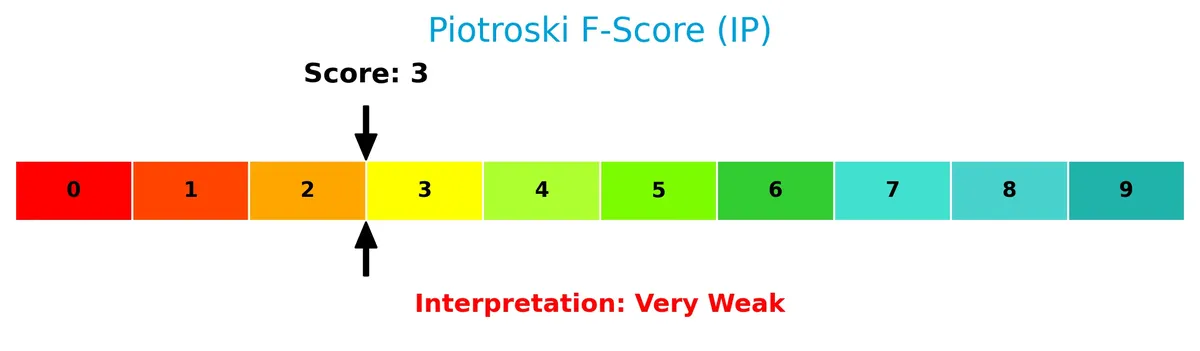

Is the company in good financial health?

The Piotroski Score diagram highlights the company’s current financial health status:

With a very weak Piotroski Score of 3, the company exhibits poor financial strength, reflecting significant weaknesses in profitability, leverage, liquidity, or operational efficiency.

Competitive Landscape & Sector Positioning

This analysis examines International Paper Company’s sector positioning, revenue segments, and key products. I will assess whether the company maintains a competitive advantage against its main competitors.

Strategic Positioning

International Paper concentrates its portfolio around Industrial Packaging, generating over 14B in North America and 1.35B in EMEA in 2024. Its Global Cellulose Fibers segment contributes roughly 2.8B. The company operates across the US, EMEA, Asia, and the Americas, reflecting moderate geographic diversification.

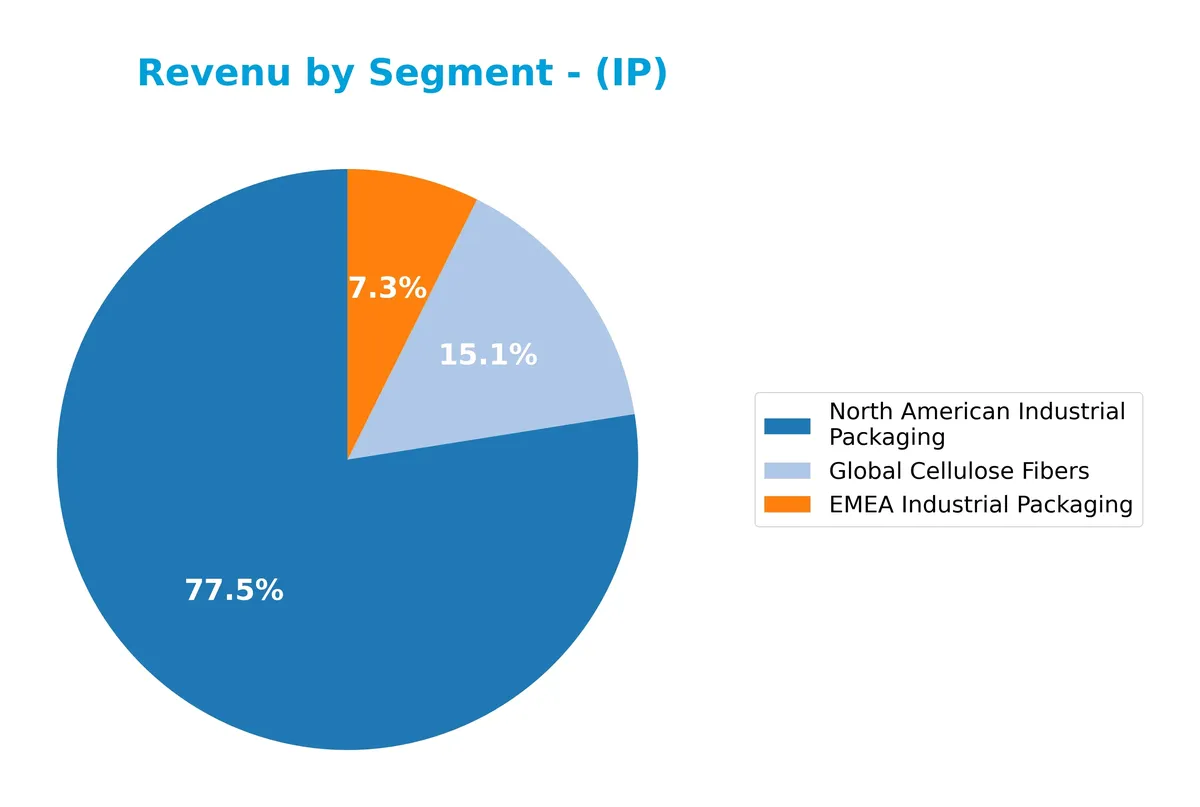

Revenue by Segment

This pie chart illustrates International Paper Company’s revenue breakdown by product segment for the fiscal year 2024, highlighting the business’s core revenue drivers.

In 2024, North American Industrial Packaging dominates with $14.3B, underscoring its critical role. Global Cellulose Fibers contribute $2.8B, showing slight contraction from prior years. EMEA Industrial Packaging adds $1.4B, reflecting geographic diversification. The recent shift from a broad Industrial Packaging category to regional segmentation suggests strategic refinement. Overall, the business remains concentrated in packaging, with modest declines in fibers signaling evolving market dynamics.

Key Products & Brands

Below is an overview of International Paper Company’s key products and brands by segment:

| Product | Description |

|---|---|

| Industrial Packaging | Manufactures containerboards including linerboard, medium, whitetop, recycled linerboard, recycled medium, and saturating kraft. |

| Global Cellulose Fibers | Produces fluff, market, and specialty pulps for absorbent hygiene products, tissue, paper, textiles, filtration, and coatings. |

International Paper focuses on two main segments: Industrial Packaging, which dominates revenue, and Global Cellulose Fibers, supplying specialty pulps for diverse industrial and consumer applications.

Main Competitors

There are 5 competitors in the Packaging & Containers industry, with the table showing the top 5 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| International Paper Company | 21.3B |

| Smurfit Westrock Plc | 20.7B |

| Amcor plc | 19.4B |

| Packaging Corporation of America | 19.0B |

| Ball Corporation | 14.3B |

International Paper Company ranks 1st among its competitors with a market cap 8.2% above the sector leader benchmark. It stands above both the average market cap of the top 10 and the median in its sector. The company leads the pack with an 11.2% gap below to its nearest competitor.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does IP have a competitive advantage?

International Paper Company currently lacks a competitive advantage, as it consistently destroys value with a ROIC significantly below its WACC and a sharply declining profitability trend. Its industrial packaging and cellulose fibers segments face profitability challenges despite solid gross margins and revenue growth.

Looking ahead, IP’s global footprint across the US, EMEA, and emerging markets offers opportunities to leverage new product applications in hygiene and specialty pulps. Expanding market presence and innovating within absorbent and non-woven products could support future growth despite near-term value erosion.

SWOT Analysis

This analysis highlights International Paper Company’s key strategic factors to guide investment decisions.

Strengths

- Leading market position in packaging

- Diversified geographic presence

- Strong dividend yield (4.7%)

Weaknesses

- Negative net margin (-14.12%)

- Declining ROIC, destroying value

- Weak profitability metrics (ROE -23.7%)

Opportunities

- Rising global demand for sustainable packaging

- Expansion in emerging markets

- Innovation in cellulose fibers

Threats

- High competition in packaging sector

- Economic sensitivity in cyclical markets

- Financial distress risk (Altman Z-score 1.24)

International Paper faces significant profitability and value destruction challenges despite market leadership and solid dividends. Strategic focus must be on operational efficiency and innovation to mitigate financial risks.

Stock Price Action Analysis

The following weekly chart illustrates International Paper Company’s stock price movement over the past 100 weeks, capturing its key highs and lows:

Trend Analysis

Over the past 12 months, IP’s stock gained 12.65%, signaling a bullish trend with accelerating momentum. The price ranged from a low of 33.83 to a high of 60.09, reflecting strong upward movement supported by a 5.9 standard deviation, indicating notable volatility.

Volume Analysis

In the last three months, trading volumes increased but showed slight seller dominance at 56.81%. This suggests cautious investor sentiment, with higher selling pressure despite growing market participation. The volume trend’s increase points to active but hesitant trading dynamics.

Target Prices

Analysts set a clear target price consensus for International Paper Company.

| Target Low | Target High | Consensus |

|---|---|---|

| 40 | 57.8 | 47.97 |

The target range reflects moderate optimism, with analysts expecting a 10–20% upside from current levels. This aligns with sector recovery trends I’ve observed.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section examines the latest analyst grades and consumer feedback related to International Paper Company (IP).

Stock Grades

Here are the recent verified stock grades for International Paper Company from recognized grading firms:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| UBS | Downgrade | Neutral | 2026-02-02 |

| Citigroup | Maintain | Buy | 2026-02-02 |

| RBC Capital | Maintain | Outperform | 2026-01-30 |

| Wells Fargo | Upgrade | Equal Weight | 2026-01-30 |

| UBS | Maintain | Buy | 2026-01-12 |

| Truist Securities | Maintain | Buy | 2026-01-06 |

| Argus Research | Maintain | Buy | 2025-12-22 |

| JP Morgan | Maintain | Neutral | 2025-12-05 |

| Citigroup | Maintain | Buy | 2025-11-03 |

| RBC Capital | Maintain | Outperform | 2025-10-31 |

The overall trend shows a majority of Buy and Outperform ratings, offset by a few Neutral and Equal Weight grades. UBS’s recent downgrade to Neutral signals some caution despite the dominant positive sentiment.

Consumer Opinions

Consumers express mixed feelings about International Paper Company, reflecting both satisfaction with product quality and concerns about customer service.

| Positive Reviews | Negative Reviews |

|---|---|

| Products are consistently high-quality and reliable. | Customer service response times are slow. |

| Packaging solutions are innovative and eco-friendly. | Some clients report delays in delivery. |

| Strong commitment to sustainability resonates well. | Pricing can be higher than competitors. |

Overall, consumers praise International Paper’s product reliability and environmental efforts. However, slow customer support and occasional delivery issues remain notable weaknesses.

Risk Analysis

Below is a summary of the key risks facing International Paper Company, highlighting likelihood and potential impact:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Financial Health | Altman Z-Score of 1.24 places IP in the distress zone, signaling bankruptcy risk. | High | Severe |

| Profitability | Negative net margin (-14.12%) and ROE (-23.71%) reflect ongoing losses. | High | High |

| Interest Coverage | Negative interest coverage (-8.01) indicates difficulty servicing debt. | Medium | High |

| Market Volatility | Beta of 1.07 shows sensitivity to market swings, increasing stock price risk. | Medium | Medium |

| Dividend Sustainability | 4.7% yield may be at risk amid weak earnings and cash flow. | Medium | Medium |

| Operational Efficiency | Asset turnover of 0.66 is neutral but leaves limited room for improvement. | Low | Medium |

The most alarming risks are financial distress and persistent unprofitability. With an Altman Z-Score in the distress zone and a very weak Piotroski score of 3, IP faces a high probability of financial strain. Interest coverage weakness further threatens debt servicing. Investors should weigh these substantial headwinds against the company’s moderate market sensitivity and dividend yield.

Should You Buy International Paper Company?

International Paper appears to have a deteriorating profitability profile with declining ROIC well below WACC, indicating value destruction. Despite a manageable debt leverage, its overall financial health suggests risks. The company’s rating stands at a cautious C, reflecting an unfavorable outlook.

Strength & Efficiency Pillars

International Paper Company shows operational resilience with a solid gross margin of 29.53%, signaling effective cost control on production. Its interest expense is low at 1.49%, suggesting manageable debt servicing costs. However, profitability metrics paint a challenging picture: net margin is negative at -14.12%, and return on invested capital (ROIC) is also negative at -7.64%, well below the weighted average cost of capital (WACC) of 6.91%. This means the company is currently destroying value rather than creating it.

Weaknesses and Drawbacks

The company is in financial distress, as indicated by an Altman Z-Score of 1.24, placing it in the distress zone and signaling a high bankruptcy risk. Profitability is a major concern with negative net margin (-14.12%) and return on equity (ROE) at -23.71%. The Piotroski score of 3 also highlights weak financial health. While the price-to-book ratio is moderate at 1.4, the negative price-to-earnings ratio reflects losses. Interest coverage is deeply negative at -8.01, underscoring difficulties in covering debt costs. Recent market behavior is slightly seller dominant, adding short-term pressure.

Our Final Verdict about International Paper Company

Despite some operational strengths like gross margin and low interest expense, International Paper Company’s financial distress and persistent losses make its profile highly speculative. The solvency risk posed by the Altman Z-Score of 1.24 outweighs potential growth signals. This company might appear too risky for conservative capital and demands cautious monitoring before considering exposure.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- International Paper (IP) Is Down 7.1% After Georgetown Closure And Regional Split Plan – What’s Changed – simplywall.st (Feb 28, 2026)

- INTERNATIONAL PAPER CO /NEW/ SEC 10-K Report – TradingView (Feb 27, 2026)

- International Paper to close South Carolina container plant – Recycling Today (Feb 26, 2026)

- Close Asset Management Ltd Has $1.94 Million Position in International Paper Company $IP – MarketBeat (Feb 27, 2026)

- International Paper further downsizing in South Carolina – Packaging Dive (Feb 25, 2026)

For more information about International Paper Company, please visit the official website: internationalpaper.com