Home > Analyses > Consumer Defensive > Inter Parfums, Inc.

Inter Parfums, Inc. crafts the scents that define luxury and personal identity worldwide. Renowned for its portfolio of prestigious fragrance brands like Coach and Jimmy Choo, it blends artistry with market reach in the Household & Personal Products sector. The company’s reputation for innovation and quality secures its leadership across global markets. As competition intensifies, I question whether Inter Parfums’ strong fundamentals continue to justify its current valuation and growth outlook.

Table of contents

Business Model & Company Overview

Inter Parfums, Inc., founded in 1982 and headquartered in New York City, commands a dominant position in the Household & Personal Products industry. It crafts a cohesive ecosystem of luxury fragrances and related products under prestigious brands like Coach, Jimmy Choo, and Montblanc. This portfolio targets a diverse clientele through department stores, specialty shops, duty-free outlets, and e-commerce channels, blending heritage with innovation across continents.

The company’s revenue engine balances product sales from its two segments: European Based Operations and United States Based Operations. Inter Parfums leverages global reach spanning the Americas, Europe, and Asia to optimize market penetration. Its competitive advantage lies in strong brand licensing and distribution networks, securing its role as a key influencer shaping the global fragrance market’s future.

Financial Performance & Fundamental Metrics

I analyze Inter Parfums, Inc.’s income statement, key financial ratios, and dividend payout policy to assess its core profitability and capital allocation efficiency.

Income Statement

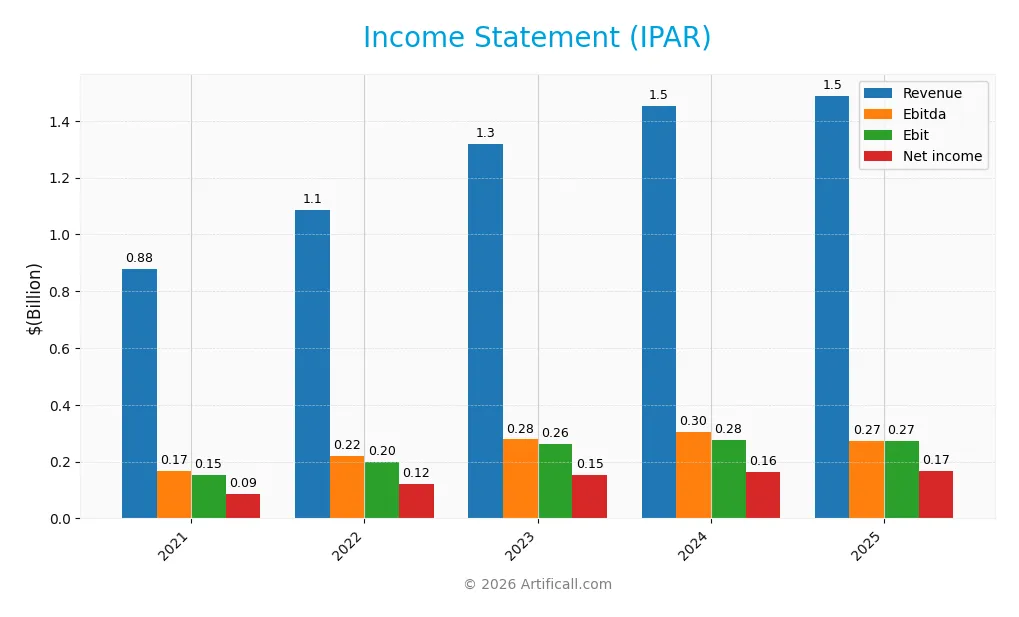

This table summarizes Inter Parfums, Inc.’s key income statement items over the past five fiscal years, reflecting revenue growth and profitability trends.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 880M | 1.09B | 1.32B | 1.45B | 1.49B |

| Cost of Revenue | 323M | 392M | 479M | 525M | 541M |

| Operating Expenses | 409M | 500M | 588M | 653M | 677M |

| Gross Profit | 557M | 694M | 839M | 927M | 947M |

| EBITDA | 167M | 220M | 278M | 305M | 271M |

| EBIT | 154M | 198M | 261M | 276M | 271M |

| Interest Expense | 3M | 4M | 11M | 8M | 0 |

| Net Income | 87M | 121M | 153M | 164M | 168M |

| EPS | 2.76 | 3.80 | 4.77 | 5.13 | 5.25 |

| Filing Date | 2022-03-01 | 2023-02-28 | 2024-02-27 | 2025-03-11 | 2026-03-10 |

Income Statement Evolution

Inter Parfums, Inc. revenue rose 69% from 2021 to 2025, reaching $1.49B in 2025. Net income grew 93% over the same period, hitting $168M. Gross margin held steady near 64%, while net margin improved to 11.3%. However, revenue growth slowed to 2.5% in the last year, with slight declines in EBIT and net margin growth.

Is the Income Statement Favorable?

The 2025 income statement shows solid fundamentals. Gross margin at 63.6% and EBIT margin at 18.2% remain favorable. Interest expense is negligible, supporting profitability. Net margin stands at 11.3%, consistent with historical gains. Despite a modest slowdown in revenue and EBIT growth, overall income statement metrics reflect a favorable financial position for 2025.

Financial Ratios

The table below summarizes key financial ratios for Inter Parfums, Inc. (IPAR) from 2021 to 2025, reflecting profitability, valuation, liquidity, leverage, and efficiency metrics:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 10% | 11% | 12% | 11% | 11% |

| ROE | 15% | 20% | 22% | 22% | 19% |

| ROIC | 12% | 15% | 17% | 18% | 16% |

| P/E | 39 | 25 | 30 | 26 | 16 |

| P/B | 5.9 | 5.0 | 6.6 | 5.7 | 3.1 |

| Current Ratio | 2.9 | 2.3 | 2.6 | 2.8 | 3.0 |

| Quick Ratio | 2.1 | 1.4 | 1.4 | 1.6 | 2.0 |

| D/E | 0.32 | 0.34 | 0.28 | 0.26 | 0.25 |

| Debt-to-Assets | 16% | 16% | 14% | 14% | 14% |

| Interest Coverage | 52 | 54 | 22 | 35 | 0 |

| Asset Turnover | 0.77 | 0.83 | 0.96 | 1.03 | 0.94 |

| Fixed Asset Turnover | 4.8 | 5.6 | 6.7 | 8.1 | 7.1 |

| Dividend Yield | 0.9% | 2.1% | 1.7% | 2.3% | 3.8% |

Evolution of Financial Ratios

Return on Equity (ROE) showed a generally positive trend, peaking around 22.1% in 2024 before settling near 19.1% in 2025. The Current Ratio improved steadily from 2.29 in 2022 to 2.99 in 2025, indicating enhanced liquidity. Debt-to-Equity Ratio declined from 0.34 in 2022 to 0.25 in 2025, reflecting reduced leverage. Profitability margins remained fairly stable over the period.

Are the Financial Ratios Favorable?

In 2025, Inter Parfums exhibited favorable profitability with a net margin of 11.31% and ROE at 19.12%, both above sector medians. Liquidity ratios, including a current ratio of 2.99 and quick ratio of 1.97, were strong. Leverage was conservative, with a debt-to-equity ratio of 0.25 and debt-to-assets at 14.11%. Market valuation metrics were mixed; the P/E ratio was neutral at 16.17, while the P/B ratio was unfavorable at 3.09. Overall, 71% of key ratios were favorable.

Shareholder Return Policy

Inter Parfums, Inc. maintains a dividend payout ratio around 58-61% over recent years, with dividends per share rising steadily to $3.20 in 2025. The annual yield reached approximately 3.77% in 2025, supported by free cash flow coverage and occasional share buybacks.

This payout approach balances shareholder returns with reinvestment capacity, suggesting a sustainable distribution policy. The consistent dividend growth and buybacks indicate management’s commitment to steady shareholder value without risking excessive financial strain.

Score analysis

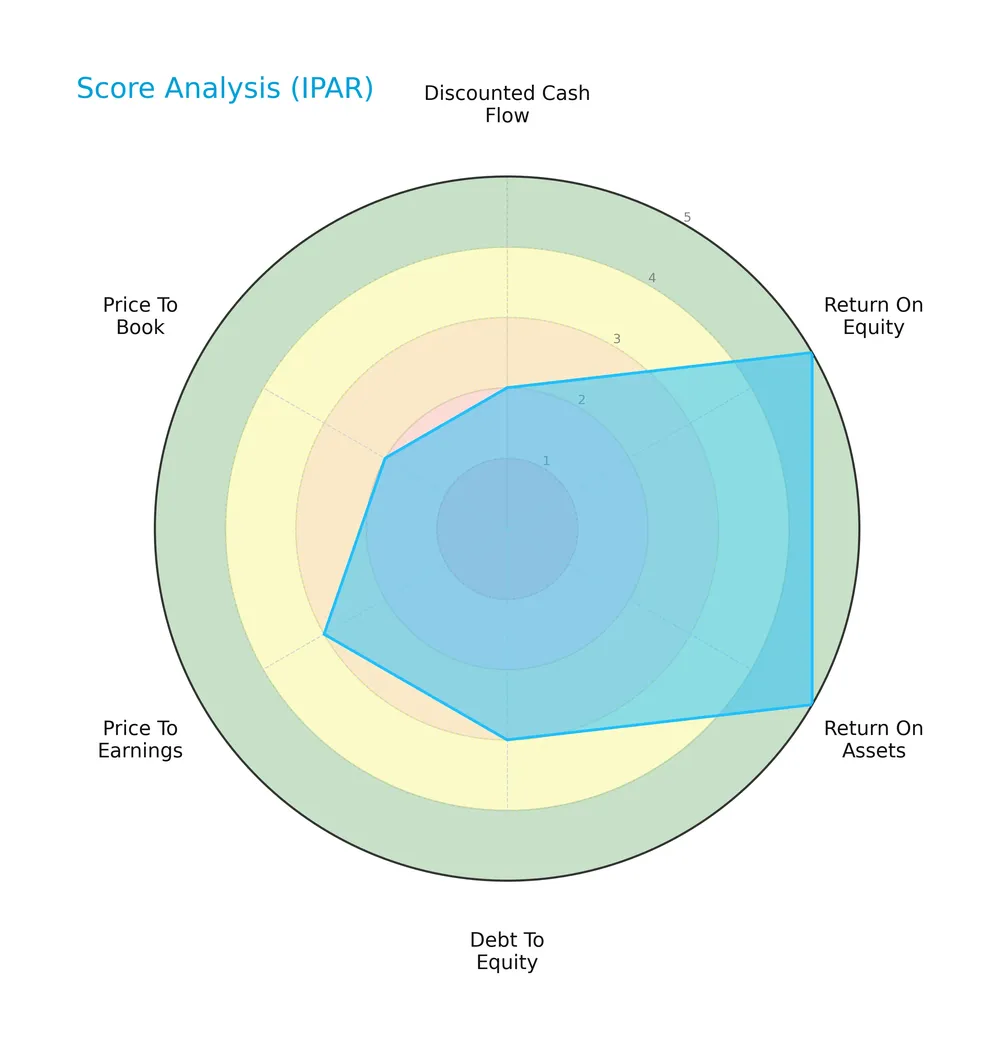

The following radar chart illustrates Inter Parfums, Inc.’s financial metric scores across key valuation and performance indicators:

The company scores very favorably in return on equity and return on assets, reflecting strong profitability. Debt-to-equity and price-to-earnings ratios show moderate standing. Discounted cash flow and price-to-book valuations are less favorable, indicating valuation concerns.

Analysis of the company’s bankruptcy risk

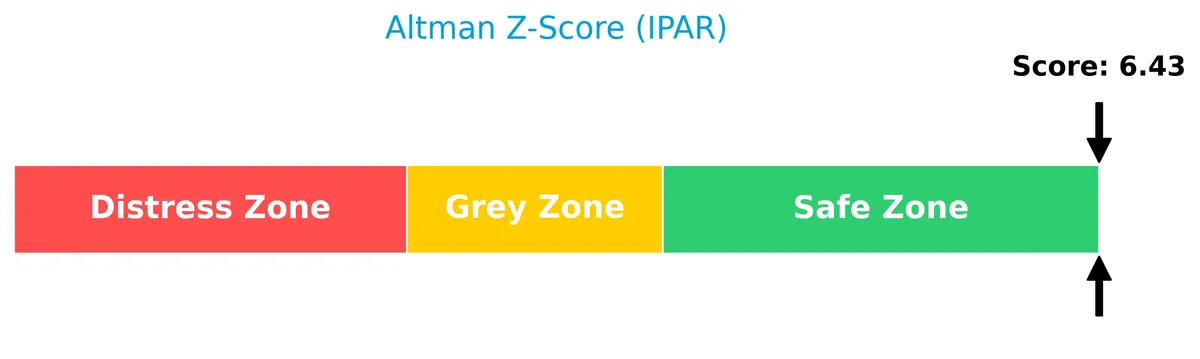

Inter Parfums, Inc. is firmly in the safe zone according to its Altman Z-Score, indicating a low risk of bankruptcy:

Is the company in good financial health?

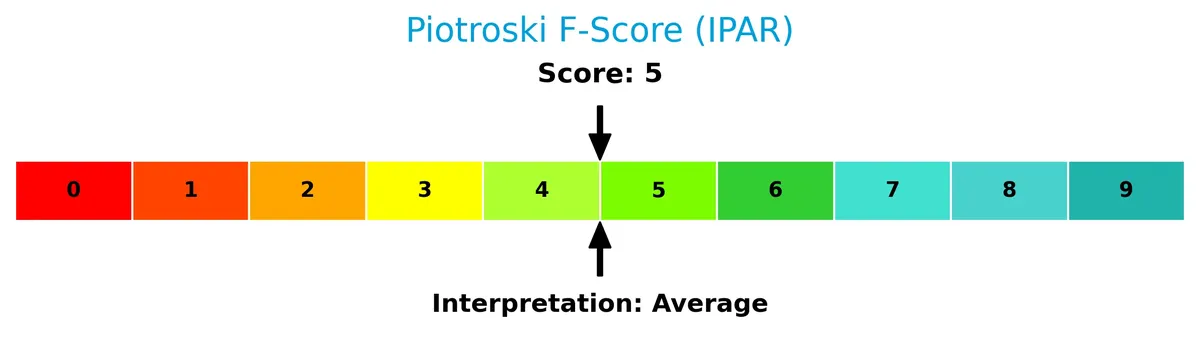

The Piotroski Score diagram provides insights into the company’s financial strength:

With a Piotroski Score of 5, Inter Parfums demonstrates average financial health, suggesting stable but not exceptional operational performance and financial robustness.

Competitive Landscape & Sector Positioning

This sector analysis explores Inter Parfums, Inc.’s strategic positioning, revenue streams, key products, and main competitors. I will assess whether Inter Parfums holds a competitive advantage within the household and personal products industry.

Strategic Positioning

Inter Parfums, Inc. maintains a diversified geographic footprint, with significant revenue from Europe, North America, and Asia. It operates two segments—European and U.S. based—offering a broad portfolio of fragrance brands sold through various retail channels globally, reflecting a balanced international presence.

Revenue by Segment

The pie chart illustrates Inter Parfums, Inc.’s revenue distribution for the fiscal year 2020, highlighting the contribution of its FranceMember segment.

In 2020, Inter Parfums generated $37.6M from its FranceMember segment, the sole reported revenue source. This concentration suggests a narrow product or geographic focus, which may heighten exposure to market fluctuations in that segment. Observing future diversification or segment growth will be essential to assess the company’s risk profile and revenue stability.

Key Products & Brands

Inter Parfums, Inc. offers a diverse portfolio of fragrance and cosmetic products under well-known brand names:

| Product | Description |

|---|---|

| Boucheron | Luxury fragrance brand with a heritage in fine jewelry and perfume. |

| Coach | Popular fashion brand extending into fragrances and cosmetics. |

| Jimmy Choo | High-end footwear and accessories brand with a fragrance line. |

| Karl Lagerfeld | Designer brand offering distinctive perfumes. |

| Kate Spade | Lifestyle brand known for vibrant and youthful fragrances. |

| Lily Aldridge | Celebrity-inspired fragrance brand. |

| Lanvin | Established French fashion house with a classic perfume collection. |

| Moncler | Luxury outerwear brand with fragrance extensions. |

| Montblanc | Premium brand known for writing instruments, watches, and fragrances. |

| Rochas | Iconic French brand producing elegant perfumes. |

| S.T. Dupont | Luxury brand with a focus on fragrances and accessories. |

| Van Cleef & Arpels | Prestigious jewelry brand offering exclusive fragrances. |

| Abercrombie & Fitch | Casual lifestyle brand with accessible fragrance lines. |

| Anna Sui | Fashion brand with a whimsical, youthful perfume range. |

| babe | Fragrance brand with a modern appeal. |

| Dunhill | British luxury brand offering refined scents. |

| Ferragamo | Italian fashion house known for elegant fragrances. |

| Graff | High-end jewelry brand with exclusive perfumes. |

| GUESS | Popular casual fashion brand with a fragrance segment. |

| Hollister | Youth-oriented lifestyle brand with fragrance products. |

| MCM | Premium leather goods brand extending into fragrances. |

| Oscar de la Renta | Renowned fashion designer brand with luxury perfumes. |

| French Connection | Contemporary fashion brand offering fragrance products. |

| Ungaro | French fashion brand with a signature perfume line. |

| Intimate | Fragrance brand focused on personal scents. |

| Aziza | Brand offering a range of fragrance products. |

Inter Parfums, Inc. manages a broad spectrum of brands, from luxury to accessible lifestyle labels. This diversification supports a wide customer base across department stores, specialty retailers, and e-commerce channels internationally.

Main Competitors

There are 17 competitors in total, with the table below listing the top 10 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| The Procter & Gamble Company | 331B |

| Unilever PLC | 143B |

| Colgate-Palmolive Company | 63B |

| The Estée Lauder Companies Inc. | 38B |

| Kimberly-Clark Corporation | 34B |

| Kenvue Inc. | 33B |

| Church & Dwight Co., Inc. | 20B |

| The Clorox Company | 12B |

| e.l.f. Beauty, Inc. | 4.3B |

| Inter Parfums, Inc. | 2.7B |

Inter Parfums ranks 10th among 17 competitors. Its market cap is just 0.88% of the leader, The Procter & Gamble Company. The company sits below both the average market cap of the top 10 (68B) and the sector median (4.3B). It trails its nearest competitor above by 48.77%, indicating a significant gap in scale.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does Inter Parfums, Inc. have a competitive advantage?

Inter Parfums, Inc. presents a clear competitive advantage, evidenced by a ROIC that exceeds its WACC by over 6%, indicating consistent value creation and efficient capital use. The firm’s growing ROIC trend further confirms a strong, sustainable moat in the highly competitive fragrance and personal products sector.

Looking ahead, Inter Parfums leverages a diverse portfolio of premium brands and operates across multiple geographic markets, including Europe, Asia, and North America. This broad presence, combined with ongoing product innovation and market expansion opportunities, supports a favorable outlook for maintaining its competitive position.

SWOT Analysis

This SWOT analysis highlights Inter Parfums, Inc.’s key strategic factors to guide investment decisions.

Strengths

- strong gross margin at 63.6%

- favorable EBIT margin at 18.2%

- very low debt with 0.25 debt-to-equity

Weaknesses

- recent 1-year revenue growth at 2.5% is weak

- unfavorable 1-year EBIT decline at -1.8%

- price-to-book ratio high at 3.09

Opportunities

- expanding global footprint beyond US base

- growing ROIC trend indicates value creation

- rising EPS over long term supports shareholder returns

Threats

- intense competition in fragrance sector

- dependence on licensing agreements

- macroeconomic risks impacting luxury spending

Inter Parfums demonstrates a solid profitability base and capital discipline. However, near-term growth challenges and valuation premium require cautious monitoring. The company’s strategy should leverage its competitive moat while addressing revenue momentum and market risks.

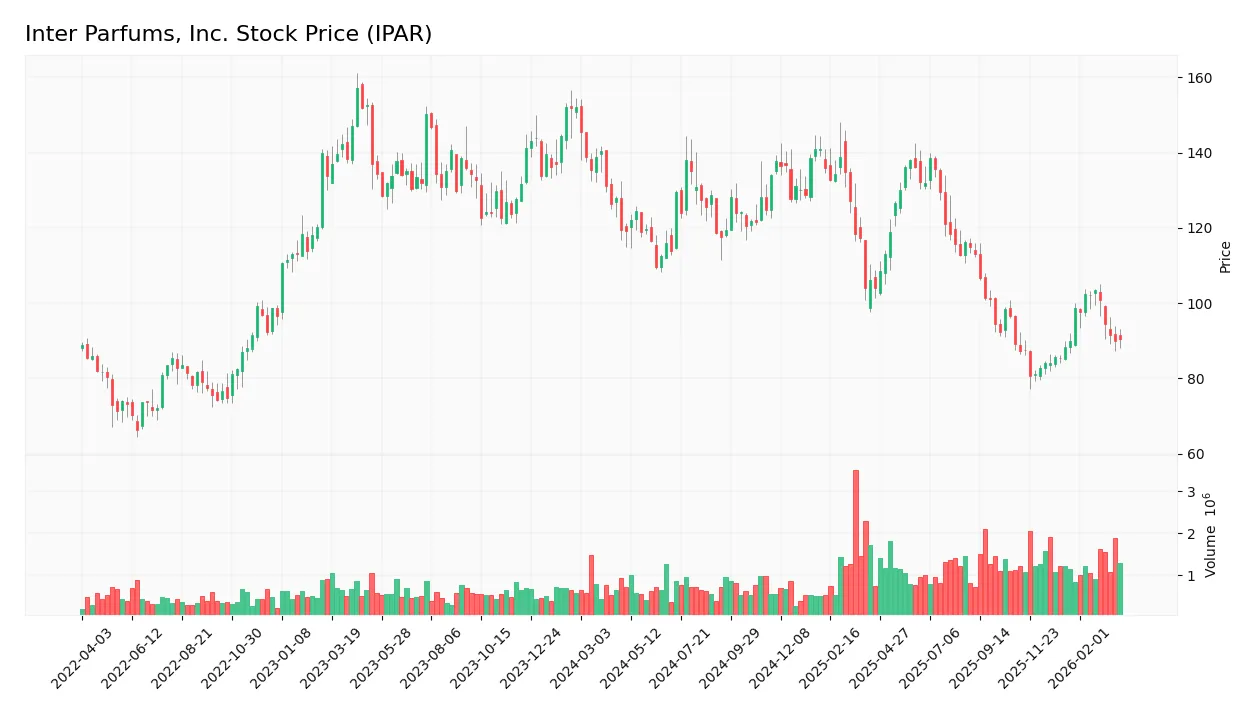

Stock Price Action Analysis

The weekly stock chart below highlights Inter Parfums, Inc.’s price fluctuations and key levels over the past 12 months:

Trend Analysis

Over the past 12 months, IPAR’s stock declined 24%, confirming a bearish trend with accelerating downside momentum. The price ranged from a high of 141.02 to a low of 80.61, reflecting significant volatility (std dev 17.21). Recent months show a mild 2.4% increase but with a negative slope, signaling possible deceleration.

Volume Analysis

Trading volume has increased overall, with sellers accounting for 58% of activity, indicating seller-driven pressure. In the recent three months, seller dominance persists at 55%, despite a slight rise in buyer participation to 45%. This suggests cautious investor sentiment amid ongoing supply pressure.

Target Prices

Analysts present a confident target consensus for Inter Parfums, Inc. (IPAR).

| Target Low | Target High | Consensus |

|---|---|---|

| 103 | 112 | 107.5 |

The target range indicates modest upside potential. Overall, analysts expect steady performance around $107.5, reflecting balanced optimism.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section examines recent analyst ratings and consumer feedback trends related to Inter Parfums, Inc. (IPAR).

Stock Grades

Here are the latest verified stock grades for Inter Parfums, Inc. from recognized financial firms:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| BWS Financial | Maintain | Neutral | 2026-01-29 |

| BWS Financial | Downgrade | Neutral | 2025-11-21 |

| Canaccord Genuity | Maintain | Buy | 2025-11-19 |

| Canaccord Genuity | Maintain | Buy | 2025-11-07 |

| Jefferies | Maintain | Buy | 2025-10-28 |

| BWS Financial | Maintain | Buy | 2025-10-22 |

| Canaccord Genuity | Maintain | Buy | 2025-10-21 |

| BWS Financial | Maintain | Buy | 2025-05-07 |

| Piper Sandler | Maintain | Overweight | 2025-04-24 |

| DA Davidson | Maintain | Buy | 2025-03-25 |

Most firms maintain a Buy rating, though BWS Financial recently downgraded to Neutral. The consensus remains positive, reflecting moderate investor confidence.

Consumer Opinions

Inter Parfums, Inc. enjoys a loyal customer base, but opinions reveal a mix of enthusiasm and caution among consumers.

| Positive Reviews | Negative Reviews |

|---|---|

| Fragrances offer unique, long-lasting scents. | Some products feel overpriced for the quality. |

| Packaging is elegant and enhances gift appeal. | Limited availability in certain regions. |

| Consistent quality across different perfume lines. | Customer service response times can lag. |

Overall, consumers praise Inter Parfums for distinctive scents and premium packaging. However, pricing and occasional supply issues temper enthusiasm. These insights reflect a brand balancing luxury appeal with operational challenges.

Risk Analysis

The table below outlines key risks affecting Inter Parfums, Inc., their likelihood, and potential impact on the business:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Market Volatility | Beta of 1.25 indicates above-average sensitivity to market swings | Medium | Medium |

| Valuation Risk | Price-to-book ratio of 3.09 signals possible overvaluation | Medium | Medium |

| Competitive Pressure | Fragmented luxury fragrance market with many established brands | High | High |

| Supply Chain | Global disruptions could increase costs or delay product delivery | Medium | Medium |

| Consumer Trends | Shifts in preferences might reduce demand for certain brands | Medium | High |

| Financial Health | Altman Z-Score of 6.43 confirms strong financial stability | Low | Low |

The most pressing risks are competitive pressure and changing consumer trends, which directly affect sales and margins. The company’s strong Altman Z-Score reassures on bankruptcy risk but does not eliminate market and brand challenges. I monitor valuation closely, given the elevated price-to-book ratio.

Should You Buy Inter Parfums, Inc.?

Inter Parfums, Inc. appears to be a profitable company with a durable moat, evidenced by its growing ROIC well above WACC. While its leverage profile is manageable, valuation scores suggest some caution; overall, it holds a very favorable A- rating.

Strength & Efficiency Pillars

Inter Parfums, Inc. posts a robust net margin of 11.31% and a return on equity of 19.12%, reflecting solid profitability. Its return on invested capital (ROIC) stands at 15.81%, notably above the weighted average cost of capital (WACC) at 9.43%, confirming the company as a value creator. The firm’s capital allocation supports sustainable competitive advantages, evidenced by a growing ROIC trend of 35.18% over recent years. Strong liquidity ratios with a current ratio of 2.99 reinforce operational efficiency.

Weaknesses and Drawbacks

The company’s price-to-book ratio of 3.09 is unfavorable, signaling potential overvaluation relative to its book value. While the price-to-earnings ratio of 16.17 is moderate, it suggests limited margin for additional multiple expansion. The stock faces mild selling pressure, with buyers accounting for 41.78% of volume and a slightly seller-dominant trend in recent months. Despite low leverage at a debt-to-equity ratio of 0.25, slower revenue growth of 2.49% over the past year flags possible near-term top-line challenges.

Our Final Verdict about Inter Parfums, Inc.

The company boasts a fundamentally strong profile with favorable profitability and value creation markers. However, recent bearish price trends and seller dominance advise caution. Despite its operational strengths, the current market pressure suggests a wait-and-see approach for a better entry point. Inter Parfums may appear attractive for long-term exposure, but investors should monitor valuation levels and market sentiment closely.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Interparfums (NASDAQ:IPAR) Downgraded by Wall Street Zen to Hold – MarketBeat (Mar 28, 2026)

- Interparfums: Planting Seeds In 2026 To Reap Rewards In 2027 (NASDAQ:IPAR) – Seeking Alpha (Mar 25, 2026)

- Vanguard disaggregates holdings; IPAR (NASDAQ: IPAR) shows 0 shares reported – Stock Titan (Mar 27, 2026)

- Interparfums, Inc. (IPAR): A Bull Case Theory – Yahoo Finance (Jan 20, 2026)

- Tudor Investment Corp ET AL Takes $5.16 Million Position in Interparfums, Inc. $IPAR – MarketBeat (Mar 25, 2026)

For more information about Inter Parfums, Inc., please visit the official website: interparfumsinc.com