Home > Analyses > Healthcare > Insulet Corporation

Insulet Corporation revolutionizes diabetes care by delivering a discreet, tubeless insulin system that transforms patients’ daily routines. Its flagship Omnipod device combines ease and innovation, setting a new standard in medical devices. Known for relentless product development and expanding global reach, Insulet shapes the future of insulin delivery. But as competition intensifies, I ask: do its fundamentals still justify its premium valuation and growth ambitions?

Table of contents

Business Model & Company Overview

Insulet Corporation, founded in 2000 and headquartered in Acton, Massachusetts, leads the medical devices sector with its core business centered on insulin delivery systems. Its flagship Omnipod System integrates a tubeless, self-adhesive wearable device and a wireless personal diabetes manager, forming a seamless ecosystem that empowers insulin-dependent patients. This innovative approach cements Insulet’s dominant position in diabetes care technology.

Insulet’s revenue engine blends durable hardware with recurring sales through independent distributors, pharmacies, and direct channels across the Americas, Europe, the Middle East, and Australia. This diversified global footprint supports sustained growth and customer engagement. I view its combination of proprietary device technology and an expanding service network as a powerful competitive advantage that shapes the future of insulin delivery.

Financial Performance & Fundamental Metrics

I analyze Insulet Corporation’s income statement, key financial ratios, and dividend payout policy to assess its earnings quality and capital allocation strategy.

Income Statement

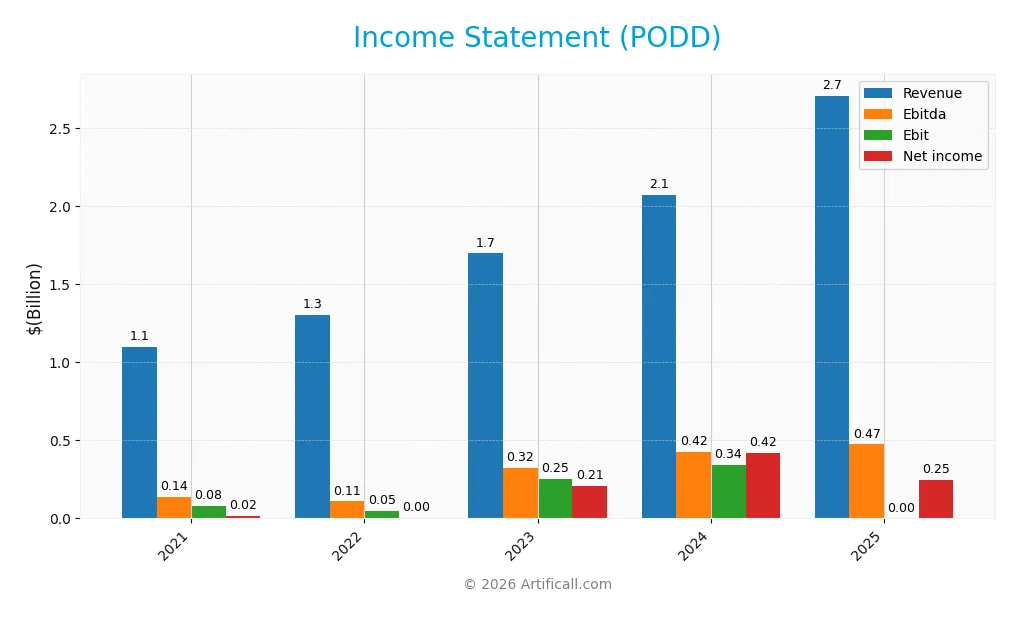

The table below summarizes Insulet Corporation’s key income statement figures for fiscal years 2021 through 2025, reflecting revenue growth and profitability trends.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 1.10B | 1.31B | 1.70B | 2.07B | 2.71B |

| Cost of Revenue | 347M | 500M | 537M | 626M | 768M |

| Operating Expenses | 626M | 768M | 940M | 1.14B | 1.47B |

| Gross Profit | 752M | 806M | 1.16B | 1.45B | 1.94B |

| EBITDA | 140M | 109M | 324M | 424M | 474M |

| EBIT | 82M | 46M | 251M | 343M | 474M |

| Interest Expense | 62M | 36M | 36M | 43M | 25M |

| Net Income | 17M | 5M | 206M | 418M | 247M |

| EPS | 0.25 | 0.066 | 2.96 | 5.97 | 3.51 |

| Filing Date | 2022-02-24 | 2023-02-24 | 2024-02-23 | 2025-02-21 | 2026-02-18 |

Income Statement Evolution

Insulet Corporation’s revenue surged 146% from 2021 to 2025, with a strong 31% increase in 2025 alone. Net income soared over 13x during this period, though it declined 55% in the last year. Gross margin remains robust near 72%, while net margin held a favorable 9.1% in 2025 despite recent contraction. EBIT margin fell sharply to zero in 2025.

Is the Income Statement Favorable?

The 2025 income statement shows mixed signals. Revenue and gross profit growth remain robust and outpace operating expenses, supporting positive cash flow fundamentals. However, EBIT dropped 100% year-over-year, driving net income and EPS lower by 40% and 55%, respectively. Interest expense is well contained at under 1% of revenue. Overall, the fundamentals lean favorable but highlight margin pressure.

Financial Ratios

The table below summarizes key financial ratios for Insulet Corporation (PODD) over the past five fiscal years, reflecting profitability, liquidity, leverage, and valuation metrics:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 1.5% | 0.4% | 12.2% | 20.2% | 9.1% |

| ROE | 3.0% | 1.0% | 28.2% | 34.5% | 16.3% |

| ROIC | 5.6% | 0.9% | 9.7% | 11.7% | 18.7% |

| P/E | 1,072 | 4,440 | 73.4 | 43.7 | 80.9 |

| P/B | 32.4 | 42.9 | 20.7 | 15.1 | 13.2 |

| Current Ratio | 5.8 | 3.6 | 3.5 | 3.5 | 2.8 |

| Quick Ratio | 4.4 | 2.6 | 2.6 | 2.7 | 2.1 |

| D/E | 2.31 | 3.01 | 1.98 | 1.17 | 0.01 |

| Debt-to-Assets | 63% | 64% | 56% | 46% | 1% |

| Interest Coverage | 2.0 | 1.0 | 6.1 | 7.2 | -19.2 |

| Asset Turnover | 0.54 | 0.58 | 0.66 | 0.67 | 0.85 |

| Fixed Asset Turnover | 2.0 | 2.1 | 2.4 | 2.7 | 3.3 |

| Dividend Yield | 0% | 0% | 0% | 0% | 0% |

All percentages are rounded to one decimal place where appropriate. Negative interest coverage in 2025 signals potential risk in meeting interest obligations. The P/E ratio shows extreme volatility, reflecting earnings fluctuations.

Evolution of Financial Ratios

From 2021 to 2025, Insulet Corporation’s Return on Equity (ROE) improved significantly, reaching 16.31% in 2025, indicating enhanced profitability. The Current Ratio declined from 5.75 in 2021 to 2.81 in 2025, yet it remains strong, reflecting solid liquidity. The Debt-to-Equity Ratio dropped sharply to 0.01, signaling much lower leverage and financial risk.

Are the Financial Ratios Favorable?

In 2025, profitability metrics like ROE (16.31%) and ROIC (18.74%) are favorable, surpassing the company’s weighted average cost of capital (WACC) at 10.31%. Liquidity ratios, including a Current Ratio of 2.81 and Quick Ratio of 2.15, are solid. However, high valuation multiples such as a P/E of 80.92 and P/B of 13.2 are unfavorable. Leverage remains minimal with a Debt-to-Equity of 0.01, but negative Interest Coverage raises caution. Overall, the ratios appear slightly favorable.

Shareholder Return Policy

Insulet Corporation (PODD) does not pay dividends, reflecting a focus on reinvestment and growth. The company generates positive net income and free cash flow but prioritizes capital allocation towards operations and expansion rather than distributions.

Though PODD does not engage in share buybacks, its dividend payout ratio remains at zero. This approach aligns with supporting sustainable long-term shareholder value through reinvestment rather than immediate cash returns, consistent with growth-phase companies in the medical device sector.

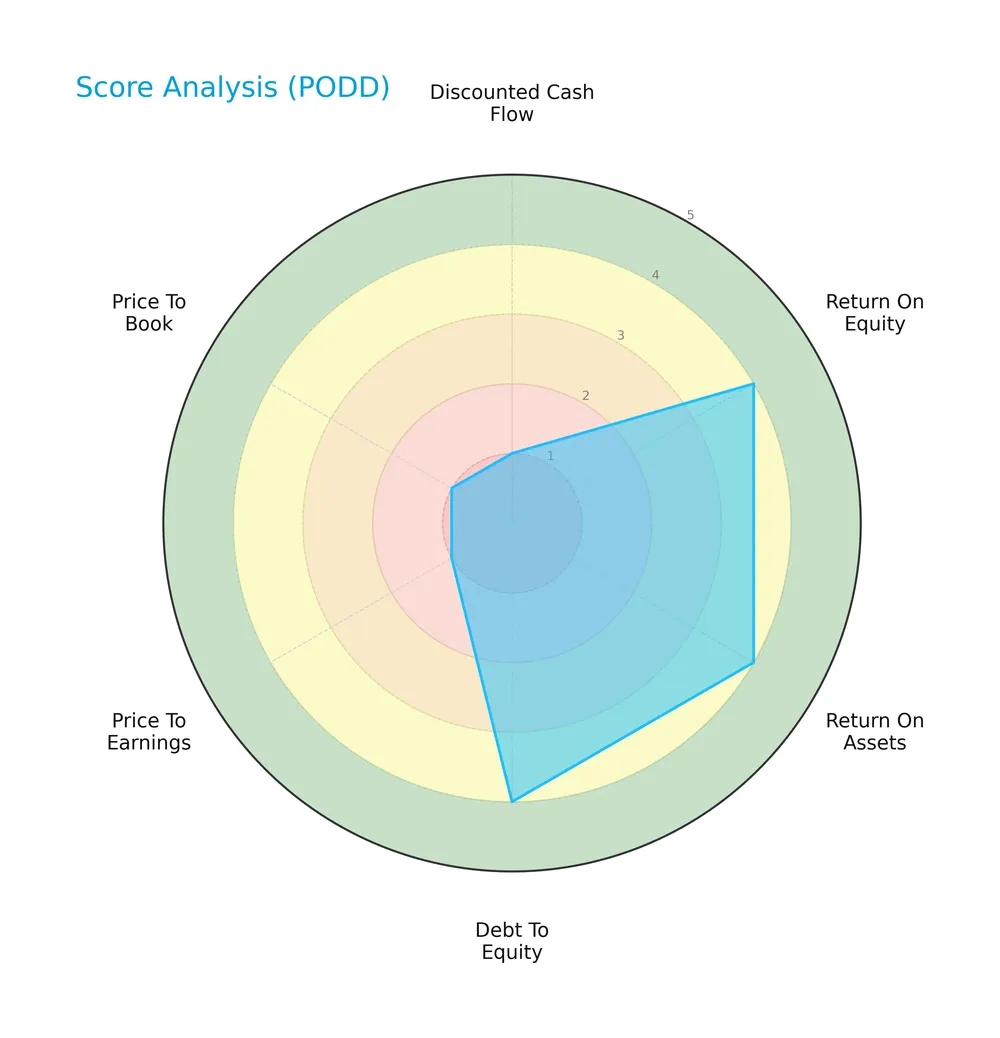

Score analysis

The radar chart below illustrates the company’s key valuation and financial performance scores:

Insulet Corporation scores favorably on return on equity, assets, and debt-to-equity, indicating operational strength and conservative leverage. However, its discounted cash flow, price-to-earnings, and price-to-book scores are very unfavorable, reflecting valuation concerns.

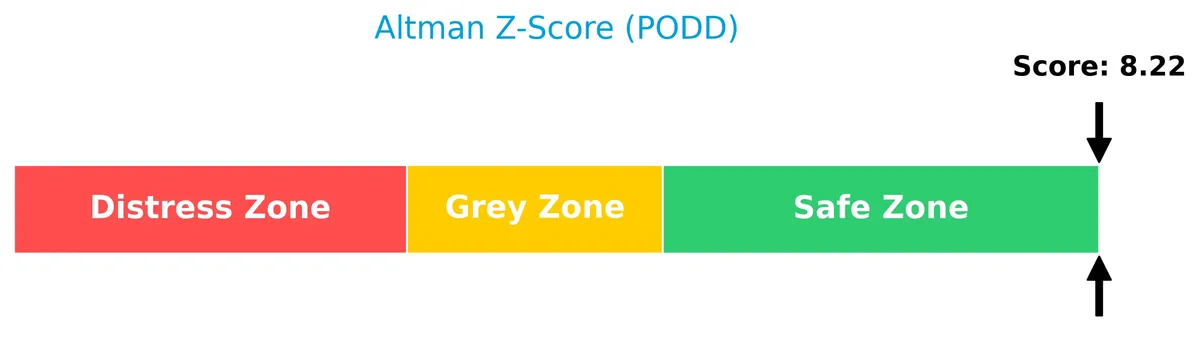

Analysis of the company’s bankruptcy risk

The Altman Z-Score places the company well within the safe zone, signaling low bankruptcy risk and strong financial stability:

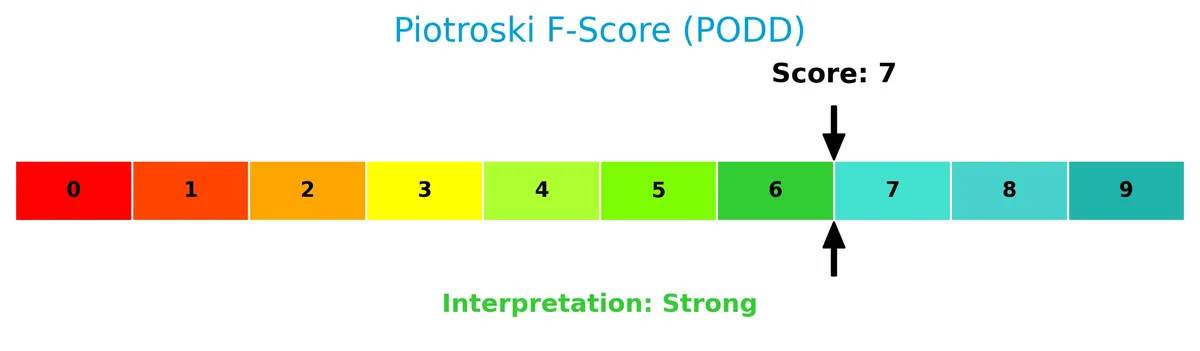

Is the company in good financial health?

The Piotroski Score diagram reveals the company’s financial condition based on profitability, leverage, and efficiency metrics:

With a strong Piotroski Score of 7, Insulet demonstrates solid financial health, balancing profitability and risk effectively.

Competitive Landscape & Sector Positioning

This section analyzes Insulet Corporation’s strategic positioning within the medical devices sector. We will examine revenue by segment, key products, and main competitors. I will assess whether Insulet holds a competitive advantage over its peers.

Strategic Positioning

Insulet concentrates on insulin delivery, with the Omnipod system dominating revenue. Its geographic exposure balances the U.S. market, contributing $1.95B in 2025, with significant international growth at $754M. This focused product and expanding global reach define its strategy.

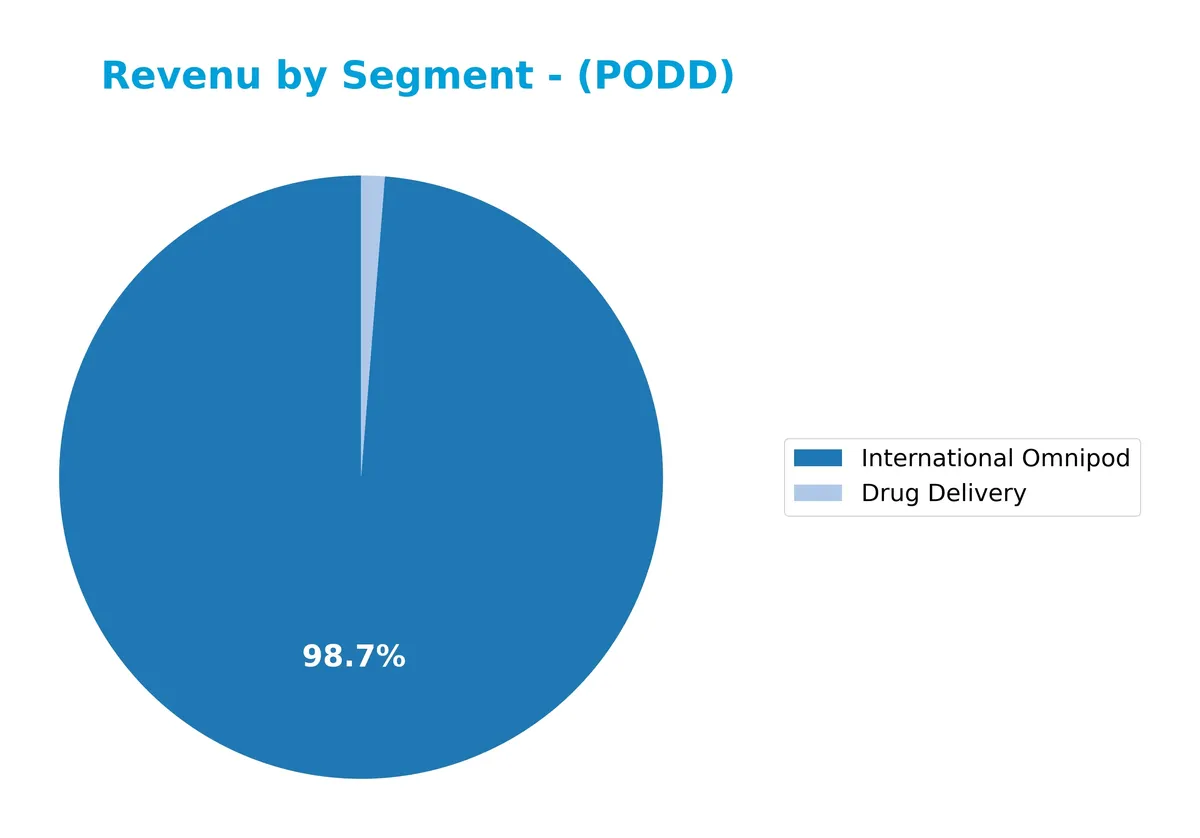

Revenue by Segment

The pie chart illustrates Insulet Corporation’s revenue breakdown by segment for fiscal year 2025, highlighting the contribution of “Drug Delivery” and “International Omnipod.”

International Omnipod dominates with $2.67B in revenue, showing robust growth from $1.01B in 2021. Drug Delivery lags significantly at $34.1M, declining from prior years. The trend reveals a strategic concentration on International Omnipod, which drives overall growth. However, Drug Delivery’s shrinking share signals a potential risk if reliance on the primary segment intensifies without diversification.

Key Products & Brands

The following table details Insulet Corporation’s primary products and brands with brief descriptions:

| Product | Description |

|---|---|

| Omnipod System | A self-adhesive, disposable, tubeless insulin delivery device worn up to three days. |

| Personal Diabetes Manager | Wireless handheld device that operates alongside the Omnipod System for insulin delivery. |

| Drug Delivery | Segment including insulin delivery-related products, generating $34M in revenue in 2025. |

| International Omnipod | Omnipod System sales outside the U.S., contributing $2.67B in revenue in 2025. |

Insulet’s product portfolio centers on the Omnipod System and its wireless controller, dominating its revenue with strong international growth. The Drug Delivery segment provides additional revenue but remains significantly smaller.

Main Competitors

There are 10 competitors in total; below is a table of the top 10 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| Abbott Laboratories | 216B |

| Boston Scientific Corporation | 140B |

| Stryker Corporation | 133B |

| Medtronic plc | 123B |

| Edwards Lifesciences Corporation | 50B |

| DexCom, Inc. | 26B |

| STERIS plc | 25B |

| Insulet Corporation | 19.9B |

| Zimmer Biomet Holdings, Inc. | 17.8B |

| Align Technology, Inc. | 11.2B |

Insulet Corporation ranks 8th among its peers with a market cap at just 8.4% of the leader, Abbott Laboratories. It sits below both the average top 10 market cap of 76.3B and the sector median of 38.1B. The company maintains a solid gap of +35.49% from its closest competitor above, signaling a clear but modest market position.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does Insulet have a competitive advantage?

Insulet demonstrates a sustainable competitive advantage, creating value with ROIC exceeding WACC by 8.4%, supported by a strong, growing profitability trend. Its 71.6% gross margin signals efficient cost management in a competitive medical devices sector.

Looking ahead, Insulet expands globally, with substantial revenue growth outside the US reaching $754M in 2025. Continued innovation in insulin delivery and geographic diversification present opportunities to reinforce its market position.

SWOT Analysis

This SWOT analysis highlights Insulet Corporation’s core strengths, weaknesses, opportunities, and threats to guide strategic investment decisions.

Strengths

- strong revenue growth

- high gross margin of 71.6%

- ROIC exceeds WACC by wide margin

Weaknesses

- high P/E ratio at 80.9

- negative EBIT growth last year

- elevated price-to-book ratio at 13.2

Opportunities

- expanding international sales

- growing diabetic population

- innovations in insulin delivery tech

Threats

- intense competition in medical devices

- regulatory risks

- pricing pressure from payers

Insulet’s strong profitability and value-creating ROIC underpin a durable competitive advantage. However, valuation remains stretched. The company should leverage growth opportunities abroad while carefully managing margin pressures and regulatory challenges.

Stock Price Action Analysis

The following weekly chart illustrates Insulet Corporation’s stock price movement over the past 12 months, highlighting key highs and lows:

Trend Analysis

Over the past 12 months, PODD’s price rose 50.57%, indicating a bullish trend with decelerating momentum. The stock fluctuated between a low of 165.0 and a high of 348.43, showing significant volatility with a 50.24 standard deviation. Recent months reversed, dropping 15.25% from December 2025 to February 2026.

Volume Analysis

Trading volume totaled 443.7M shares, with slightly more sellers (51.4%) than buyers overall, and volume is decreasing. Over the last three months, seller dominance strengthened, with buyers at 24.9%, indicating waning investor enthusiasm and lower market participation.

Target Prices

Analysts present a bullish consensus on Insulet Corporation’s stock, reflecting confidence in its growth prospects.

| Target Low | Target High | Consensus |

|---|---|---|

| 274 | 435 | 374.91 |

The target range implies upside potential from current levels, signaling strong market expectations for PODD’s performance.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section examines the latest analyst ratings and consumer feedback on Insulet Corporation’s market performance and product reception.

Stock Grades

Here are the latest verified grades from recognized financial analysts for Insulet Corporation (PODD):

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| BTIG | Maintain | Buy | 2026-02-18 |

| Stifel | Maintain | Buy | 2026-02-04 |

| Barclays | Downgrade | Underweight | 2026-01-12 |

| Bernstein | Maintain | Outperform | 2026-01-09 |

| Truist Securities | Maintain | Buy | 2025-12-18 |

| Canaccord Genuity | Maintain | Buy | 2025-12-17 |

| Canaccord Genuity | Maintain | Buy | 2025-11-24 |

| RBC Capital | Maintain | Outperform | 2025-11-21 |

| BTIG | Maintain | Buy | 2025-11-21 |

| Truist Securities | Maintain | Buy | 2025-11-21 |

The majority of analysts maintain a “Buy” rating, reflecting consistent confidence. Barclays’ recent downgrade to “Underweight” stands out as a notable divergence. Overall consensus remains positive with a “Buy” rating.

Consumer Opinions

Insulet Corporation (PODD) consistently earns praise for its innovative insulin delivery systems, though some users express concerns about device reliability.

| Positive Reviews | Negative Reviews |

|---|---|

| “The OmniPod system is life-changing and discreet.” | “Pods sometimes fail to adhere properly.” |

| “Customer service is responsive and helpful.” | “Battery life could be improved.” |

| “Easy to use and reduces the hassle of multiple injections.” | “Occasional glitches in the app connectivity.” |

Overall, consumers applaud Insulet’s user-friendly design and customer support. However, device adhesion and technical issues remain common pain points.

Risk Analysis

The following table presents key risks for Insulet Corporation, highlighting their likelihood and potential impact:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Valuation Risk | High P/E of 80.9 and P/B of 13.2 suggest overvaluation risk in a volatile market. | High | High |

| Interest Coverage | Negative interest coverage signals vulnerability to rising debt costs. | Moderate | Moderate |

| Competitive Pressure | Innovating in a crowded medical devices sector could pressure margins. | Moderate | Moderate |

| Regulatory Risk | Healthcare regulations may tighten, impacting product approvals and sales. | Low | High |

| Market Volatility | Beta of 1.41 indicates above-market volatility, increasing share price swings. | High | Moderate |

I emphasize valuation risk as most pressing. Despite strong ROIC (18.7%) comfortably above WACC (10.3%), the steep P/E and P/B ratios raise red flags. Investors must watch for market corrections that could punish stretched multiples. Interest coverage remains a concern, reflecting tight earnings relative to debt costs. However, Insulet’s Altman Z-Score (8.2) confirms financial stability, reducing bankruptcy fears. Overall, prudent risk management demands caution on valuation and debt servicing as key vulnerabilities.

Should You Buy Insulet Corporation?

Insulet appears to be generating strong value creation with a very favorable moat supported by growing ROIC. The company maintains a manageable leverage profile and solid profitability. Despite some valuation concerns, its overall B- rating suggests a cautiously optimistic financial profile.

Strength & Efficiency Pillars

Insulet Corporation exhibits solid operational efficiency with a net margin of 9.12% and a return on equity (ROE) of 16.31%. Its return on invested capital (ROIC) stands at 18.74%, comfortably above the weighted average cost of capital (WACC) at 10.31%, marking it as a clear value creator. The firm’s gross margin remains robust at 71.63%, supporting sustainable profitability. With a strong Piotroski Score of 7 and a safe-zone Altman Z-Score of 8.22, the company demonstrates resilience and operational strength in a competitive healthcare sector.

Weaknesses and Drawbacks

Despite operational strengths, Insulet faces valuation headwinds with a high price-to-earnings ratio of 80.92 and a price-to-book ratio of 13.2, indicating a premium market valuation that may limit upside. The interest coverage ratio remains unfavorable at -0.0, signaling potential challenges in covering debt costs despite low debt-to-equity at 0.01. Recent market activity shows a seller-dominant trend with buyers accounting for only 24.9%, which could weigh on near-term price momentum amid decelerating bullish trends and decreasing volume.

Our Final Verdict about Insulet Corporation

Insulet Corporation presents a fundamentally sound profile with strong value creation and profitability metrics. However, despite its bullish long-term trajectory, recent market pressure and elevated valuation multiples suggest investors might adopt a wait-and-see stance. The combination of strong operational fundamentals and cautious technical signals indicates the stock may appear attractive for patient, risk-tolerant investors seeking long-term exposure.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Insulet Corporation (PODD) Announces Strategic Expansion and Supply Agreement Update – Yahoo Finance (Feb 15, 2026)

- Decoding Insulet Corp (PODD): A Strategic SWOT Insight – GuruFocus (Feb 19, 2026)

- Insulet (PODD) Shares Skyrocket, What You Need To Know – Finviz (Feb 18, 2026)

- Insulet stock gains on Q4 2025 print, outlook (PODD:NASDAQ) – Seeking Alpha (Feb 18, 2026)

- Insulet Reports Fourth Quarter and Full Year 2025 Results – BioSpace (Feb 18, 2026)

For more information about Insulet Corporation, please visit the official website: insulet.com