Home > Analyses > Industrials > Ferguson plc

Ferguson plc plays a crucial role in shaping the infrastructure of daily life by distributing essential plumbing and heating products across North America. As a dominant force in the industrial distribution sector, it serves residential, commercial, and civil markets with a broad portfolio ranging from water heaters to HVAC systems. Renowned for its extensive branch network and innovative supply chain solutions, Ferguson continually adapts to evolving market demands. The key question now: does its strong market position and operational excellence still translate into compelling investment potential in 2026?

Table of contents

Business Model & Company Overview

Ferguson plc, founded in 1887 and headquartered in Wokingham, UK, stands as a dominant distributor of plumbing and heating products across the US and Canada. Its extensive ecosystem serves residential, commercial, civil infrastructure, and industrial markets, integrating pipes, valves, HVAC products, and advanced metering solutions. With 1,679 branches and 11 distribution centers, Ferguson creates a seamless supply chain that supports a broad spectrum of customer needs in essential infrastructure and building services.

The company’s revenue engine balances product sales with value-added services like project management, digital design, and logistics, enhancing customer retention and operational efficiency. Ferguson’s strategic footprint spans the Americas, leveraging online and physical channels to sustain growth. Its competitive advantage lies in this comprehensive distribution network combined with expertise-driven services, securing a durable economic moat in the industrial distribution sector.

Financial Performance & Fundamental Metrics

In this section, I analyze Ferguson plc’s income statement, key financial ratios, and dividend payout policy to assess its financial health and shareholder value.

Income Statement

The following table presents Ferguson plc’s key income statement figures for the fiscal years 2021 through 2025, reported in USD.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 22.8B | 28.6B | 29.7B | 29.6B | 30.8B |

| Cost of Revenue | 15.8B | 19.8B | 20.7B | 20.6B | 21.3B |

| Operating Expenses | 5.03B | 5.94B | 6.37B | 6.40B | 6.83B |

| Gross Profit | 7.0B | 8.8B | 9.0B | 9.1B | 9.4B |

| EBITDA | 2.26B | 3.12B | 2.97B | 2.98B | 3.06B |

| EBIT | 1.96B | 2.82B | 2.65B | 2.64B | 2.69B |

| Interest Expense | 98M | 111M | 184M | 179M | 190M |

| Net Income | 1.47B | 2.12B | 1.89B | 1.74B | 1.86B |

| EPS | 6.59 | 9.75 | 9.15 | 8.55 | 9.33 |

| Filing Date | 2021-09-28 | 2022-09-27 | 2023-09-26 | 2024-09-25 | 2025-09-26 |

Income Statement Evolution

Between 2021 and 2025, Ferguson plc’s revenue increased by 34.97%, reflecting steady growth, while net income grew by 26.09%. However, net margin declined by 6.58% over the period, signaling some margin pressure. Gross margin remained favorable at 30.67%, while EBIT margin was stable at 8.73%, indicating consistent operating profitability despite rising operating expenses.

Is the Income Statement Favorable?

In 2025, Ferguson posted a 3.8% revenue increase and a 3.05% net margin improvement, both neutral in assessment, while EPS growth of 9.26% was favorable. Interest expense remained low at 0.62% of revenue, aiding net profitability. Overall, half of the income statement metrics were favorable, with a global opinion rating the fundamentals as favorable, supported by solid gross margins and positive earnings per share trends.

Financial Ratios

The following table presents key financial ratios for Ferguson plc over the fiscal years 2021 to 2025, facilitating year-on-year performance comparison:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 6.5% | 7.4% | 6.4% | 5.9% | 6.0% |

| ROE | 29.4% | 45.5% | 37.5% | 30.9% | 31.8% |

| ROIC | 18.5% | 21.0% | 18.6% | 15.7% | 15.9% |

| P/E | 21.3 | 12.8 | 17.7 | 26.0 | 23.9 |

| P/B | 6.3 | 5.8 | 6.6 | 8.0 | 7.6 |

| Current Ratio | 1.72 | 1.65 | 1.67 | 1.80 | 1.68 |

| Quick Ratio | 1.02 | 0.90 | 0.95 | 1.00 | 0.94 |

| D/E | 0.72 | 1.10 | 1.04 | 0.98 | 1.02 |

| Debt-to-Assets | 26.3% | 32.7% | 32.9% | 33.3% | 33.7% |

| Interest Coverage | 19.9 | 25.4 | 14.5 | 14.8 | 13.7 |

| Asset Turnover | 1.66 | 1.82 | 1.86 | 1.79 | 1.74 |

| Fixed Asset Turnover | 9.5 | 11.1 | 9.7 | 8.9 | 8.5 |

| Dividend Yield | 3.3% | 2.0% | 2.1% | 1.7% | 1.1% |

Evolution of Financial Ratios

Over the 2021–2025 period, Ferguson plc’s Return on Equity (ROE) generally improved, reaching 31.8% in 2025, indicating enhanced profitability. The Current Ratio remained relatively stable around 1.68 to 1.80, reflecting consistent liquidity. The Debt-to-Equity Ratio increased from 0.72 in 2021 to about 1.02 in 2025, showing a higher leverage level but with manageable risk given coverage ratios.

Are the Financial Ratios Favorable?

In 2025, Ferguson’s profitability ratios, including ROE at 31.8% and Return on Invested Capital (ROIC) at 15.9%, are favorable, while the Net Profit Margin at 6.03% is neutral. Liquidity is sound with a Current Ratio of 1.68 (favorable) and Quick Ratio near 0.94 (neutral). Leverage metrics show a Debt-to-Equity Ratio of 1.02 (unfavorable), but strong interest coverage of 14.14 supports debt service capacity. Market valuation ratios like Price-to-Book at 7.62 appear unfavorable, balancing the overall slightly favorable financial ratio profile.

Shareholder Return Policy

Ferguson plc maintains a consistent dividend payout ratio around 26-45%, with dividend per share increasing moderately over recent years. The annual dividend yield ranges between 1.1% and 3.3%, supported by robust free cash flow coverage and manageable payout relative to net income.

The company does not report share buyback programs, focusing on dividend distributions funded by solid operating cash flow and free cash flow. This approach supports a balanced shareholder return policy that appears sustainable, aligning with steady profitability and cash generation.

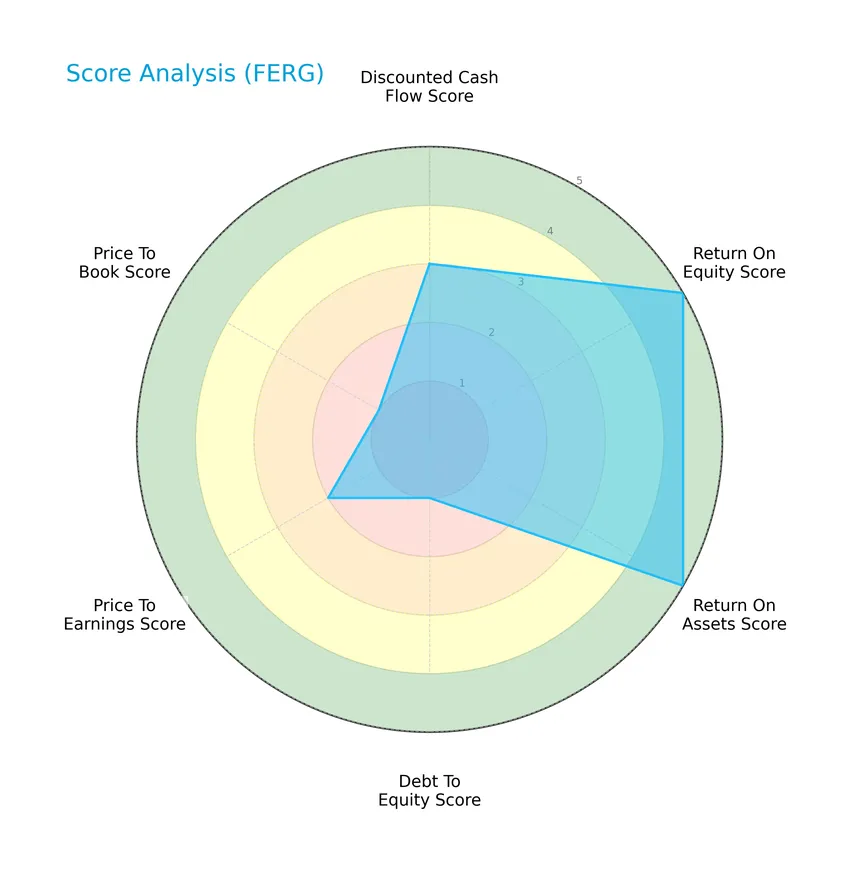

Score analysis

The following radar chart presents a comprehensive view of Ferguson plc’s key financial scores:

Ferguson plc shows very favorable returns on equity and assets with scores of 5 each, indicating strong profitability. However, the debt-to-equity and price-to-book ratios are very unfavorable at 1, reflecting higher leverage and valuation concerns. Other scores like discounted cash flow and price-to-earnings are moderate, suggesting a balanced overall financial profile.

Analysis of the company’s bankruptcy risk

Ferguson plc’s Altman Z-Score places it firmly in the safe zone, indicating a low risk of bankruptcy based on its financial ratios:

Is the company in good financial health?

The Piotroski Score diagram highlights Ferguson plc’s solid financial strength based on nine key accounting criteria:

With a Piotroski Score of 7 categorized as strong, the company demonstrates good financial health, reflecting profitability, efficient asset use, and manageable leverage.

Competitive Landscape & Sector Positioning

This sector analysis will examine Ferguson plc’s strategic positioning, revenue segmentation, key products, main competitors, and competitive advantages. I will assess whether Ferguson plc holds a competitive advantage within the industrial distribution sector.

Strategic Positioning

Ferguson plc concentrates its product portfolio on plumbing, heating, HVAC, and related industrial supplies, serving residential to infrastructure markets. Geographically, it focuses on North America, with 29.3B USD revenue from the US and 1.5B USD from Canada, supported by 1,679 branches and 11 distribution centers.

Revenue by Segment

This pie chart illustrates Ferguson plc’s revenue distribution by segment for the fiscal year 2025, highlighting the company’s segment performance and contribution to overall income.

In 2025, Ferguson plc’s revenue is concentrated solely in the United States Segment, which generated 29.3B. This indicates a high dependency on the U.S. market, with no reported revenues from other segments. The data suggests a concentrated business model with potential risks related to geographic concentration, emphasizing the importance of monitoring diversification efforts in future periods.

Key Products & Brands

The following table outlines Ferguson plc’s main products and brands offered in its distribution network:

| Product | Description |

|---|---|

| Plumbing and Heating Products | Includes pipes, valves, fittings, plumbing supplies, water heaters, kitchen and bathroom fixtures, and appliances. |

| HVAC and Refrigeration Products | Heating, ventilation, air conditioning, and refrigeration products and supplies. |

| Fire Sprinkler Systems and Fasteners | Fire sprinkler systems, hangers, struts, and fasteners for various installations. |

| Water and Wastewater Treatment Products | Products related to water meters, automation, irrigation, drainage, stormwater management, and wastewater treatment. |

| Industrial Maintenance and Fabrication Products | Flanges, general industrial maintenance repair and operations products, high density polyethylene products, and fabrication items. |

| Services | Consultation, project management, pro pick-up and delivery, online tools, quotation, logistics, digital estimation, and supply chain services. |

Ferguson plc distributes a wide range of plumbing, heating, HVAC, water treatment, and industrial maintenance products, supported by comprehensive services and a vast branch network across the US and Canada.

Main Competitors

There are 3 competitors in total, with the table below listing the top 3 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| W.W. Grainger, Inc. | 47.7B |

| Fastenal Company | 46.4B |

| Pool Corporation | 8.6B |

Ferguson plc is not ranked among the top 3 competitors by market capitalization in this sector. The company’s relative market cap to the leader is 0, indicating it is not among the largest players. It is positioned above both the average market cap of the top 10 and the median market cap in the sector. Since Ferguson is not ranked, no distance to the next competitor above can be calculated.

Comparisons with competitors

Check out how we compare the company to its competitors:

Aucun article trouvé pour ces critères.

Does FERG have a competitive advantage?

Ferguson plc demonstrates a competitive advantage, as evidenced by its ROIC exceeding WACC by 7.38%, indicating value creation. However, the declining ROIC trend suggests weakening profitability, leading to a slightly favorable moat status. The company benefits from a broad distribution network with 1,679 branches and diverse product offerings across plumbing, HVAC, and industrial supplies in the US and Canada.

Looking ahead, Ferguson’s opportunities lie in expanding its digital services, online sales channels, and advanced project management solutions. The company’s focus on enhancing supply chain logistics, fabrications, and metering infrastructure services may support growth in residential, commercial, and infrastructure markets. Continued innovation and market penetration will be critical to sustaining its competitive position.

SWOT Analysis

This SWOT analysis highlights Ferguson plc’s key internal and external factors to guide investment decisions.

Strengths

- Strong market position in US and Canada

- Wide product and service portfolio

- Favorable profitability and ROE above 30%

Weaknesses

- High debt-to-equity ratio

- Declining ROIC trend

- Elevated price-to-book ratio indicating potential overvaluation

Opportunities

- Growth in infrastructure and residential markets

- Expansion of digital and logistics services

- Increasing demand for sustainable plumbing solutions

Threats

- Competitive pressure from other distributors

- Economic slowdown affecting construction sector

- Supply chain disruptions and rising costs

Overall, Ferguson plc demonstrates robust profitability and market presence but faces challenges from leverage and valuation. Strategic focus on operational efficiency and market expansion could mitigate risks and enhance shareholder value.

Stock Price Action Analysis

The weekly stock chart for Ferguson plc (ticker: FERG) over the past 100 weeks illustrates key price movements and trend shifts:

Trend Analysis

Over the past 12 months, Ferguson plc’s stock price increased by 18.46%, indicating a bullish trend with deceleration in momentum. The price ranged from a low of 155.56 to a high of 254.02, with a high volatility level reflected by a 24.26 standard deviation. Recent weeks show a neutral trend with a 1.75% gain and a slight downward slope.

Volume Analysis

In the last three months, trading volumes have been increasing with a total volume near 85M shares. Buyer volume slightly exceeds seller volume at 50.23%, indicating neutral buyer behavior. This balanced activity suggests cautious investor sentiment and stable market participation during the recent period.

Target Prices

The consensus target prices for Ferguson plc indicate a generally positive outlook among analysts.

| Target High | Target Low | Consensus |

|---|---|---|

| 291.99 | 220 | 266.67 |

Analysts expect Ferguson plc’s stock price to range between 220 and 292, with a consensus target around 267, reflecting moderate growth potential.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section examines the latest analyst ratings and consumer feedback related to Ferguson plc (FERG) performance and reputation.

Stock Grades

Here is a concise overview of the latest stock grades assigned to Ferguson plc by leading financial institutions:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Barclays | Maintain | Overweight | 2026-01-15 |

| Deutsche Bank | Maintain | Hold | 2025-12-11 |

| UBS | Maintain | Neutral | 2025-12-10 |

| Baird | Maintain | Outperform | 2025-12-10 |

| Barclays | Maintain | Overweight | 2025-12-10 |

| Wells Fargo | Maintain | Overweight | 2025-12-04 |

| Jefferies | Maintain | Buy | 2025-12-02 |

| JP Morgan | Maintain | Overweight | 2025-10-15 |

| Barclays | Maintain | Overweight | 2025-09-18 |

| UBS | Maintain | Neutral | 2025-09-17 |

The grades for Ferguson plc predominantly reflect a positive outlook, with multiple Overweight and Buy ratings maintained across late 2025 and early 2026. Neutral and Hold grades appear less frequently, indicating some cautious sentiment among certain analysts.

Consumer Opinions

Consumer sentiment around Ferguson plc (FERG) reflects a mix of appreciation for product quality and concerns about customer service responsiveness.

| Positive Reviews | Negative Reviews |

|---|---|

| “Ferguson offers a wide range of reliable plumbing supplies with excellent durability.” | “Customer support can be slow to respond, causing delays in project timelines.” |

| “The product availability and delivery times have improved significantly over the past year.” | “Pricing can be higher compared to some competitors, impacting budget-conscious buyers.” |

| “Their knowledgeable staff provides valuable technical advice, helping me make informed purchases.” | “Occasional issues with order accuracy, leading to the need for returns or exchanges.” |

Overall, consumers praise Ferguson plc for product quality and knowledgeable staff, but recurring issues with customer service speed and pricing remain areas for improvement.

Risk Analysis

Below is a summary table of key risks associated with Ferguson plc, highlighting their probability and potential impact on the company and investors:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Market Risk | Exposure to economic cycles affecting construction and infrastructure demand in US and Canada | Medium | High |

| Leverage Risk | Relatively high debt-to-equity ratio (1.02), increasing financial risk in downturns | Medium | Medium |

| Valuation Risk | Elevated price-to-book ratio (7.62) suggests potential overvaluation | Medium | Medium |

| Operational Risk | Supply chain disruptions impacting distribution efficiency across 1,679 branches | Medium | Medium |

| Competitive Risk | Intense competition in industrial distribution could pressure margins | Medium | Medium |

| Regulatory Risk | Changes in trade policies or regulations in North America may affect operations | Low | Medium |

The most significant risks are market sensitivity and financial leverage. Despite a strong Altman Z-Score (5.6, safe zone) and solid profitability metrics, Ferguson’s debt levels and valuation multiples warrant caution. Ongoing vigilance on economic cycles and debt management is essential for risk mitigation.

Should You Buy Ferguson plc?

Ferguson plc appears to be a profitable company with robust operational efficiency, supported by a slightly favorable moat despite a declining ROIC trend. The leverage profile could be seen as substantial, while the overall B rating suggests a very favorable financial health profile.

Strength & Efficiency Pillars

Ferguson plc exhibits solid profitability and value creation metrics, with a return on equity (ROE) of 31.82% and a return on invested capital (ROIC) of 15.91%, notably exceeding its weighted average cost of capital (WACC) at 8.53%, confirming the company as a clear value creator. The firm’s Altman Z-Score stands robustly at 5.61, situating it in the safe zone, while a Piotroski Score of 7 underscores strong financial health. Favorable gross margin at 30.67% and a current ratio of 1.68 further demonstrate operational efficiency and liquidity strength.

Weaknesses and Drawbacks

The company faces valuation concerns, with a price-to-book ratio of 7.62 flagged as very unfavorable, suggesting the stock may be trading at a significant premium relative to its book value. Debt levels also pose risks, evidenced by a debt-to-equity ratio of 1.02, rated unfavorable, indicating relatively high leverage that could amplify financial vulnerability in adverse conditions. Although the price-to-earnings ratio of 23.93 is moderate, it still reflects elevated valuation. Recent market behavior shows a near balance between buyers (50.23%) and sellers, signaling neutral investor sentiment and potential short-term volatility.

Our Verdict about Ferguson plc

Ferguson plc’s long-term fundamental profile appears favorable, supported by strong profitability and financial health metrics alongside value creation. However, despite a generally bullish overall trend, the recent neutral buyer dominance and deceleration in price momentum may suggest a cautious stance. Investors might consider a wait-and-see approach for a more attractive entry point, as valuation and leverage risks could temper near-term upside potential.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Quilter Plc Cuts Stake in Ferguson plc $FERG – MarketBeat (Jan 25, 2026)

- Ferguson PLC (FERG) Receives a Buy from Wells Fargo – The Globe and Mail (Jan 21, 2026)

- iA Global Asset Management Inc. Acquires Shares of 5,574 Ferguson plc $FERG – MarketBeat (Jan 25, 2026)

- Brasada Capital Management’s Views on Ferguson Plc (FERG) – Yahoo Finance (Dec 12, 2025)

- Rakuten Investment Management Inc. Buys New Holdings in Ferguson plc $FERG – MarketBeat (Jan 25, 2026)

For more information about Ferguson plc, please visit the official website: fergusonplc.com