Home > Analyses > Utilities > Essential Utilities, Inc.

Essential Utilities, Inc. delivers vital water and natural gas services that touch millions of lives daily. As a dominant player in the regulated water sector, it operates under trusted brands like Aqua and Peoples, known for reliability and innovation. Its expansive footprint across key U.S. states secures steady demand and regulatory support. Yet, as market dynamics evolve, I question whether its fundamentals continue to justify its valuation and growth outlook in 2026.

Table of contents

Business Model & Company Overview

Essential Utilities, Inc., founded in 1886 and headquartered in Bryn Mawr, Pennsylvania, stands as a leading force in the regulated water industry. Serving 7.5M customers across multiple states, it delivers an integrated ecosystem of water, wastewater, and natural gas services. Its operations span residential, commercial, industrial, and fire protection sectors under the Aqua and Peoples brands, reflecting a cohesive mission to provide essential utility infrastructure reliably and sustainably.

The company’s revenue engine balances regulated water and natural gas services with value-added offerings like water line protection and raw water supply for energy firms. This diversified model captures stable, recurring cash flows within the highly regulated U.S. markets—primarily Pennsylvania, Ohio, Texas, and surrounding states. Essential Utilities’ extensive network and deep municipal partnerships create a formidable economic moat, positioning it to shape the future of water and utility infrastructure.

Financial Performance & Fundamental Metrics

I will analyze Essential Utilities, Inc.’s income statement, key financial ratios, and dividend payout policy to assess its financial health and shareholder value.

Income Statement

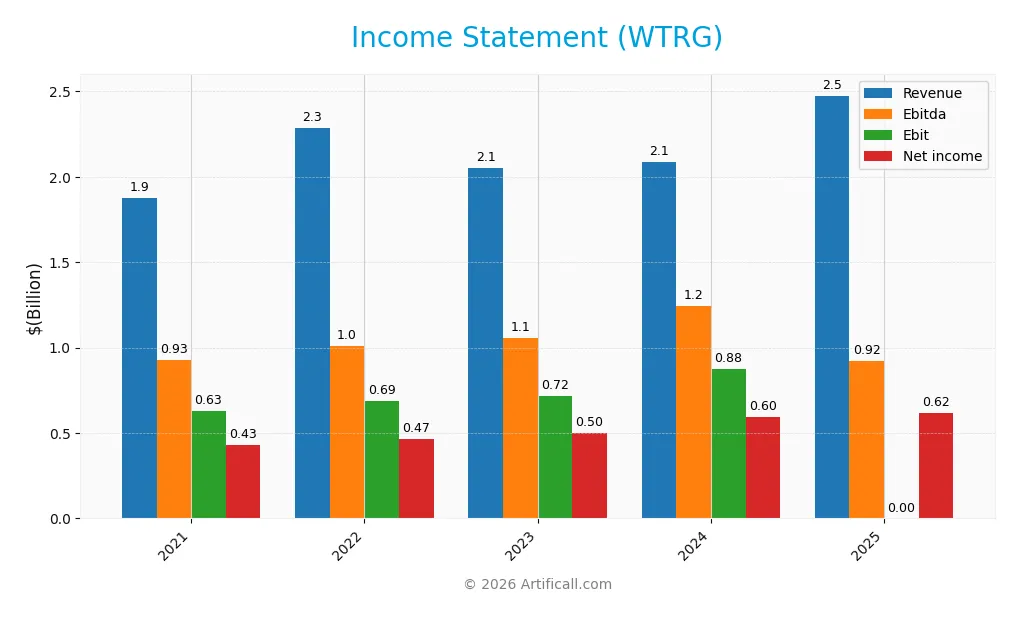

The table below summarizes Essential Utilities, Inc.’s annual income statement figures from 2021 to 2025, highlighting revenue, profit metrics, expenses, and earnings per share.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 1.88B | 2.29B | 2.05B | 2.09B | 2.47B |

| Cost of Revenue | 891M | 1.22B | 928M | 864M | 0 |

| Operating Expenses | 385M | 411M | 434M | 464M | 0 |

| Gross Profit | 987M | 1.07B | 1.13B | 1.22B | 0 |

| EBITDA | 928M | 1.01B | 1.06B | 1.25B | 921M |

| EBIT | 630M | 689M | 715M | 876M | 0 |

| Interest Expense | 208M | 238M | 283M | 302M | 329M |

| Net Income | 432M | 465M | 498M | 595M | 616M |

| EPS | 1.68 | 1.77 | 1.86 | 2.17 | 2.20 |

| Filing Date | 2022-03-01 | 2023-03-01 | 2024-02-29 | 2025-02-27 | 2026-02-26 |

Income Statement Evolution

From 2021 to 2025, Essential Utilities, Inc. grew revenue by 32%, reaching $2.47B in 2025. Net income rose 43%, improving margins overall. However, gross profit and EBIT margins turned unfavorable in 2025 due to missing cost data. The net margin remains strong at 24.9%, despite a slight decline in margin growth last year.

Is the Income Statement Favorable?

The 2025 income statement shows solid fundamentals with $617M net income and a 24.9% net margin, reflecting efficient capital allocation. EBITDA stands at $921M. Interest expense at 13.3% of revenue weighs on profitability. Missing cost and expense details cloud margin analysis, but overall, the income metrics align favorably with sector benchmarks.

Financial Ratios

The table below summarizes key financial ratios for Essential Utilities, Inc. over recent fiscal years:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 23% | 20% | 24% | 29% | 25% |

| ROE | 8.3% | 8.7% | 8.4% | 9.6% | 9.0% |

| ROIC | 4.3% | 4.4% | 4.3% | 4.4% | 7.6% |

| P/E | 32.0 | 27.0 | 20.0 | 16.7 | 17.4 |

| P/B | 2.67 | 2.33 | 1.69 | 1.60 | 1.57 |

| Current Ratio | 0.65 | 0.64 | 0.62 | 0.50 | 1.04 |

| Quick Ratio | 0.49 | 0.45 | 0.48 | 0.40 | 1.04 |

| D/E | 1.16 | 1.27 | 1.20 | 1.25 | 0.00 |

| Debt-to-Assets | 41% | 43% | 42% | 43% | 0% |

| Interest Coverage | 2.90 | 2.78 | 2.44 | 2.50 | 2.80 |

| Asset Turnover | 0.13 | 0.15 | 0.12 | 0.12 | 0.20 |

| Fixed Asset Turnover | 0.18 | 0.20 | 0.17 | 0.16 | 0.00 |

| Dividend Yield | 1.9% | 2.3% | 3.2% | 3.5% | 3.5% |

Evolution of Financial Ratios

From 2021 to 2025, Essential Utilities’ Return on Equity (ROE) fluctuated mildly but declined slightly to 8.99% in 2025, indicating stable yet modest profitability. The Current Ratio improved notably to 1.04 in 2025, reflecting enhanced liquidity. Debt-to-Equity dropped sharply to zero by 2025, showing significant deleveraging over the period.

Are the Financial Ratios Favorable?

In 2025, profitability ratios like net margin (24.91%) appeared favorable, while ROE (8.99%) was unfavorable relative to typical utilities benchmarks. Liquidity showed mixed signals: a neutral Current Ratio (1.04) but favorable Quick Ratio (1.04). Leverage ratios stood out positively with zero debt, yet asset turnover and interest coverage ratios were unfavorable. Overall, the financial ratios are slightly favorable, balancing strengths and weaknesses.

Shareholder Return Policy

Essential Utilities, Inc. maintains a dividend payout ratio near 60%, with a steady dividend per share rising to $1.33 in 2025 and a yield around 3.48%. The company funds dividends partly through free cash flow, despite negative free cash flow per share and significant capital expenditures.

The firm also engages in share buybacks, supporting shareholder returns alongside dividends. This distribution approach balances income and reinvestment, though free cash flow coverage below one signals caution. Overall, the policy aims for sustainable long-term value amid capital intensity and moderate leverage.

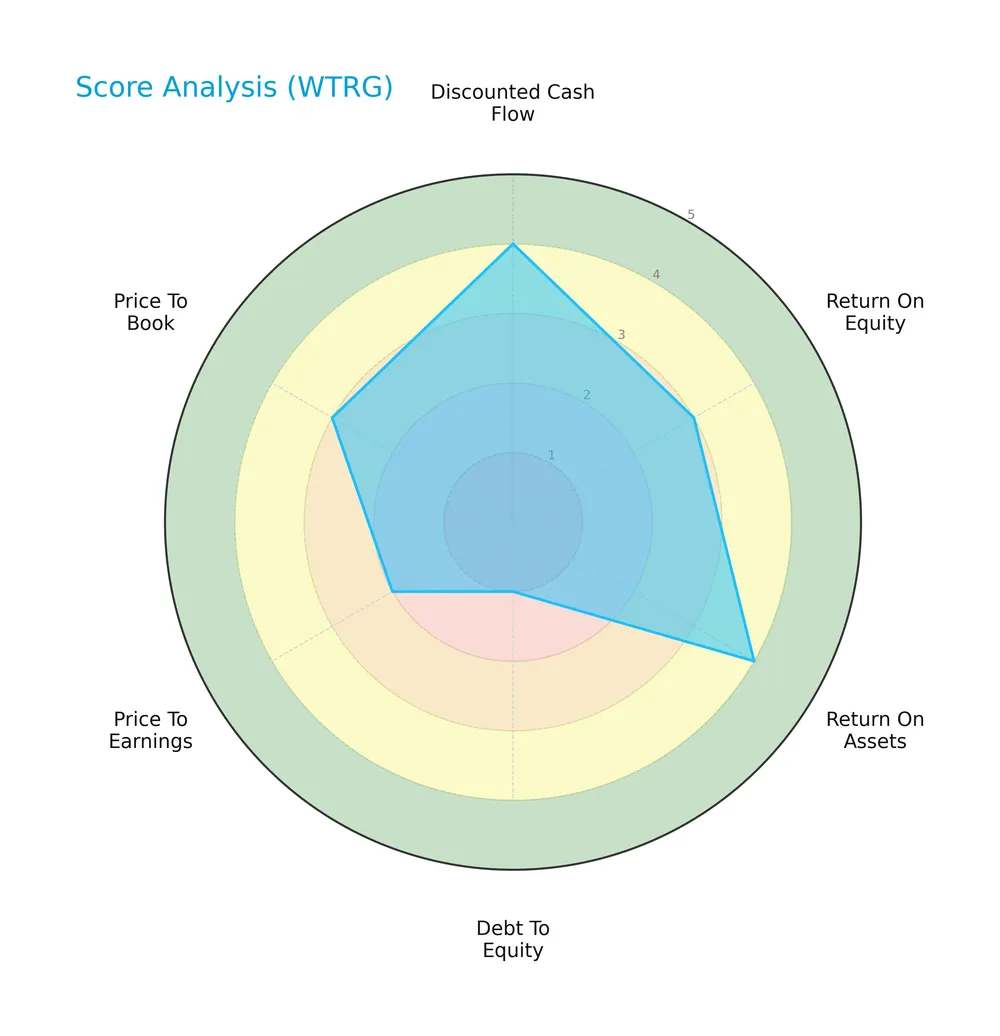

Score analysis

Below is a radar chart illustrating Essential Utilities, Inc.’s key financial scores across several valuation and performance metrics:

The company scores favorably on discounted cash flow (4) and return on assets (4), but struggles with debt-to-equity (1) and price-to-earnings (2). Return on equity and price-to-book metrics are moderate at 3 each.

Analysis of the company’s bankruptcy risk

Essential Utilities, Inc. falls in the distress zone with an Altman Z-Score of 1.31, indicating elevated bankruptcy risk and financial instability:

Is the company in good financial health?

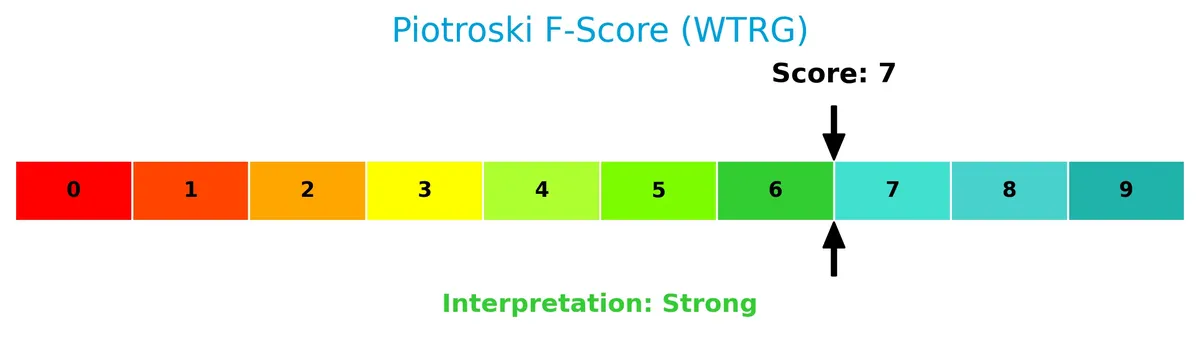

The Piotroski Score diagram below reflects the company’s financial strength based on nine criteria:

With a Piotroski Score of 7, Essential Utilities demonstrates strong financial health, signaling effective profitability, liquidity, and operational efficiency despite some risks.

Competitive Landscape & Sector Positioning

This sector analysis examines Essential Utilities, Inc.’s strategic positioning, revenue breakdown, key products, competitors, and competitive strengths. I will assess whether the company holds a sustainable competitive advantage in the regulated water industry.

Strategic Positioning

Essential Utilities, Inc. maintains a diversified product portfolio with leading revenue from natural gas (1.12B in 2025) and water services (1.09B), alongside wastewater and other segments. Its geographic exposure spans multiple U.S. states, serving 7.5M customers primarily under Aqua and Peoples brands.

Revenue by Segment

This pie chart displays Essential Utilities, Inc.’s revenue breakdown by segment for fiscal year 2025, highlighting contributions from Water, Natural Gas, Wastewater, and Other categories.

Essential Utilities’ revenue in 2025 centers on Natural Gas at 1.12B and Water at 1.09B, jointly driving the business. Wastewater, at 223M, adds meaningful diversification. Notably, Natural Gas revenue surged from 843M in 2024, signaling strong growth momentum. The Other segment remains minor but stable. This concentration in core utilities illustrates robust performance but also potential exposure to sector-specific risks.

Key Products & Brands

The table below outlines Essential Utilities, Inc.’s main products and brands along with their descriptions:

| Product | Description |

|---|---|

| Water | Provides regulated water services to residential, commercial, industrial, and fire protection customers. |

| Wastewater | Delivers wastewater treatment and sewer services across multiple U.S. states. |

| Natural Gas | Offers regulated natural gas services and raw water supply for natural gas drilling firms. |

| Other | Includes water and sewer line protection and repair services through third-party providers. |

| Aqua Brand | One of the primary brand names under which water and wastewater services are delivered. |

| Peoples Brand | Serves customers in selected states with water, wastewater, and natural gas utilities. |

Essential Utilities operates a diversified portfolio focused on regulated water, wastewater, and natural gas services. Its leading brands, Aqua and Peoples, serve approximately 7.5M customers across ten states, supporting steady utility demand.

Main Competitors

There are 34 competitors in the regulated water sector; below is a list of the top 10 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| GE Vernova Inc. | 184B |

| NextEra Energy, Inc. | 169B |

| Constellation Energy Corporation | 114B |

| The Southern Company | 96B |

| Duke Energy Corporation | 91B |

| American Electric Power Company, Inc. | 62B |

| Sempra | 59B |

| Vistra Corp. | 56B |

| Dominion Energy, Inc. | 51B |

| Exelon Corporation | 44B |

Essential Utilities, Inc. lacks a clear rank due to missing market cap data. The company falls below both the average market cap of the top 10 competitors (92.6B) and the sector median (29.6B). Without market cap figures, it is impossible to assess its distance from the nearest competitor or relative scale against the leader, GE Vernova Inc.

Comparisons with competitors

Check out how we compare the company to its competitors:

Aucun article trouvé pour ces critères.

Does Essential Utilities have a competitive advantage?

Essential Utilities does not yet demonstrate a clear competitive advantage, as its ROIC remains below WACC, indicating value erosion despite growing profitability. The company’s net margin of 24.9% is favorable, but gross and EBIT margins remain weak.

Looking ahead, Essential Utilities’ growth in revenue and net income suggests potential from expanding water services across multiple states. Opportunities lie in increasing municipal contracts and offering water and sewer line protection solutions to residential customers.

SWOT Analysis

This SWOT analysis highlights Essential Utilities, Inc.’s key strategic factors to guide investment decisions.

Strengths

- Strong net margin at 24.9%

- Growing revenue with 31.8% over five years

- Favorable dividend yield of 3.48%

Weaknesses

- Low ROE at 9% signals moderate equity returns

- Interest coverage is weak, raising financial risk

- Asset turnover is low, indicating inefficient use of assets

Opportunities

- Expanding water services in multiple states

- Increasing demand for regulated utilities

- Potential to improve operational efficiency and ROIC

Threats

- Regulatory changes in utilities sector

- Rising interest expenses could strain finances

- Competitive pressures from alternative water providers

Essential Utilities benefits from solid profitability and steady revenue growth. However, financial leverage and efficiency issues require caution. Strategic focus on operational improvements and regulatory navigation will be critical to sustain its competitive position.

Stock Price Action Analysis

The weekly stock chart of Essential Utilities, Inc. (WTRG) reveals price movements and volatility patterns over the past 12 months:

Trend Analysis

Over the past year, WTRG’s stock gained 11.02%, indicating a bullish trend. The price moved between $33.49 and $41.49, showing clear acceleration. The standard deviation of 1.64 signals moderate volatility. Recent months show a 4.82% gain with a gentle slope of 0.1 and lower volatility at 0.75.

Volume Analysis

Trading volume for WTRG is increasing overall, with 51.56% buyer participation across the year. However, the recent three months display seller dominance at 61.58%, with lower buyer volume. This shift suggests cautious or bearish sentiment and heightened selling pressure amid rising market activity.

Target Prices

Analysts present a clear target consensus for Essential Utilities, Inc. (WTRG).

| Target Low | Target High | Consensus |

|---|---|---|

| 38 | 45 | 42.25 |

The target range suggests moderate upside potential, reflecting confidence in stable utility sector fundamentals. Analyst expectations center on steady growth without aggressive expansion.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section examines Essential Utilities, Inc. (WTRG) through analyst grades and consumer feedback for balanced insights.

Stock Grades

The latest grades for Essential Utilities, Inc. reveal a cautious shift among top-tier analysts in late 2025:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Barclays | Downgrade | Underweight | 2025-12-17 |

| Jefferies | Downgrade | Hold | 2025-10-28 |

| UBS | Downgrade | Neutral | 2025-10-28 |

| Janney Montgomery Scott | Downgrade | Neutral | 2025-10-27 |

| Barclays | Maintain | Overweight | 2025-10-10 |

| Jefferies | Maintain | Buy | 2025-10-10 |

| UBS | Maintain | Buy | 2025-08-15 |

| Baird | Maintain | Outperform | 2025-08-04 |

| Baird | Maintain | Outperform | 2025-05-13 |

| Baird | Maintain | Outperform | 2025-04-04 |

Recent downgrades from Buy/Overweight to Hold/Neutral and Underweight indicate increased caution. However, several firms maintain positive views, supporting a consensus Buy rating overall.

Consumer Opinions

Consumers express a mix of appreciation and frustration toward Essential Utilities, Inc., reflecting its operational strengths and areas needing improvement.

| Positive Reviews | Negative Reviews |

|---|---|

| Reliable service with minimal interruptions | Customer service response times are often slow |

| Competitive pricing compared to regional peers | Billing errors reported by several customers |

| Transparent communication during outages | Limited digital tools for account management |

| Commitment to sustainability efforts | Occasional delays in infrastructure repairs |

Overall, customers praise Essential Utilities for dependable service and clear communication. However, slow customer support and billing issues emerge as consistent concerns, suggesting room for operational enhancements.

Risk Analysis

Below is a summary table outlining the key risks Essential Utilities, Inc. faces as an investment:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Financial Health | Altman Z-Score of 1.31 signals distress zone, risk of bankruptcy | Medium-High | High |

| Leverage | Debt-to-equity reported as zero, but interest coverage is zero | Medium | Medium |

| Profitability | ROE weak at 8.99%, below sector average, limiting capital returns | Medium | Medium |

| Operational Efficiency | Asset turnover very low at 0.2, signaling inefficiency | Medium | Medium |

| Market Valuation | P/E ratio neutral at 17.43 but price-to-earnings score unfavorable | Medium | Medium |

| Dividend Stability | Dividend yield favorable at 3.48%, but payout sustainability risk | Low | Medium |

The most pressing risk is the company’s Altman Z-Score, which places it in the distress zone, indicating elevated bankruptcy risk. Despite strong Piotroski score of 7, signaling solid fundamentals, the zero interest coverage ratio raises red flags about debt servicing ability. Low asset turnover also points to operational challenges. Investors should weigh these risks carefully against the stable dividend yield and moderate valuation.

Should You Buy Essential Utilities, Inc.?

Essential Utilities, Inc. appears to have improving profitability with a slightly favorable moat supported by growing ROIC, yet its leverage profile remains substantial, reflected in a distressed Altman Z-score. Overall, its financial health could be seen as moderate with a “B” rating.

Strength & Efficiency Pillars

Essential Utilities, Inc. shows operational resilience with a strong net margin of 24.91%. Its return on invested capital (ROIC) of 7.6% slightly exceeds its weighted average cost of capital (WACC) at 7.42%, indicating modest value creation. Despite an unimpressive return on equity (8.99%), the company’s revenue and net income have grown significantly over the long term, signaling improving profitability and operational efficiency.

Weaknesses and Drawbacks

The company is in financial distress, with an Altman Z-Score of 1.31, signaling a high bankruptcy risk. This overrides other profitability measures. Additionally, interest coverage is zero, highlighting severe difficulty in meeting debt obligations. Market pressure is evident as recent buyer dominance drops to 38.42%, reflecting seller control. The valuation remains neutral with a P/E of 17.43 and P/B of 1.57, but the distressed solvency casts a shadow on these metrics.

Our Final Verdict about Essential Utilities, Inc.

Despite operational strengths and a bullish long-term price trend, Essential Utilities, Inc.’s financial distress, highlighted by a dangerously low Altman Z-Score, makes this investment highly speculative. Solvency concerns dominate the risk profile. For conservative capital, the company appears too risky. Investors might consider waiting for signs of improved financial stability before adding exposure.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Decoding Essential Utilities Inc (WTRG): A Strategic SWOT Insigh – GuruFocus (Feb 27, 2026)

- Essential Utilities, Inc. SEC 10-K Report – TradingView (Feb 26, 2026)

- Why Essential Utilities (WTRG) is a Top Dividend Stock for Your Portfolio – Yahoo Finance (Feb 26, 2026)

- Essential pours $1.4B into pipes as American Water merger advances – Stock Titan (Feb 25, 2026)

- Essential Utilities Q4 Earnings Beat Estimates, Revenues Rise Y/Y – Zacks Investment Research (Feb 26, 2026)

For more information about Essential Utilities, Inc., please visit the official website: essential.co