Home > Analyses > Healthcare > Edwards Lifesciences Corporation

Edwards Lifesciences transforms cardiac care by pioneering minimally invasive heart valve therapies. Its innovative transcatheter solutions redefine treatment for structural heart disease worldwide. Renowned for cutting-edge technology and clinical excellence, Edwards dominates the medical devices sector with flagship products like the PASCAL and INSPIRIS valve systems. As the company navigates evolving healthcare demands, I question whether its robust fundamentals justify current valuations and future growth prospects.

Table of contents

Business Model & Company Overview

Edwards Lifesciences Corporation, founded in 1958 and based in Irvine, California, leads the medical devices sector with a dominant position in structural heart disease solutions. Its portfolio forms a cohesive ecosystem, including transcatheter heart valve replacements and repairs, surgical heart solutions, and critical care monitoring technologies. This integrated approach targets complex cardiac conditions with innovative, minimally invasive therapies.

The company’s revenue engine balances high-value devices and advanced software, such as the Acumen Hypotension Prediction Index, enhancing patient outcomes. Edwards commands strategic markets across the Americas, Europe, and Asia through direct sales and distributors. Its strong economic moat stems from proprietary technologies and a robust global footprint that shapes the future of cardiac care.

Financial Performance & Fundamental Metrics

I analyze Edwards Lifesciences Corporation’s income statement, key financial ratios, and dividend payout policy to assess its core financial health and shareholder returns.

Income Statement

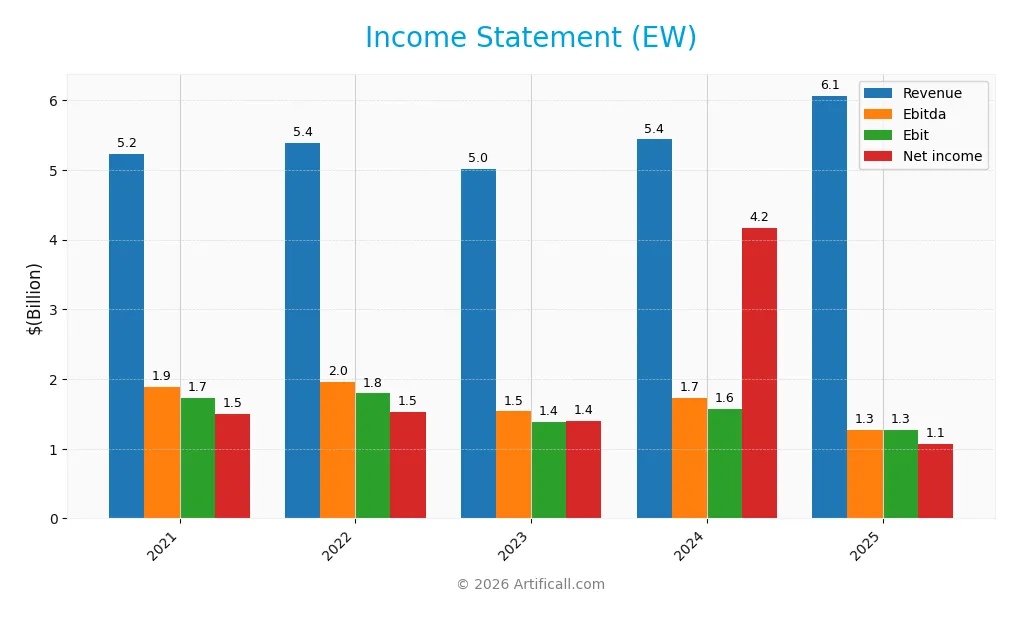

The table below summarizes Edwards Lifesciences Corporation’s key income statement figures for the fiscal years 2021 through 2025.

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| Revenue | 5.23B | 5.38B | 5.01B | 5.44B | 6.07B |

| Cost of Revenue | 1.23B | 1.17B | 1.04B | 1.12B | 1.33B |

| Operating Expenses | 2.40B | 2.51B | 2.55B | 2.94B | 3.10B |

| Gross Profit | 4.01B | 4.22B | 3.97B | 4.32B | 4.74B |

| EBITDA | 1.89B | 1.96B | 1.53B | 1.72B | 1.27B |

| EBIT | 1.73B | 1.79B | 1.39B | 1.57B | 1.27B |

| Interest Expense | 24.8M | 26.2M | 17.6M | 19.8M | 0 |

| Net Income | 1.50B | 1.52B | 1.40B | 4.17B | 1.07B |

| EPS | 2.41 | 2.46 | 2.31 | 6.98 | 1.84 |

| Filing Date | 2022-02-14 | 2023-02-13 | 2024-02-12 | 2025-02-28 | 2026-02-25 |

Income Statement Evolution

Between 2021 and 2025, Edwards Lifesciences’ revenue grew 16%, reaching $6.07B in 2025. However, net income declined 29% over the same period. Gross margin remained strong at 78%, but net margin compressed 38%, indicating rising costs or margin pressure despite top-line growth. EBIT showed a notable 19% drop in the latest year.

Is the Income Statement Favorable?

In 2025, fundamentals appear generally favorable with a 17.7% net margin and zero interest expense, signaling efficient cost control and low leverage. Revenue grew 11.6% year-over-year, supporting operational scale. Yet, the 19% EBIT decline and nearly 74% EPS drop warn of profitability challenges. Overall, the income statement balances solid margins against deteriorating earnings trends.

Financial Ratios

The following table presents key financial ratios for Edwards Lifesciences Corporation (EW) over the last five fiscal years, illustrating profitability, valuation, liquidity, leverage, and efficiency metrics:

| Ratios | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Net Margin | 29% | 28% | 28% | 77% | 18% |

| ROE | 26% | 26% | 21% | 42% | 10% |

| ROIC | 19% | 20% | 15% | 11% | 11% |

| P/E | 54 | 30 | 33 | 11 | 46 |

| P/B | 14 | 8 | 7 | 4 | 5 |

| Current Ratio | 3.1 | 3.0 | 3.4 | 4.2 | 3.7 |

| Quick Ratio | 2.4 | 2.2 | 2.6 | 3.5 | 3.1 |

| D/E | 0.12 | 0.12 | 0.10 | 0.07 | 0.01 |

| Debt-to-Assets | 8% | 8% | 7% | 5% | 1% |

| Interest Coverage | 65 | 65 | 81 | 70 | 0 |

| Asset Turnover | 0.62 | 0.65 | 0.54 | 0.42 | 0.44 |

| Fixed Asset Turnover | 3.2 | 3.1 | 3.0 | 3.0 | 3.2 |

| Dividend Yield | 0% | 0% | 0% | 0% | 0% |

*Net Margin and ROE show volatility, with an outlier spike in 2024’s reported net margin suggesting a data anomaly or one-time effect. *Interest coverage drops to zero in 2025, which is a red flag warranting further investigation. *Leverage remains very low throughout, with debt-to-equity under 0.12 consistently, indicating minimal financial risk from debt. *Liquidity ratios remain strong, well above 1.0, signaling good short-term financial health. *Valuation multiples fluctuate, with P/E peaking in 2021 and dipping sharply in 2024 before rising again in 2025. *The consistent zero dividend yield confirms no dividend payments over these years.

Evolution of Financial Ratios

Return on Equity (ROE) showed a steep decline from 41.75% in 2024 to 10.38% in 2025, indicating lower profitability. The Current Ratio fluctuated, peaking at 4.18 in 2024 before easing to 3.72 in 2025, reflecting stable liquidity. Debt-to-Equity Ratio steadily decreased to a very low 0.01 in 2025, signaling reduced leverage.

Are the Financial Ratios Fovorable?

Profitability ratios in 2025 present a mixed picture: net margin (17.7%) and ROIC (11.4%) are favorable, but ROE (10.4%) and WACC (8.0%) are neutral. Liquidity shows strength in the quick ratio (3.1, favorable) but weakness in the current ratio (3.7, unfavorable). Low debt ratios (D/E 0.01, debt/assets 0.78%) and infinite interest coverage are positive. Market multiples, however, exhibit overvaluation risks with a high P/E of 46.4 and P/B of 4.82. Asset turnover is weak at 0.44. Overall, the ratios are slightly favorable.

Shareholder Return Policy

Edwards Lifesciences Corporation does not pay dividends, reflecting its reinvestment strategy likely aimed at sustaining growth and innovation. The company maintains a strong liquidity position and minimal debt, supporting capital allocation towards R&D and acquisitions.

While share buybacks are not explicitly reported, the absence of dividends aligns with a focus on long-term value creation. This approach suits companies in growth phases, though investors should monitor for any shift in capital distribution to ensure sustainability.

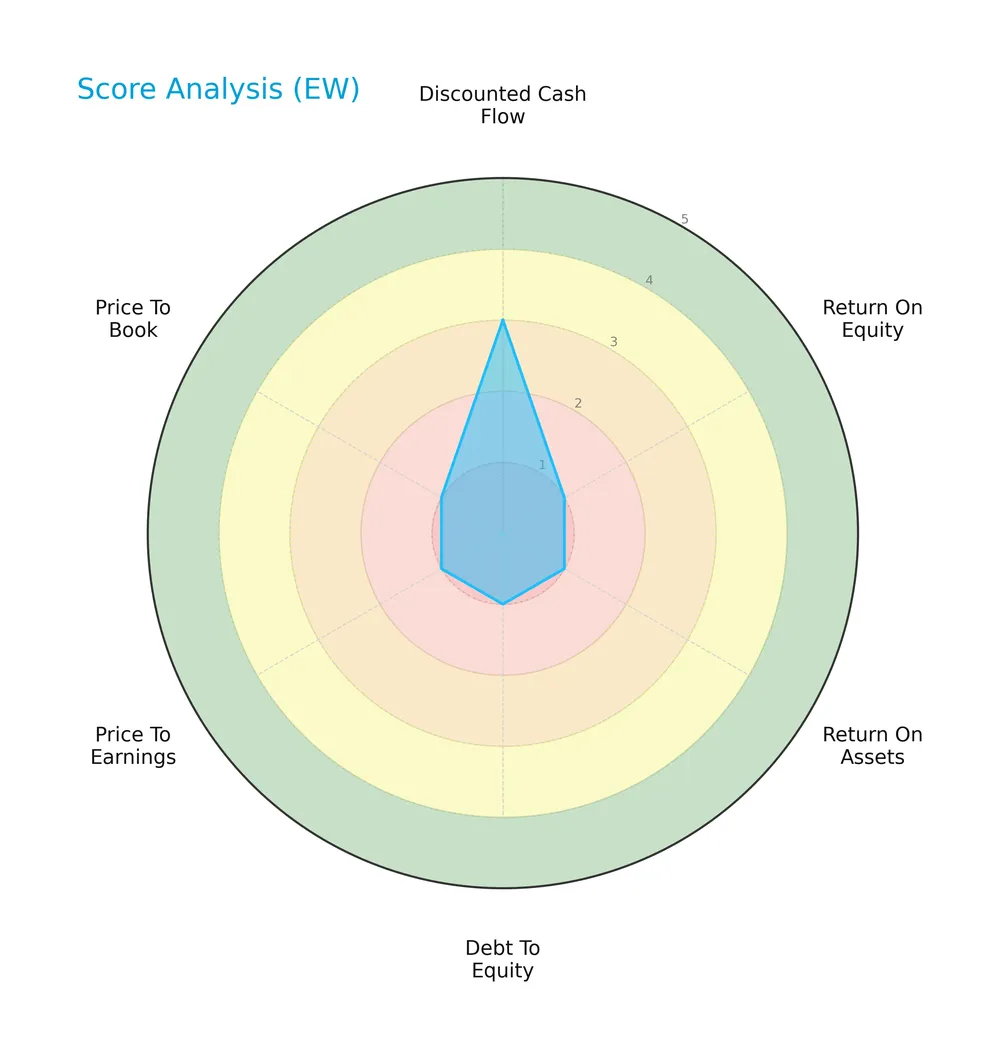

Score analysis

The radar chart below presents Edwards Lifesciences Corporation’s key financial scores for a quick performance overview:

The discounted cash flow score rates moderate at 3, while all other metrics—including ROE, ROA, debt to equity, P/E, and P/B—score very unfavorable at 1, indicating significant weaknesses across profitability and valuation measures.

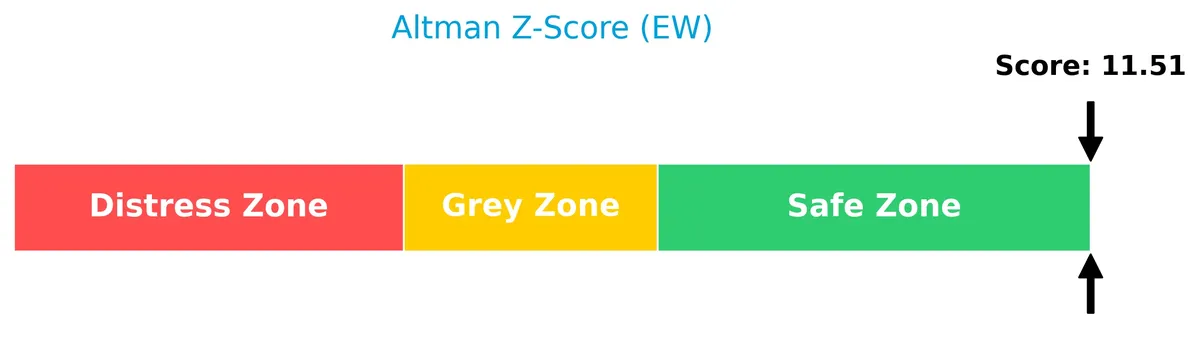

Analysis of the company’s bankruptcy risk

Edwards Lifesciences’ Altman Z-Score places it confidently in the safe zone, signaling low risk of bankruptcy:

Is the company in good financial health?

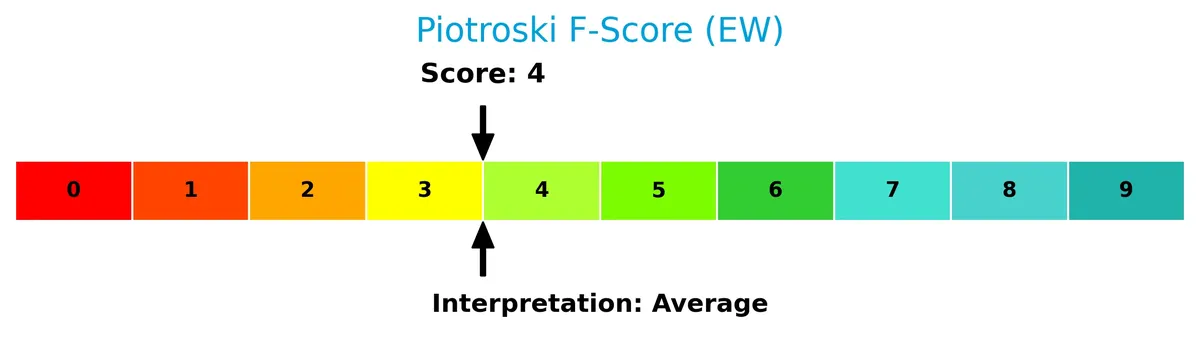

The Piotroski Score diagram highlights the company’s financial strength based on nine key accounting criteria:

With a Piotroski Score of 6, Edwards Lifesciences shows average financial health, suggesting moderate operational efficiency and stability but leaving room for improvement.

Competitive Landscape & Sector Positioning

This sector analysis reviews Edwards Lifesciences Corporation’s strategic positioning, revenue segments, and key products. I will assess whether Edwards holds a competitive advantage over its main competitors.

Strategic Positioning

Edwards Lifesciences focuses on a concentrated product portfolio in heart valve therapies and critical care solutions. Its revenue predominantly derives from the US (3.54B in 2025), with significant exposure to Europe (1.52B), Japan, and other regions, reflecting a balanced geographic presence.

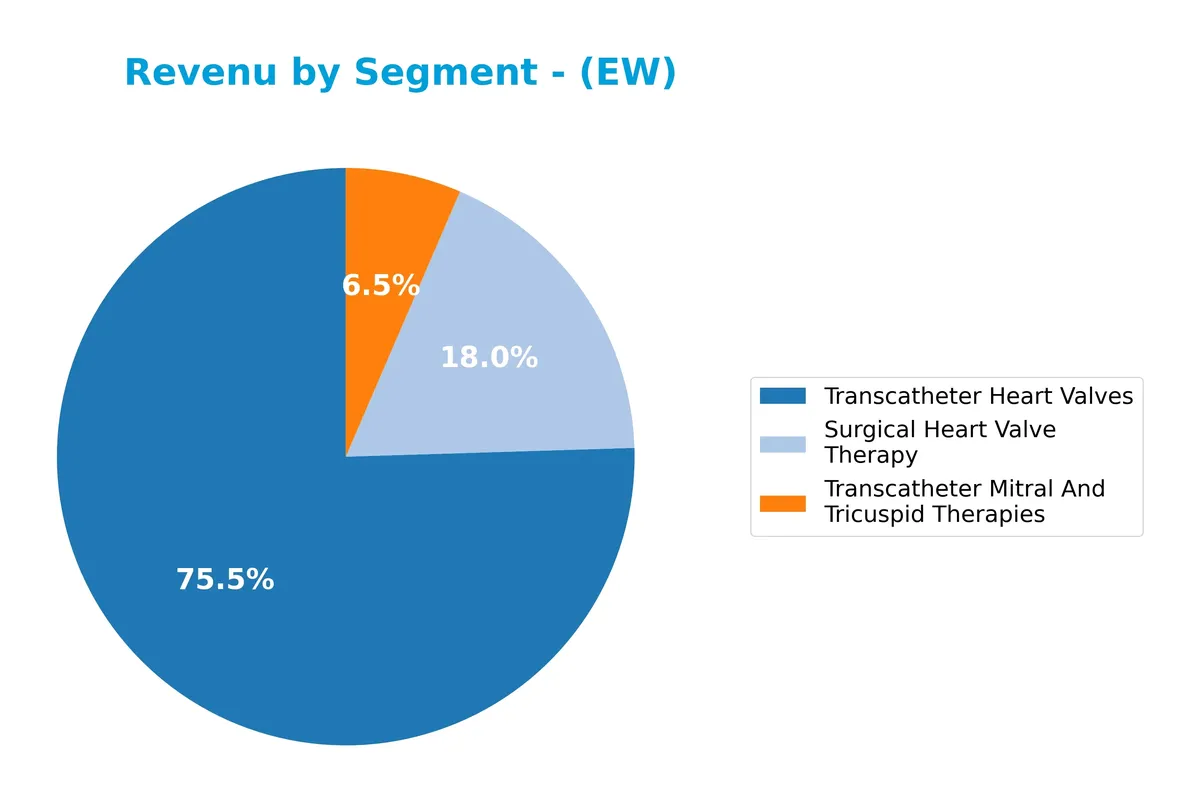

Revenue by Segment

This pie chart illustrates Edwards Lifesciences Corporation’s revenue distribution by product segment for the fiscal year 2025, highlighting key areas of growth and concentration.

In 2025, Transcatheter Heart Valves dominate revenue at $4.49B, reflecting strong market adoption and innovation. Surgical Heart Valve Therapy remains a solid contributor with $1.03B, showing steady demand. Notably, Transcatheter Mitral and Tricuspid Therapies surged to $551M, more than doubling from 2024, signaling accelerating growth in this niche. The shift toward transcatheter solutions underscores Edwards’ strategic focus on less invasive procedures and expanding its technological moat.

Key Products & Brands

Edwards Lifesciences generates revenue through these key products and brands:

| Product | Description |

|---|---|

| Transcatheter Heart Valves | Minimally invasive replacement of heart valves, leading the company’s revenue streams. |

| Transcatheter Mitral And Tricuspid Therapies | Repair and replacement products for mitral and tricuspid valve diseases using transcatheter systems. |

| Surgical Heart Valve Therapy | Surgical solutions including aortic surgical valves and specialized valve conduits like INSPIRIS and KONECT RESILIA. |

| Critical Care | Advanced hemodynamic monitoring systems and predictive software for managing patient heart function and blood pressure. |

Edwards Lifesciences focuses on structural heart disease and critical care devices. The transcatheter heart valves segment dominates, reflecting industry trends favoring minimally invasive procedures. Surgical and critical care products complement the portfolio, supporting broad clinical applications.

Main Competitors

In total, 10 competitors operate in the Healthcare Medical – Devices sector; below are the top 10 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| Abbott Laboratories | 216B |

| Boston Scientific Corporation | 140B |

| Stryker Corporation | 133B |

| Medtronic plc | 123B |

| Edwards Lifesciences Corporation | 50B |

| DexCom, Inc. | 26B |

| STERIS plc | 25B |

| Insulet Corporation | 20B |

| Zimmer Biomet Holdings, Inc. | 18B |

| Align Technology, Inc. | 11B |

Edwards Lifesciences ranks 5th among its peers, holding about 23% of the market cap of the sector leader Abbott Laboratories. The company sits below the average market cap of the top 10 competitors but remains above the sector median. It enjoys a substantial 151.6% market cap gap over its nearest larger rival.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does Edwards Lifesciences Corporation have a competitive advantage?

Edwards Lifesciences shows a competitive advantage by generating returns on invested capital (ROIC) 3.36% above its cost of capital, indicating value creation despite a declining ROIC trend. Its strong gross margin of 78.13% and favorable net margin of 17.69% further support its market position in medical devices.

Looking ahead, Edwards Lifesciences pursues growth through innovative transcatheter heart valve products and advanced critical care monitoring systems. Expansion in established markets like the US and Europe, alongside emerging opportunities in Japan and other regions, underpins its future revenue potential.

SWOT Analysis

This analysis highlights Edwards Lifesciences Corporation’s key internal and external factors to inform strategic decisions.

Strengths

- strong gross margin at 78%

- favorable net margin near 18%

- very low debt levels with high interest coverage

Weaknesses

- declining ROIC trend signals weakening profitability

- high valuation multiples (PE 46, PB 4.8)

- net income and EPS growth negative over 5 years

Opportunities

- expanding structural heart disease market globally

- innovation in minimally-invasive valve technologies

- growth potential in emerging markets

Threats

- regulatory risks in medical device approvals

- intense competition in cardiac devices

- economic downturns impacting elective procedures

Edwards shows solid profitability and a strong balance sheet, but its declining profitability trend and rich valuation warrant caution. Growth hinges on innovation and global expansion, while regulatory and market risks remain critical.

Stock Price Action Analysis

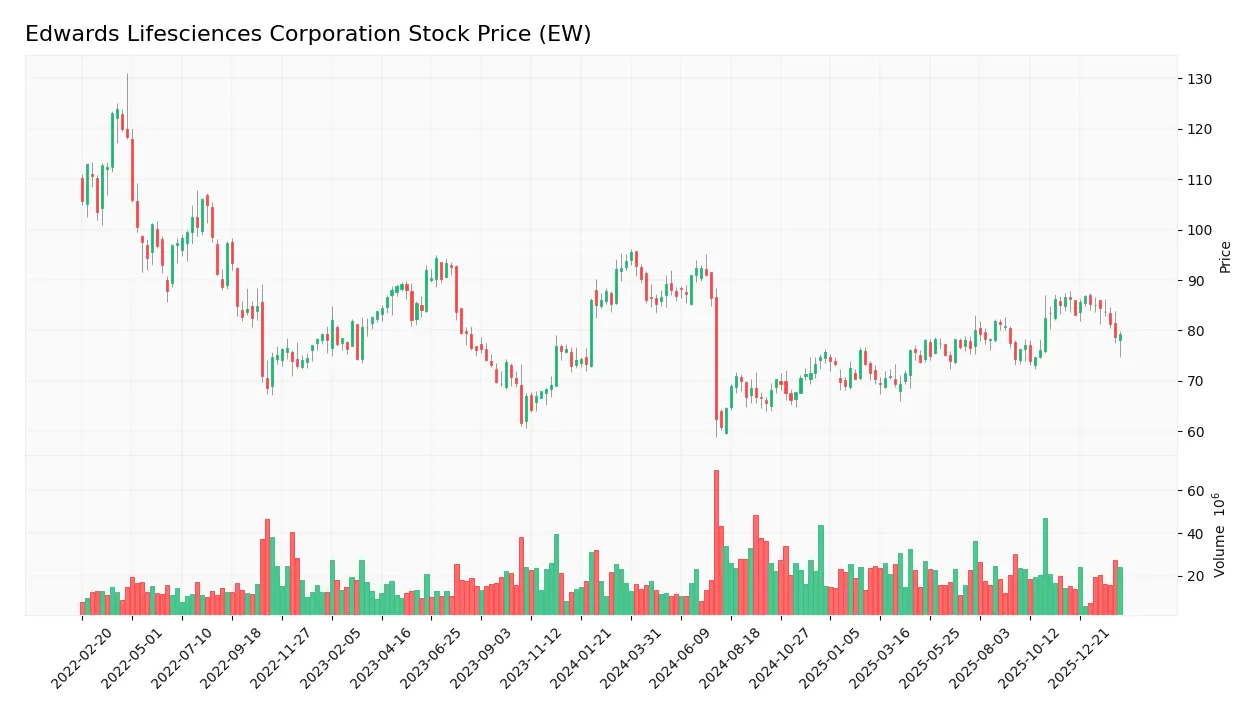

The weekly stock chart for Edwards Lifesciences Corporation displays price movements over the past 12 months, highlighting key highs and lows:

Trend Analysis

Over the past 12 months, EW’s stock price fell by 10.03%, indicating a bearish trend. The descent shows deceleration, with a high of 92.7 and a low of 60.83. Recent three-month data reveals a slight 0.39% increase but maintains a negative slope, confirming a neutral short-term trend.

Volume Analysis

Trading volume over the last three months is decreasing, with seller dominance at 71.41%. This indicates cautious investor sentiment and subdued market participation, as selling pressure outweighs buying interest significantly during this period.

Target Prices

Analysts set a consensus target price of $96.38, reflecting cautious optimism.

| Target Low | Target High | Consensus |

|---|---|---|

| 87 | 110 | 96.38 |

The target range suggests moderate upside potential, with expectations centered near $96, indicating confidence tempered by market uncertainties.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

This section examines Edwards Lifesciences Corporation’s analyst ratings and consumer feedback to provide balanced insights.

Stock Grades

Here is the latest summary of Edwards Lifesciences Corporation’s stock grades from recognized analysts:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Truist Securities | Maintain | Hold | 2026-02-11 |

| Piper Sandler | Maintain | Overweight | 2026-02-11 |

| Wells Fargo | Maintain | Overweight | 2026-02-11 |

| BTIG | Maintain | Buy | 2026-02-11 |

| Goldman Sachs | Maintain | Buy | 2026-02-11 |

| Piper Sandler | Maintain | Overweight | 2026-01-20 |

| Stifel | Maintain | Buy | 2026-01-20 |

| UBS | Maintain | Neutral | 2026-01-12 |

| Barclays | Maintain | Overweight | 2026-01-12 |

| TD Cowen | Upgrade | Buy | 2026-01-09 |

The overall trend leans positive, with most analysts assigning Buy or Overweight ratings. Only a few maintain Hold or Neutral grades, indicating measured optimism around Edwards Lifesciences.

Consumer Opinions

Edwards Lifesciences commands strong loyalty, yet some users voice concerns that merit attention.

| Positive Reviews | Negative Reviews |

|---|---|

| “Exceptional product quality and reliability.” | “High prices limit accessibility.” |

| “Outstanding customer support and responsiveness.” | “Occasional delays in product delivery.” |

| “Innovative technology that improves patient outcomes.” | “Complex installation process for some devices.” |

| “Trusted brand with a strong industry reputation.” | “Limited availability in certain regions.” |

Consumers consistently praise Edwards for innovation and customer service. However, pricing and supply chain issues appear as recurring challenges.

Risk Analysis

Below is a summary of key risks facing Edwards Lifesciences Corporation, assessing likelihood and potential impact:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Valuation Risk | High P/E (46.44) and P/B (4.82) ratios suggest the stock is overvalued. | Medium | High |

| Profitability Pressure | ROE (10.38%) and asset turnover (0.44) are weak, limiting growth potential. | Medium | Medium |

| Competitive Risk | Intense innovation in med-tech may erode Edwards’ market share. | Medium | High |

| Operational Risk | Supply chain disruptions could impact product availability. | Low | Medium |

| Financial Stability | Strong Altman Z-Score (11.37) indicates low bankruptcy risk. | Low | Low |

| Dividend Policy Risk | No dividend yield may deter income-focused investors. | High | Low |

Edwards faces the most significant risks from stretched valuation metrics and moderate profitability constraints. Despite solid financial stability, its premium multiples imply expectations for strong innovation and growth. Recent sector trends underscore intensifying competition in structural heart devices, which could pressure margins. Investors should weigh these factors carefully.

Should You Buy Edwards Lifesciences Corporation?

Edwards Lifesciences appears to have a slightly favorable moat with value creation despite a declining ROIC trend. Its debt profile looks manageable, supported by a strong Altman Z-score, yet profitability signals and overall rating suggest caution, indicating a C- rating.

Strength & Efficiency Pillars

Edwards Lifesciences Corporation exhibits solid operational efficiency with a net margin of 17.69% and a ROIC of 11.4%, both favorable indicators. Its ROIC exceeds the WACC of 8.04%, confirming the company as a value creator. Despite a declining ROIC trend, the firm maintains a slightly favorable moat, supported by a strong gross margin of 78.13% and efficient fixed asset turnover at 3.17. These metrics underscore its ability to generate returns above its cost of capital, a key driver of sustained value creation.

Weaknesses and Drawbacks

The company faces valuation challenges, with an elevated P/E ratio of 46.44 and a P/B ratio of 4.82, signaling premium market expectations. Additionally, asset turnover is weak at 0.44, reflecting potential inefficiencies in asset utilization. Market pressure intensifies due to seller dominance at 71.41% over the recent period, heightening short-term volatility risks. While liquidity ratios are mixed, a high current ratio of 3.72 contrasts with a favorable debt-to-equity of 0.01, suggesting ample liquidity but possible capital underutilization.

Our Final Verdict about Edwards Lifesciences Corporation

Edwards Lifesciences maintains a fundamentally sound profile, underpinned by value creation and profitability above its cost of capital. However, bearish overall and recent market trends coupled with seller dominance suggest caution. Despite its operational strengths, the stock’s premium valuation and technical softness may warrant a wait-and-see approach for a more favorable entry point. The profile might appear attractive for long-term exposure, but timing remains critical.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Here is Why Edwards Lifesciences Corporation (EW) Looks Attractive – Yahoo Finance (Feb 23, 2026)

- Decoding Edwards Lifesciences Corp (EW): A Strategic SWOT Insigh – GuruFocus (Feb 26, 2026)

- Edwards Lifesciences Corporation $EW Shares Sold by Citigroup Inc. – MarketBeat (Feb 24, 2026)

- Here is Why Edwards Lifesciences Corporation (EW) Looks Attractive – Bitget (Feb 23, 2026)

- Zacks Industry Outlook Highlights Intuitive Surgical, Edwards Lifesciences and Electromed – TradingView (Feb 24, 2026)

For more information about Edwards Lifesciences Corporation, please visit the official website: edwards.com