Home > Analyses > Energy > Denison Mines Corp.

Denison Mines Corp. powers the future of clean energy by unlocking some of the world’s richest uranium deposits in Canada’s Athabasca Basin. As a recognized leader in uranium exploration and development, Denison’s flagship Wheeler River project stands at the forefront of the nuclear fuel supply chain, combining innovation with disciplined resource management. With growing interest in nuclear power’s role in carbon reduction, I explore whether Denison’s current fundamentals and market position justify its valuation and offer compelling growth potential for investors.

Table of contents

Business Model & Company Overview

Denison Mines Corp., founded in 1997 and headquartered in Toronto, Canada, is a leading player in the uranium sector. Its core mission revolves around developing a robust ecosystem of uranium assets, notably the flagship Wheeler River project in Saskatchewan’s Athabasca Basin, where it holds a 95% interest. This focus positions Denison as a significant force in uranium exploration and extraction, underpinning its competitive stature within the energy industry.

The company’s revenue engine is driven primarily by uranium property acquisition, development, and processing, supported by its strategic foothold in Canada’s prolific mining regions. While its operations concentrate heavily on hardware—mining and processing facilities—the value creation also depends on its ability to advance projects toward production. Denison’s deep specialization and dominant asset base build a durable economic moat, shaping the future of nuclear fuel supply in global energy markets.

Financial Performance & Fundamental Metrics

This section provides a fundamental analysis of Denison Mines Corp., focusing on its income statement, key financial ratios, and dividend payout policy.

Income Statement

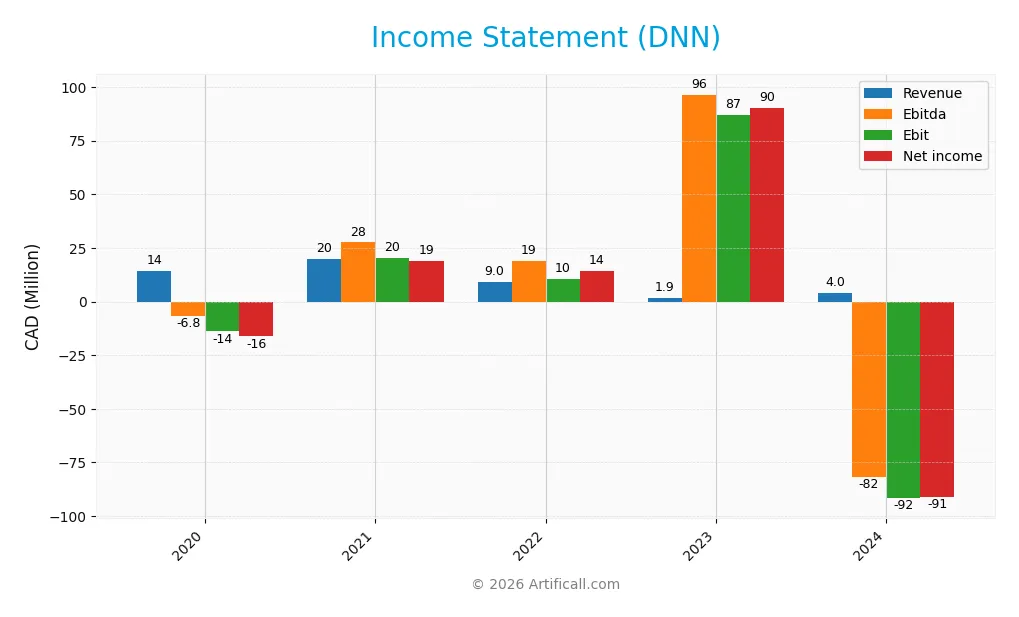

The table below presents Denison Mines Corp.’s key income statement figures for the fiscal years 2020 through 2024, reported in CAD.

| 2020 | 2021 | 2022 | 2023 | 2024 | |

|---|---|---|---|---|---|

| Revenue | 14.4M | 20.0M | 8.97M | 1.86M | 4.02M |

| Cost of Revenue | 10.3M | 12.6M | 5.11M | 3.71M | 4.82M |

| Operating Expenses | 4.09M | 30.7M | 40.4M | -1.86M | 62.5M |

| Gross Profit | 4.09M | 7.38M | 3.87M | -1.86M | -0.79M |

| EBITDA | -6.82M | 27.5M | 19.0M | 96.5M | -81.8M |

| EBIT | -13.97M | 20.1M | 10.4M | 87.1M | -91.7M |

| Interest Expense | 3.18M | 3.17M | 0.06M | 0.05M | 0.11M |

| Net Income | -16.3M | 19.0M | 14.4M | 90.4M | -91.1M |

| EPS | -0.0259 | 0.0242 | 0.0175 | 0.11 | -0.1 |

| Filing Date | 2021-03-29 | 2022-03-25 | 2023-03-28 | 2024-03-28 | 2025-03-28 |

Income Statement Evolution

Denison Mines Corp. experienced a significant decline in revenue and net income from 2020 to 2024, with revenue dropping by 72.11% over the period. Despite a favorable 116.87% revenue increase from 2023 to 2024, the company’s gross margin remained negative at -19.69%, indicating persistent cost challenges. EBIT and net margins also deteriorated substantially, reflecting worsening profitability and efficiency.

Is the Income Statement Favorable?

The 2024 income statement shows unfavorable fundamentals, with a net loss of CAD 91.1M and a negative net margin of -2264.95%. Operating expenses rose in line with revenue growth, but EBIT declined by 205.33%, signaling operational inefficiency. Although interest expense is low relative to income, the overall financial results remain unfavorable, with 78.57% of income statement metrics assessed negatively.

Financial Ratios

The table below presents key financial ratios for Denison Mines Corp. (ticker: DNN) over the fiscal years 2020 to 2024, illustrating profitability, valuation, liquidity, leverage, and operational efficiency metrics:

| Ratios | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Net Margin | -1.13% | 0.95% | 1.60% | 48.72% | -22.65% |

| ROE | -9.13% | 4.78% | 3.29% | 14.08% | -16.15% |

| ROIC | 0% | -4.73% | -7.34% | 0% | -10.03% |

| P/E | -31.85 | 71.52 | 88.84 | 21.99 | -25.35 |

| P/B | 2.91 | 3.42 | 2.92 | 3.10 | 4.09 |

| Current Ratio | 4.17 | 5.31 | 3.65 | 8.28 | 3.65 |

| Quick Ratio | 3.92 | 5.10 | 3.50 | 8.08 | 3.54 |

| D/E | 0.003 | 0 | 0 | 0 | 0 |

| Debt-to-Assets | 0.002 | 0 | 0 | 0 | 0 |

| Interest Coverage | 0 | -7.37 | -608.55 | 0 | -586.32 |

| Asset Turnover | 0.051 | 0.039 | 0.017 | 0.003 | 0.006 |

| Fixed Asset Turnover | 0.072 | 0.079 | 0.035 | 0.007 | 0.015 |

| Dividend Yield | 0% | 0% | 0% | 0% | 0% |

Evolution of Financial Ratios

Denison Mines Corp. experienced a marked decline in Return on Equity (ROE), dropping to -16.15% in 2024, indicating a significant downturn in profitability. The Current Ratio decreased from a high of 8.28 in 2023 to 3.65 in 2024, showing reduced but still strong short-term liquidity. The Debt-to-Equity Ratio remained stable at zero, reflecting no reliance on debt financing. Profitability margins deteriorated sharply in 2024 compared to prior years.

Are the Financial Ratios Favorable?

In 2024, Denison Mines posted unfavorable profitability ratios with a negative net margin of -2264.95% and a negative ROE, signaling weak earnings performance. Liquidity showed mixed signals: the quick ratio was favorable at 3.54, while the current ratio was unfavorable at 3.65. Leverage ratios were favorable with zero debt, but efficiency ratios such as asset turnover were unfavorable, pointing to poor asset utilization. Market value ratios were largely unfavorable except for a favorable price-to-earnings ratio, leading to an overall unfavorable financial ratio evaluation.

Shareholder Return Policy

Denison Mines Corp. (DNN) does not pay dividends, reflecting its negative net income and free cash flow in recent years. The company appears to prioritize reinvestment and operational development over shareholder distributions, with no indication of share buyback programs.

This approach aligns with a potential long-term value creation strategy focused on growth and capital preservation, given current financial constraints. However, sustained negative margins and cash flow deficits suggest ongoing risks to profitability and shareholder returns.

Score analysis

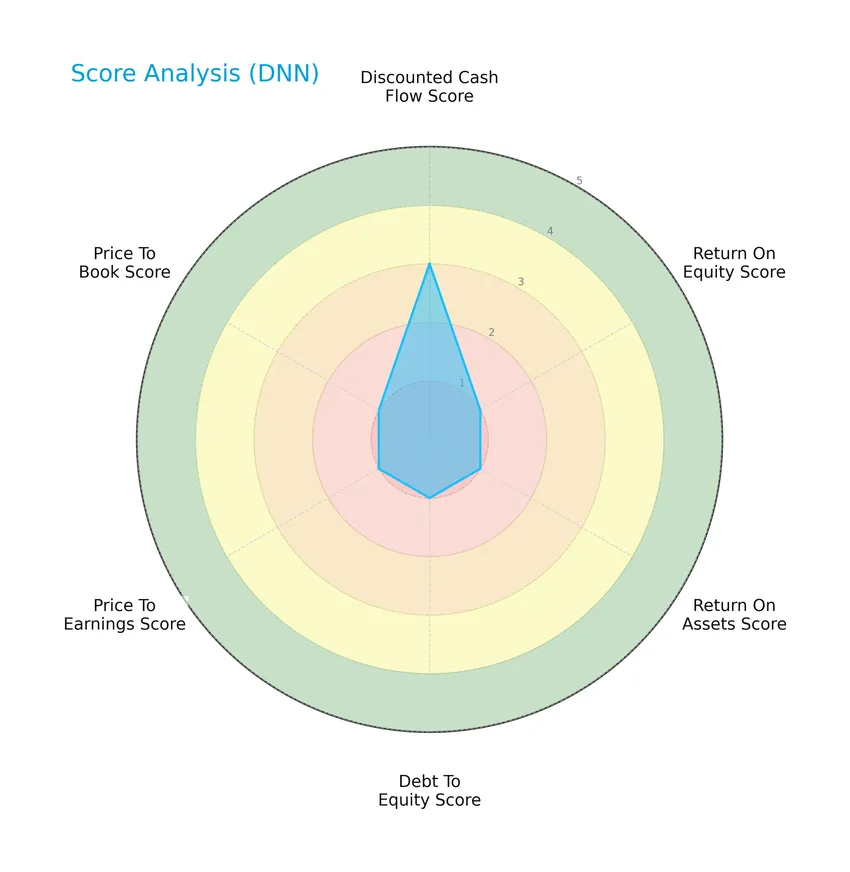

The following radar chart presents Denison Mines Corp.’s key financial scores for a comprehensive evaluation:

Denison Mines Corp. shows a moderate discounted cash flow score of 3, while all other scores—including return on equity, return on assets, debt to equity, price to earnings, and price to book—register very unfavorable values at 1, reflecting significant challenges in profitability, leverage, and valuation metrics.

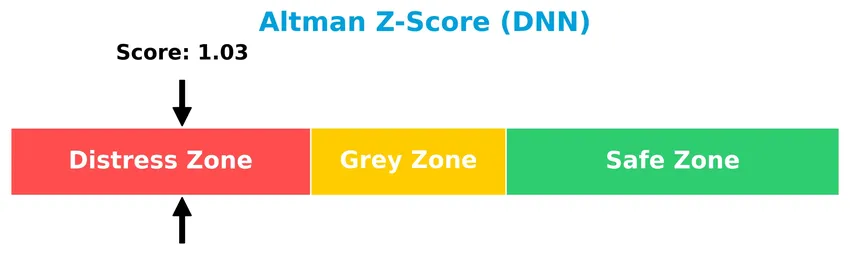

Analysis of the company’s bankruptcy risk

The Altman Z-Score places Denison Mines Corp. in the distress zone, indicating a high probability of financial distress and potential bankruptcy risk:

Is the company in good financial health?

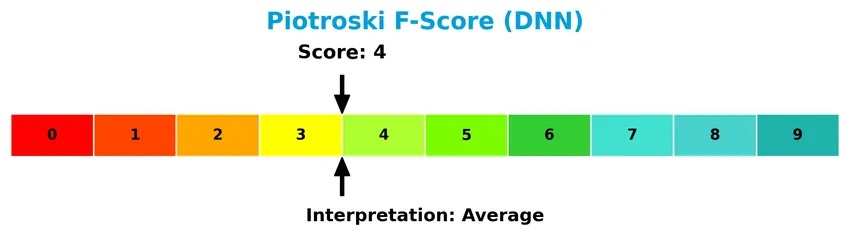

The Piotroski Score diagram below illustrates Denison Mines Corp.’s financial health evaluation based on nine accounting criteria:

With a Piotroski Score of 4, Denison Mines Corp. demonstrates average financial strength, suggesting moderate but not robust financial health. This score indicates some positive aspects in profitability and efficiency, yet also highlights room for improvement in stability and leverage.

Competitive Landscape & Sector Positioning

This sector analysis will examine Denison Mines Corp.’s strategic positioning, revenue by segment, key products, main competitors, competitive advantages, and SWOT analysis. I will assess whether Denison Mines holds a competitive advantage relative to its peers in the uranium industry.

Strategic Positioning

Denison Mines Corp. maintains a concentrated strategic position focused on uranium through acquisition, exploration, and development primarily in Canada, notably its 95% interest in the Wheeler River project in Saskatchewan’s Athabasca Basin, highlighting a geographically and product-focused portfolio.

Key Products & Brands

The table below outlines Denison Mines Corp.’s key products and projects:

| Product | Description |

|---|---|

| Wheeler River uranium project | A flagship uranium property with a 95% ownership, located in the Athabasca Basin, northern Saskatchewan, Canada. |

| Uranium exploration and development | Activities focused on acquiring, exploring, developing, extracting, processing, and selling uranium properties in Canada. |

Denison Mines Corp. primarily focuses on uranium-related assets and operations, with the Wheeler River project as its central asset in the Canadian energy sector.

Main Competitors

There are 10 competitors in total, with the table below listing the top 10 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| Cameco Corporation | 39.8B |

| NexGen Energy Ltd. | 6.0B |

| Uranium Energy Corp. | 5.6B |

| Centrus Energy Corp. | 4.2B |

| Energy Fuels Inc. | 3.5B |

| Denison Mines Corp. | 2.4B |

| Ur-Energy Inc. | 507M |

| IsoEnergy Ltd. | 499M |

| Uranium Royalty Corp. | 471M |

| enCore Energy Corp. | 464M |

Denison Mines Corp. ranks 6th among its competitors with a market cap about 8.78% that of the leader, Cameco Corporation. The company is positioned below the average market cap of the top 10 competitors (6.35B) but remains above the sector median of 2.92B. Denison Mines is closely trailing Energy Fuels Inc. by approximately 1.41%, highlighting a narrow gap to its nearest competitor above.

Does DNN have a competitive advantage?

Denison Mines Corp. does not present a competitive advantage as it consistently shows unfavorable profitability metrics and a return on invested capital (ROIC) below its cost of capital, indicating value destruction. The company’s financial performance from 2020 to 2024 reflects negative margins and a declining income statement overall.

Looking ahead, Denison Mines benefits from its flagship Wheeler River uranium project in Canada’s Athabasca Basin, which may offer growth opportunities in the uranium sector. However, current financial indicators suggest ongoing challenges in translating these prospects into profitable returns.

Comparisons with competitors

Check out how we compare the company to its competitors:

SWOT Analysis

This SWOT analysis highlights Denison Mines Corp.’s key internal and external factors to inform strategic investment decisions.

Strengths

- strong uranium asset base

- low debt levels

- experienced management team

Weaknesses

- negative profitability margins

- declining long-term revenue

- weak financial ratios

Opportunities

- rising global uranium demand

- potential expansion in Athabasca Basin

- favourable energy transition trends

Threats

- uranium price volatility

- regulatory risks in mining

- financial distress risk indicated by Altman Z-Score

Denison Mines shows solid asset positioning and a clean balance sheet but struggles with profitability and financial performance. The company’s future relies on uranium market recovery and effective cost control to mitigate bankruptcy risk and capitalize on growth opportunities.

Stock Price Action Analysis

The weekly stock chart below illustrates Denison Mines Corp. (DNN) price movement and volatility over the past 12 months:

Trend Analysis

Over the past 12 months, Denison Mines Corp. stock price increased by 103.12%, indicating a bullish trend with clear acceleration. The price ranged from a low of 1.19 to a high of 3.9, with a moderate volatility level reflected by a standard deviation of 0.51. Recent months continue this upward momentum.

Volume Analysis

In the last three months, trading volume has been increasing, with buyers accounting for 52.76% of activity, showing neutral buyer behavior. This balanced participation suggests cautious optimism among investors, with neither side strongly dominating, reflecting moderate market engagement.

Target Prices

The consensus target price for Denison Mines Corp. reflects a unified outlook among analysts.

| Target High | Target Low | Consensus |

|---|---|---|

| 2.6 | 2.6 | 2.6 |

Analysts expect Denison Mines to trade around 2.6, indicating a stable price expectation with limited variance.

Analyst & Consumer Opinions

This section examines recent grades and consumer feedback related to Denison Mines Corp. (DNN) to provide balanced insights.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Stock Grades

Here is the latest available grading overview for Denison Mines Corp., reflecting recent analyst evaluations:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Roth MKM | Maintain | Buy | 2024-10-23 |

| TD Securities | Maintain | Speculative Buy | 2023-06-27 |

| Raymond James | Maintain | Outperform | 2023-06-27 |

| TD Securities | Maintain | Speculative Buy | 2023-06-26 |

| Raymond James | Maintain | Outperform | 2023-06-26 |

| Credit Suisse | Downgrade | Underperform | 2017-07-18 |

| Credit Suisse | Downgrade | Underperform | 2017-07-17 |

| Roth Capital | Maintain | Buy | 2016-02-10 |

| Credit Suisse | Upgrade | Neutral | 2014-04-01 |

| Credit Suisse | Upgrade | Neutral | 2014-03-31 |

The consensus rating remains a Buy, supported by seven buy recommendations and one sell from recognized firms. Recent grades predominantly maintain positive stances, while earlier years show some downgrades, indicating a generally favorable but cautiously monitored outlook.

Consumer Opinions

Consumer sentiment around Denison Mines Corp. (DNN) reveals a mix of optimism about its growth potential and concerns about market volatility.

| Positive Reviews | Negative Reviews |

|---|---|

| Strong potential in uranium market growth | Stock price volatility causes uncertainty |

| Solid management team with clear strategy | Limited dividend payouts for investors |

| Commitment to sustainable mining practices | Exposure to regulatory risks |

| Good transparency in financial reporting | Slow progress on some exploration projects |

Overall, consumers appreciate Denison Mines’ strategic focus and sustainability efforts. However, they remain cautious due to market fluctuations and regulatory challenges impacting the mining sector.

Risk Analysis

Below is a summary table highlighting key risk categories, their descriptions, probabilities, and potential impacts for Denison Mines Corp.:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Financial Risk | Negative net margin (-2265%) and poor returns (ROE -16.15%) indicate weak profitability. | High | High |

| Bankruptcy Risk | Altman Z-Score of 1.03 places the company in the distress zone, signaling bankruptcy risk. | Moderate | Very High |

| Market Volatility | Beta of 1.89 shows stock price is more volatile than the market, increasing investment risk. | High | Medium |

| Liquidity Risk | Current ratio 3.65 but unfavorable interest coverage (-849) suggests cash flow issues. | Moderate | High |

| Sector Risk | Uranium industry exposure involves regulatory and commodity price fluctuations. | High | Medium |

The most critical risks include the high probability of financial distress and bankruptcy, as shown by the Altman Z-Score and negative profitability metrics. Investors should carefully monitor liquidity and sector-specific volatility before investing in Denison Mines Corp.

Should You Buy Denison Mines Corp.?

Denison Mines Corp. appears to be in financial distress with a weak profitability profile and an unfavorable competitive moat suggesting value destruction. Despite a manageable leverage profile, its overall rating of C- could be seen as reflective of operational challenges and moderate financial health.

Strength & Efficiency Pillars

Denison Mines Corp. demonstrates pockets of financial resilience despite overall challenges. The company boasts a debt-to-equity ratio of 0, indicating an absence of leverage risk, and a quick ratio of 3.54, signaling strong short-term liquidity. Interest expense remains modest at 2.68% of revenue, which is favorable for maintaining operational flexibility. However, critical profitability metrics reveal significant underperformance: a net margin of -2264.95%, ROE at -16.15%, and ROIC at -10.03%, all well below the WACC of 12.76%, confirming that the company is currently a value destroyer rather than a creator.

Weaknesses and Drawbacks

Denison Mines faces substantial headwinds, reflected in its distressed Altman Z-score of 1.03, placing it in the bankruptcy risk “distress zone.” The valuation profile is stretched, with a price-to-book ratio of 4.09, signaling a premium relative to book value, which may not be justified given negative earnings. The current ratio sits at 3.65, which, while superficially strong, could indicate inefficient asset use. Market momentum is bullish overall but the company’s operational inefficiencies, including extremely negative margins and poor returns on capital, present significant risks that could pressure the stock if profitability does not improve.

Our Verdict about Denison Mines Corp.

Denison Mines Corp. presents an unfavorable long-term fundamental profile, characterized by financial distress and value destruction. Nonetheless, the stock exhibits a bullish overall trend with accelerating price gains and neutral recent buyer dominance. This suggests that while the company might appear to benefit from market momentum, fundamental weaknesses imply that investors could adopt a cautious stance, waiting for clearer signs of financial turnaround before committing to long-term exposure.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Here’s What National Bank Thinks About Denison Mines Corp (DNN) – Yahoo Finance (Jan 03, 2026)

- Denison Mines: De-Risking And The New Phoenix ISR Milestone – Seeking Alpha (Jan 22, 2026)

- Denison Mine (NYSEAMERICAN:DNN) Reaches New 52-Week High – Here’s Why – MarketBeat (Jan 22, 2026)

- Denison Reports Financial and Operational Results for Q3 2025, Including First Production from McClean North Uranium Mine – PR Newswire (Nov 06, 2025)

- Canaccord hikes Denison Mines (DNN) PT to C$5 on Phoenix Project construction readiness, strategic expansion – MSN (Jan 08, 2026)

For more information about Denison Mines Corp., please visit the official website: denisonmines.com