Home > Analyses > Technology > CrowdStrike Holdings, Inc.

CrowdStrike transforms cybersecurity by delivering cloud-native protection that safeguards millions of endpoints and workloads worldwide. Its Falcon platform redefines threat detection with real-time intelligence and seamless scalability. Known for pioneering Zero Trust identity solutions, CrowdStrike leads the software infrastructure sector with innovation and robust market influence. As cyber risks escalate, I question whether CrowdStrike’s growth trajectory and fundamentals continue to justify its lofty valuation and investor enthusiasm.

Table of contents

Business Model & Company Overview

CrowdStrike Holdings, Inc., founded in 2011 and headquartered in Austin, Texas, stands as a leader in the software infrastructure sector. It delivers a cohesive ecosystem of cloud-based protection across endpoints, cloud workloads, identity, and data. Its Falcon platform integrates threat intelligence, managed security, IT operations, threat hunting, and Zero Trust identity protection, creating a unified defense system.

The company’s revenue engine hinges on subscription sales of its Falcon platform and cloud modules, primarily through a direct sales force and channel partners. CrowdStrike commands a strategic footprint across the Americas, Europe, and Asia, capitalizing on global demand for cybersecurity. Its robust competitive advantage lies in its cloud-native architecture and comprehensive threat coverage, solidifying its economic moat in a rapidly evolving industry.

Financial Performance & Fundamental Metrics

I analyze CrowdStrike Holdings, Inc.’s income statement, key financial ratios, and dividend payout policy to assess its underlying financial health and growth potential.

Income Statement

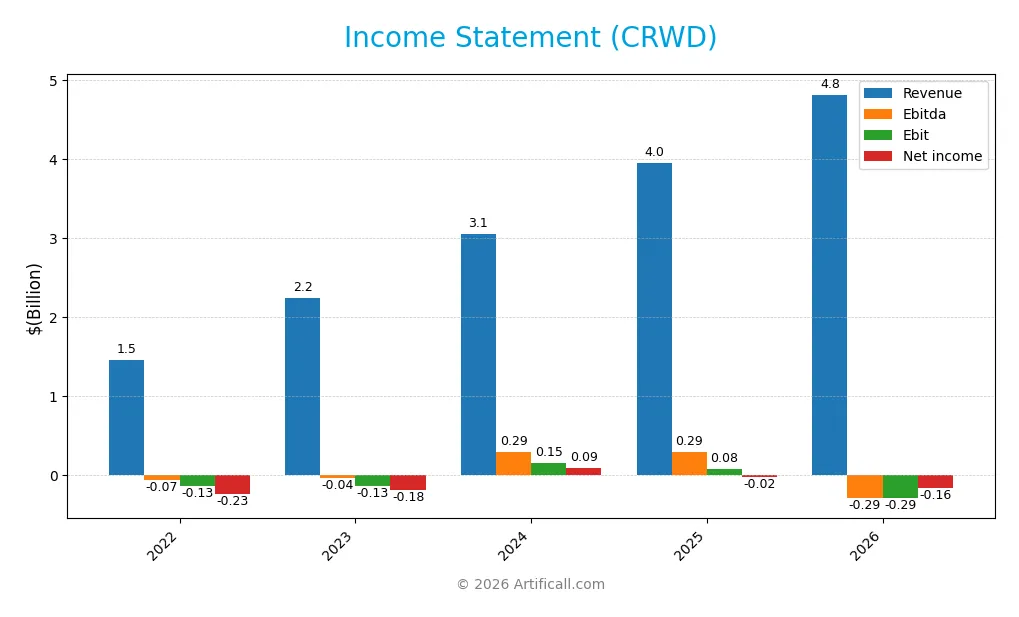

The table below summarizes CrowdStrike Holdings, Inc.’s income statement for fiscal years 2022 through 2026, showing key profitability and expense metrics.

| 2022 | 2023 | 2024 | 2025 | 2026 | |

|---|---|---|---|---|---|

| Revenue | 1.45B | 2.24B | 3.06B | 3.95B | 4.81B |

| Cost of Revenue | 383M | 601M | 756M | 991M | 1.22B |

| Operating Expenses | 1.21B | 1.83B | 2.30B | 3.08B | 3.89B |

| Gross Profit | 1.07B | 1.64B | 2.30B | 2.96B | 3.59B |

| EBITDA | -66M | -41M | 294M | 295M | -293M |

| EBIT | -135M | -135M | 149M | 81M | -293M |

| Interest Expense | 25M | 25M | 26M | 26M | 28M |

| Net Income | -235M | -183M | 89M | -19M | -161M |

| EPS | -1.02 | -0.78 | 0.37 | -0.08 | -0.65 |

| Filing Date | 2022-03-16 | 2023-03-09 | 2024-03-07 | 2025-03-10 | 2026-03-05 |

Income Statement Evolution

From 2022 to 2026, CrowdStrike’s revenue surged 231.5% to $4.8B, with gross profit growth closely tracking at 74.7% margin. However, operating and net margins remained negative in 2026, reflecting increased operating expenses aligned with revenue growth. Margins fluctuated but showed an overall improvement in net margin and EPS over the period.

Is the Income Statement Favorable?

In 2026, fundamentals were mixed. Revenue grew 21.7% year-over-year, supported by a strong 74.7% gross margin, indicating efficient core operations. Yet, EBIT and net income stayed negative at -6.1% and -3.35% margins, respectively, due to rising operating expenses. Interest expense remained low and favorable, but net losses and negative EPS highlight ongoing profitability challenges despite revenue momentum.

Financial Ratios

The table below summarizes key financial ratios for CrowdStrike Holdings, Inc. over the fiscal years 2022 to 2026, illustrating profitability, liquidity, leverage, and valuation metrics:

| Ratios | 2022 | 2023 | 2024 | 2025 | 2026 |

|---|---|---|---|---|---|

| Net Margin | -16% | -8% | 3% | 0% | -3% |

| ROE | -23% | -13% | 4% | -1% | -4% |

| ROIC | -6% | -6% | 0% | 1% | -4% |

| P/E | -175 | -135 | 781 | -5,056 | -692 |

| P/B | 40.0 | 16.9 | 30.3 | 29.7 | 25.2 |

| Current Ratio | 1.74 | 1.64 | 1.67 | 1.67 | 1.77 |

| Quick Ratio | 1.74 | 1.64 | 1.67 | 1.67 | 1.77 |

| D/E | 0.76 | 0.54 | 0.34 | 0.24 | 0.19 |

| Debt-to-Assets | 21% | 16% | 12% | 9% | 7% |

| Interest Coverage | -5.6 | -7.5 | -0.1 | -4.6 | 7.1 |

| Asset Turnover | 0.40 | 0.45 | 0.46 | 0.45 | 0.43 |

| Fixed Asset Turnover | 5.0 | 4.2 | 4.6 | 4.8 | 4.6 |

| Dividend Yield | 0% | 0% | 0% | 0% | 0% |

Evolution of Financial Ratios

Return on Equity (ROE) for CrowdStrike Holdings, Inc. deteriorated to -3.64% in 2026, reflecting declining profitability. The Current Ratio improved slightly to 1.77, signaling stable liquidity. The Debt-to-Equity Ratio decreased to 0.19, indicating reduced leverage and a stronger balance sheet. Overall, profitability weakened despite stable liquidity and lower leverage.

Are the Financial Ratios Favorable?

In 2026, profitability ratios like net margin (-3.35%) and ROE (-3.64%) remain unfavorable, signaling losses. Liquidity ratios, including current and quick ratios at 1.77, are favorable, showing good short-term financial health. Leverage metrics such as debt-to-equity (0.19) and debt-to-assets (7.4%) are also favorable. Asset turnover is weak at 0.43, while market valuation ratios like price-to-book (25.18) are unfavorable. Overall, the financial ratios present a slightly favorable profile with mixed signals.

Shareholder Return Policy

CrowdStrike Holdings, Inc. does not pay dividends, reflecting its negative net income and focus on reinvestment. The company does not engage in share buybacks either, prioritizing growth and capital allocation toward operating and free cash flow generation.

This approach supports long-term value creation by emphasizing cash flow and balance sheet strength over distributions. However, the absence of returns to shareholders may concern income-focused investors seeking immediate cash returns.

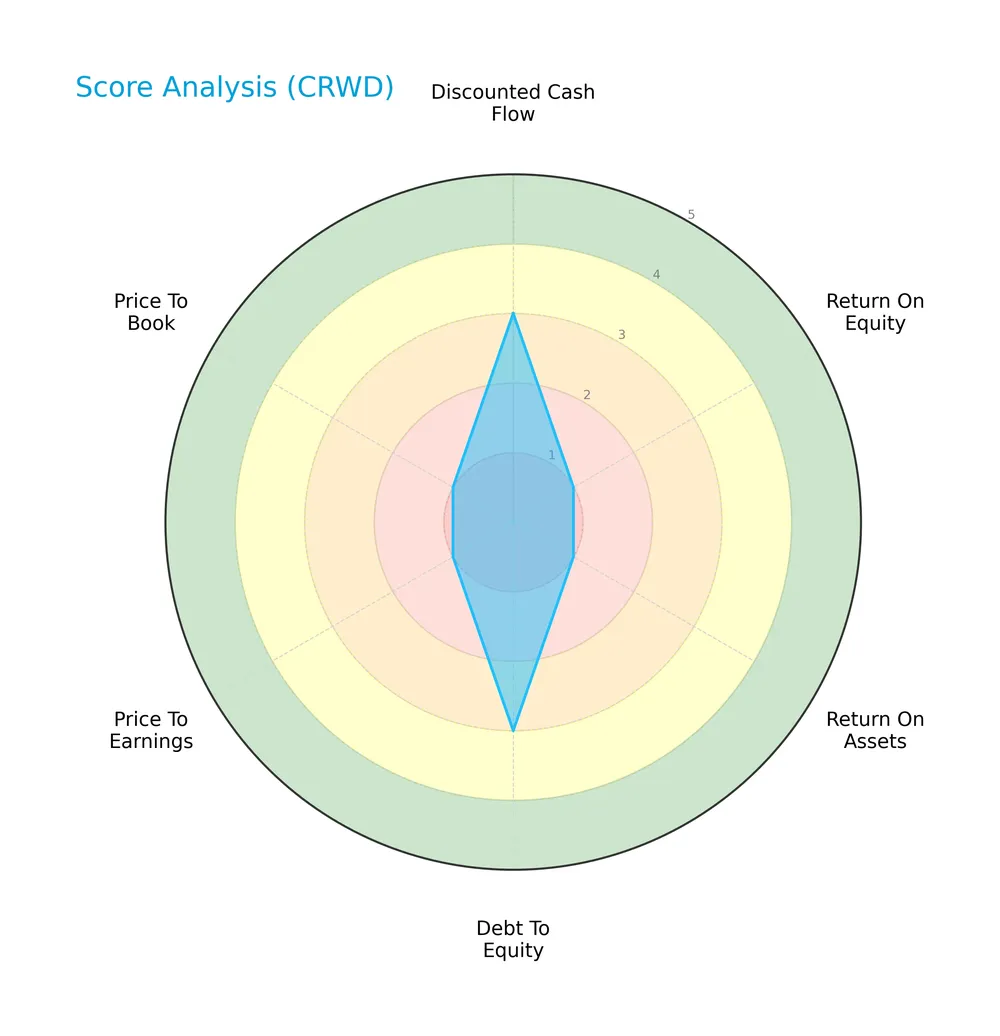

Score analysis

The radar chart below illustrates key financial ratios evaluating CrowdStrike Holdings, Inc.’s valuation, profitability, and leverage:

CrowdStrike scores moderately on discounted cash flow and debt-to-equity metrics. However, it shows very unfavorable returns on equity and assets, alongside weak price-to-earnings and price-to-book valuations.

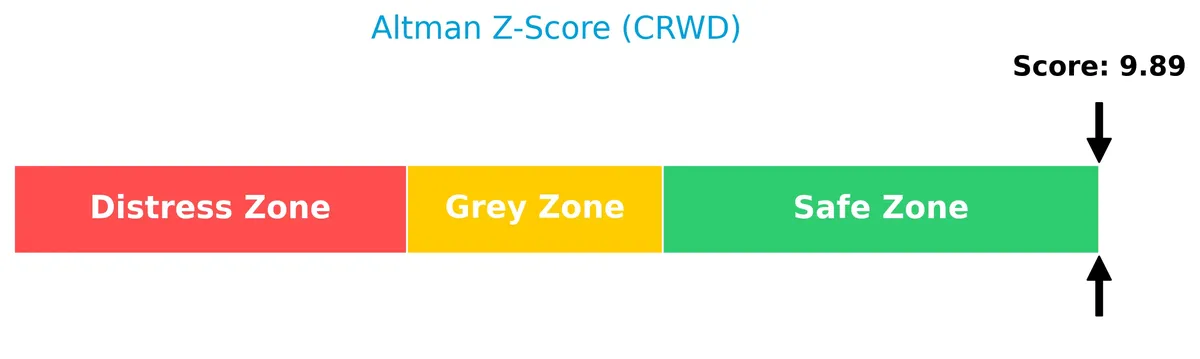

Analysis of the company’s bankruptcy risk

The Altman Z-Score places CrowdStrike well within the safe zone, indicating a low risk of bankruptcy based on its financial stability:

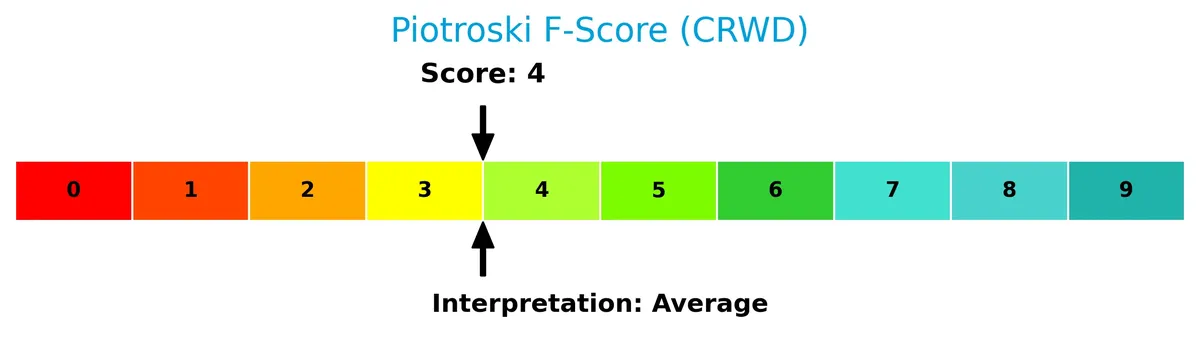

Is the company in good financial health?

The Piotroski Score diagram reflects an average financial health rating for CrowdStrike Holdings, Inc., suggesting moderate strength but room for improvement:

With a Piotroski Score of 4, the company demonstrates some positive financial attributes but lacks the robustness typical of strong investments.

Competitive Landscape & Sector Positioning

This section analyzes CrowdStrike Holdings, Inc.’s position within the software infrastructure sector. It examines strategic positioning, revenue segmentation, key products, and main competitors. I will assess whether CrowdStrike holds a competitive advantage over its peers.

Strategic Positioning

CrowdStrike concentrates its revenue largely on subscription services, exceeding $4.5B in 2026, with professional services under $250M. Geographically, the company is heavily US-focused, generating $3.2B, though it steadily expands in EMEA and Asia Pacific regions.

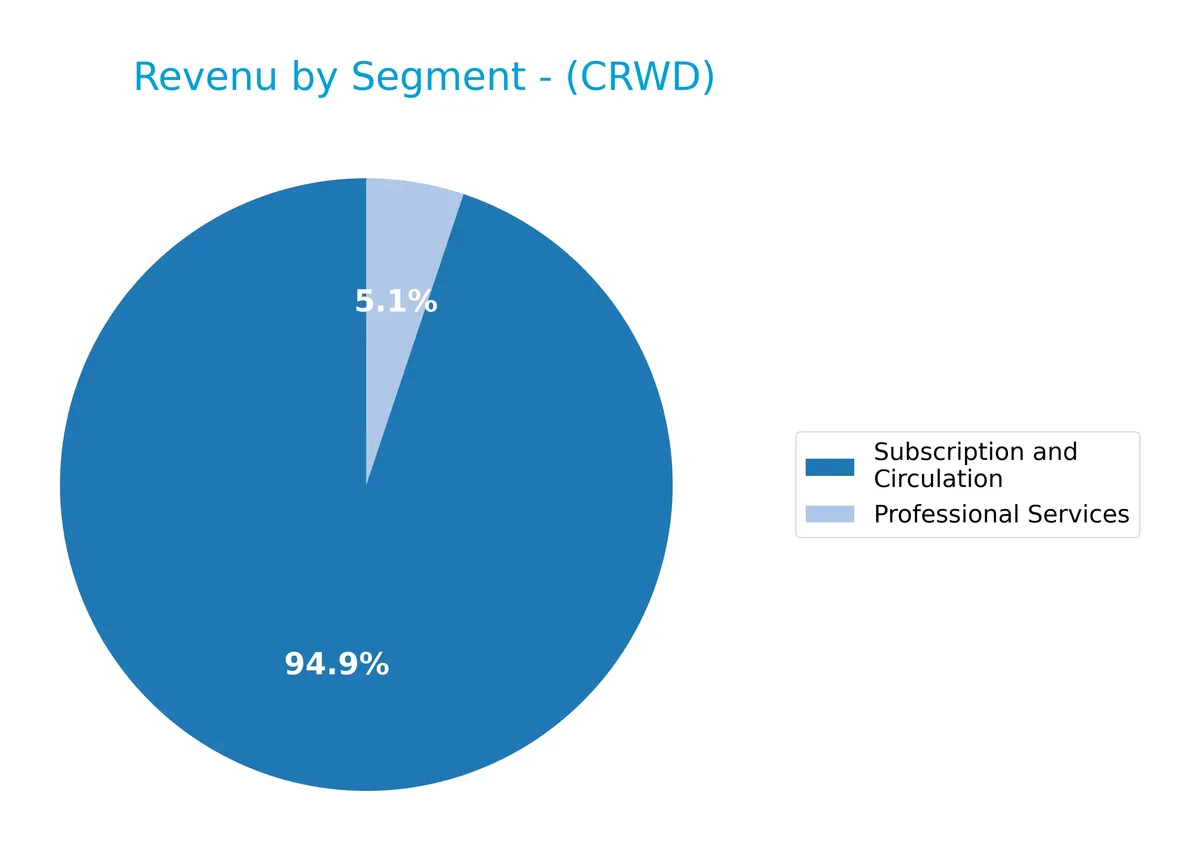

Revenue by Segment

This pie chart illustrates CrowdStrike Holdings’ revenue distribution by segment for fiscal year 2026, highlighting the contributions of subscription services versus professional services.

Subscription and Circulation dominates CrowdStrike’s revenue, reaching $4.56B in 2026, reflecting rapid annual growth and solidifying its role as the core business driver. Professional Services, while much smaller at $247M, shows steady expansion but remains a supplementary revenue source. The increasing concentration in subscriptions underscores CrowdStrike’s successful shift toward a recurring revenue model, though investors should watch for dependency risks.

Key Products & Brands

Below is a summary of CrowdStrike Holdings, Inc.’s principal products and brands with their descriptions:

| Product | Description |

|---|---|

| Falcon Platform Subscriptions | Cloud-delivered protection across endpoints, cloud workloads, identity, and data, sold via subscriptions. |

| Professional Services | Consulting and support services complementing the Falcon platform offerings. |

CrowdStrike’s revenue predominantly comes from subscriptions to its Falcon platform, reflecting strong recurring demand. Professional services form a smaller, yet growing segment, enhancing customer integration and support.

Main Competitors

The Technology sector includes 32 competitors, with the table below listing the top 10 leaders by market capitalization:

| Competitor | Market Cap. |

|---|---|

| Microsoft Corporation | 3.52T |

| Oracle Corporation | 553B |

| Palantir Technologies Inc. | 383B |

| Adobe Inc. | 140B |

| Palo Alto Networks, Inc. | 120B |

| CrowdStrike Holdings, Inc. | 113B |

| Synopsys, Inc. | 92B |

| Cloudflare, Inc. | 69B |

| Fortinet, Inc. | 59B |

| Block, Inc. | 40B |

CrowdStrike ranks 6th among 32 competitors, holding about 3.0% of the market cap of the leader, Microsoft. The company sits below the average market cap of the top 10 (508B) but remains above the sector median (18.8B). CrowdStrike maintains a 13% market cap gap from its closest competitor above, illustrating a moderate lead in this mid-tier position.

Comparisons with competitors

Check out how we compare the company to its competitors:

Does CrowdStrike Holdings have a competitive advantage?

CrowdStrike shows a slightly unfavorable competitive advantage as its ROIC lags 13% below WACC, indicating value destruction despite growing profitability. Its 75% gross margin confirms solid core product economics but operating losses weigh on overall returns.

Looking ahead, expanding international revenues, especially in Asia Pacific and EMEA, and broadening its cloud-delivered security modules offer meaningful growth opportunities. Successful capital allocation will be critical to convert these into sustained value creation.

SWOT Analysis

This SWOT analysis highlights CrowdStrike’s key internal and external factors to guide strategic decisions.

Strengths

- Strong revenue growth of 21.7% in 2026

- High gross margin at 74.7%

- Robust current and quick ratios at 1.77

Weaknesses

- Negative net margin of -3.35%

- ROIC below WACC, indicating value destruction

- High price-to-book ratio at 25.18 signals overvaluation

Opportunities

- Expanding global footprint, especially in Asia Pacific and EMEA

- Growing demand for cloud-delivered cybersecurity

- Opportunity to improve profitability through cost control

Threats

- Intense competition in cybersecurity sector

- Rapid technology changes require constant innovation

- Macroeconomic uncertainties impacting IT budgets

CrowdStrike’s strengths lie in rapid top-line growth and strong liquidity, crucial in this high-growth tech sector. However, persistent unprofitability and valuation concerns warrant caution. The company must leverage market expansion while tightening cost discipline to convert growth into sustainable profits.

Stock Price Action Analysis

The weekly stock chart for CrowdStrike Holdings, Inc. displays significant movement over the past 100 weeks, highlighting key price levels and trend shifts:

Trend Analysis

Over the past 12 months, CRWD’s stock price increased 35.86%, indicating a bullish trend. The highest price reached 543.01, the lowest was 217.89. Despite strong gains, the trend shows deceleration. Volatility is high, with a standard deviation of 78.77.

Volume Analysis

In the last three months, trading volume is decreasing overall. Seller dominance prevails with 73.2% of volume, reflecting bearish pressure. This suggests cautious investor sentiment and reduced market participation during this period.

Target Prices

The consensus target price for CrowdStrike Holdings, Inc. reflects strong analyst confidence in its growth trajectory.

| Target Low | Target High | Consensus |

|---|---|---|

| 368 | 706 | 535 |

Analysts expect CrowdStrike’s shares to appreciate significantly, with a broad range reflecting optimism tempered by market uncertainties.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

Analyst & Consumer Opinions

I will analyze CrowdStrike Holdings, Inc.’s recent analyst grades alongside consumer feedback to present a balanced perspective.

Stock Grades

Here are the latest verified analyst grades for CrowdStrike Holdings, Inc. as of early 2026:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Bernstein | Maintain | Market Perform | 2026-03-04 |

| Morgan Stanley | Maintain | Equal Weight | 2026-03-04 |

| Needham | Maintain | Buy | 2026-03-04 |

| Cantor Fitzgerald | Maintain | Overweight | 2026-03-04 |

| Rosenblatt | Maintain | Buy | 2026-03-04 |

| DA Davidson | Maintain | Buy | 2026-03-04 |

| Evercore ISI Group | Maintain | In Line | 2026-03-04 |

| Macquarie | Maintain | Neutral | 2026-03-04 |

| BNP Paribas | Maintain | Neutral | 2026-03-04 |

| BMO Capital | Maintain | Outperform | 2026-03-04 |

Most analysts maintain a positive stance, with a strong bias toward buy and outperform ratings. The consensus favors moderate optimism, reflecting confidence without exuberance.

Consumer Opinions

CrowdStrike commands strong consumer admiration, but not without some friction points.

| Positive Reviews | Negative Reviews |

|---|---|

| “Exceptional threat detection and fast response times.” | “Pricing feels steep for small businesses.” |

| “User-friendly interface simplifies complex security tasks.” | “Occasional false positives disrupt workflow.” |

| “Reliable cloud-based platform with excellent uptime.” | “Customer support can be slow during peak hours.” |

Overall, users praise CrowdStrike’s advanced protection and intuitive design. However, cost concerns and sporadic service issues temper enthusiasm. These highlight areas for potential improvement in customer experience.

Risk Analysis

Below is a summary table of key risks facing CrowdStrike Holdings, Inc. as of 2026, highlighting likelihood and potential impact:

| Category | Description | Probability | Impact |

|---|---|---|---|

| Profitability | Negative net margin (-3.35%) signals ongoing losses | High | High |

| Return on Capital | ROIC at -4.24% below WACC (8.94%) indicates value destruction | High | High |

| Valuation | Extremely high P/B ratio (25.18) suggests overvaluation | Moderate | Medium |

| Market Volatility | Beta of 1.124 implies above-market price swings | Moderate | Medium |

| Dividend Policy | Zero dividend yield limits income potential | Low | Low |

| Financial Health | Altman Z-Score near 9.9 shows very low bankruptcy risk | Low | Low |

| Financial Strength | Piotroski Score of 4 indicates average financial health | Moderate | Medium |

Profitability and capital efficiency risks dominate. Negative margins and ROIC below WACC highlight challenges in generating returns above cost of capital. Despite a strong balance sheet (Altman Z-Score), high valuation multiples elevate downside risk if growth falters. Investors must weigh growth potential against fundamental weaknesses and market sensitivity.

Should You Buy CrowdStrike Holdings, Inc.?

CrowdStrike appears to be shedding value despite improving profitability, suggesting operational efficiency gains. Its leverage profile seems moderate, yet the overall rating stands at C, reflecting a slightly unfavorable moat and average financial strength.

Strength & Efficiency Pillars

CrowdStrike Holdings, Inc. exhibits strong operational efficiency with a robust gross margin of 74.67%. Despite unfavorable net margin (-3.35%), the company maintains a safe financial footing, reflected by an Altman Z-Score of 9.89 in the safe zone. Its return on invested capital (ROIC) is -4.24%, below the weighted average cost of capital (WACC) at 8.94%, indicating value destruction. However, the growing ROIC trend suggests improving profitability, signaling potential operational progress.

Weaknesses and Drawbacks

CrowdStrike faces valuation challenges, with a very high price-to-book ratio of 25.18 signaling an expensive premium. The negative return on equity (-3.64%) and asset turnover of 0.43 highlight inefficiencies in capital use. While debt levels remain moderate (debt-to-equity at 0.19) and liquidity is solid (current ratio 1.77), the recent seller dominance (buyer dominance at 26.8%) pressures the stock, raising short-term volatility risks. These factors suggest investor caution despite operational strengths.

Our Final Verdict about CrowdStrike Holdings, Inc.

The company’s safe solvency profile and improving profitability indicate a fundamentally sound business. Despite a bullish long-term trend, recent seller dominance suggests a wait-and-see approach for a better entry point. CrowdStrike’s profile might appeal to investors seeking growth exposure but could require patience amid near-term market pressure and valuation concerns.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or other professional advice. Investing in financial markets involves a significant risk of loss, and past performance is not indicative of future results.

Additional Resources

- Analysts see tailwinds from AI after CrowdStrike’s ‘solid’ Q4, outlook – Seeking Alpha (Mar 04, 2026)

- What’s Going On With CrowdStrike Stock Thursday? – CrowdStrike Holdings (NASDAQ:CRWD) – Benzinga (Mar 05, 2026)

- Cybersecurity firm CrowdStrike tops $5.25B in recurring revenue after record year – Stock Titan (Mar 03, 2026)

- 10 Stocks That Could Skyrocket in 2026 – Insider Monkey (Mar 03, 2026)

- CrowdStrike in focus as Citi reiterates Buy rating after results (CRWD:NASDAQ) – Seeking Alpha (Mar 05, 2026)

For more information about CrowdStrike Holdings, Inc., please visit the official website: crowdstrike.com