Home > Comparison > Technology > TER vs CMCO

The strategic rivalry between Teradyne, Inc. and Columbus McKinnon Corporation shapes dynamics in their respective sectors. Teradyne, a Technology leader in semiconductor and automation testing, contrasts sharply with Columbus McKinnon, an Industrials specialist in intelligent motion and material handling solutions. This analysis pits cutting-edge tech manufacturing against robust industrial engineering to identify which trajectory delivers superior risk-adjusted returns for diversified portfolios in volatile markets.

Table of contents

Companies Overview

Teradyne, Inc. and Columbus McKinnon Corporation both hold pivotal roles in their respective industrial and technology markets.

Teradyne, Inc.: Semiconductor & Automation Powerhouse

Teradyne dominates the semiconductor test equipment industry, generating revenue from wafer and device-level testing for automotive, communication, and consumer sectors. Its strategic thrust in 2026 focuses on expanding industrial automation and wireless test solutions, leveraging platforms like FLEX and IQxel to support evolving technologies including 5G and IoT devices.

Columbus McKinnon Corporation: Motion Solutions Specialist

Columbus McKinnon leads in intelligent motion and material handling solutions, offering hoists, crane systems, and automation to diverse sectors such as construction, energy, and e-commerce. In 2026, it emphasizes power and motion technology innovations, scaling automation and diagnostics capabilities to enhance ergonomic and safety features across its product lines.

Strategic Collision: Similarities & Divergences

Teradyne pursues a high-tech, innovation-driven model focused on semiconductor testing and automation, while Columbus McKinnon emphasizes mechanical and electromechanical motion solutions. Their primary battleground lies in industrial automation, but Teradyne’s advanced robotics contrast with Columbus McKinnon’s heavy machinery focus. This divergence creates distinctly different investment profiles rooted in technology intensity versus industrial legacy.

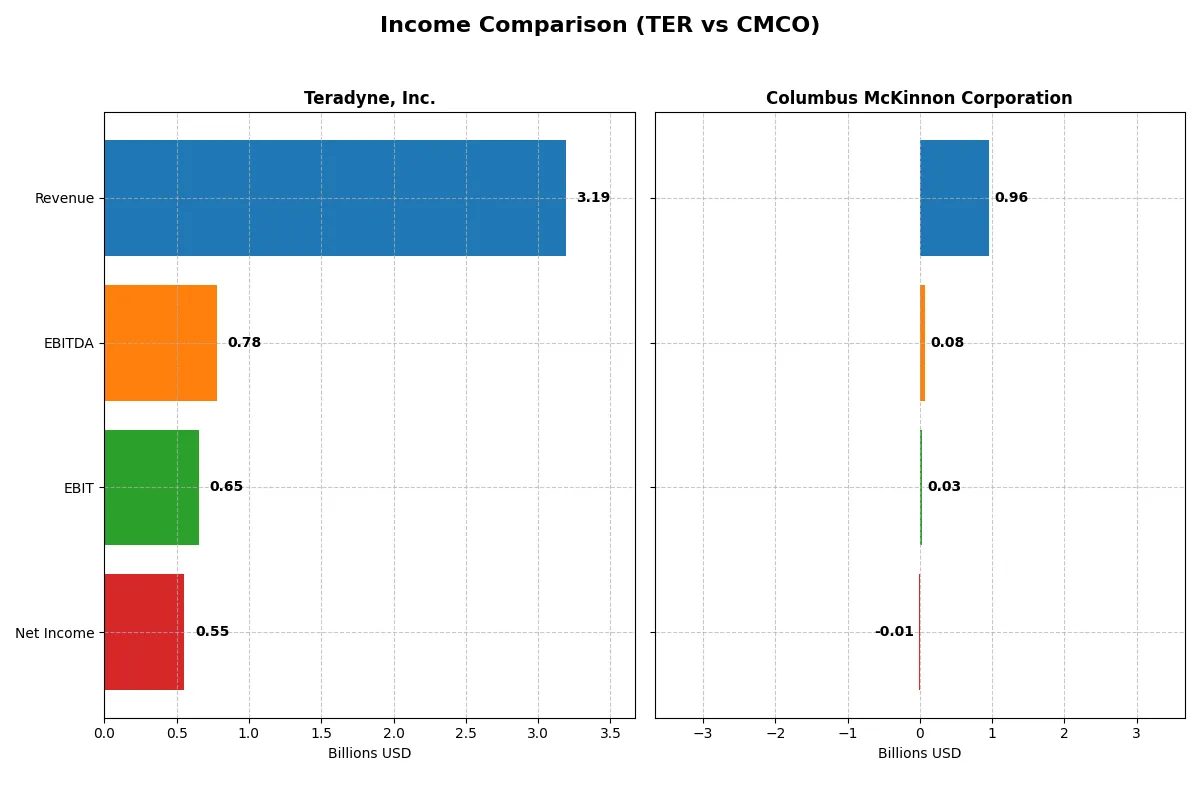

Income Statement Comparison

The following data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Teradyne, Inc. (TER) | Columbus McKinnon Corporation (CMCO) |

|---|---|---|

| Revenue | 3.19B | 963M |

| Cost of Revenue | 1.32B | 637M |

| Operating Expenses | 1.17B | 271M |

| Gross Profit | 1.87B | 326M |

| EBITDA | 780M | 75M |

| EBIT | 653M | 27M |

| Interest Expense | 8M | 32M |

| Net Income | 554M | -5M |

| EPS | 3.49 | -0.18 |

| Fiscal Year | 2025 | 2024 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals the true efficiency and profitability of each company’s core business engine over recent years.

Teradyne, Inc. Analysis

Teradyne’s revenue grew steadily to $3.19B in 2025, with net income at $554M. Its gross margin remains robust at 58.55%, showing strong cost control. Despite a slight net margin dip, Teradyne sustains favorable EBIT and EPS growth, signaling efficient operations and resilient momentum entering 2026.

Columbus McKinnon Corporation Analysis

Columbus McKinnon posted $963M revenue in 2024, down 5% year over year, with a net loss of $5.1M. Its gross margin at 33.82% is moderate, but EBIT margin is only 2.8%, reflecting operational pressure. The company faces declining profitability and negative earnings growth, indicating challenges in sustaining financial efficiency.

Margin Strength vs. Profitability Struggles

Teradyne leads with superior margin health and consistent profit growth, while Columbus McKinnon battles shrinking net income and margins. Teradyne’s profile appeals to investors valuing operational excellence and stable returns. Columbus McKinnon’s weaker income metrics suggest higher risk and a need for strategic turnaround.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Teradyne, Inc. (TER) | Columbus McKinnon Corporation (CMCO) |

|---|---|---|

| ROE | 19.8% | -0.6% |

| ROIC | 18.4% | 3.3% |

| P/E | 54.6 | -94.7 |

| P/B | 10.8 | 0.55 |

| Current Ratio | 1.76 | 1.81 |

| Quick Ratio | 1.41 | 1.04 |

| D/E (Debt-to-Equity) | 0.12 | 0.61 |

| Debt-to-Assets | 8.3% | 31.1% |

| Interest Coverage | 86.4 | 1.68 |

| Asset Turnover | 0.76 | 0.55 |

| Fixed Asset Turnover | 4.99 | 9.07 |

| Payout Ratio | 13.8% | -156.5% |

| Dividend Yield | 0.25% | 1.65% |

| Fiscal Year | 2025 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as the company’s DNA, exposing hidden risks and operational excellence crucial for informed investment decisions.

Teradyne, Inc.

Teradyne delivers strong profitability with ROE near 20% and net margin at 17.4%, signaling operational efficiency. However, its valuation appears stretched, with a P/E of 54.6 and P/B above 10. The modest 0.25% dividend yield contrasts with significant reinvestment in R&D, supporting long-term growth potential.

Columbus McKinnon Corporation

Columbus McKinnon struggles with negative net margin and ROE, reflecting weak profitability. Yet, the stock trades attractively at a P/B of 0.55 and a negative P/E, implying undervaluation. The company maintains a 1.65% dividend yield despite challenges, balancing shareholder returns amid operational headwinds.

Operational Strength vs. Value Opportunity

Teradyne’s superior profitability and solid reinvestment strategy come at a premium valuation, increasing risk. Columbus McKinnon presents value through low multiples but faces profitability and coverage concerns. Investors prioritizing growth may lean toward Teradyne, while value seekers might find Columbus McKinnon’s profile more fitting.

Which one offers the Superior Shareholder Reward?

I observe Teradyne, Inc. (TER) delivers a modest dividend yield near 0.38% with a sustainable payout ratio around 14%, backed by strong free cash flow coverage above 66%. TER pairs this with steady buybacks, reinforcing capital return. Columbus McKinnon Corporation (CMCO) offers a higher dividend yield near 1.65%, but its payout ratio is negative due to net losses, signaling risk to dividend sustainability. CMCO’s buyback activity is limited amid financial leverage and weak cash flow metrics. Historically, I’ve found that consistent free cash flow coverage and manageable payout ratios, like TER’s, better support long-term shareholder returns. Thus, TER provides a superior total return profile in 2026.

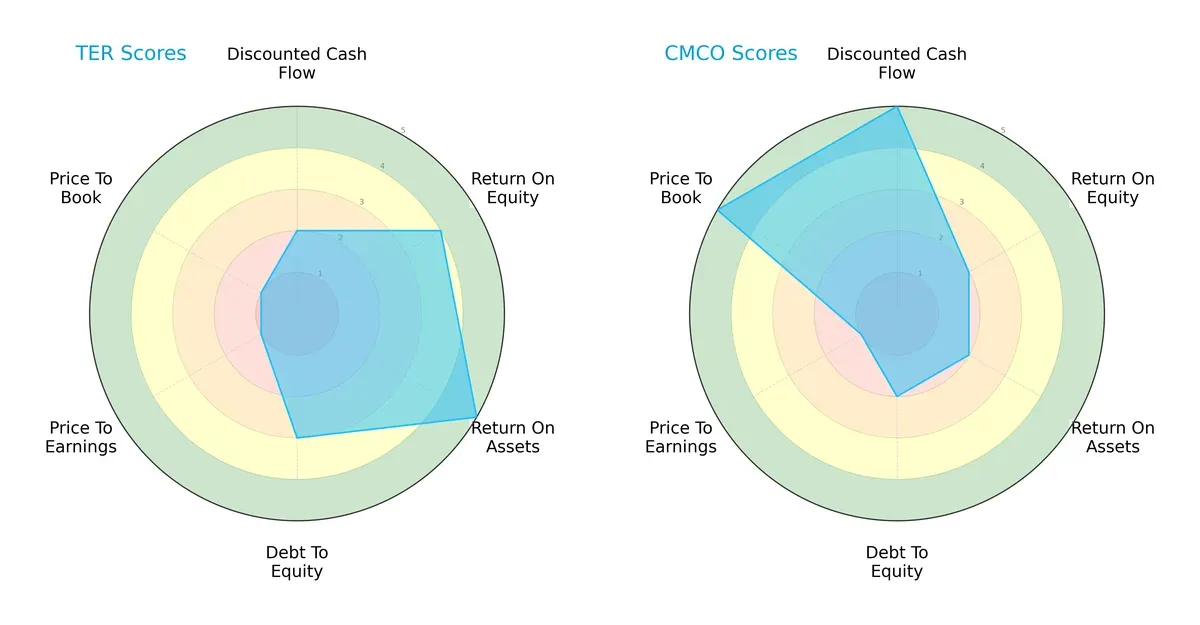

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Teradyne, Inc. and Columbus McKinnon Corporation:

Teradyne excels in asset utilization (ROA 5) and equity returns (ROE 4), showing operational strength. Columbus McKinnon leads in discounted cash flow (DCF 5) and price-to-book valuation (P/B 5), indicating potential undervaluation but weaker profitability (ROE 2, ROA 2). Teradyne presents a more balanced profile, while Columbus McKinnon relies heavily on valuation advantages.

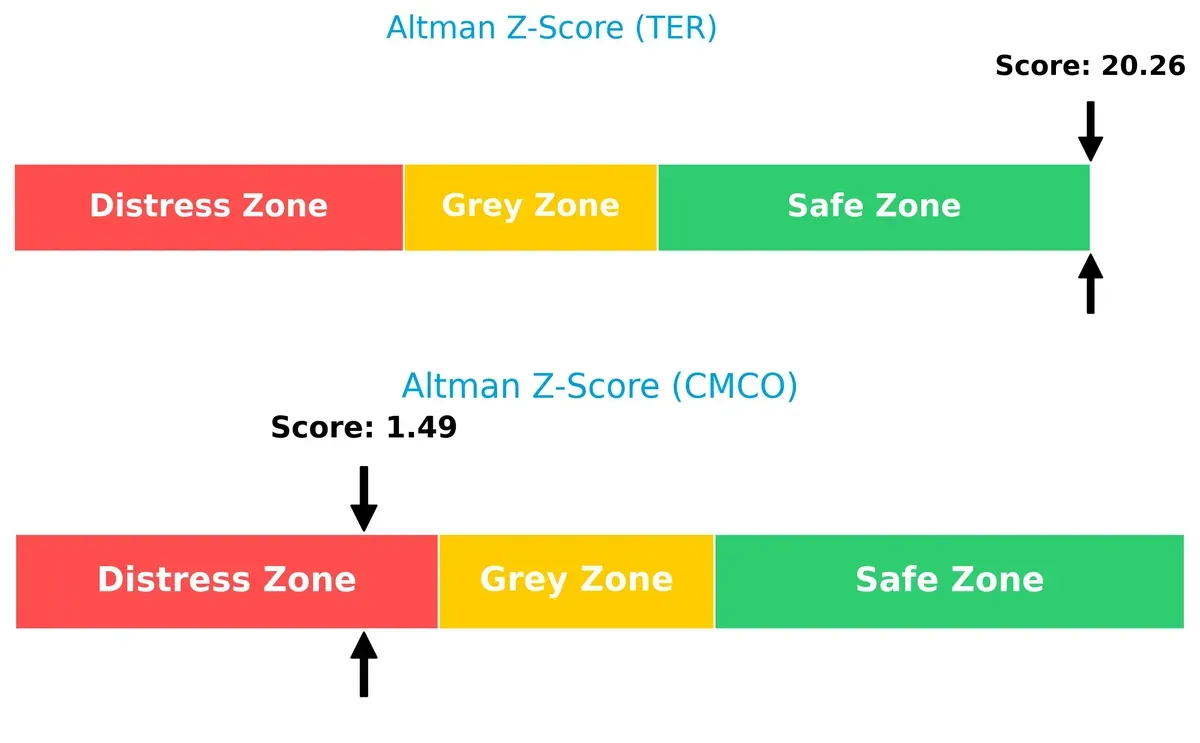

Bankruptcy Risk: Solvency Showdown

Teradyne’s Altman Z-Score of 20.3 places it deep in the safe zone, signaling robust long-term survival. Columbus McKinnon’s 1.49 score flags distress risk, indicating financial vulnerability in this cycle:

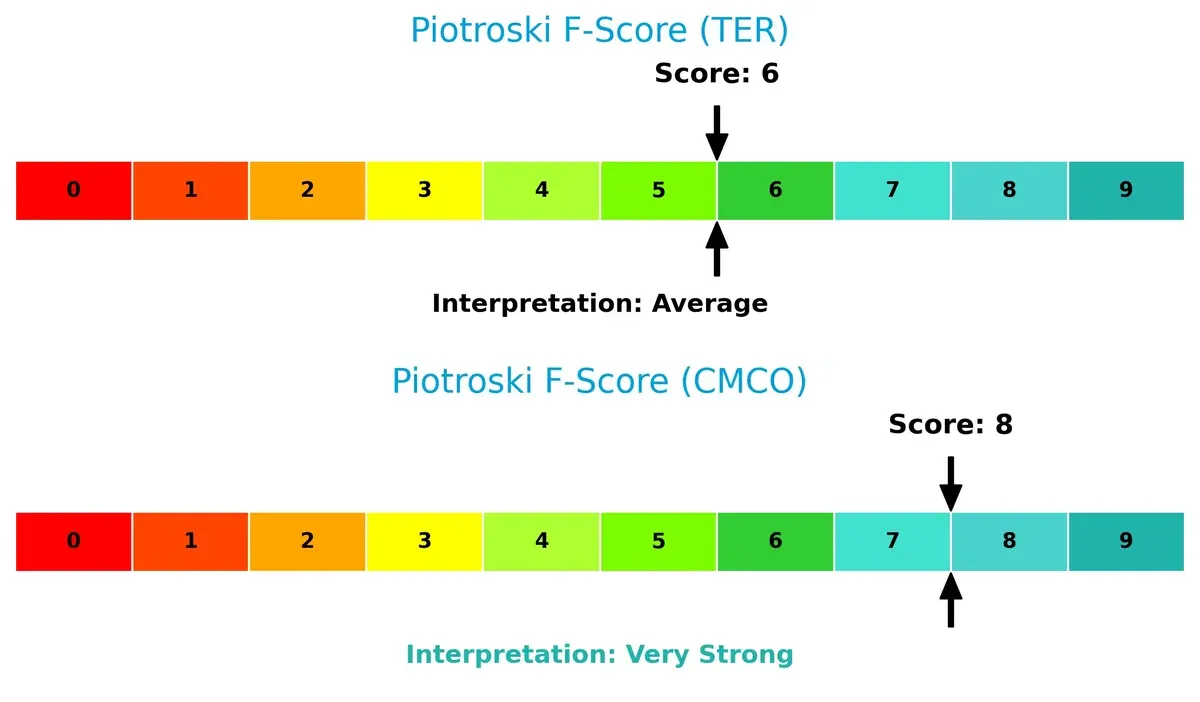

Financial Health: Quality of Operations

Columbus McKinnon scores an 8 on the Piotroski F-Score, reflecting very strong financial health. Teradyne’s 6 is average, suggesting some operational caution but no immediate red flags:

How are the two companies positioned?

This section dissects Teradyne and Columbus McKinnon’s operational DNA by comparing revenue distribution and internal strengths and weaknesses. The goal is to confront their economic moats to identify which model offers the most resilient competitive advantage today.

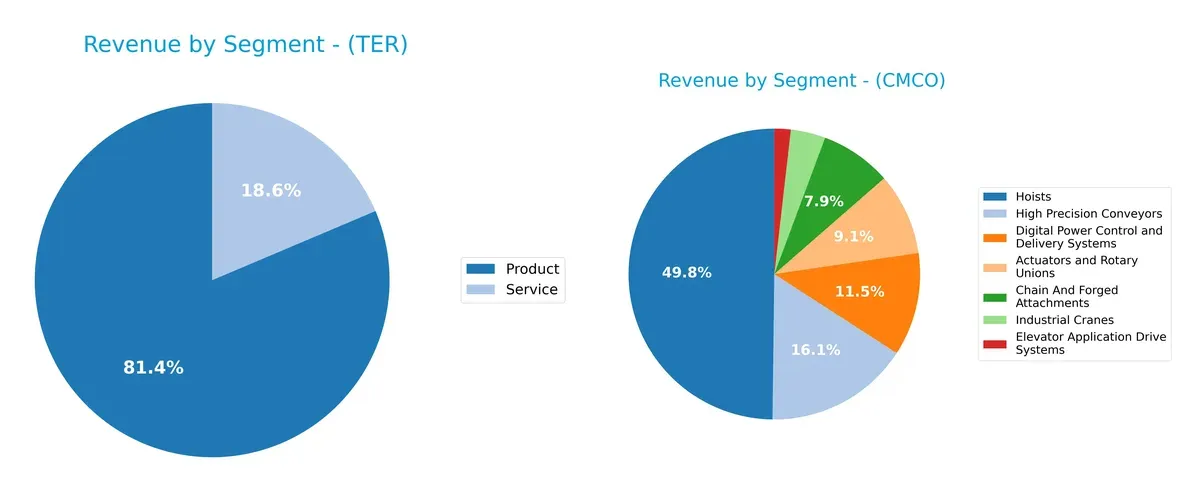

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Teradyne, Inc. and Columbus McKinnon Corporation diversify their income streams and where their primary sector bets lie:

Teradyne anchors revenue heavily in Products, with $2.3B in 2024, complemented by $525M in Services, showing moderate diversification. Columbus McKinnon spreads revenue more evenly across Hoists ($480M), High Precision Conveyors ($155M), and Digital Power Control ($110M), signaling broader industrial reach. Teradyne’s concentration on products suggests strong infrastructure dominance but also concentration risk. Columbus McKinnon’s mix reduces dependency on any single segment, enhancing resilience.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Teradyne and Columbus McKinnon based on diversification, profitability, financials, innovation, global presence, and market share:

Teradyne Strengths

- Strong profitability with 17.37% net margin and 19.82% ROE

- Favorable liquidity ratios (current 1.76, quick 1.41)

- Low leverage with debt to assets at 8.32%

- Innovation reflected in product and service revenue streams

- Broad global presence including Asia and Americas

- Solid market positions in semiconductor test and automation

Columbus McKinnon Strengths

- Favorable WACC at 7.61% supports capital efficiency

- Reasonable valuation metrics (PE negative but favorable, PB 0.55)

- Diversified product lines including hoists, conveyors, and cranes

- Stable liquidity (current ratio 1.81)

- Strong presence in US and Europe with notable German market share

- High fixed asset turnover at 9.07 indicates asset utilization

Teradyne Weaknesses

- High valuation multiples (PE 54.64, PB 10.83) may pressure returns

- WACC at 12.29% exceeds ROIC, reducing value creation

- Dividend yield very low at 0.25%

- Moderate asset turnover at 0.76 suggests room for efficiency gains

Columbus McKinnon Weaknesses

- Negative profitability metrics with net margin -0.53% and ROE -0.58%

- Weak interest coverage at 0.83 signals financial risk

- Higher leverage with debt to assets at 31.09%

- Lower ROIC at 3.3% versus WACC, indicating limited value generation

- Asset turnover lower at 0.55 despite high fixed asset turnover

- Dividend yield neutral at 1.65%, not a strong income source

Teradyne’s strengths lie in profitability, low leverage, and global diversification, though its high valuation and cost of capital may limit upside. Columbus McKinnon shows operational diversity and asset efficiency but struggles with profitability and financial risk, impacting its capital allocation strategy.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat protects long-term profits from competition’s relentless erosion by sustaining economic advantages over time:

Teradyne, Inc.: Innovation-Driven Cost Advantage

Teradyne’s moat stems from advanced automation and testing tech. It translates into high ROIC (+6.16% vs. WACC) and stable margins near 20%. New robotics and wireless test segments promise deeper market entrenchment in 2026.

Columbus McKinnon Corporation: Legacy Brand with Narrow Operational Moat

Columbus McKinnon relies on entrenched customer relationships and specialized material handling products. However, its ROIC lags below WACC by 4.3%, signaling value destruction. Weak margin trends challenge future expansion despite steady industrial demand.

Innovation Leadership vs. Operational Legacy: The Competitive Moat Face-off

Teradyne’s wider, innovation-fueled moat outpaces Columbus McKinnon’s shrinking operational edge. Teradyne’s superior capital efficiency better equips it to defend and grow market share amidst intensifying technological disruption.

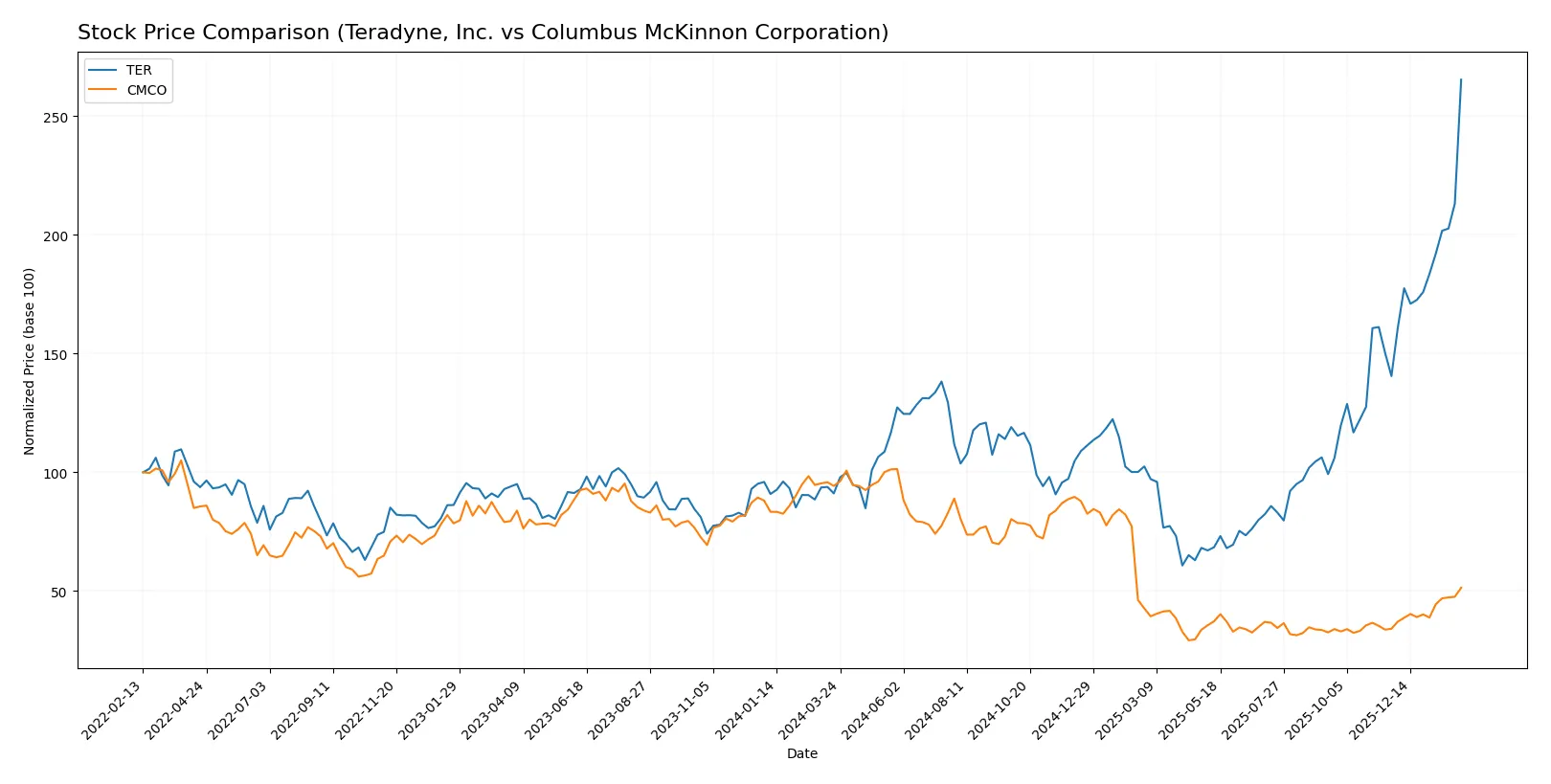

Which stock offers better returns?

Teradyne, Inc. displays a strong bullish trend with substantial price gains and accelerating momentum over the past year. Columbus McKinnon Corporation shows a pronounced bearish trend despite recent positive movement, reflecting a volatile trading dynamic.

Trend Comparison

Teradyne’s stock surged 191.2% over the past year, accelerating upward with a high volatility of 40.42, ranging from $68.72 to $300.11. Recent gains remain robust, up 88.86% with strong buyer dominance.

Columbus McKinnon’s stock declined 45.49% over the past year, showing accelerating losses despite a recent 50.53% recovery. Volatility remains moderate at 10.81, with prices between $12.96 and $44.90. Buyer dominance surged recently but with a shallow trend slope.

Teradyne has delivered significantly higher market performance than Columbus McKinnon, driven by strong price appreciation and accelerating investor demand.

Target Prices

Analysts present a mixed but defined outlook for Teradyne, Inc. and Columbus McKinnon Corporation.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Teradyne, Inc. | 175 | 335 | 276.08 |

| Columbus McKinnon Corporation | 15 | 15 | 15 |

Teradyne’s target consensus at 276.08 is slightly below its current price of 300.11, signaling cautious optimism. Columbus McKinnon’s consensus target at 15 is well below its current price of 22.76, indicating significant downside risk according to analysts.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Teradyne, Inc. Grades

Here are the latest grades issued by reputable financial institutions for Teradyne, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Goldman Sachs | Maintain | Buy | 2026-02-04 |

| Citigroup | Maintain | Buy | 2026-02-04 |

| Cantor Fitzgerald | Maintain | Overweight | 2026-02-04 |

| Evercore ISI Group | Maintain | Outperform | 2026-02-04 |

| Stifel | Maintain | Buy | 2026-02-04 |

| Evercore ISI Group | Maintain | Outperform | 2026-02-03 |

| Cantor Fitzgerald | Maintain | Overweight | 2026-02-02 |

| Stifel | Maintain | Buy | 2026-01-30 |

| UBS | Maintain | Buy | 2026-01-26 |

| B of A Securities | Maintain | Buy | 2026-01-22 |

Columbus McKinnon Corporation Grades

Here are the latest grades issued by reputable financial institutions for Columbus McKinnon Corporation:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| DA Davidson | Downgrade | Neutral | 2025-02-11 |

| DA Davidson | Maintain | Buy | 2024-02-05 |

| DA Davidson | Maintain | Buy | 2022-10-04 |

| DA Davidson | Maintain | Buy | 2022-10-03 |

| Barrington Research | Maintain | Outperform | 2022-07-29 |

| Barrington Research | Maintain | Outperform | 2022-07-28 |

| JP Morgan | Downgrade | Neutral | 2022-05-26 |

| Barrington Research | Maintain | Outperform | 2022-05-26 |

| Barrington Research | Maintain | Outperform | 2022-05-25 |

| JP Morgan | Downgrade | Neutral | 2022-05-25 |

Which company has the best grades?

Teradyne, Inc. consistently holds buy and outperform ratings from major institutions, reflecting strong confidence. Columbus McKinnon shows mixed grades with recent downgrades to neutral, signaling caution. Investors may view Teradyne’s grade consistency as a positive signal for stability.

Risks specific to each company

The following categories identify critical pressure points and systemic threats facing Teradyne, Inc. and Columbus McKinnon Corporation in the 2026 market environment:

1. Market & Competition

Teradyne, Inc.

- Operates in highly competitive semiconductor and automation markets with rapid innovation cycles.

Columbus McKinnon Corporation

- Faces intense competition in industrial machinery with cyclical demand tied to manufacturing and infrastructure sectors.

2. Capital Structure & Debt

Teradyne, Inc.

- Maintains low debt levels (D/E 0.12) with strong interest coverage, signaling financial stability.

Columbus McKinnon Corporation

- Higher leverage (D/E 0.61) and weak interest coverage (0.83) raise concerns over financial risk.

3. Stock Volatility

Teradyne, Inc.

- Exhibits high beta (1.82), reflecting greater sensitivity to market swings in tech sector.

Columbus McKinnon Corporation

- Moderate beta (1.31) indicates somewhat lower stock volatility typical of industrial stocks.

4. Regulatory & Legal

Teradyne, Inc.

- Subject to technology and export regulations impacting semiconductor testing and wireless equipment.

Columbus McKinnon Corporation

- Faces safety and environmental regulations related to machinery manufacturing and industrial operations.

5. Supply Chain & Operations

Teradyne, Inc.

- Complex global supply chain for semiconductor components vulnerable to geopolitical disruptions.

Columbus McKinnon Corporation

- Supply chain depends on raw materials and components for industrial products, exposed to commodity price volatility.

6. ESG & Climate Transition

Teradyne, Inc.

- Increasing pressure to reduce energy consumption in manufacturing and improve sustainability of automation products.

Columbus McKinnon Corporation

- Challenges to meet evolving ESG standards in heavy manufacturing and reduce carbon footprint of operations.

7. Geopolitical Exposure

Teradyne, Inc.

- Exposure to US-China trade tensions affecting semiconductor supply and demand.

Columbus McKinnon Corporation

- Limited direct exposure but vulnerable to global infrastructure spending fluctuations due to geopolitical instability.

Which company shows a better risk-adjusted profile?

Teradyne’s strongest risk is market competition in a fast-evolving tech sector with high stock volatility. Columbus McKinnon’s critical risk centers on capital structure weaknesses and operational cyclicality. Teradyne’s low leverage and robust interest coverage provide a more resilient financial footing. The semiconductor leader’s superior Altman Z-Score (20.26, safe zone) contrasts sharply with Columbus McKinnon’s distress zone (1.49). Consequently, Teradyne demonstrates a better risk-adjusted profile, supported by solid liquidity and profitability despite sector volatility.

Final Verdict: Which stock to choose?

Teradyne, Inc. (TER) excels as a cash-generating powerhouse with a robust economic moat built on efficient capital allocation and strong returns above its cost of capital. Its key point of vigilance is a declining ROIC trend, signaling potential pressure on future profitability. TER suits aggressive growth portfolios seeking market leadership in tech-driven automation.

Columbus McKinnon Corporation (CMCO) offers a strategic moat rooted in tangible asset management and a compelling price-to-book valuation. Though its recent profitability and returns trail TER’s, CMCO provides a more cautious profile with lower valuation multiples, fitting well within GARP portfolios that balance value with moderate growth expectations.

If you prioritize sustained value creation and premium market momentum, TER outshines with superior cash flow generation and higher returns despite valuation risks. However, if you seek relative safety with an eye on undervaluation and potential turnaround, CMCO offers better stability and a more attractive entry multiple. Both narratives present distinct analytical scenarios aligned to specific investor strategies.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Teradyne, Inc. and Columbus McKinnon Corporation to enhance your investment decisions: