Home > Comparison > Consumer Defensive > TSN vs SFD

The strategic rivalry between Tyson Foods, Inc. and Smithfield Foods Inc. shapes the competitive landscape of the agricultural farm products sector. Tyson operates as a diversified food company with integrated beef, pork, chicken, and prepared foods segments. Smithfield focuses primarily on packaged meats and fresh pork, emphasizing vertical integration through hog production. This head-to-head highlights a contrast between scale-driven diversification and specialized vertical control. This analysis will clarify which trajectory offers superior risk-adjusted returns for diversified portfolios.

Table of contents

Companies Overview

Tyson Foods and Smithfield Foods stand as formidable players in the global agricultural products sector.

Tyson Foods, Inc.: Global Protein Powerhouse

Tyson Foods dominates as a leading food company with a diverse portfolio spanning beef, pork, chicken, and prepared foods. Its core revenue stems from processing live cattle, hogs, and chickens into various fresh and frozen meat products. In 2026, Tyson focuses strategically on expanding ready-to-eat and branded frozen foods, leveraging strong brand equity across multiple consumer channels.

SMITHFIELD FOODS INC: Pork Industry Specialist

Smithfield Foods commands a strong market position in packaged meats and fresh pork, processing live hogs into primal cuts and specialty products. Its revenue engine integrates packaged meats and hog production, including a bioscience segment producing pharmaceutical heparin. In 2026, Smithfield prioritizes expanding export markets and enhancing its integrated hog production to secure supply chain resilience.

Strategic Collision: Similarities & Divergences

Both companies share a core focus on meat processing but diverge in scope; Tyson operates a broader protein portfolio, while Smithfield specializes in pork and bioscience. They compete primarily in North American retail and foodservice channels, with Tyson leaning on branded prepared foods and Smithfield on fresh pork exports. Their distinct business models reflect divergent investment profiles: Tyson as a diversified protein giant, Smithfield as a focused pork and bioscience innovator.

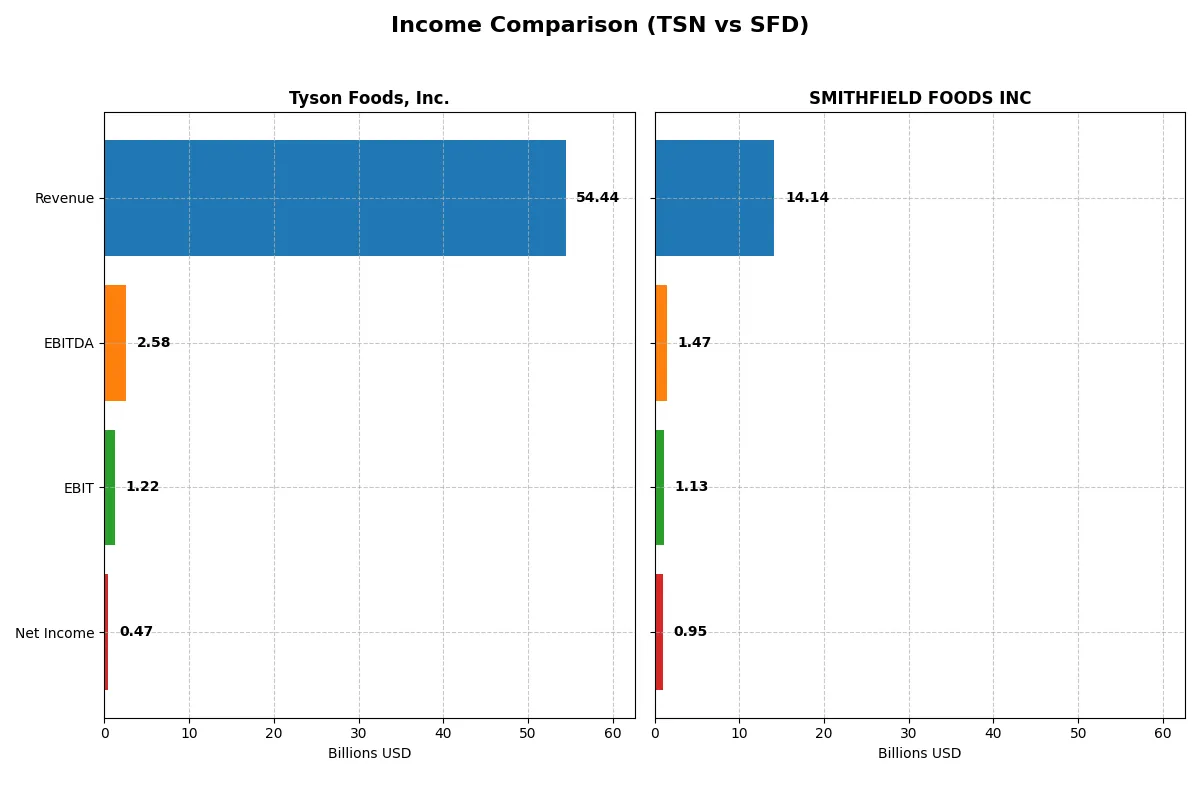

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Tyson Foods, Inc. (TSN) | SMITHFIELD FOODS INC (SFD) |

|---|---|---|

| Revenue | 54.4B | 14.1B |

| Cost of Revenue | 50.9B | 12.2B |

| Operating Expenses | 2.12B | 780M |

| Gross Profit | 3.56B | 1.90B |

| EBITDA | 2.58B | 1.47B |

| EBIT | 1.22B | 1.13B |

| Interest Expense | 449M | 66M |

| Net Income | 474M | 953M |

| EPS | 1.36 | 2.42 |

| Fiscal Year | 2025 | 2024 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company operates more efficiently by dissecting revenue, profits, and margin dynamics.

Tyson Foods, Inc. Analysis

Tyson Foods’ revenue grew modestly to $54.4B in 2025 but net income plunged to $474M. Its gross margin remains thin at 6.54%, and net margin dropped sharply to 0.87%. Despite stable interest expense, earnings momentum slowed, signaling efficiency challenges amid rising costs.

SMITHFIELD FOODS INC Analysis

Smithfield’s revenue declined slightly to $14.1B in 2024, yet net income surged to $953M. Gross margin improved substantially to 13.41%, and net margin expanded to 6.74%. Its EBIT and net margins soared, reflecting a strong operational turnaround and better cost control.

Margin Resilience vs. Revenue Scale

Smithfield outperforms Tyson on profitability and margin expansion despite lower revenue. Tyson’s revenue scale fails to translate into solid earnings or margin health. For investors, Smithfield’s profile offers a more attractive combination of operational efficiency and profit growth.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Tyson Foods, Inc. (TSN) | SMITHFIELD FOODS INC (SFD) |

|---|---|---|

| ROE | 4.35% | 16.34% |

| ROIC | 3.27% | 8.86% |

| P/E | 39.79 | 9.97 |

| P/B | 1.04 | 1.63 |

| Current Ratio | 1.55 | 2.46 |

| Quick Ratio | 0.66 | 1.05 |

| D/E | 0.49 | 0.40 |

| Debt-to-Assets | 24.1% | 21.3% |

| Interest Coverage | 3.21 | 16.94 |

| Asset Turnover | 1.49 | 1.28 |

| Fixed Asset Turnover | 5.91 | 4.03 |

| Payout ratio | 147.0% | 30.2% |

| Dividend yield | 3.70% | 3.03% |

| Fiscal Year | 2025 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as a company’s DNA, exposing hidden risks and signaling operational strength or weakness with precision.

Tyson Foods, Inc.

Tyson’s core profitability struggles with a low ROE of 2.62% and a slim net margin of 0.87%, indicating operational challenges. Its P/E ratio of 39.79 signals an expensive stock relative to earnings. The company supports shareholders with a 3.7% dividend yield, balancing reinvestment and returns amid modest efficiency.

SMITHFIELD FOODS INC

Smithfield commands a robust ROE of 16.34% and a healthier net margin at 6.74%, reflecting solid profitability. The stock trades at a modest P/E of 9.97, suggesting undervaluation. Shareholders gain from a 3.03% dividend yield, supported by strong interest coverage and efficient capital use, signaling operational resilience.

Balanced Efficiency vs. Valuation Stretch

Smithfield offers a far stronger profitability profile and more attractive valuation than Tyson, which appears stretched despite some financial stability. Investors seeking operational safety and value align better with Smithfield’s metrics, while Tyson’s profile may suit those accepting higher valuation risk for dividend income.

Which one offers the Superior Shareholder Reward?

I observe Tyson Foods (TSN) and Smithfield Foods (SFD) differ markedly in shareholder reward strategies. TSN yields around 3.7% with a payout ratio exceeding 100%, signaling aggressive dividends possibly covered by debt or asset sales. SFD offers a slightly lower yield near 3.0% but maintains a prudent payout ratio around 30%, preserving ample free cash flow for buybacks and growth. Both companies deploy buybacks, but SFD’s consistent free cash flow coverage (69%) and robust dividend-plus-capex coverage ratio (1.78) suggest a more sustainable distribution model. TSN’s elevated payout ratio and fluctuating margins raise red flags on dividend safety. I conclude SFD provides a superior total return profile for 2026, balancing yield with long-term capital preservation and buyback discipline.

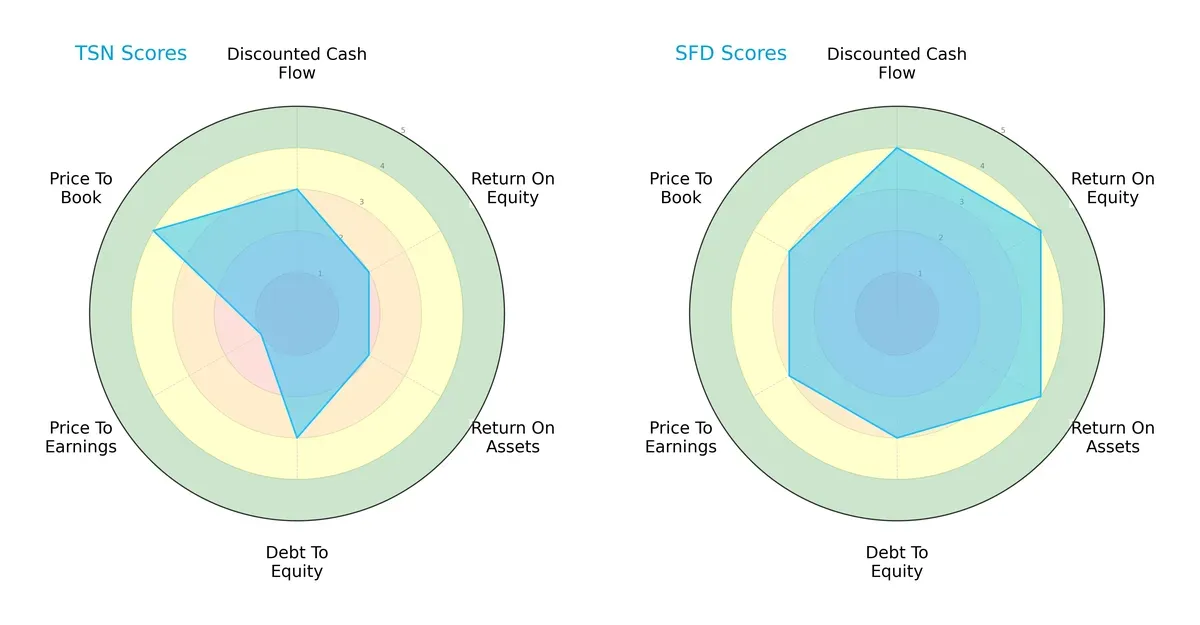

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Tyson Foods, Inc. and SMITHFIELD FOODS INC, highlighting their financial strengths and valuation differences:

SMITHFIELD FOODS INC outperforms Tyson Foods with higher scores in DCF (4 vs. 3), ROE (4 vs. 2), and ROA (4 vs. 2), reflecting superior profitability and asset efficiency. Both share moderate debt-to-equity profiles (3), but Tyson suffers from a very unfavorable P/E score (1) compared to Smithfield’s moderate (3). Tyson compensates somewhat with a stronger P/B score (4 vs. 3). Overall, Smithfield presents a more balanced and robust financial profile, while Tyson relies heavily on book value attractiveness amidst weaker earnings metrics.

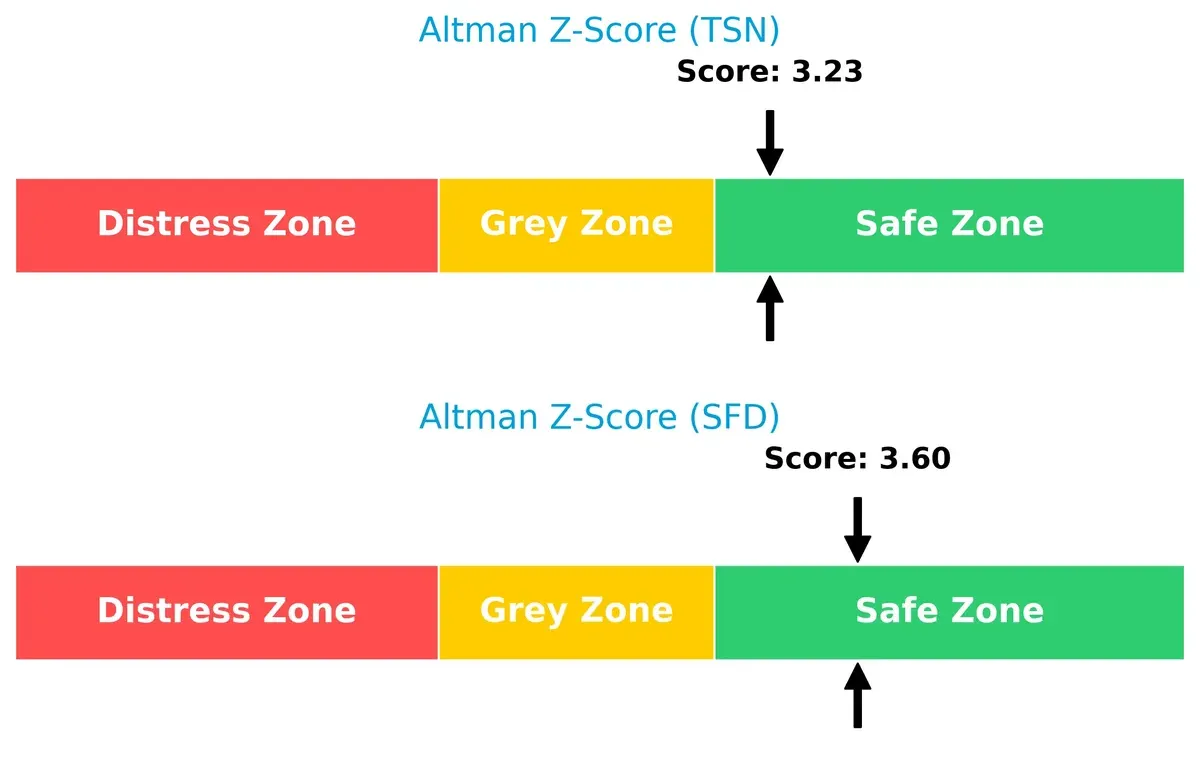

Bankruptcy Risk: Solvency Showdown

The Altman Z-Scores place both Tyson Foods (3.23) and SMITHFIELD FOODS INC (3.60) comfortably in the safe zone, indicating solid solvency and low bankruptcy risk in this cycle:

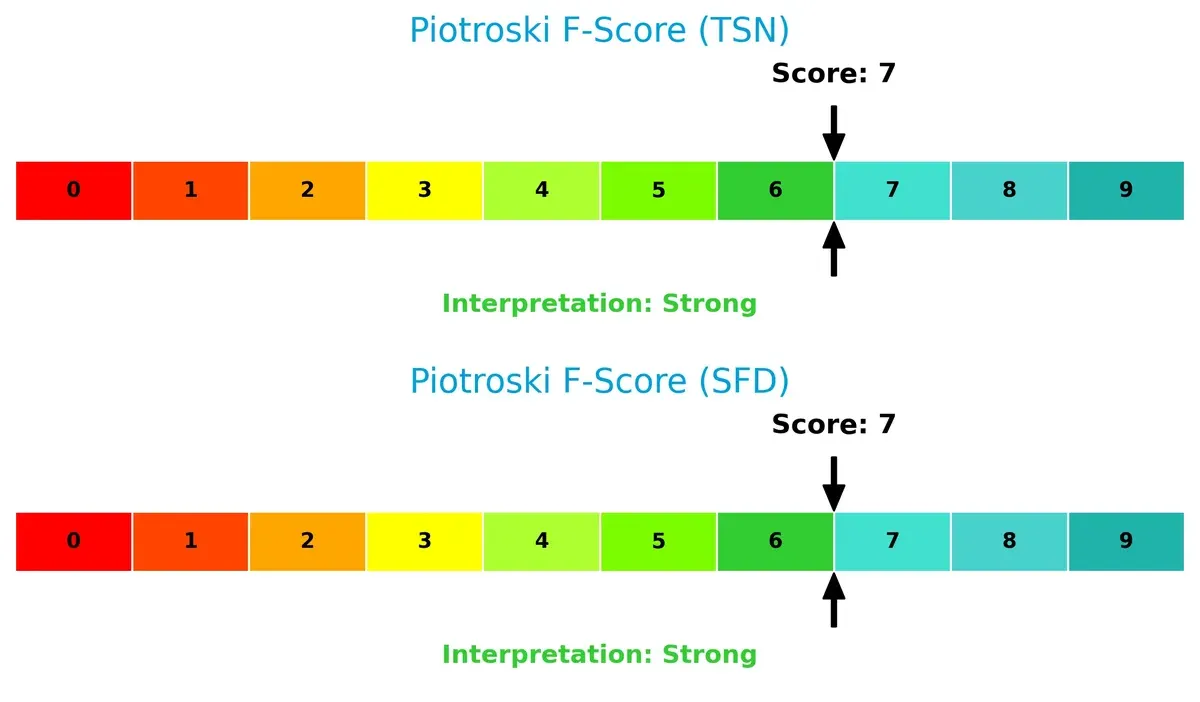

Financial Health: Quality of Operations

Both companies share a strong Piotroski F-Score of 7, signaling robust financial health and operational quality without immediate red flags in internal metrics:

How are the two companies positioned?

This section dissects the operational DNA of Tyson Foods and Smithfield by comparing their revenue distribution by segment and internal dynamics. The goal is to confront their economic moats, identifying which business model offers the most resilient and sustainable competitive advantage.

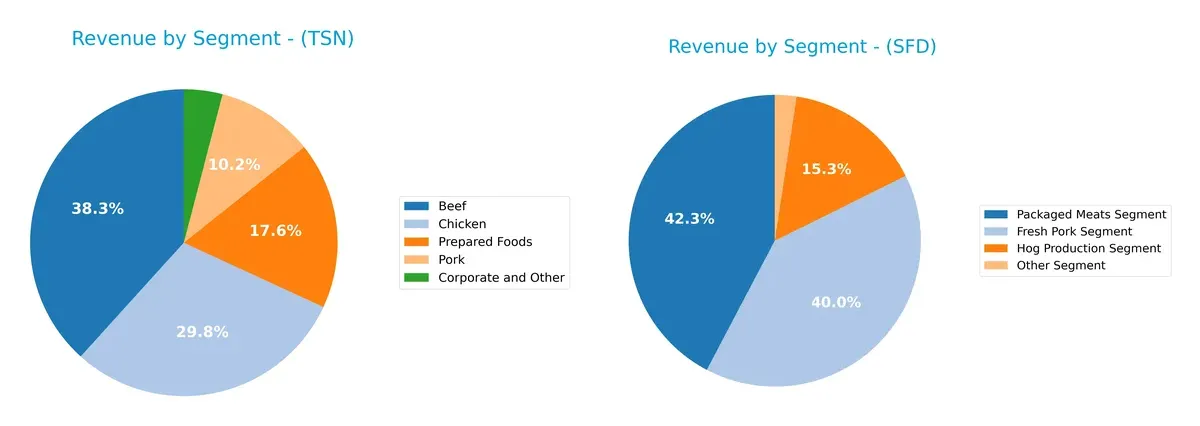

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Tyson Foods and Smithfield Foods diversify their income streams and reveals their primary sector bets:

Tyson Foods anchors its revenue in Beef ($21.6B) and Chicken ($16.8B), with significant contributions from Prepared Foods ($9.9B) and Pork ($5.8B). This mix reflects a broad protein portfolio, reducing concentration risk. Smithfield Foods pivots around Fresh Pork ($7.9B) and Packaged Meats ($8.3B), relying heavily on pork-related segments. Tyson’s diversified protein ecosystem contrasts with Smithfield’s more concentrated pork dominance, highlighting different strategic bets on market resilience and supply chain control.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Tyson Foods and Smithfield Foods based on diversification, profitability, financials, innovation, global presence, and market share:

Tyson Foods Strengths

- Diversified product segments including beef, chicken, pork, and prepared foods

- Favorable asset turnover and fixed asset turnover rates

- Strong dividend yield of 3.7%

- Solid current ratio 1.55 supports liquidity

- Low debt-to-assets ratio at 24.09%

- Presence in export sales totaling $5.1B

Smithfield Foods Strengths

- Favorable profitability metrics with ROE of 16.34% and net margin neutral at 6.74%

- Very favorable interest coverage at 17.08 supports debt servicing

- Higher current ratio 2.46 and quick ratio 1.05 indicate strong liquidity

- Broad product segments including fresh pork, hog production, and packaged meats

- Strong U.S. market presence with $11.8B revenue

- Lower WACC at 4.33% supports investment efficiency

Tyson Foods Weaknesses

- Low net margin at 0.87% and ROE of 2.62% indicate weak profitability

- ROIC of 3.05% below WACC of 5.43% suggests value destruction

- Elevated P/E ratio near 40 is expensive relative to earnings

- Quick ratio 0.66 signals potential short-term liquidity risk

- Neutral interest coverage of 2.71 may constrain financial flexibility

Smithfield Foods Weaknesses

- Neutral ROIC of 8.86% limits capital efficiency upside

- PB ratio of 1.63 is less attractive compared to Tyson’s 1.04

- Limited recent international revenue data restricts global presence visibility

- Heavy intersegment eliminations may reduce transparency of segment performance

Overall, Tyson Foods shows strength in diversified revenue streams and solid liquidity but struggles with profitability and valuation. Smithfield Foods exhibits superior profitability and liquidity metrics, supported by a focused product portfolio and strong U.S. market presence. Both companies face distinct challenges that will influence their strategic priorities going forward.

The Moat Duel: Analyzing Competitive Defensibility

A true structural moat protects long-term profits from relentless competitive pressures. Here’s how Tyson Foods and Smithfield Foods stack up:

Tyson Foods, Inc.: Cost Advantage with Margin Pressure

Tyson leverages scale and integration to manage costs in beef, pork, and chicken. Yet, declining ROIC and eroding margins warn of weakening efficiency. New product innovation offers limited moat deepening in 2026.

SMITHFIELD FOODS INC: Efficient Value Creator with Expanding ROIC

Smithfield’s moat stems from efficient hog production and strong brand portfolio, driving superior EBIT and net margins. Its rising ROIC signals growing capital efficiency and competitive resilience amid market shifts.

Cost Leadership vs. Operational Excellence: Smithfield’s Moat Deepens

Smithfield holds a wider and deeper moat, evidenced by a 4.5% ROIC premium over WACC and growing profitability. Tyson’s negative ROIC trend signals value destruction. Smithfield is better positioned to defend market share going forward.

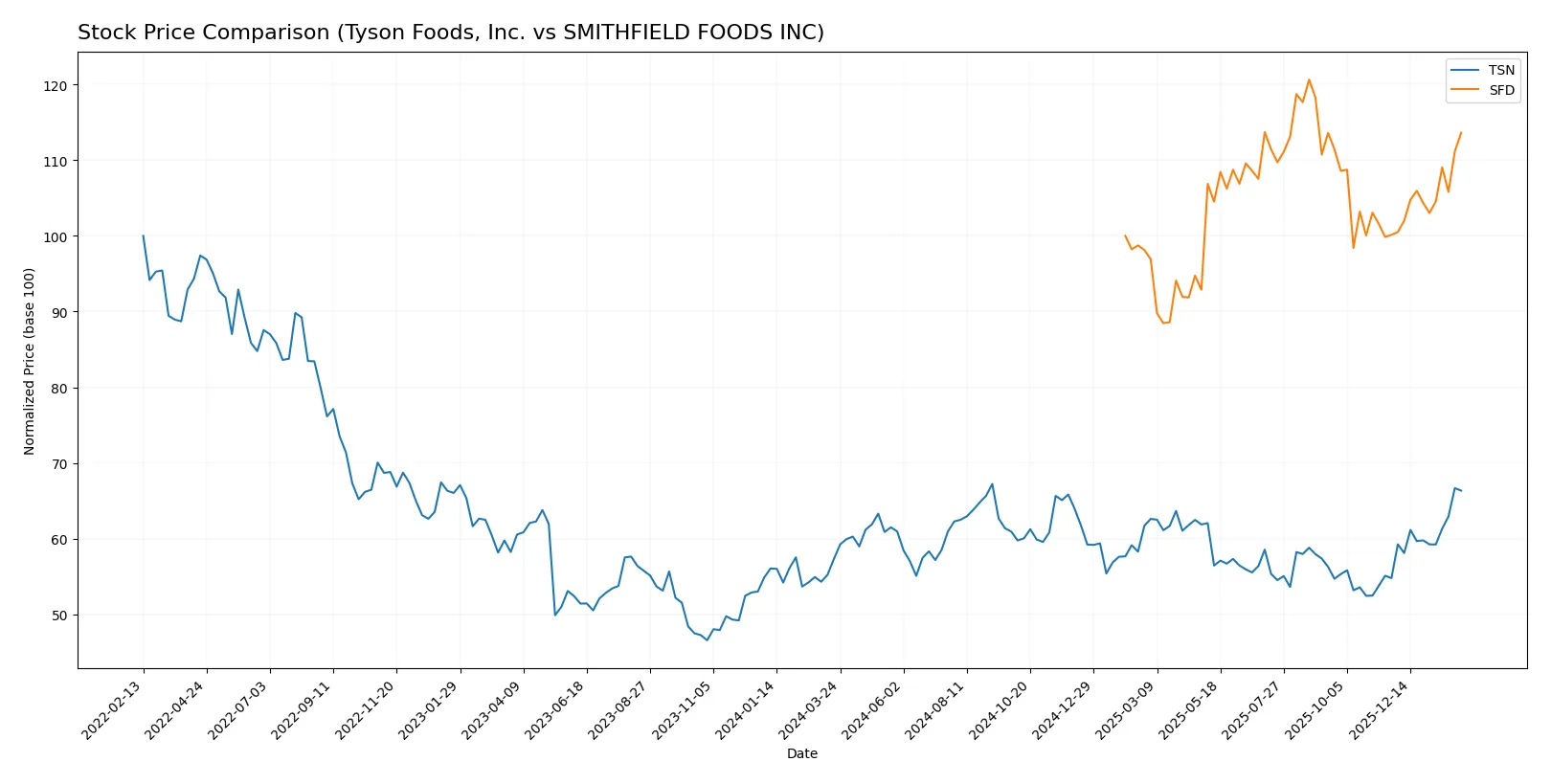

Which stock offers better returns?

Key price movements over the past year reveal Tyson Foods’ stronger bullish momentum and higher volatility compared to Smithfield Foods, which shows steady gains with lower price fluctuation.

Trend Comparison

Tyson Foods, Inc. posted a 15.76% price increase over the past year, showing a bullish trend with accelerating gains and notable volatility (3.29 std dev). It reached a high of 65.87 and a low of 51.38.

SMITHFIELD FOODS INC rose 13.63% in the same period, also bullish with acceleration but lower volatility (1.67 std dev). Its price ranged from 19.02 to 25.94, indicating steadier upward movement.

Tyson Foods outperformed Smithfield Foods by 2.13 percentage points, delivering the highest market performance with stronger recent acceleration.

Target Prices

Analysts present a clear consensus on target prices for Tyson Foods, Inc. and Smithfield Foods Inc.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Tyson Foods, Inc. | 61 | 78 | 70.25 |

| SMITHFIELD FOODS INC | 29 | 30 | 29.5 |

Tyson Foods’ consensus target of 70.25 exceeds its current price of 65, signaling moderate upside potential. Smithfield Foods shows a tighter range near 29.5, well above its recent price of 24.43, suggesting stronger expected appreciation.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Tyson Foods, Inc. Grades

The following table summarizes recent institutional grades for Tyson Foods, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| JP Morgan | Maintain | Neutral | 2026-02-03 |

| BMO Capital | Maintain | Outperform | 2026-02-03 |

| Barclays | Maintain | Overweight | 2026-02-03 |

| BMO Capital | Upgrade | Outperform | 2026-01-08 |

| Piper Sandler | Maintain | Neutral | 2025-12-12 |

| BMO Capital | Maintain | Market Perform | 2025-11-11 |

| B of A Securities | Maintain | Neutral | 2025-10-08 |

| Bernstein | Downgrade | Market Perform | 2025-07-23 |

| JP Morgan | Maintain | Neutral | 2025-05-06 |

| Stephens & Co. | Maintain | Equal Weight | 2025-05-06 |

SMITHFIELD FOODS INC Grades

Below are the latest institutional grades for SMITHFIELD FOODS INC:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| B of A Securities | Maintain | Buy | 2025-10-08 |

| Barclays | Maintain | Overweight | 2025-08-13 |

| UBS | Maintain | Buy | 2025-08-13 |

| Morgan Stanley | Maintain | Overweight | 2025-08-13 |

Which company has the best grades?

SMITHFIELD FOODS INC consistently receives Buy and Overweight grades, while Tyson Foods, Inc. shows more mixed ratings with Neutral to Outperform grades and some downgrades. Investors may view Smithfield’s stronger consensus as a sign of greater institutional confidence.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

Tyson Foods, Inc.

- Faces intense competition across beef, pork, and chicken segments, pressuring margins amid shifting consumer preferences.

SMITHFIELD FOODS INC

- Operates in packaged meats and fresh pork with strong brand portfolio but faces rising competition in retail and export markets.

2. Capital Structure & Debt

Tyson Foods, Inc.

- Maintains moderate leverage with debt-to-assets at 24%, interest coverage neutral at 2.7x, signaling manageable but watchful debt risk.

SMITHFIELD FOODS INC

- Shows healthier debt profile with 21% debt-to-assets and robust interest coverage at 17x, indicating stronger financial flexibility.

3. Stock Volatility

Tyson Foods, Inc.

- Beta at 0.47 suggests moderate sensitivity to market swings, offering relative stability in volatile sectors.

SMITHFIELD FOODS INC

- Exhibits low beta of 0.15, reflecting lower volatility and defensive stock characteristics.

4. Regulatory & Legal

Tyson Foods, Inc.

- Subject to complex food safety, labor, and environmental regulations, with potential exposure to litigation risks.

SMITHFIELD FOODS INC

- Similar regulatory pressures but benefits from recent restructuring and tighter controls reducing legal vulnerabilities.

5. Supply Chain & Operations

Tyson Foods, Inc.

- Large scale operations create complexity; recent supply disruptions highlight vulnerability to input cost inflation.

SMITHFIELD FOODS INC

- More focused hog production and vertical integration improve supply chain resilience but rely on contract farmers.

6. ESG & Climate Transition

Tyson Foods, Inc.

- Faces increasing pressure on emissions and sustainable sourcing, with ongoing initiatives but room for improvement.

SMITHFIELD FOODS INC

- Progressive on ESG initiatives, especially in bioscience and waste management, positioning better for climate transition risks.

7. Geopolitical Exposure

Tyson Foods, Inc.

- Global footprint exposes it to trade tensions and tariffs, especially in export markets like China and Mexico.

SMITHFIELD FOODS INC

- Export-focused but more concentrated in stable markets; geopolitical risks somewhat mitigated by diversified product lines.

Which company shows a better risk-adjusted profile?

Smithfield Foods presents a stronger overall risk-adjusted profile than Tyson Foods. Its superior debt metrics and stock stability reduce financial risk significantly. Tyson’s main risk lies in weaker profitability and higher competitive pressure, while Smithfield’s largest threat is its reliance on contract farming amidst operational complexity. Smithfield’s 17x interest coverage ratio exemplifies its robust balance sheet, justifying my confidence in its resilience.

Final Verdict: Which stock to choose?

Tyson Foods, Inc. (TSN) boasts unmatched operational efficiency and a solid dividend yield, making it a compelling cash generator in the food sector. However, its declining profitability and value destruction present a clear point of vigilance. TSN appears best suited for aggressive growth investors willing to weather volatility.

SMITHFIELD FOODS INC (SFD) stands out with a durable strategic moat, demonstrated by growing ROIC and robust financial health. Its conservative leverage and stable earnings growth offer better safety compared to TSN. SFD fits well within a GARP (Growth at a Reasonable Price) portfolio seeking sustainable value creation.

If you prioritize high operational efficiency and income generation, TSN is the compelling choice due to its cash flow strength and dividend appeal despite recent profitability challenges. However, if you seek superior financial stability and a proven competitive advantage, SFD offers better stability and consistent value creation, commanding a moderate premium in valuation.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Tyson Foods, Inc. and SMITHFIELD FOODS INC to enhance your investment decisions: