In the dynamic world of software applications, Salesforce, Inc. (CRM) and Shopify Inc. (SHOP) stand out as innovators reshaping customer engagement and commerce. Both companies lead in their industry—Salesforce with its comprehensive customer relationship management platform, and Shopify by empowering merchants worldwide with versatile e-commerce solutions. Their market overlap and innovation strategies make this comparison crucial for investors. Let’s explore which company presents the most compelling investment opportunity for your portfolio.

Table of contents

Companies Overview

I will begin the comparison between Salesforce, Inc. and Shopify Inc. by providing an overview of these two companies and their main differences.

Salesforce Overview

Salesforce, Inc. specializes in customer relationship management technology, offering its Customer 360 platform to help companies create connected experiences with customers. It serves various industries including financial services, healthcare, and manufacturing. Headquartered in San Francisco, Salesforce provides a broad range of services such as sales, service, marketing, commerce, analytics, and integration solutions, supported by a global workforce of approximately 76K employees.

Shopify Overview

Shopify Inc. is a commerce company providing a platform that enables merchants worldwide to manage and sell products across multiple sales channels, including online and physical stores. Based in Ottawa, Canada, Shopify offers merchant solutions like payments, shipping, and financing, targeting a diverse range of businesses. The company employs around 8.1K people and focuses on empowering merchants with tools to optimize their commerce operations.

Key similarities and differences

Both Salesforce and Shopify operate in the technology sector within the software-application industry, focusing on platforms that enhance customer engagement and business operations. Salesforce emphasizes customer relationship management and enterprise solutions across industries, whereas Shopify centers on commerce and merchant services across global sales channels. Salesforce’s workforce is significantly larger, reflecting its broader service scope compared to Shopify’s specialized commerce platform.

Income Statement Comparison

The table below presents a side-by-side comparison of key income statement metrics for Salesforce, Inc. and Shopify Inc. for their most recent fiscal years.

| Metric | Salesforce, Inc. (CRM) | Shopify Inc. (SHOP) |

|---|---|---|

| Market Cap | 218.4B | 203.7B |

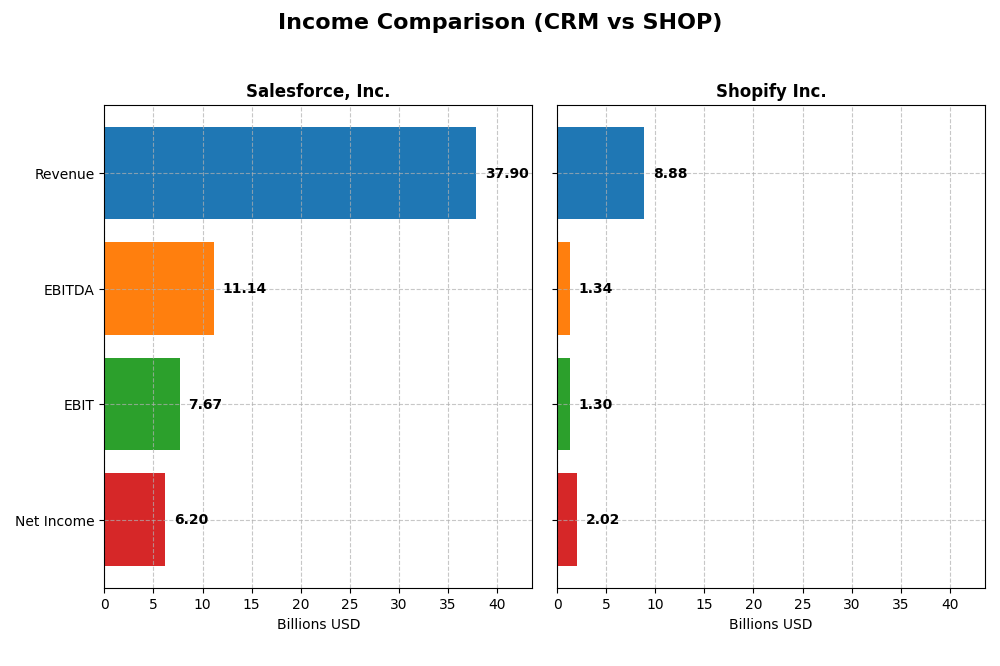

| Revenue | 37.9B | 8.9B |

| EBITDA | 11.1B | 1.3B |

| EBIT | 7.7B | 1.3B |

| Net Income | 6.2B | 2.0B |

| EPS | 6.44 | 1.56 |

| Fiscal Year | 2025 | 2024 |

Income Statement Interpretations

Salesforce, Inc.

Salesforce’s revenue and net income have shown consistent growth from 2021 to 2025, with revenue increasing from $21.3B to $37.9B and net income rising from $4.07B to $6.20B. Margins remain strong, with a gross margin of 77.19% and a favorable net margin of 16.35% in 2025. The latest year saw revenue growth slow to 8.72%, but net income and EBIT margins improved significantly.

Shopify Inc.

Shopify’s revenue and net income have expanded markedly between 2020 and 2024, with revenue rising from $2.93B to $8.88B and net income soaring from $320M to $2.02B. Margins improved notably, with a gross margin of 50.36% and a net margin of 22.74% in 2024. The most recent year exhibited strong growth rates, including a 25.78% revenue increase and over 1000% net margin expansion, reflecting significant operational leverage.

Which one has the stronger fundamentals?

Both companies present favorable income statement fundamentals, with Salesforce demonstrating steady, substantial revenue and net income growth alongside high margins. Shopify exhibits more dramatic growth rates and margin improvements, reflecting rapid scale-up from a smaller base. Salesforce’s stability contrasts with Shopify’s volatility, making each company’s fundamentals strong but distinct in risk and growth profiles based on the income statement data.

Financial Ratios Comparison

The table below presents a side-by-side comparison of key financial ratios for Salesforce, Inc. (CRM) and Shopify Inc. (SHOP) based on their most recent full fiscal year data from 2025 and 2024 respectively.

| Ratios | Salesforce, Inc. (CRM) 2025 | Shopify Inc. (SHOP) 2024 |

|---|---|---|

| ROE | 10.1% | 17.5% |

| ROIC | 7.95% | 7.55% |

| P/E | 53.0 | 68.2 |

| P/B | 5.37 | 11.9 |

| Current Ratio | 1.06 | 3.71 |

| Quick Ratio | 1.06 | 3.70 |

| D/E (Debt-to-Equity) | 0.19 | 0.10 |

| Debt-to-Assets | 11.1% | 8.1% |

| Interest Coverage | 26.5 | 0 |

| Asset Turnover | 0.37 | 0.64 |

| Fixed Asset Turnover | 7.03 | 63.4 |

| Payout ratio | 24.8% | 0% |

| Dividend yield | 0.47% | 0% |

Interpretation of the Ratios

Salesforce, Inc.

Salesforce shows a balanced financial profile with 43% of its ratios favorable and 29% unfavorable. Its net margin is solid at 16.35%, while the PE ratio at 53.04 and PB at 5.37 suggest a potentially expensive valuation. The company pays a dividend with a low yield of 0.47%, which may indicate cautious distribution given the payout coverage by free cash flow and moderate share buybacks.

Shopify Inc.

Shopify exhibits a strong profitability profile with a 22.74% net margin and a high 17.47% return on equity. Half of its ratios are favorable, though the company faces a high WACC of 17.1% and elevated valuation multiples, PE at 68.18 and PB at 11.91. Shopify does not pay dividends, reflecting its reinvestment focus in growth and R&D, supported by a strong current ratio of 3.71 and share repurchase flexibility.

Which one has the best ratios?

Both Salesforce and Shopify present slightly favorable overall ratio evaluations, with Shopify having a higher proportion of favorable profitability metrics but also more unfavorable valuation indicators. Salesforce balances moderate profitability and valuation concerns with a consistent dividend policy, while Shopify prioritizes growth over distributions. The choice depends on investor preference for valuation versus growth focus.

Strategic Positioning

This section compares the strategic positioning of Salesforce, Inc. and Shopify Inc., including market position, key segments, and exposure to technological disruption:

Salesforce, Inc.

- Leading CRM provider with strong market cap and moderate beta, facing steady competitive pressure.

- Diverse segments: Sales, Service, Marketing, Commerce, Analytics, Integration, and Professional Services.

- Invests in flexible platform, analytics, and integration tools to mitigate disruption risks.

Shopify Inc.

- Commerce platform leader with high beta, experiencing intense competition in e-commerce.

- Focused on merchant solutions and subscription services for online and physical retail merchants.

- Emphasizes multi-channel commerce platform, adapting to evolving retail technologies.

Salesforce vs Shopify Positioning

Salesforce has a diversified business model across CRM, analytics, and cloud services, supporting various industries globally. Shopify concentrates on commerce platform solutions, targeting merchants with integrated sales tools. Salesforce’s scale offers breadth, while Shopify’s focus drives specialized innovation.

Which has the best competitive advantage?

Both companies exhibit a slightly unfavorable MOAT with growing ROIC trends, indicating improving profitability but ongoing value destruction. Neither currently sustains a strong competitive advantage based on ROIC versus WACC metrics.

Stock Comparison

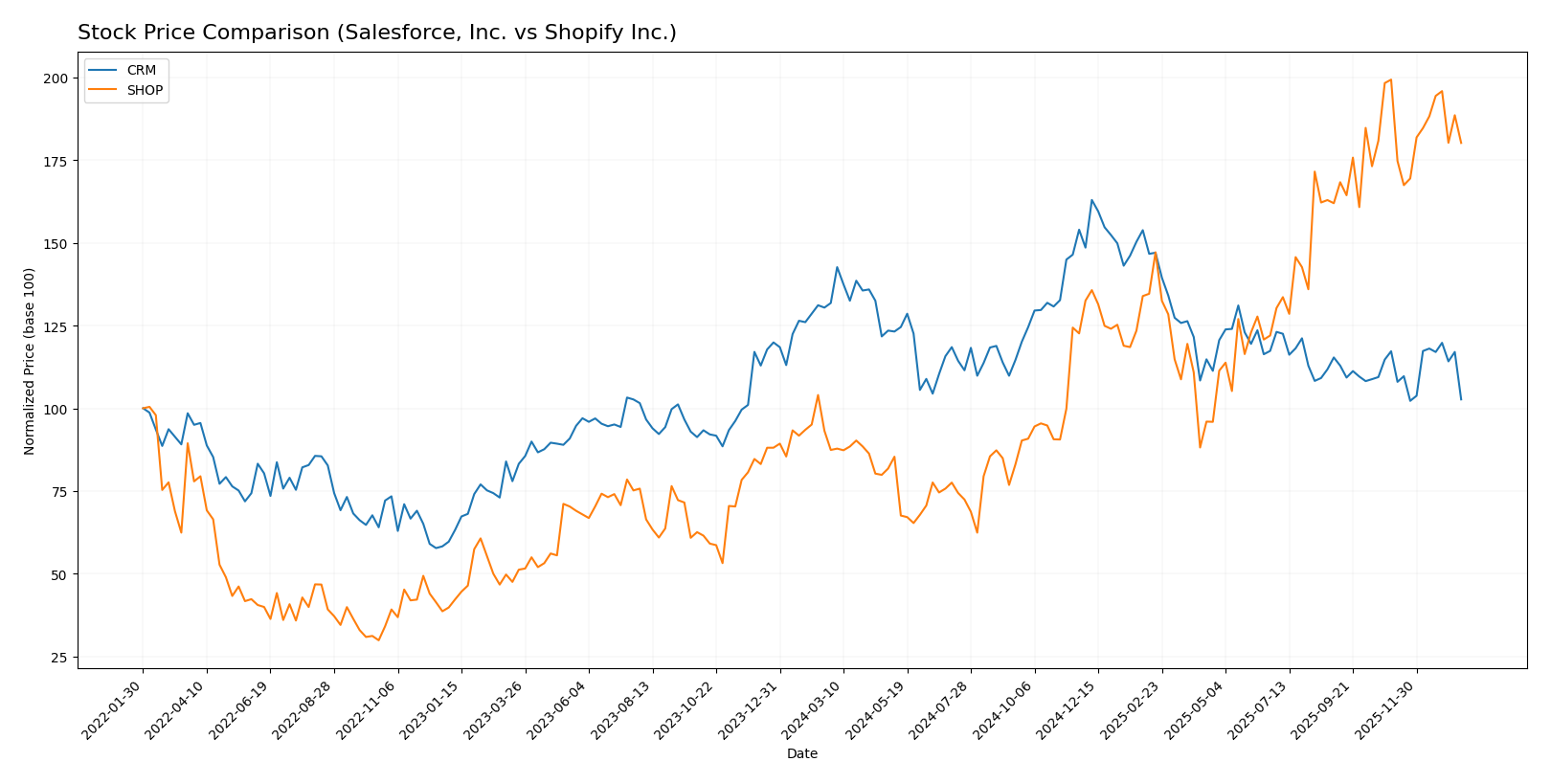

The past year reveals divergent stock price movements for Salesforce, Inc. (CRM) and Shopify Inc. (SHOP), with CRM experiencing a significant bearish trend and SHOP showing a strong bullish trend despite recent softness in both.

Trend Analysis

Salesforce, Inc. (CRM) recorded a -22.1% price decline over the past 12 months, indicating a bearish trend with accelerating downward momentum and a high price volatility of 31.8%. The stock hit a high of 361.99 and a low of 227.11 within this period.

Shopify Inc. (SHOP) posted a 106.15% price increase over the past 12 months, reflecting a bullish trend with decelerating gains and a volatility of 33.7%. The stock’s highest price was 173.86 and lowest was 54.43 during this timeframe.

Comparing both, Shopify delivered the highest market performance with robust gains, while Salesforce showed a pronounced decline, marking clear divergence in investor sentiment over the last year.

Target Prices

The current analyst consensus for target prices indicates moderate upside potential for both Salesforce, Inc. and Shopify Inc.

| Company | Target High | Target Low | Consensus |

|---|---|---|---|

| Salesforce, Inc. | 400 | 250 | 324.17 |

| Shopify Inc. | 200 | 140 | 186.24 |

Analysts expect Salesforce’s stock to trade significantly above its current price of 228.43 USD, implying upside potential. Shopify’s consensus target is also well above its current price of 156.46 USD, reflecting positive growth expectations.

Analyst Opinions Comparison

This section compares analysts’ ratings and financial scores for Salesforce, Inc. (CRM) and Shopify Inc. (SHOP):

Rating Comparison

CRM Rating

- Rating: B+ indicating a very favorable outlook.

- Discounted Cash Flow Score: 4, favorable value.

- ROE Score: 4, favorable efficiency in equity use.

- ROA Score: 4, favorable asset utilization.

- Debt To Equity Score: 3, moderate financial risk.

- Overall Score: 3, moderate overall financial health.

SHOP Rating

- Rating: B indicating a very favorable outlook.

- Discounted Cash Flow Score: 2, moderate value.

- ROE Score: 4, favorable efficiency in equity use.

- ROA Score: 5, very favorable asset utilization.

- Debt To Equity Score: 3, moderate financial risk.

- Overall Score: 3, moderate overall financial health.

Which one is the best rated?

Salesforce (CRM) holds a slightly higher overall rating (B+) and a better discounted cash flow score compared to Shopify (SHOP). However, Shopify scores higher on return on assets, indicating more effective asset use. Both have moderate overall scores and similar debt-to-equity ratings.

Scores Comparison

Here is a comparison of the Altman Z-Score and Piotroski Score for Salesforce, Inc. and Shopify Inc.:

Salesforce, Inc. Scores

- Altman Z-Score: 5.26, indicating a safe zone, low bankruptcy risk.

- Piotroski Score: 7, categorized as strong financial health.

Shopify Inc. Scores

- Altman Z-Score: 50.42, indicating a safe zone, very low bankruptcy risk.

- Piotroski Score: 6, categorized as average financial health.

Which company has the best scores?

Shopify has a significantly higher Altman Z-Score, indicating lower bankruptcy risk, while Salesforce shows a stronger Piotroski Score. Based on these scores, Shopify ranks better in bankruptcy risk, Salesforce in financial strength.

Grades Comparison

Here is the grades comparison for Salesforce, Inc. and Shopify Inc.:

Salesforce, Inc. Grades

The following table summarizes recent grades from reputable grading firms for Salesforce, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Barclays | maintain | Overweight | 2026-01-12 |

| RBC Capital | maintain | Sector Perform | 2026-01-05 |

| Morgan Stanley | maintain | Overweight | 2025-12-09 |

| Citigroup | maintain | Neutral | 2025-12-08 |

| DA Davidson | maintain | Neutral | 2025-12-05 |

| Citizens | maintain | Market Outperform | 2025-12-04 |

| Deutsche Bank | maintain | Buy | 2025-12-04 |

| Wedbush | maintain | Outperform | 2025-12-04 |

| Northland Capital Markets | maintain | Market Perform | 2025-12-04 |

| Canaccord Genuity | maintain | Buy | 2025-12-04 |

Salesforce’s grades show a stable pattern with most firms maintaining favorable ratings, mainly ranging from Neutral to Overweight and Buy.

Shopify Inc. Grades

The following table summarizes recent grades from reputable grading firms for Shopify Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Scotiabank | upgrade | Sector Outperform | 2026-01-08 |

| Wolfe Research | downgrade | Peer Perform | 2026-01-06 |

| Wells Fargo | maintain | Overweight | 2025-12-17 |

| Truist Securities | maintain | Hold | 2025-11-05 |

| CIBC | maintain | Outperform | 2025-11-05 |

| Cantor Fitzgerald | maintain | Neutral | 2025-11-05 |

| DA Davidson | maintain | Buy | 2025-11-05 |

| Scotiabank | maintain | Sector Perform | 2025-11-05 |

| Needham | maintain | Buy | 2025-11-05 |

| JP Morgan | maintain | Overweight | 2025-11-05 |

Shopify’s grades exhibit some recent volatility with upgrades and downgrades, but predominantly favorable ratings from Buy to Overweight.

Which company has the best grades?

Both Salesforce and Shopify hold a consensus “Buy” rating, but Salesforce has a stronger proportion of Buy and Strong Buy recommendations (73) compared to Shopify’s 37. Salesforce’s consistently stable and mostly positive grades may appeal to investors seeking steadiness, while Shopify shows some variability that could imply higher risk or opportunity.

Strengths and Weaknesses

Below is a comparison of key strengths and weaknesses for Salesforce, Inc. (CRM) and Shopify Inc. (SHOP) based on recent financial and market data.

| Criterion | Salesforce, Inc. (CRM) | Shopify Inc. (SHOP) |

|---|---|---|

| Diversification | Highly diversified product portfolio across clouds and services, with over $37B revenue in FY2025 | Moderate diversification between Merchant and Subscription Solutions, ~$8.9B revenue in FY2024 |

| Profitability | Net margin 16.35% (favorable), ROIC 7.95% (neutral), but ROIC below WACC (9.41%) indicating slight value destruction | Higher net margin 22.74% and ROE 17.47% (both favorable), but ROIC (7.55%) below high WACC (17.1%), showing value erosion |

| Innovation | Strong focus on integration, analytics, and platform development, with steady revenue growth in new segments | Innovation reflected in rapid growth of Merchant Solutions and Subscription revenues, with impressive fixed asset turnover |

| Global presence | Extensive global footprint with cloud services widely adopted | Growing international presence, but less extensive than Salesforce |

| Market Share | Leading CRM market position with dominant cloud software offerings | Significant e-commerce platform player but smaller market share compared to Salesforce in software |

Key takeaways: Both companies show strong innovation and revenue growth, but both currently shed value as their ROIC falls below WACC. Salesforce benefits from greater diversification and global reach, while Shopify excels in profitability but faces higher capital costs. Investors should weigh growth potential against the current value destruction risk.

Risk Analysis

Below is a comparative overview of key risks for Salesforce, Inc. (CRM) and Shopify Inc. (SHOP) based on the most recent financial and market data for 2025 and 2024 respectively.

| Metric | Salesforce, Inc. (CRM) | Shopify Inc. (SHOP) |

|---|---|---|

| Market Risk | Beta 1.27; moderate volatility with NYSE listing | Beta 2.84; high volatility on NASDAQ |

| Debt level | Low debt-to-equity 0.19; favorable leverage | Low debt-to-equity 0.10; very favorable leverage |

| Regulatory Risk | Moderate; US tech regulations impact | Moderate; Canadian and US operations subject to multiple regimes |

| Operational Risk | Large scale with 76.5K employees; complexity manageable | Smaller workforce (8.1K) but rapid growth adds risk |

| Environmental Risk | Moderate; US-based tech company with sustainability initiatives | Moderate; global e-commerce platform with supply chain exposure |

| Geopolitical Risk | US-focused but global clients; moderate exposure | High exposure due to global merchant base in diverse regions |

Salesforce’s moderate market risk and strong balance sheet reduce financial distress concerns, supported by a safe Altman Z-score above 5. Shopify’s higher beta indicates market sensitivity and elevated price volatility, though it benefits from very low debt and a safe bankruptcy risk score. The most impactful risks remain Shopify’s market volatility and geopolitical exposure, while Salesforce’s operational scale and regulatory compliance are key considerations for investors.

Which Stock to Choose?

Salesforce, Inc. (CRM) shows a favorable income evolution with 8.72% revenue growth in 2025 and strong profitability metrics, including a 16.35% net margin. Financial ratios are slightly favorable overall, with low debt levels and a solid rating of B+. However, its ROIC is below WACC, indicating slight value destruction despite improving profitability.

Shopify Inc. (SHOP) demonstrates robust growth with 25.78% revenue increase in 2024 and a higher net margin of 22.74%. Its financial ratios are slightly favorable, featuring strong profitability and low debt, though challenged by high valuation multiples and a B rating. Like CRM, its ROIC is below WACC but trending positively, signaling improving efficiency.

For investors, Shopify’s stronger growth and profitability could appeal to those with a risk-tolerant or growth-oriented profile, while Salesforce’s stable income and moderate financial ratios may appear more suitable for those prioritizing quality and financial resilience. Both companies show improving profitability amid value shedding, suggesting cautious consideration aligned with individual risk tolerance.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Salesforce, Inc. and Shopify Inc. to enhance your investment decisions: