Home > Comparison > Technology > WDC vs RGTI

The strategic rivalry between Western Digital Corporation and Rigetti Computing, Inc. shapes the evolution of the technology sector’s hardware landscape. Western Digital operates as a capital-intensive data storage manufacturer with a broad product portfolio and global reach. In contrast, Rigetti is a nimble innovator focused on quantum computing systems and cloud integration. This analysis will assess which company’s trajectory delivers superior risk-adjusted returns for a diversified portfolio navigating technology’s next frontier.

Table of contents

Companies Overview

Western Digital and Rigetti Computing represent two distinct pillars in the evolving technology hardware landscape. Both command significant attention in their specialized domains, shaping the future of data storage and quantum computing.

Western Digital Corporation: Data Storage Powerhouse

Western Digital dominates as a leader in data storage solutions. Its revenue stems from manufacturing HDDs, SSDs, and flash-based products for PCs, mobile devices, and data centers. In 2026, the company focuses on expanding its enterprise storage platforms and tiered storage models, reinforcing its competitive edge in scalable data management across global markets.

Rigetti Computing, Inc.: Quantum Computing Innovator

Rigetti Computing stands out as a pioneering quantum systems company. It generates revenue by building integrated quantum computers and superconducting processors, offering access through its Quantum Cloud Services platform. The firm’s 2026 strategy emphasizes scaling cloud integration and advancing quantum processor capabilities to accelerate commercial adoption.

Strategic Collision: Similarities & Divergences

Western Digital and Rigetti contrast sharply in their business models: Western Digital relies on mature, high-volume hardware sales, while Rigetti pursues cutting-edge quantum cloud infrastructure. Their primary battleground is technological innovation versus market scale within computer hardware. This divergence shapes their investment profiles—Western Digital offers a robust, established cash flow; Rigetti embodies high-risk, high-reward growth potential.

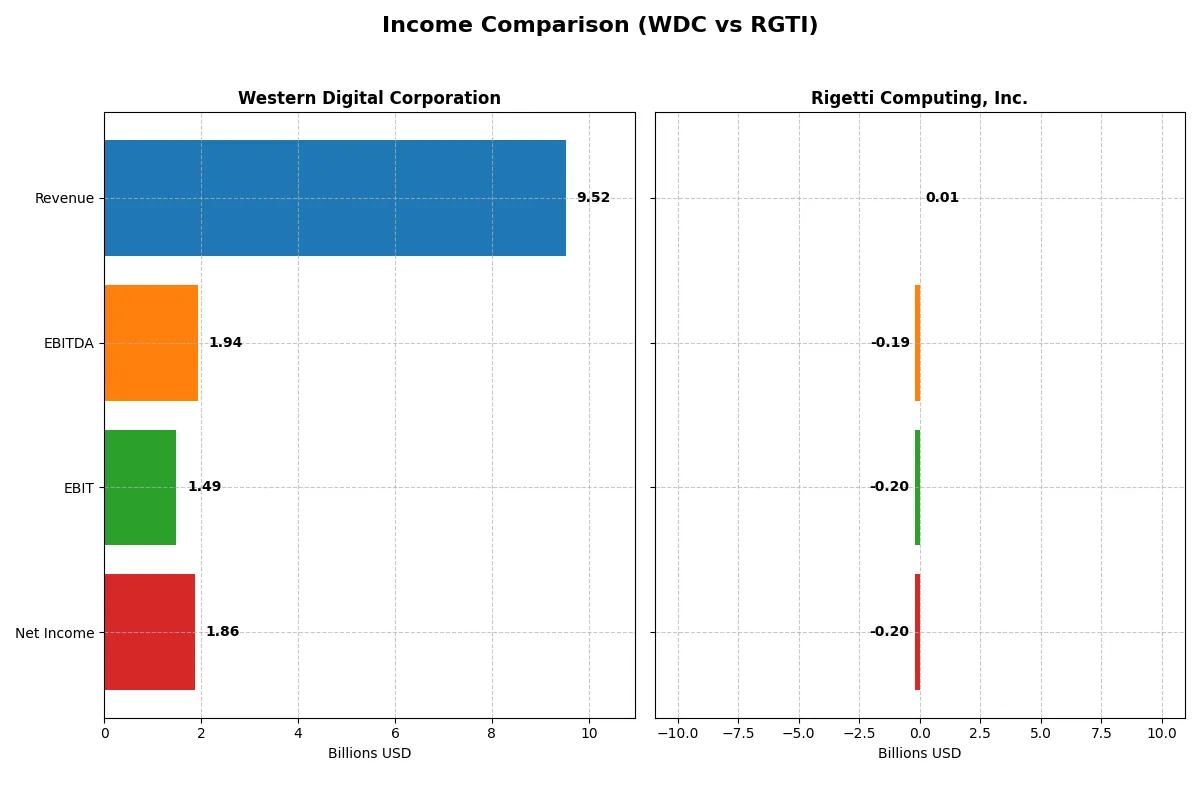

Income Statement Comparison

This table dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Western Digital Corporation (WDC) | Rigetti Computing, Inc. (RGTI) |

|---|---|---|

| Revenue | 9.52B | 10.8M |

| Cost of Revenue | 5.83B | 5.09M |

| Operating Expenses | 1.36B | 74.2M |

| Gross Profit | 3.69B | 5.70M |

| EBITDA | 1.94B | -190.8M |

| EBIT | 1.49B | -197.7M |

| Interest Expense | 357M | 3.26M |

| Net Income | 1.86B | -201.0M |

| EPS | 5.31 | -1.09 |

| Fiscal Year | 2025 | 2024 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company runs its operations most efficiently and generates superior profitability.

Western Digital Corporation Analysis

Western Digital’s revenue recovered impressively, rising 51% in 2025 to $9.5B after a steep drop in 2024. Net income swung from a loss of $798M in 2024 to a strong profit of $1.86B in 2025. Its gross margin holds firm at 38.8%, while net margin surged to 19.6%, signaling robust operational efficiency and a powerful earnings comeback.

Rigetti Computing, Inc. Analysis

Rigetti’s revenue slipped 10% to $10.8M in 2024, reflecting ongoing challenges scaling its business. Despite a strong gross margin of 52.8%, it reported a net loss of $201M and a severe negative net margin of -1863%. The widening losses and deteriorating EBIT margin underscore persistent inefficiencies and high operational expenses relative to revenue.

Profitability Rebound vs. Persistent Losses

Western Digital emerges as the clear fundamental winner with a sharp rebound in revenue and profitability, underpinned by healthy margins and effective cost control. Rigetti’s profile remains that of a high-burn startup struggling to convert innovation into profit. For investors prioritizing earnings strength and margin stability, Western Digital’s turnaround offers a more compelling, lower-risk investment profile.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of each company:

| Ratios | Western Digital Corporation (WDC) | Rigetti Computing, Inc. (RGTI) |

|---|---|---|

| ROE | 35.0% | -158.8% |

| ROIC | 21.5% | -24.9% |

| P/E | 11.8 | -14.0 |

| P/B | 4.14 | 22.26 |

| Current Ratio | 1.08 | 17.42 |

| Quick Ratio | 0.84 | 17.42 |

| D/E | 0.96 | 0.07 |

| Debt-to-Assets | 36.3% | 3.1% |

| Interest Coverage | 6.54 | -21.0 |

| Asset Turnover | 0.68 | 0.04 |

| Fixed Asset Turnover | 4.06 | 0.20 |

| Payout ratio | 2.4% | 0% |

| Dividend yield | 0.20% | 0% |

| Fiscal Year | 2025 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios serve as a company’s DNA, exposing hidden risks and operational strengths that raw numbers alone cannot reveal.

Western Digital Corporation

Western Digital exhibits a robust 35% ROE and a healthy 19.6% net margin, signaling strong profitability. Its P/E of 11.8 remains attractive, suggesting the stock is reasonably valued, though a 4.14 PB ratio flags some premium on assets. Dividend yield is minimal at 0.2%, indicating modest shareholder returns with a focus on operational efficiency and capital allocation.

Rigetti Computing, Inc.

Rigetti shows deeply negative profitability with a -158.8% ROE and a net margin of -1862.7%, revealing significant operational challenges. The P/E ratio is negative but flagged favorable due to losses, while a steep 22.26 PB ratio signals stretched valuation. No dividends exist; instead, Rigetti reinvests aggressively in R&D, reflecting a growth-oriented but high-risk profile.

Balanced Profitability vs. High-Risk Growth

Western Digital offers a far more balanced risk-reward profile with solid profitability and reasonable valuation metrics. Rigetti’s ratios reflect a high-risk, speculative growth play with operational inefficiencies and stretched asset valuations. Investors seeking stability may prefer Western Digital; those favoring aggressive growth must accept Rigetti’s elevated risks.

Which one offers the Superior Shareholder Reward?

Western Digital Corporation (WDC) offers a modest dividend yield of 0.20% with a very low payout ratio of 2.36%, indicating ample free cash flow coverage and capacity for future distributions. It complements dividends with steady buybacks, supporting shareholder returns sustainably. Rigetti Computing, Inc. (RGTI) pays no dividends and burns free cash flow, focusing entirely on reinvestment for growth in quantum computing. However, RGTI’s negative margins and high valuation multiples signal elevated risk and uncertain near-term returns. I view WDC’s balanced distribution model as more sustainable and attractive for total shareholder reward in 2026, especially when benchmarked against the S&P 500’s average yield near 1.5%. Rigetti’s aggressive reinvestment is promising but speculative, making WDC the superior choice for disciplined investors seeking reliable returns.

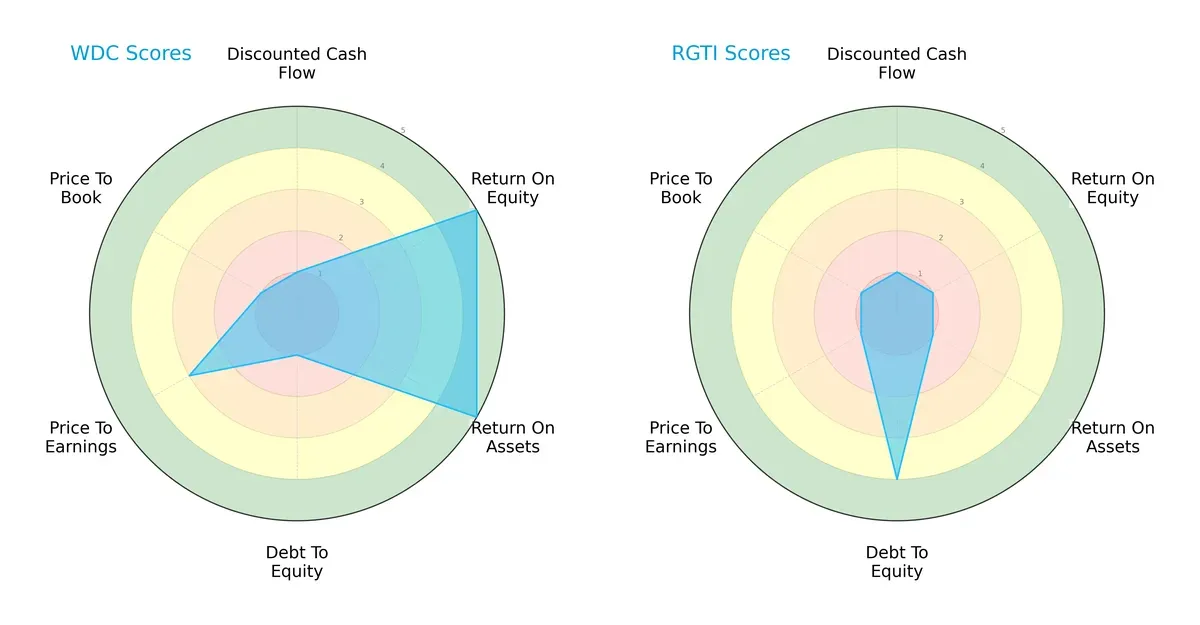

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Western Digital Corporation and Rigetti Computing, Inc.:

Western Digital shows strong operational efficiency with top ROE and ROA scores (5 each), but suffers from a weak balance sheet, indicated by a low debt-to-equity score (1). Rigetti, conversely, has a healthier leverage profile (debt-to-equity score 4) but lags significantly in profitability and valuation metrics. Western Digital presents a more balanced yet riskier profile, while Rigetti relies on financial prudence amid operational challenges.

Bankruptcy Risk: Solvency Showdown

Western Digital’s Altman Z-Score of 8.96 versus Rigetti’s 12.33 places both firms safely above distress thresholds, signaling robust long-term survival prospects in this cycle:

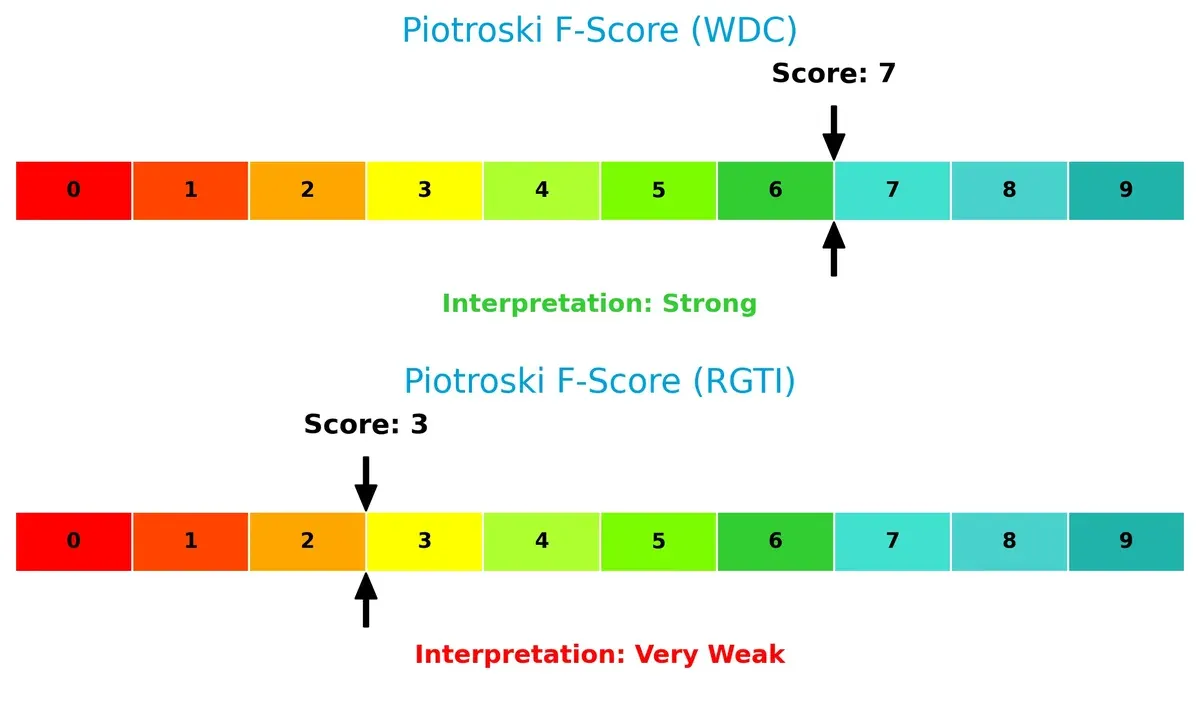

Financial Health: Quality of Operations

Western Digital’s Piotroski F-Score of 7 reveals strong financial health and operational quality. Rigetti’s score of 3 flags potential internal weaknesses and red flags for investors:

How are the two companies positioned?

This section dissects the operational DNA of WDC and RGTI by comparing their revenue distribution and internal dynamics—strengths and weaknesses. The final objective is to confront their economic moats and identify which business model offers the most resilient competitive advantage today.

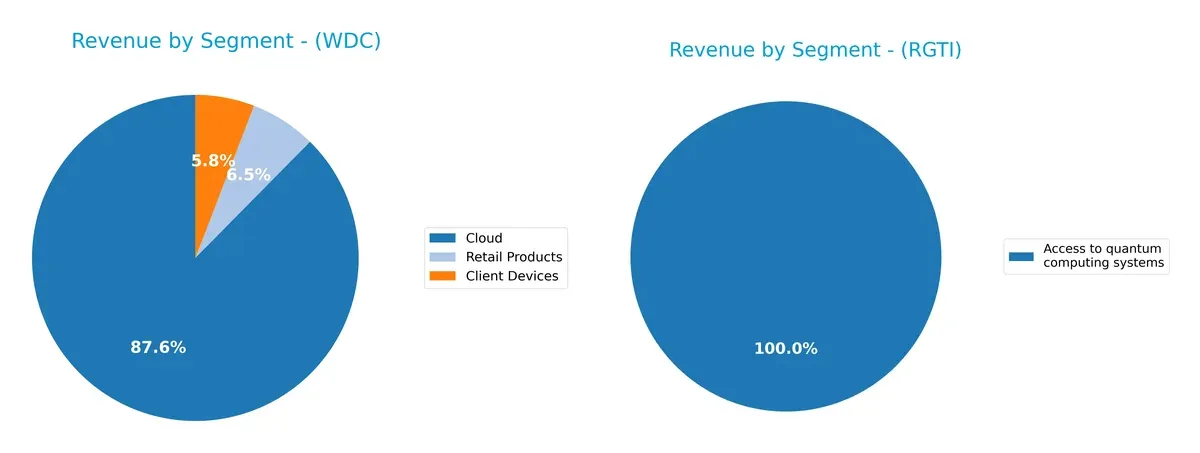

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Western Digital Corporation and Rigetti Computing diversify their income streams and reveals their primary sector bets:

Western Digital anchors its revenue heavily in Cloud at $8.3B and Client Devices at $556M in 2025, showing moderate diversification with Retail Products. Rigetti Computing relies almost entirely on Access to quantum computing systems, with $3.6M in 2024, revealing a concentrated revenue base. Western Digital’s broader mix reduces concentration risk, while Rigetti’s focus signals early-stage dependency and potential volatility in quantum tech adoption.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of Western Digital Corporation and Rigetti Computing, Inc.:

Western Digital Corporation Strengths

- Diverse revenue streams across Client Devices, Cloud, and Retail Products

- Strong profitability with 19.55% net margin and 35.04% ROE

- Favorable fixed asset turnover at 4.06

- Global presence in Asia, Americas, and EMEA regions

Rigetti Computing, Inc. Strengths

- Low debt levels with 0.07 debt-to-equity and 3.09% debt-to-assets

- Favorable quick ratio at 17.42 indicating liquidity

- Positive PE ratio despite losses

- Revenue from quantum computing access and collaborative research

Western Digital Corporation Weaknesses

- Elevated weighted average cost of capital at 12.21%

- Unfavorable price-to-book ratio at 4.14

- Low dividend yield at 0.2%

- Neutral liquidity metrics with current ratio at 1.08 and quick ratio at 0.84

Rigetti Computing, Inc. Weaknesses

- Large negative profitability with -1862.72% net margin and -158.77% ROE

- Negative return on invested capital at -24.91%

- Poor interest coverage at -60.75

- Low asset turnover at 0.04 and fixed asset turnover at 0.2

- High current ratio at 17.42 flagged as unfavorable

Western Digital shows operational strength through diversified revenue and solid profitability but faces some valuation and capital cost challenges. Rigetti struggles with profitability and asset efficiency but maintains strong liquidity and low leverage, reflecting early-stage investment risks.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only shield guarding long-term profits against relentless competitive erosion. Let’s dissect the moats of two tech firms:

Western Digital Corporation: Durable Cost Advantage

Western Digital leverages scale and manufacturing efficiency to sustain a cost advantage. Its consistent 9%+ ROIC above WACC confirms durable value creation. Expansion into enterprise SSDs in 2026 could deepen this moat.

Rigetti Computing, Inc.: Emerging Innovation Moat

Rigetti’s moat stems from proprietary quantum computing technology, distinct from Western Digital’s hardware scale. Despite negative ROIC, its rising profitability signals nascent competitive potential. Success in cloud integration could unlock future market disruption.

Verdict: Cost Leadership vs. Innovation Potential

Western Digital’s wide moat grounded in cost leadership currently outpaces Rigetti’s narrower, innovation-driven moat. WDC’s proven value creation better defends market share, while RGTI remains a high-risk, high-reward speculative play.

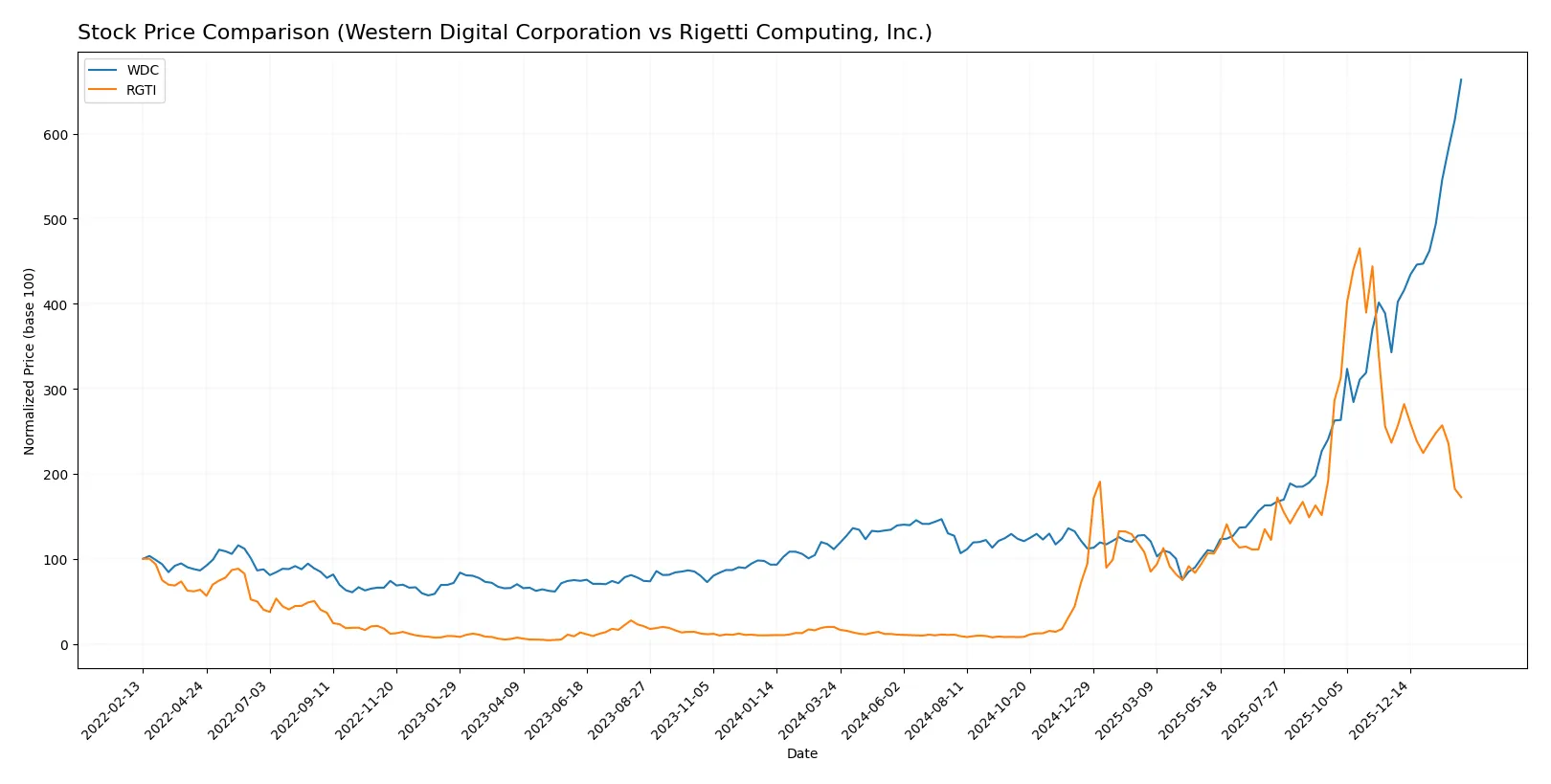

Which stock offers better returns?

The past year reveals stark contrasts in price momentum and trading dynamics between Western Digital Corporation and Rigetti Computing, Inc., highlighting divergent investor sentiment and performance trajectories.

Trend Comparison

Western Digital Corporation’s stock surged 496.3% over the past year, showing a bullish trend with accelerating gains. It reached a high of 269.41 and a low of 30.54, indicating significant volatility with a standard deviation of 52.49.

Rigetti Computing, Inc. gained 772.59% over the past year, also bullish but with decelerating momentum. Its price ranged between 0.75 and 46.38, showing lower volatility at a standard deviation of 11.24.

Comparing the two, Rigetti Computing delivered the highest overall market performance with a 772.59% gain, outpacing Western Digital’s 496.3% increase despite recent negative price movement.

Target Prices

Analysts show a clear bullish consensus for Western Digital and a moderate outlook for Rigetti Computing.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Western Digital Corporation | 205 | 340 | 286 |

| Rigetti Computing, Inc. | 30 | 50 | 38 |

Western Digital’s consensus target sits about 6% above the current price of 269, signaling upside potential. Rigetti’s target consensus of 38 suggests significant room to grow from its current 17.19, reflecting high expectations despite elevated risk.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Here are the institutional grades for Western Digital Corporation and Rigetti Computing, Inc.:

Western Digital Corporation Grades

The table below shows recent grades from major financial institutions for Western Digital Corporation.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Citigroup | Maintain | Buy | 2026-02-02 |

| Barclays | Maintain | Overweight | 2026-02-02 |

| Cantor Fitzgerald | Maintain | Overweight | 2026-01-30 |

| Wells Fargo | Maintain | Overweight | 2026-01-30 |

| Goldman Sachs | Maintain | Neutral | 2026-01-30 |

| Morgan Stanley | Maintain | Overweight | 2026-01-30 |

| TD Cowen | Maintain | Buy | 2026-01-30 |

| Wedbush | Maintain | Outperform | 2026-01-30 |

| Mizuho | Maintain | Outperform | 2026-01-27 |

| Morgan Stanley | Maintain | Overweight | 2026-01-22 |

Rigetti Computing, Inc. Grades

The table below summarizes recent grades from credible financial firms for Rigetti Computing, Inc.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| B. Riley Securities | Upgrade | Buy | 2026-01-22 |

| Rosenblatt | Maintain | Buy | 2026-01-21 |

| Wedbush | Maintain | Outperform | 2026-01-21 |

| B. Riley Securities | Maintain | Neutral | 2025-11-12 |

| Benchmark | Maintain | Buy | 2025-11-12 |

| B. Riley Securities | Downgrade | Neutral | 2025-11-03 |

| Benchmark | Maintain | Buy | 2025-10-07 |

| B. Riley Securities | Maintain | Buy | 2025-09-22 |

| Benchmark | Maintain | Buy | 2025-08-13 |

| Needham | Maintain | Buy | 2025-08-04 |

Which company has the best grades?

Western Digital consistently receives strong grades like Overweight and Outperform from multiple reputable firms. Rigetti shows a mix of Buy and Neutral grades with recent upgrades. Western Digital’s more stable and higher consensus grades suggest stronger institutional confidence, potentially attracting more risk-averse investors.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

Western Digital Corporation

- Established player in data storage with strong brand presence but faces intense competition from SSD and cloud storage rivals.

Rigetti Computing, Inc.

- Emerging quantum computing firm in a nascent, highly competitive market with uncertain adoption timelines and technological hurdles.

2. Capital Structure & Debt

Western Digital Corporation

- Moderate leverage with a debt-to-assets ratio of 36%, interest coverage ratio at 4.17, indicating manageable but notable debt service risk.

Rigetti Computing, Inc.

- Very low debt levels (3%), favorable debt-to-equity, but negative interest coverage suggests operational losses impair debt service capacity.

3. Stock Volatility

Western Digital Corporation

- Beta at 1.84 signals above-market volatility, with wide trading range reflecting cyclical demand in hardware.

Rigetti Computing, Inc.

- Beta at 1.70, high trading volume and price range imply significant stock price swings linked to speculative quantum sector risks.

4. Regulatory & Legal

Western Digital Corporation

- Operates globally; exposed to data privacy laws and semiconductor export controls that could impact supply chain and sales.

Rigetti Computing, Inc.

- Faces evolving regulations on quantum technology export and IP protection, with potential for increased compliance costs.

5. Supply Chain & Operations

Western Digital Corporation

- Complex global supply chain sensitive to semiconductor shortages and geopolitical tensions, but diversified manufacturing footprint.

Rigetti Computing, Inc.

- Highly specialized supply chain for quantum processors; operational scale is limited but vulnerable to supplier disruptions and tech delays.

6. ESG & Climate Transition

Western Digital Corporation

- Moderate ESG risks with ongoing pressure to reduce energy consumption in manufacturing and data centers.

Rigetti Computing, Inc.

- Emerging firm with limited ESG disclosures; quantum computing promises energy efficiency but faces scrutiny on material sourcing.

7. Geopolitical Exposure

Western Digital Corporation

- Significant exposure to US-China trade tensions affecting manufacturing and sales in Asia.

Rigetti Computing, Inc.

- Less exposed due to smaller scale but sensitive to US government policies on advanced technology development and export controls.

Which company shows a better risk-adjusted profile?

Western Digital’s main risk lies in moderate leverage and global supply chain complexity. Rigetti’s critical risk is severe operating losses reflected in poor profitability and interest coverage. Despite Western Digital’s volatility, its mature market position and financial strength offer a superior risk-adjusted profile. Rigetti’s speculative technology and fragile financials create elevated investment risk, underscored by a weak Piotroski score of 3 versus Western Digital’s strong 7.

Final Verdict: Which stock to choose?

Western Digital’s superpower lies in its proven ability to generate strong and growing returns on invested capital, reflecting a durable competitive advantage in data storage technology. Its point of vigilance is a modest liquidity cushion, which may require monitoring in volatile sectors. It suits portfolios targeting steady, aggressive growth with value discipline.

Rigetti Computing commands a strategic moat through cutting-edge quantum computing research, offering high innovation potential and low leverage risk. Relative to Western Digital, it presents greater volatility and financial uncertainty. Rigetti fits speculative growth portfolios willing to embrace early-stage technology risks for outsized future gains.

If you prioritize robust capital efficiency and consistent profitability, Western Digital outshines as a compelling choice due to its value creation and improving fundamentals. However, if you seek speculative exposure to frontier technology and can tolerate elevated risk, Rigetti offers superior innovation potential despite its financial challenges. Both present distinct analytical scenarios aligned with differing investor risk appetites.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Western Digital Corporation and Rigetti Computing, Inc. to enhance your investment decisions: