Home > Comparison > Healthcare > DGX vs RVTY

The strategic rivalry between Quest Diagnostics Incorporated and Revvity, Inc. defines the current trajectory of the healthcare diagnostics sector. Quest operates as a broad-based diagnostic services provider with an extensive patient network, while Revvity focuses on specialized instruments and solutions for life sciences and analytical markets. This analysis pits Quest’s scale against Revvity’s innovation, aiming to identify which corporate strategy delivers superior risk-adjusted returns for a diversified portfolio.

Table of contents

Companies Overview

Quest Diagnostics and Revvity stand as pivotal players in the medical diagnostics and research sector, shaping healthcare innovation.

Quest Diagnostics: Diagnostic Testing Powerhouse

Quest Diagnostics dominates the diagnostic testing market in the US and internationally. Its core revenue engine revolves around routine and advanced clinical testing delivered through a vast network of laboratories and patient service centers. In 2026, the company focuses strategically on expanding its diagnostic information services and enhancing IT solutions for healthcare organizations.

Revvity: Life Sciences and Diagnostics Innovator

Revvity operates globally, providing instruments and reagents for diagnostics, life sciences, and applied services markets. Its revenue model combines technology-driven solutions in genomics, oncology, and infectious disease testing. The company’s 2026 strategic emphasis lies in advancing genomic workflows and expanding its analytical technologies across diverse industries.

Strategic Collision: Similarities & Divergences

Both companies lead in medical diagnostics but diverge in focus—Quest Diagnostics leverages a broad testing network, while Revvity invests in cutting-edge genomic and analytical technologies. Their primary battleground is the diagnostics innovation space, competing for influence in healthcare and research markets. Quest offers a stable, service-driven investment profile; Revvity presents growth potential through technology leadership.

Income Statement Comparison

This table dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Quest Diagnostics (DGX) | Revvity (RVTY) |

|---|---|---|

| Revenue | 9.87B | 2.76B |

| Cost of Revenue | 6.63B | 1.43B |

| Operating Expenses | 1.90B | 912M |

| Gross Profit | 3.24B | 1.32B |

| EBITDA | 1.89B | 840M |

| EBIT | 1.40B | 412M |

| Interest Expense | 226M | 96M |

| Net Income | 871M | 296M |

| EPS | 7.8 | 2.41 |

| Fiscal Year | 2024 | 2024 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company operates more efficiently and converts revenue into profit with greater precision.

Quest Diagnostics Incorporated Analysis

Quest Diagnostics exhibits steady revenue growth, reaching $9.87B in 2024, up 6.7% year-over-year. Its gross margin remains favorable at 32.9%, while net margin holds strong at 8.8%. Despite a slight net margin decline, Quest improves operating efficiency, with EBIT growing 8.35% and EPS rising 2.26% in the latest year, signaling solid momentum.

Revvity, Inc. Analysis

Revvity reports $2.86B revenue in 2025, with 3.7% annual growth, but overall revenue has declined over five years. Its gross margin is notably robust at 53.1%, yet EBIT margin dropped to 11.95%. Net income and EPS fell sharply last year, reflecting operational challenges and compressed profitability despite maintaining a favorable interest expense ratio.

Margin Resilience vs. Growth Stability

Quest Diagnostics outperforms Revvity in revenue growth and operational momentum, maintaining consistent profitability and margin health. Revvity’s superior gross margin contrasts with its shrinking net income and earnings, exposing volatility. For investors prioritizing stable profit conversion and growth, Quest Diagnostics presents a more attractive fundamental profile.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Quest Diagnostics Incorporated (DGX) | Revvity, Inc. (RVTY) |

|---|---|---|

| ROE | 12.85% | 3.33% |

| ROIC | 6.96% | 2.82% |

| P/E | 19.23 | 45.32 |

| P/B | 2.47 | 1.51 |

| Current Ratio | 1.10 | 1.68 |

| Quick Ratio | 1.02 | 1.40 |

| D/E | 1.05 | 0.46 |

| Debt-to-Assets | 43.87% | 27.68% |

| Interest Coverage | 5.96 | 3.87 |

| Asset Turnover | 0.61 | 0.23 |

| Fixed Asset Turnover | 3.57 | 4.43 |

| Payout ratio | 38.00% | 13.57% |

| Dividend yield | 1.98% | 0.30% |

| Fiscal Year | 2024 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Ratios serve as a company’s DNA, uncovering hidden risks and operational strengths that drive investment decisions.

Quest Diagnostics Incorporated

Quest Diagnostics posts a solid 12.85% ROE and 8.82% net margin, reflecting steady profitability. Its P/E of 19.23 and P/B of 2.47 suggest a fairly valued stock, neither cheap nor stretched. The company rewards shareholders with a 1.98% dividend yield, indicating stable cash returns rather than aggressive reinvestment.

Revvity, Inc.

Revvity shows weak profitability with a 3.33% ROE and 8.46% net margin, signaling operational challenges. Its high P/E of 45.32 marks the stock as expensive relative to earnings. The minimal 0.3% dividend yield hints at limited direct shareholder returns, likely prioritizing R&D and growth initiatives instead.

Balanced Efficiency vs. Growth Risk

Quest Diagnostics offers a better balance of profitability and valuation, with consistent returns and moderate risk. Revvity’s profile fits investors seeking growth but willing to tolerate operational inefficiencies and a stretched valuation. Each appeals to distinct risk appetites.

Which one offers the Superior Shareholder Reward?

I compare Quest Diagnostics (DGX) and Revvity (RVTY) on dividends and buybacks. DGX offers a steady 2.0% dividend yield with a sustainable payout ratio around 38%, backed by strong free cash flow coverage (~68%). Its buyback program remains active, supporting shareholder returns. RVTY yields a mere 0.3%, with a low payout ratio near 13%, reflecting its growth focus and reinvestment in R&D. Buybacks are modest, less consistent, limiting immediate capital return. Historically, DGX’s mature distribution strategy balances income and buybacks, providing a more reliable total return. RVTY’s model bets on growth, but with higher risk and uncertain near-term rewards. For 2026, I favor DGX for superior shareholder reward due to sustainable dividends and disciplined buybacks.

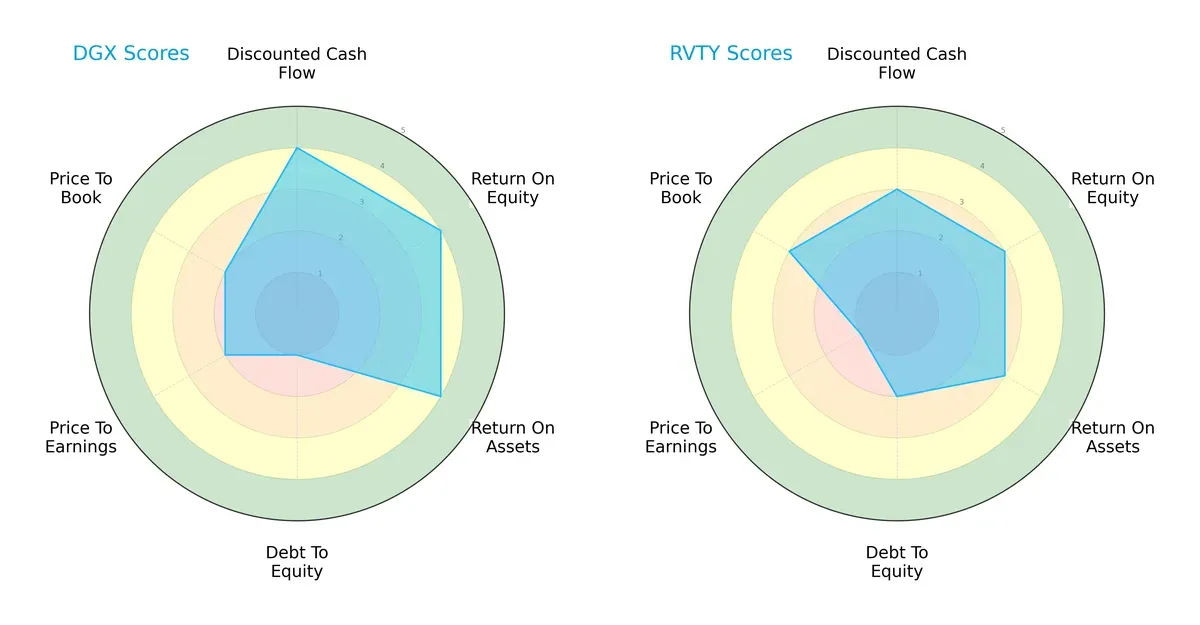

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Quest Diagnostics Incorporated and Revvity, Inc., highlighting their financial strengths and vulnerabilities:

Quest Diagnostics scores higher on DCF, ROE, and ROA, showing operational efficiency and cash flow strength. However, it carries a heavy debt burden, reflected in a very unfavorable Debt/Equity score. Revvity exhibits a more conservative leverage position but lags in profitability and valuation metrics. Quest has a sharper edge in earnings power, while Revvity maintains a slightly more balanced financial risk profile.

Bankruptcy Risk: Solvency Showdown

The Altman Z-Score delta signals a clear solvency advantage for Quest Diagnostics, firmly in the safe zone, while Revvity rests in the grey zone, implying higher bankruptcy risk in volatile markets:

Financial Health: Quality of Operations

Revvity edges out with a very strong Piotroski F-Score of 8, indicating robust internal financial health. Quest Diagnostics, scoring 7, remains strong but shows minor red flags compared to its peer:

How are the two companies positioned?

This section dissects the operational DNA of DGX and RVTY by comparing their revenue distribution and internal strengths and weaknesses. The objective is to confront their economic moats and identify which model offers the most resilient, sustainable competitive advantage today.

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Quest Diagnostics and Revvity diversify their income streams and reveals where their primary sector bets lie:

Quest Diagnostics anchors its revenue heavily on Diagnostic Information Services, generating $9.6B in 2024, signaling concentrated reliance. Revvity exhibits a more balanced mix with $1.5B from Diagnostics and $1.25B from Life Sciences, reflecting broader diversification. Quest’s dominance in diagnostics hints at ecosystem lock-in but heightens concentration risk. Revvity’s split revenue reduces vulnerability and supports flexibility amid market shifts.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of Quest Diagnostics Incorporated and Revvity, Inc.:

DGX Strengths

- Strong Diagnostic Information Services revenue at 9.6B USD

- Favorable WACC at 5.91% supports value creation

- Solid quick ratio at 1.02 indicates liquidity

- Favorable interest coverage ratio at 6.2

- Favorable fixed asset turnover at 3.57

RVTY Strengths

- Diverse revenue streams across Diagnostics and Life Sciences totaling 2.8B USD

- Favorable current ratio at 1.68 and quick ratio at 1.4 support liquidity

- Low debt-to-equity at 0.46 and debt-to-assets at 27.7% show conservative leverage

- Favorable fixed asset turnover at 4.43

- Slightly favorable WACC at 7.43%

DGX Weaknesses

- Elevated debt-to-equity at 1.05 signals higher financial risk

- Neutral net margin and ROE at 8.82% and 12.85% respectively limit profitability upside

- Neutral asset turnover at 0.61 suggests moderate efficiency

- Dividend yield modest at 1.98%

RVTY Weaknesses

- Unfavorable ROE and ROIC at 3.33% and 2.82% limit returns

- High PE ratio at 45.32 may reflect overvaluation risk

- Low net margin at 8.46% and asset turnover at 0.23 indicate efficiency challenges

- Unfavorable dividend yield at 0.3%

Quest Diagnostics shows strength in scale and efficient asset utilization but carries higher leverage risk. Revvity benefits from diversified business segments and strong liquidity but faces profitability and valuation concerns. Each company’s financial profile suggests differing strategic priorities in balancing growth, risk, and capital efficiency.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat alone protects long-term profits from relentless competition and market pressures. Let’s dissect how two leaders defend their turf:

Quest Diagnostics Incorporated: Intangible Assets & Brand Strength

Quest leverages powerful intangible assets and trusted brand recognition. This drives stable margins and a 14% EBIT margin. Yet, a declining ROIC signals looming margin pressure in 2026.

Revvity, Inc.: Innovation-Driven Technological Edge

Revvity depends on advanced diagnostic instruments and proprietary technologies, reflected in a robust 53% gross margin. However, a steep ROIC decline warns of shrinking value creation ahead.

Verdict: Intangible Assets vs. Innovation Edge

Quest Diagnostics holds a wider moat with enduring brand loyalty and service scale. Revvity’s innovation is promising but its value destruction signals vulnerability. Quest is better equipped to defend market share in 2026.

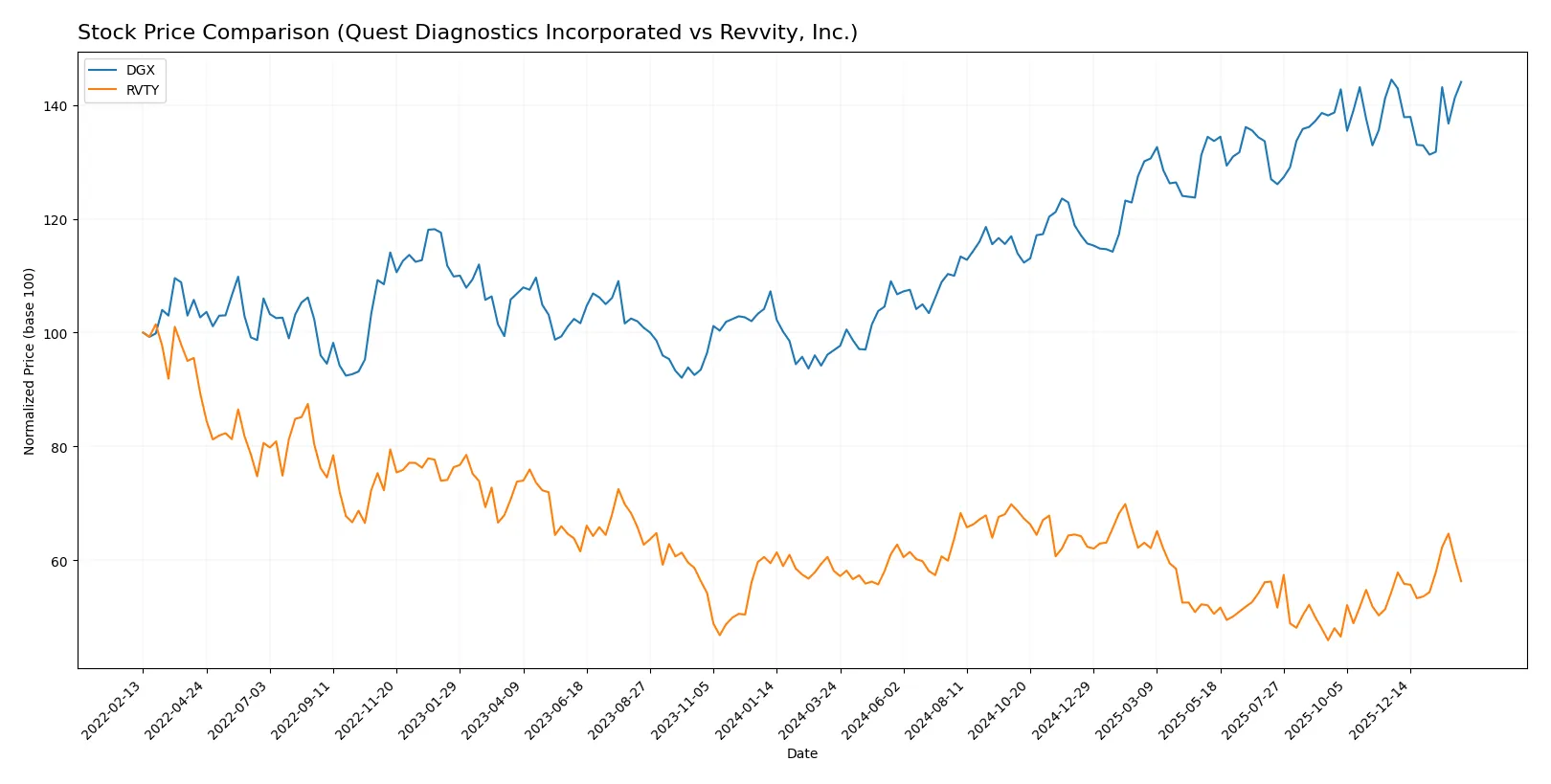

Which stock offers better returns?

The past year shows distinct price movements for Quest Diagnostics and Revvity, with Quest Diagnostics gaining sharply before recent stabilization, while Revvity has faced overall declines despite a late uptick.

Trend Comparison

Quest Diagnostics (DGX) recorded a strong 48.67% price increase over the past 12 months, marking a bullish trend with deceleration. Its price ranged from 128.28 to 191.25, reflecting significant overall gains.

Revvity (RVTY) experienced a 3.16% price decline in the same period, indicating a bearish trend with accelerating downward momentum. Prices fluctuated between 82.87 and 126.13, with a recent mild recovery of 3.38%.

Comparing both, Quest Diagnostics outperformed Revvity clearly, delivering the highest market returns and sustained buyer interest throughout the year.

Target Prices

Analysts project moderate upside potential for both Quest Diagnostics and Revvity, reflecting cautious optimism in the diagnostics sector.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Quest Diagnostics Incorporated | 190 | 215 | 203.1 |

| Revvity, Inc. | 105 | 129 | 115.14 |

Quest Diagnostics trades near its low target, suggesting limited immediate appreciation, while Revvity offers roughly 13% upside from current levels, indicating stronger growth expectations.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Quest Diagnostics Incorporated Grades

The following table summarizes recent institutional grades for Quest Diagnostics Incorporated:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Piper Sandler | Maintain | Neutral | 2025-10-27 |

| Barclays | Maintain | Equal Weight | 2025-10-22 |

| Truist Securities | Maintain | Hold | 2025-10-22 |

| Jefferies | Maintain | Buy | 2025-10-21 |

| Leerink Partners | Maintain | Outperform | 2025-10-21 |

| UBS | Maintain | Neutral | 2025-10-17 |

| Mizuho | Maintain | Outperform | 2025-10-17 |

| Evercore ISI Group | Maintain | In Line | 2025-10-08 |

| Barclays | Maintain | Equal Weight | 2025-10-02 |

| Baird | Downgrade | Neutral | 2025-08-25 |

Revvity, Inc. Grades

Institutional grades for Revvity, Inc. are listed in the table below:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Evercore ISI Group | Maintain | Outperform | 2026-02-03 |

| Jefferies | Maintain | Hold | 2026-02-03 |

| Wells Fargo | Maintain | Equal Weight | 2026-02-03 |

| TD Cowen | Maintain | Buy | 2026-02-03 |

| Barclays | Maintain | Overweight | 2026-02-03 |

| JP Morgan | Maintain | Neutral | 2026-02-03 |

| Wells Fargo | Maintain | Equal Weight | 2025-12-15 |

| Barclays | Maintain | Overweight | 2025-12-15 |

| Barclays | Maintain | Overweight | 2025-10-28 |

| Baird | Maintain | Outperform | 2025-10-28 |

Which company has the best grades?

Revvity, Inc. generally receives more positive grades, including multiple Outperform and Overweight ratings. Quest Diagnostics shows a mix with fewer Buy and Outperform calls and one recent downgrade. This difference may influence investor sentiment and portfolio positioning.

Risks specific to each company

The following categories identify critical pressure points and systemic threats facing Quest Diagnostics Incorporated and Revvity, Inc. in the 2026 market environment:

1. Market & Competition

Quest Diagnostics Incorporated

- Established leader in diagnostic services with broad patient base and network. Faces strong competition in advanced clinical testing.

Revvity, Inc.

- Focuses on diagnostics and life sciences solutions with diversified product segments but faces intense innovation-driven competition.

2. Capital Structure & Debt

Quest Diagnostics Incorporated

- Debt-to-equity ratio at 1.05 signals higher leverage, a moderate red flag despite solid interest coverage (6.2x).

Revvity, Inc.

- Lower debt-to-equity at 0.46 indicates stronger balance sheet; interest coverage is moderate (3.7x), requiring monitoring.

3. Stock Volatility

Quest Diagnostics Incorporated

- Beta of 0.675 suggests lower volatility, offering defensive qualities in turbulent markets.

Revvity, Inc.

- Beta of 1.089 signals higher volatility, reflecting sensitivity to market swings and growth expectations.

4. Regulatory & Legal

Quest Diagnostics Incorporated

- Operates under tight healthcare regulations; risk of compliance issues but long experience mitigates surprises.

Revvity, Inc.

- Exposed to evolving diagnostics and biotech regulations, increasing compliance complexity and potential legal challenges.

5. Supply Chain & Operations

Quest Diagnostics Incorporated

- Extensive network requires robust supply chain; potential disruption risks but proven operational scale provides resilience.

Revvity, Inc.

- Supply chain complexity higher due to diverse product lines; operational efficiency challenged by lower asset turnover.

6. ESG & Climate Transition

Quest Diagnostics Incorporated

- Moderate ESG exposure; healthcare services increasingly pressured to improve sustainability and social governance.

Revvity, Inc.

- Growing ESG demands in biotech and industrial sectors served; must adapt rapidly to climate-related regulations.

7. Geopolitical Exposure

Quest Diagnostics Incorporated

- Primarily US-focused with limited international risk, reducing geopolitical volatility.

Revvity, Inc.

- Global operations expose it to geopolitical risks, including trade tensions and regulatory shifts abroad.

Which company shows a better risk-adjusted profile?

Quest Diagnostics faces leverage concerns but benefits from stable operations, lower stock volatility, and a strong Altman Z-score in the safe zone. Revvity offers a healthier balance sheet and strong Piotroski score but endures higher market volatility, weaker profitability metrics, and an Altman Z-score in the grey zone. Quest Diagnostics demonstrates a better risk-adjusted profile due to its defensive traits and financial stability, despite some debt concerns. The key worry for Quest is its leverage, whereas Revvity’s greatest risk lies in market valuation and operational efficiency, underscored by its high P/E of 45.32 and lower asset turnover.

Final Verdict: Which stock to choose?

Quest Diagnostics (DGX) excels as a reliable cash generator with steady operational efficiency. Its main point of vigilance lies in a slightly elevated debt load, which could pressure financial flexibility. DGX suits investors seeking stable income and moderate growth within a defensive portfolio.

Revvity (RVTY) rides on a strategic moat of specialized life sciences innovation and recurring revenue streams. It offers a stronger liquidity profile and lower leverage compared to DGX, enhancing its risk posture. RVTY fits growth-oriented investors willing to navigate volatility for potential long-term rewards.

If you prioritize dependable cash flow and a defensive stance, Quest Diagnostics outshines due to its proven operational resilience. However, if you seek innovation-driven growth and better balance sheet stability, Revvity offers superior upside despite current profitability challenges. Each presents an analytical scenario tailored to distinct investor profiles.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Quest Diagnostics Incorporated and Revvity, Inc. to enhance your investment decisions: