Home > Comparison > Technology > SWKS vs ONTO

The strategic rivalry between Skyworks Solutions, Inc. and Onto Innovation Inc. shapes the semiconductor industry’s evolution. Skyworks operates as a broad-based semiconductor manufacturer serving diverse markets, while Onto Innovation specializes in precision process control tools and metrology solutions. This head-to-head contrasts scale and product breadth against niche technological expertise. This analysis will reveal which business model delivers superior risk-adjusted returns for a diversified portfolio in the ever-competitive tech sector.

Table of contents

Companies Overview

Skyworks Solutions and Onto Innovation both hold pivotal roles in the semiconductor industry, shaping technology’s backbone globally.

Skyworks Solutions, Inc.: Semiconductor Powerhouse

Skyworks Solutions dominates as a leading semiconductor manufacturer focused on analog and mixed-signal chips. Its revenue stems from diversified proprietary products including amplifiers, filters, and front-end modules sold across aerospace, automotive, and smartphone markets. In 2026, Skyworks sharpens its strategic focus on expanding high-performance components for connected devices, enhancing its broad product portfolio and global reach.

Onto Innovation Inc.: Process Control Innovator

Onto Innovation specializes in process control tools and analytical software that ensure semiconductor manufacturing quality and yield. Its core revenue comes from advanced inspection systems, lithography, and metrology solutions serving leading semiconductor fabs worldwide. The company’s 2026 strategy emphasizes scaling integrated factory-wide software suites to drive efficiency and precision in next-gen semiconductor production.

Strategic Collision: Similarities & Divergences

Both companies operate in semiconductors but differ sharply in focus: Skyworks champions component manufacturing, while Onto leads in process control technology. They compete indirectly in the semiconductor value chain, where product innovation meets manufacturing precision. Investors face distinct profiles—Skyworks offers broad market exposure with product diversity; Onto offers niche leadership in manufacturing efficiency and quality control.

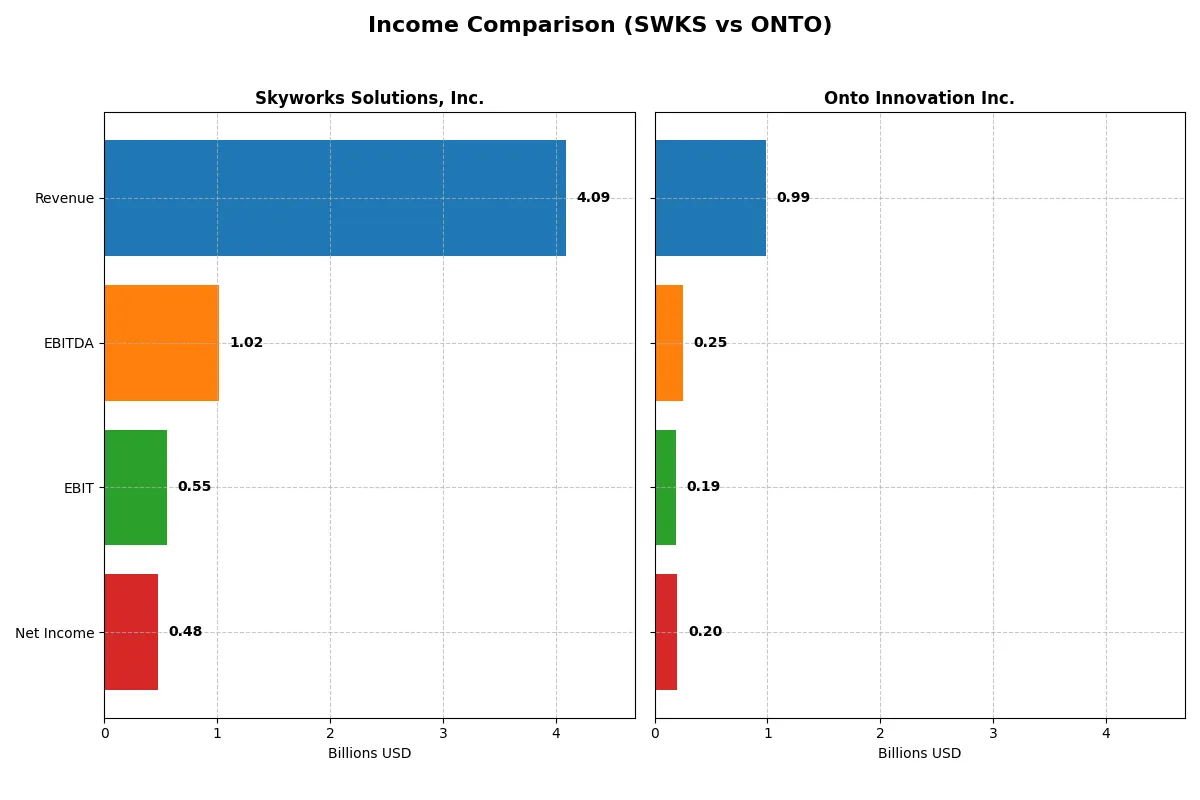

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Skyworks Solutions, Inc. (SWKS) | Onto Innovation Inc. (ONTO) |

|---|---|---|

| Revenue | 4.09B | 987M |

| Cost of Revenue | 2.40B | 472M |

| Operating Expenses | 1.18B | 328M |

| Gross Profit | 1.68B | 515M |

| EBITDA | 1.02B | 249M |

| EBIT | 554M | 187M |

| Interest Expense | 27M | 0 |

| Net Income | 477M | 202M |

| EPS | 3.09 | 4.09 |

| Fiscal Year | 2025 | 2024 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison exposes which company runs its financial engine with superior efficiency and stronger growth momentum.

Skyworks Solutions, Inc. Analysis

Skyworks Solutions’ revenue declined from 5.1B in 2021 to 4.1B in 2025, with net income plummeting from 1.5B to 477M. Its gross margin remains healthy at 41.2%, but net margin compressed to 11.7%, reflecting weakened profitability. The latest year shows deteriorating efficiency amid shrinking top line and bottom line.

Onto Innovation Inc. Analysis

Onto Innovation’s revenue grew steadily from 556M in 2020 to 987M in 2024, while net income surged from 31M to 202M. Its gross margin expanded to 52.2% and net margin climbed to 20.4%, indicating robust profitability. The latest fiscal year reveals strong momentum with double-digit growth across key income metrics.

Growth Resilience vs. Profitability Compression

Onto Innovation clearly outperforms Skyworks with consistent revenue and net income growth, alongside expanding margins. Skyworks shows margin strength but suffers from prolonged revenue and profit declines. For investors, Onto’s growth and improving profitability profile offers a more compelling and resilient earnings trajectory.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Skyworks Solutions (SWKS) | Onto Innovation (ONTO) |

|---|---|---|

| ROE | 8.29% | 10.47% |

| ROIC | 6.35% | 8.77% |

| P/E | 24.95 | 41.76 |

| P/B | 2.07 | 4.37 |

| Current Ratio | 2.33 | 8.69 |

| Quick Ratio | 1.76 | 7.00 |

| D/E | 0.21 | 0.01 |

| Debt-to-Assets | 15.20% | 0.72% |

| Interest Coverage | 18.45 | 0 |

| Asset Turnover | 0.52 | 0.47 |

| Fixed Asset Turnover | 2.95 | 7.16 |

| Payout ratio | 90.67% | 0% |

| Dividend yield | 3.63% | 0% |

| Fiscal Year | 2025 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios serve as a company’s DNA, unveiling hidden risks and operational excellence beneath headline numbers.

Skyworks Solutions, Inc.

Skyworks shows moderate profitability with an 8.3% ROE and 11.7% net margin, indicating steady core earnings. Its P/E of 24.95 and P/B of 2.07 suggest a fairly valued stock, not stretched in valuation. A 3.63% dividend yield rewards shareholders, reflecting a balanced capital allocation between payouts and reinvestment.

Onto Innovation Inc.

Onto posts a stronger 10.5% ROE and robust 20.4% net margin, signaling efficient profit generation. However, its P/E of 41.76 and P/B of 4.37 mark a premium valuation that may strain downside risk. The company pays no dividend, likely focusing on growth through R&D and operational expansion.

Balanced Efficiency vs. Premium Growth Valuation

Skyworks offers a more balanced risk-reward profile with reasonable valuation and steady dividends. Onto commands higher profitability but at a stretched valuation and no shareholder payouts. Investors seeking income and valuation discipline may prefer Skyworks, while those chasing growth might lean toward Onto.

Which one offers the Superior Shareholder Reward?

Skyworks Solutions, Inc. (SWKS) delivers a stronger shareholder reward in 2026 compared to Onto Innovation Inc. (ONTO). SWKS offers a 3.63% dividend yield with a payout ratio near 91%, supported by solid free cash flow coverage, signaling a mature, shareholder-friendly distribution policy. SWKS also runs active buybacks, enhancing total returns. ONTO pays no dividend, opting to reinvest all free cash flow into growth, reflected in its high price-to-earnings and price-to-free-cash-flow ratios above 39. While ONTO’s growth strategy could pay off long-term, its current valuation risks limit near-term reward. SWKS’s balanced dividends and buybacks provide a more sustainable, attractive total return profile today.

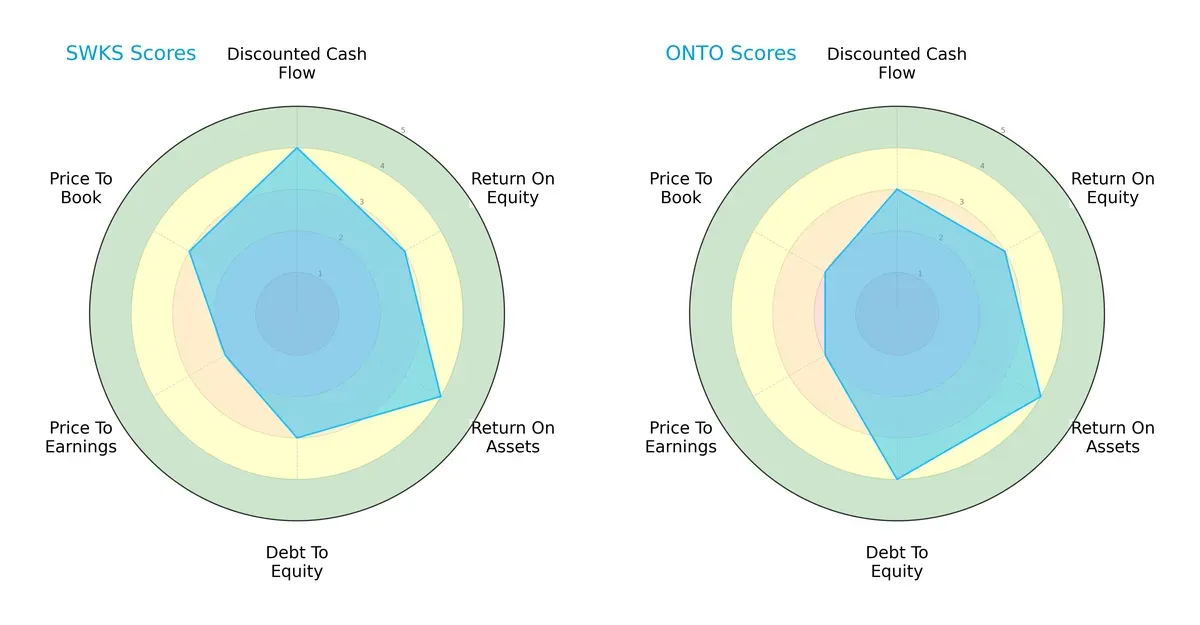

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Skyworks Solutions and Onto Innovation, highlighting their distinct financial strengths and weaknesses:

Skyworks excels in discounted cash flow (4) and return on assets (4), showing strong cash generation and asset efficiency. Onto Innovation leads in debt-to-equity (4), indicating a more conservative leverage profile. Both share moderate overall scores (3) and return on equity (3). Skyworks holds a slight edge in price-to-book (3) versus Onto’s lower valuation scores. I see Skyworks as more balanced across profitability and valuation metrics, while Onto relies on financial stability through lower leverage.

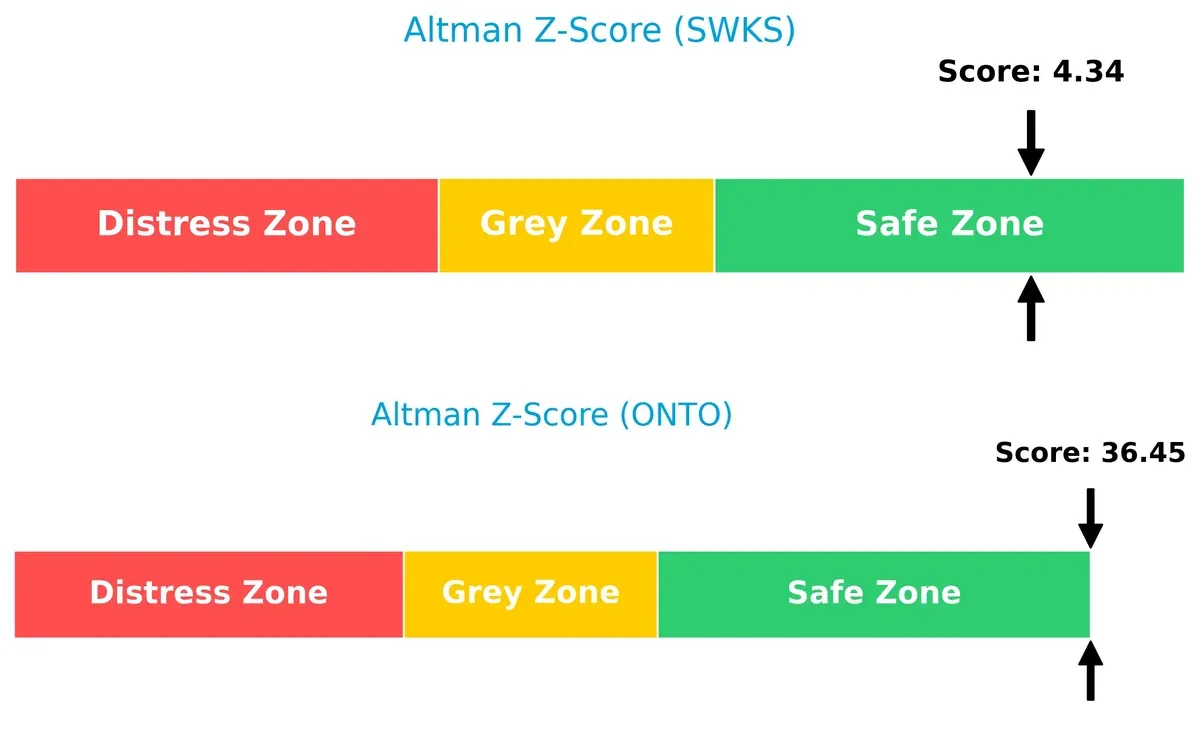

Bankruptcy Risk: Solvency Showdown

The Altman Z-Score gap favors Onto Innovation’s 36.45 versus Skyworks’ 4.34, both firmly in the safe zone, signaling robust solvency but vastly different risk buffers:

Onto’s exceptionally high score suggests an exceptionally low bankruptcy risk, ideal for conservative portfolios. Skyworks remains solid but closer to typical industry norms, implying moderate risk tolerance is required.

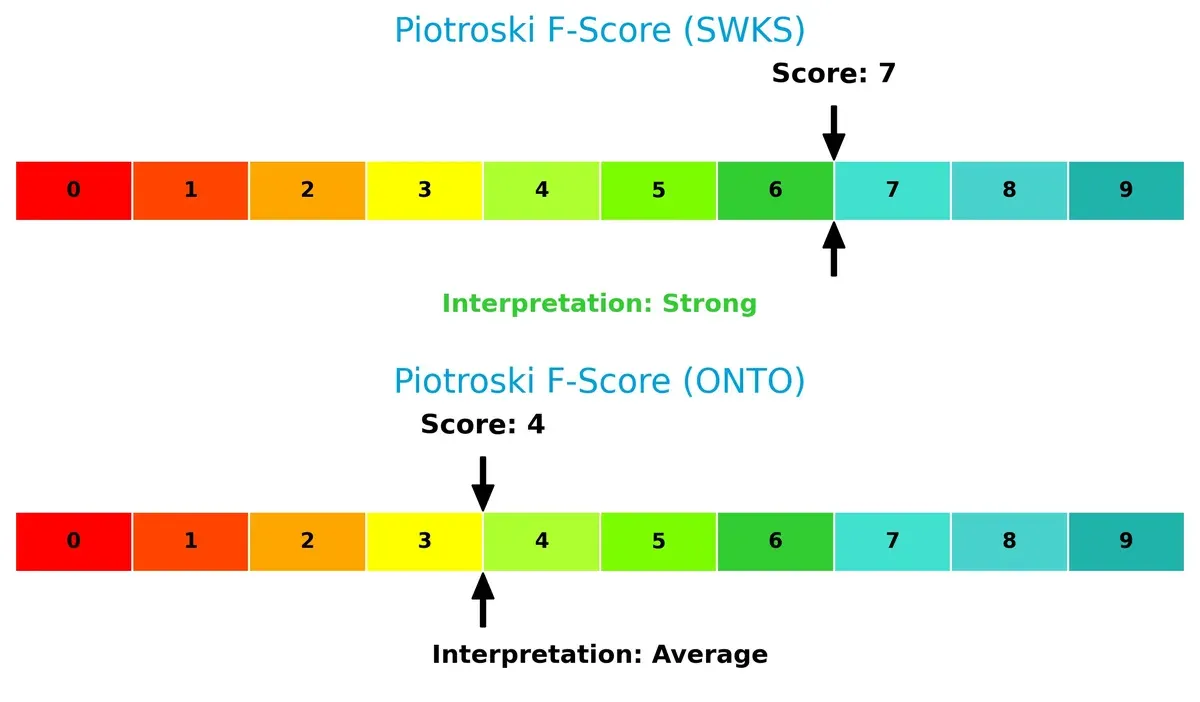

Financial Health: Quality of Operations

Skyworks scores a strong 7 on the Piotroski F-Score, outperforming Onto’s average 4, highlighting superior internal financial health and operational quality:

Skyworks demonstrates solid profitability, leverage, and efficiency metrics, while Onto’s middling score flags potential red flags in financial quality. I view Skyworks as the safer operational bet with fewer internal risks.

How are the two companies positioned?

This section dissects the operational DNA of Skyworks and Onto by comparing their revenue distribution and internal strengths and weaknesses. The goal is to confront their economic moats and identify which model yields the most resilient competitive advantage today.

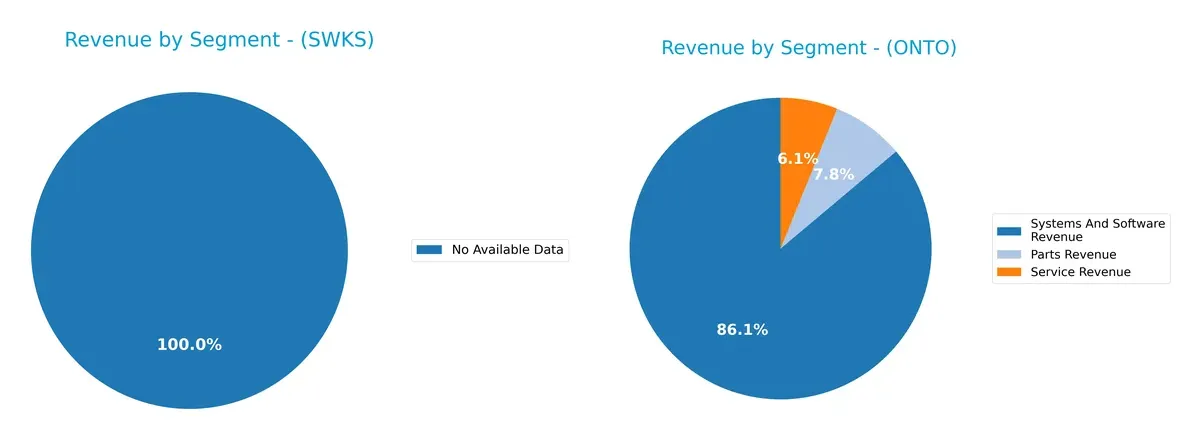

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Skyworks Solutions, Inc. and Onto Innovation Inc. diversify income streams and reveals each firm’s primary sector bets:

Skyworks lacks disclosed segment data, limiting direct comparison. Onto Innovation pivots heavily on Systems And Software Revenue, which dwarfs Parts ($77M) and Service ($60M) revenues in 2024. Onto’s concentrated bet on a dominant segment signals infrastructure dominance but also exposes concentration risk if market dynamics shift. Without Skyworks’ segmentation, Onto appears more focused, while Skyworks’ diversification remains unclear.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Skyworks Solutions, Inc. and Onto Innovation Inc.:

Skyworks Solutions Strengths

- Favorable net margin at 11.67%

- Strong current and quick ratios at 2.33 and 1.76

- Low debt-to-equity of 0.21

- Global presence with strong US and Asia sales

- Dividend yield of 3.63%

- Neutral ROIC/WACC balance

Onto Innovation Strengths

- Higher net margin at 20.43%

- Favorable quick ratio and debt levels

- Exceptional fixed asset turnover at 7.16

- Diverse product revenue streams

- Growing global footprint including Korea and Taiwan

- Favorable interest coverage ratio

Skyworks Solutions Weaknesses

- Unfavorable ROE at 8.29% below cost of capital

- Neutral asset turnover at 0.52 limits efficiency

- Neutral P/E and P/B ratios suggest moderate valuation

- Moderate global diversification concentrated in US and China

Onto Innovation Weaknesses

- Unfavorable WACC at 10.8% above ROIC

- Elevated P/E of 41.76 and P/B of 4.37 signal expensive valuation

- Unfavorable current ratio at 8.69 may indicate liquidity management issues

- Zero dividend yield limits income appeal

- Unfavorable asset turnover at 0.47

Skyworks Solutions shows solid financial health with prudent leverage and dividend policy but faces challenges in returns on equity and efficiency. Onto Innovation excels in profitability and asset utilization but contends with valuation and liquidity concerns that may influence its capital strategy.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only reliable shield protecting long-term profits from relentless competitive erosion. Let’s examine the key moats of two semiconductor players:

Skyworks Solutions, Inc. (SWKS): Legacy Scale and Product Breadth Moat

Skyworks relies on its expansive product portfolio and established customer base, creating moderate switching costs. However, its declining ROIC and shrinking margins signal a weakening moat. New markets in automotive and IoT could partially restore competitiveness in 2026 but face stiff rivals.

Onto Innovation Inc. (ONTO): Innovation-Driven Efficiency Moat

Onto’s competitive edge stems from its specialized process control technology and rapid ROIC growth, outperforming peers financially. Unlike Skyworks’ broad approach, Onto leverages innovation to deepen its moat. Expansion into advanced packaging and 3D metrology promises further market disruption in 2026.

Legacy Scale vs. Innovation Efficiency: The Moat Showdown

Skyworks’ moat is broader but eroding, marked by value destruction and revenue decline. Onto’s moat is narrower yet deepening, with accelerating profitability and growth. I believe Onto is better positioned to defend and expand its market share through focused innovation.

Which stock offers better returns?

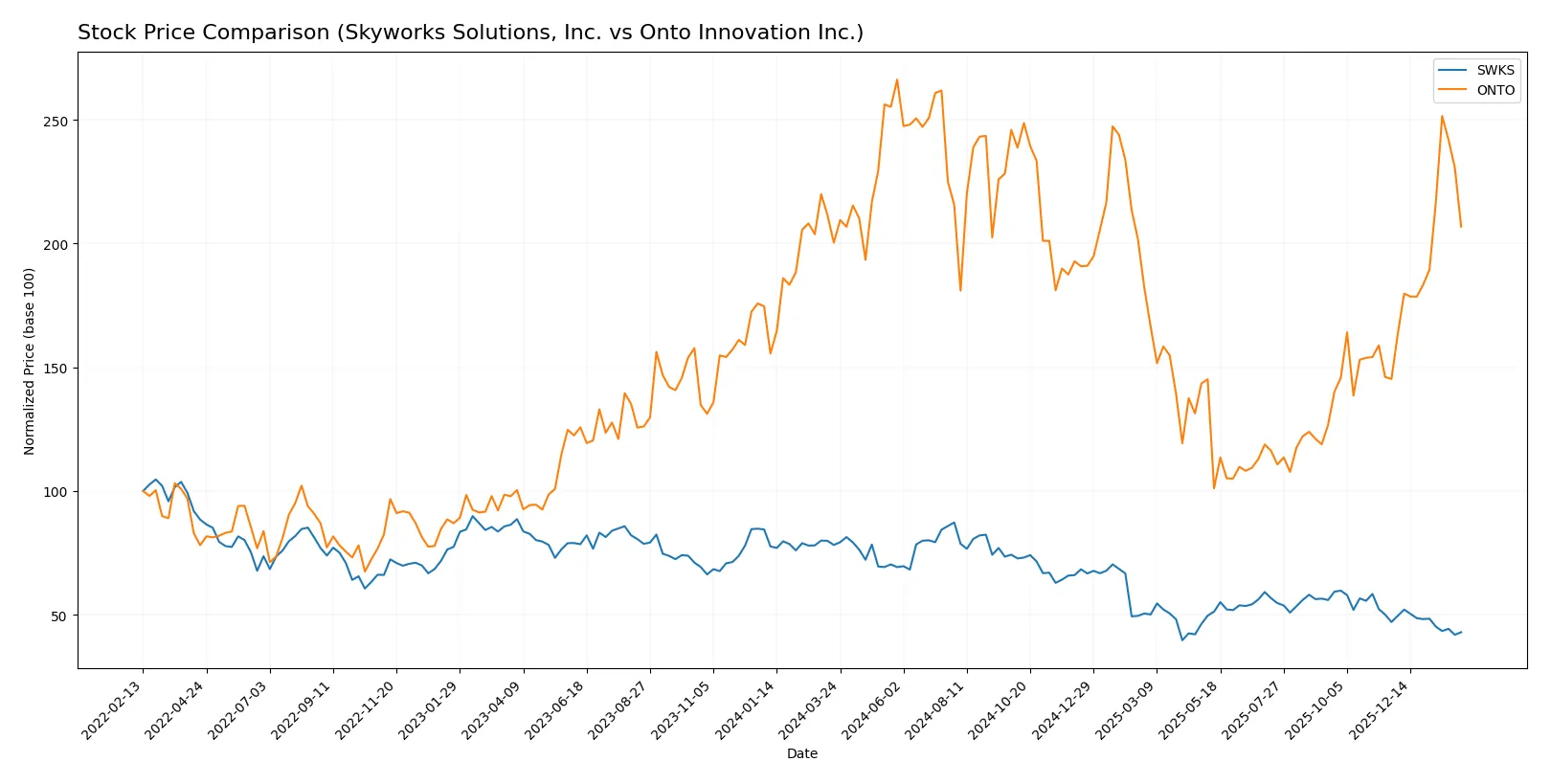

The past year reveals stark contrasts in price movement between Skyworks Solutions and Onto Innovation, highlighting divergent trading momentum and investor sentiment.

Trend Comparison

Skyworks Solutions’ stock shows a bearish trend over the past 12 months with a 45.1% price decline and decelerating downward momentum. The price ranged from a high of 116.18 to a low of 52.78, with moderate volatility at 16.52%.

Onto Innovation’s stock exhibits a bullish trend with a 3.24% gain over the same period, accelerating upwards. It experienced higher volatility at 42.97%, with prices spanning from 88.5 to 233.14, reflecting strong upward swings.

Comparing both, Onto Innovation outperforms Skyworks Solutions, delivering positive performance while Skyworks sharply declines, indicating Onto offers the superior market return over the past year.

Target Prices

Analysts present a wide but insightful consensus on target prices for Skyworks Solutions and Onto Innovation.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Skyworks Solutions, Inc. | 58 | 140 | 77.36 |

| Onto Innovation Inc. | 160 | 260 | 191.67 |

Skyworks trades near its low target at $57, suggesting potential undervaluation or caution. Onto Innovation sits close to its consensus at $181, reflecting balanced analyst expectations.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

The following tables summarize recent institutional grades assigned to both companies:

Skyworks Solutions, Inc. Grades

This table displays the latest grades from reputable financial institutions for Skyworks Solutions, Inc.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Stifel | Maintain | Hold | 2026-02-04 |

| Keybanc | Maintain | Overweight | 2026-02-04 |

| JP Morgan | Maintain | Neutral | 2026-02-04 |

| Benchmark | Maintain | Hold | 2026-02-04 |

| Morgan Stanley | Maintain | Equal Weight | 2026-02-02 |

| Mizuho | Maintain | Neutral | 2026-01-26 |

| B. Riley Securities | Maintain | Neutral | 2026-01-26 |

| Susquehanna | Maintain | Neutral | 2026-01-22 |

| UBS | Maintain | Neutral | 2026-01-20 |

| Mizuho | Upgrade | Neutral | 2025-11-11 |

Onto Innovation Inc. Grades

This table shows the most recent grades from established analysts for Onto Innovation Inc.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Needham | Maintain | Buy | 2026-01-20 |

| B. Riley Securities | Maintain | Buy | 2026-01-15 |

| Stifel | Maintain | Hold | 2026-01-14 |

| Needham | Maintain | Buy | 2026-01-06 |

| Jefferies | Maintain | Buy | 2025-12-15 |

| Needham | Maintain | Buy | 2025-11-18 |

| B. Riley Securities | Maintain | Buy | 2025-11-18 |

| Evercore ISI Group | Maintain | Outperform | 2025-11-05 |

| Oppenheimer | Maintain | Outperform | 2025-10-14 |

| Stifel | Maintain | Hold | 2025-10-13 |

Which company has the best grades?

Onto Innovation consistently earns Buy and Outperform ratings, signaling stronger analyst confidence. Skyworks mostly receives Neutral to Hold grades, indicating more cautious sentiment. This divergence may affect investor perception of growth potential and risk.

Risks specific to each company

The following categories identify critical pressure points and systemic threats facing Skyworks Solutions, Inc. and Onto Innovation Inc. in the 2026 market environment:

1. Market & Competition

Skyworks Solutions, Inc.

- Faces intense semiconductor competition; established IP portfolio supports moderate moat.

Onto Innovation Inc.

- Operates in niche process control tools; higher P/E and P/B indicate premium valuation risk.

2. Capital Structure & Debt

Skyworks Solutions, Inc.

- Maintains low debt-to-equity (0.21) and strong interest coverage (20.44x); prudent leverage.

Onto Innovation Inc.

- Virtually debt-free (D/E 0.01) with infinite interest coverage; very conservative capital structure.

3. Stock Volatility

Skyworks Solutions, Inc.

- Beta of 1.32 shows moderate market sensitivity; range $47.93–90.9 implies medium volatility.

Onto Innovation Inc.

- Higher beta at 1.48 and wider price range $85.88–227.07 indicate greater stock price swings.

4. Regulatory & Legal

Skyworks Solutions, Inc.

- Global semiconductor sales expose it to diverse regulatory regimes, including export controls.

Onto Innovation Inc.

- Specialized manufacturing tools may face fewer direct regulations but depend on customer compliance.

5. Supply Chain & Operations

Skyworks Solutions, Inc.

- Complex global supply chain exposes it to geopolitical and component scarcity risks.

Onto Innovation Inc.

- Smaller scale and specialized product line reduce supply chain complexity but increase dependency on few suppliers.

6. ESG & Climate Transition

Skyworks Solutions, Inc.

- Larger workforce and extensive manufacturing footprint require robust ESG policies; risk of lagging peers.

Onto Innovation Inc.

- Smaller workforce and focused operations may facilitate agile ESG adaptation but less public disclosure.

7. Geopolitical Exposure

Skyworks Solutions, Inc.

- Significant exposure to Asia-Pacific markets, including China, heightens geopolitical risk.

Onto Innovation Inc.

- Primarily US-based operations reduce direct geopolitical risks but may limit global growth.

Which company shows a better risk-adjusted profile?

Skyworks Solutions faces its greatest risk from intense global competition and supply chain complexity. Onto Innovation’s key risk lies in its stretched valuation and higher stock volatility. Despite these risks, Skyworks’ balanced capital structure and moderate volatility offer a more stable risk-adjusted profile. Onto’s higher beta and valuation multiple heighten investment risk amid uncertain market conditions. Recent ratio data reveal Skyworks’ strong liquidity and manageable debt, underscoring my preference for its steadier financial footing.

Final Verdict: Which stock to choose?

Skyworks Solutions’ superpower lies in its robust balance sheet and reliable dividend yield, signaling financial discipline. However, its declining profitability and shrinking moat present a point of vigilance. It suits investors with an appetite for turnaround potential in a mature semiconductor portfolio.

Onto Innovation benefits from a strategic moat rooted in accelerating profitability and strong asset efficiency. Its high valuation and long operating cycle introduce some caution but offer relative safety compared to Skyworks. This makes it attractive for portfolios focused on growth with a premium on innovation.

If you prioritize stable cash generation and income, Skyworks Solutions presents a compelling scenario despite its current challenges. However, if you seek dynamic growth and expanding profitability, Onto Innovation outshines with better momentum and operational leverage. Both require careful risk management given their contrasting profiles.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Skyworks Solutions, Inc. and Onto Innovation Inc. to enhance your investment decisions: