In the fast-evolving semiconductor industry, Onto Innovation Inc. and SkyWater Technology, Inc. stand out as dynamic players with distinct approaches to innovation and market presence. Onto Innovation focuses on advanced process control tools and metrology, while SkyWater emphasizes semiconductor manufacturing services and co-development. Their overlapping sectors and growth strategies make them compelling choices for investors seeking exposure to semiconductor technology. This article will help you decide which company holds the most promise for your portfolio.

Table of contents

Companies Overview

I will begin the comparison between Onto Innovation Inc. and SkyWater Technology, Inc. by providing an overview of these two companies and their main differences.

Onto Innovation Inc. Overview

Onto Innovation Inc. focuses on developing and manufacturing process control tools for the semiconductor industry, including macro defect inspection, 2D/3D optical metrology, lithography, and analytical software. The company serves advanced packaging device manufacturers and other industrial applications globally. Founded in 1940 and headquartered in Massachusetts, Onto Innovation operates with 1,551 employees and trades on the NYSE.

SkyWater Technology, Inc. Overview

SkyWater Technology, Inc. provides semiconductor development and manufacturing services, including engineering and process support for silicon-based analog, mixed-signal, power discrete, and rad-hard integrated circuits. It supports industries such as aerospace, defense, automotive, and consumer electronics. Established in 2017, headquartered in Minnesota, SkyWater employs 702 people and is listed on NASDAQ Capital Market.

Key similarities and differences

Both Onto and SkyWater operate in the semiconductor sector within the US technology industry, offering semiconductor-related products and services. Onto focuses on process control tools and software, while SkyWater specializes in semiconductor manufacturing and co-development services. Onto is a more established company with a larger workforce and market cap of about 10.7B USD, compared to SkyWater’s 1.5B USD with a higher beta, indicating greater price volatility.

Income Statement Comparison

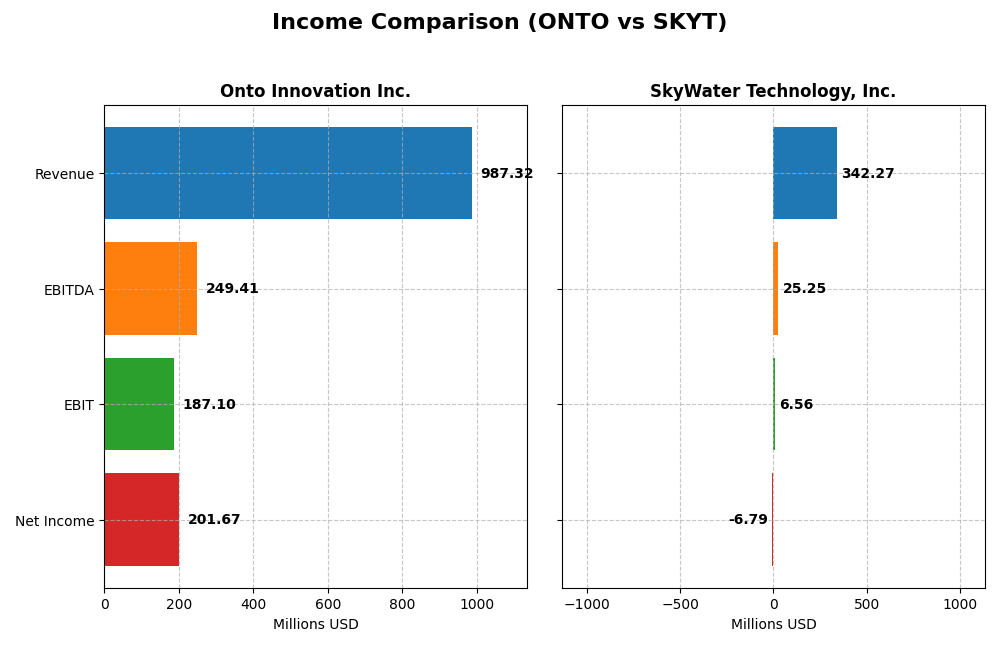

This table presents a side-by-side comparison of key income statement metrics for Onto Innovation Inc. and SkyWater Technology, Inc. for the fiscal year 2024.

| Metric | Onto Innovation Inc. | SkyWater Technology, Inc. |

|---|---|---|

| Market Cap | 10.7B | 1.54B |

| Revenue | 987M | 342M |

| EBITDA | 249M | 25.3M |

| EBIT | 187M | 6.56M |

| Net Income | 202M | -6.79M |

| EPS | 4.09 | -0.14 |

| Fiscal Year | 2024 | 2024 |

Income Statement Interpretations

Onto Innovation Inc.

Onto Innovation’s revenue rose from $557M in 2020 to $987M in 2024, reflecting a 77% growth over five years. Net income expanded significantly, surging 550% to $202M in 2024. Margins improved steadily, with a gross margin above 52% and net margin reaching 20.4%. The latest year showed strong momentum, with revenue growth at 21% and a 37.5% increase in net margin, signaling robust profitability enhancement.

SkyWater Technology, Inc.

SkyWater’s revenue climbed from $140M in 2020 to $342M in 2024, marking a 144% increase over five years. Despite top-line growth, net income remained negative at -$6.8M in 2024, though improved from earlier losses. Gross margin held around 20%, but net margin lingered at -2%, reflecting ongoing profitability challenges. The 2024 fiscal year showed favorable EBIT growth of 144%, indicating operational improvements despite continued net losses.

Which one has the stronger fundamentals?

Onto Innovation displays stronger fundamentals given its consistent profitability, expanding margins, and substantial net income growth. SkyWater, while exhibiting rapid revenue expansion and operational gains, faces ongoing net losses and negative net margins. The overall income statement evaluations favor Onto Innovation’s stability and margin improvements, contrasting with SkyWater’s mixed profitability metrics.

Financial Ratios Comparison

The table below compares key financial ratios of Onto Innovation Inc. and SkyWater Technology, Inc. based on their most recent full fiscal year data for 2024.

| Ratios | Onto Innovation Inc. (ONTO) | SkyWater Technology, Inc. (SKYT) |

|---|---|---|

| ROE | 10.47% | -11.79% |

| ROIC | 8.77% | 3.40% |

| P/E | 41.76 | -100.26 |

| P/B | 4.37 | 11.82 |

| Current Ratio | 8.69 | 0.86 |

| Quick Ratio | 7.00 | 0.76 |

| D/E | 0.008 | 1.33 |

| Debt-to-Assets | 0.72% | 24.46% |

| Interest Coverage | 0 | 0.74 |

| Asset Turnover | 0.47 | 1.09 |

| Fixed Asset Turnover | 7.16 | 2.07 |

| Payout ratio | 0% | 0% |

| Dividend yield | 0% | 0% |

Interpretation of the Ratios

Onto Innovation Inc.

Onto Innovation shows a mixed profile with 43% favorable and 43% unfavorable ratios, resulting in a neutral overall rating. Strengths include a high current ratio of 8.69 and low debt-to-equity of 0.01, indicating solid liquidity and leverage control. However, a high PE of 41.76 and price-to-book of 4.37 signal possible overvaluation risks. The company does not currently pay dividends, likely prioritizing reinvestment in growth and innovation.

SkyWater Technology, Inc.

SkyWater Technology presents predominantly unfavorable ratios, with 71% flagged negatively and only 21% favorable, leading to an unfavorable overall assessment. Weaknesses include a negative net margin of -1.98%, a low current ratio of 0.86, and high debt-to-equity at 1.33, suggesting liquidity and solvency concerns. The absence of dividend payments reflects its current negative profitability and focus on reinvestment amid operational challenges.

Which one has the best ratios?

Comparing both, Onto Innovation holds the advantage with a more balanced ratio distribution and stronger liquidity and leverage metrics. SkyWater Technology’s financials are weaker, marked by negative profitability and liquidity shortfalls. Consequently, Onto Innovation demonstrates relatively better financial stability and operational efficiency based on the available ratio analysis.

Strategic Positioning

This section compares the strategic positioning of Onto Innovation Inc. and SkyWater Technology, Inc. based on market position, key segments, and exposure to technological disruption:

Onto Innovation Inc.

- Market leader in process control tools with a $10.7B market cap and moderate competitive pressure.

- Focuses on process control tools, software, and device packaging serving diverse semiconductor applications.

- Exposure includes lithography systems and advanced packaging, with ongoing innovation in process control software.

SkyWater Technology, Inc.

- Smaller $1.5B market cap firm with high beta, facing strong competitive dynamics.

- Concentrates on semiconductor development and manufacturing services for various industries.

- Provides engineering and manufacturing services, co-developing technologies with customers.

Onto Innovation Inc. vs SkyWater Technology, Inc. Positioning

Onto Innovation pursues a diversified strategy across hardware, software, and services with a large market presence. SkyWater concentrates on semiconductor manufacturing services and co-innovation, operating at a smaller scale but serving multiple industrial sectors.

Which has the best competitive advantage?

Both companies have a slightly unfavorable MOAT status due to ROIC below WACC but show improving profitability trends. Onto Innovation’s larger scale and diversified portfolio may provide a more stable competitive base than SkyWater’s narrower focus.

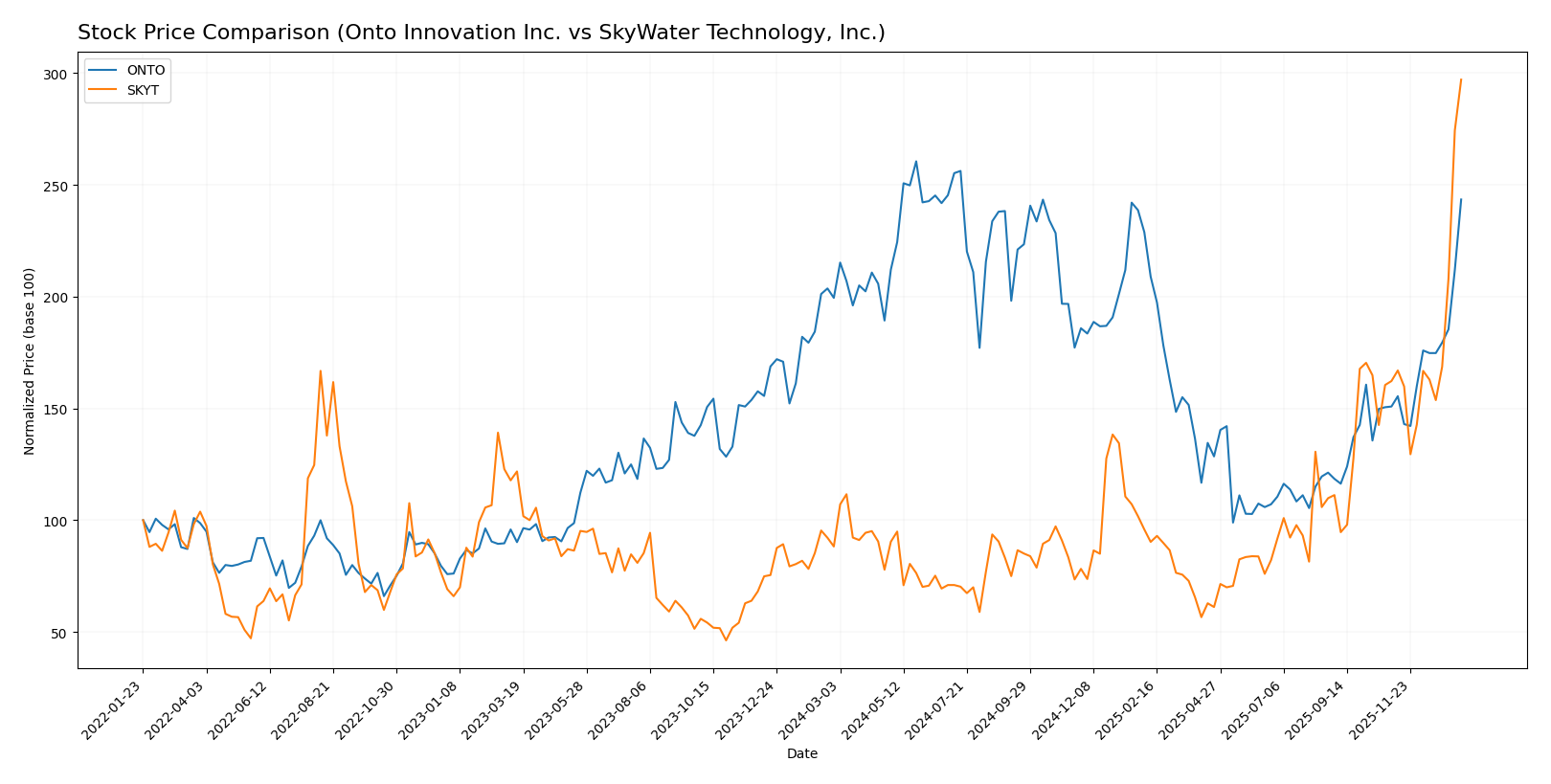

Stock Comparison

The stock price chart reveals significant bullish momentum for both Onto Innovation Inc. and SkyWater Technology, Inc. over the past year, with marked acceleration in price appreciation and increasing trading volumes reflecting strong buyer dominance.

Trend Analysis

Onto Innovation Inc. (ONTO) experienced a bullish trend over the past 12 months with a 22.07% price increase, showing acceleration and a high volatility level (std deviation 42.61). The stock hit a low of 88.5 and a high of 233.14.

SkyWater Technology, Inc. (SKYT) demonstrated a stronger bullish trend, surging 236.8% in the same period with acceleration and low volatility (std deviation 4.41). The stock’s range was from 6.1 to 32.03, indicating steady growth.

Comparing both, SKYT delivered the highest market performance with a substantially larger percentage gain, while ONTO showed greater price volatility and a smaller but solid upward trend.

Target Prices

The current analyst consensus target prices suggest mixed valuation perspectives for Onto Innovation Inc. and SkyWater Technology, Inc.

| Company | Target High | Target Low | Consensus |

|---|---|---|---|

| Onto Innovation Inc. | 200 | 160 | 178 |

| SkyWater Technology, Inc. | 25 | 25 | 25 |

Onto Innovation’s consensus target of 178 is below its current price of 217.85, indicating potential overvaluation or market optimism. SkyWater’s target at 25 is also below its current price of 32.03, suggesting a cautious outlook.

Analyst Opinions Comparison

This section compares analysts’ ratings and grades for Onto Innovation Inc. and SkyWater Technology, Inc.:

Rating Comparison

ONTO Rating

- Rating: B+ with a very favorable status.

- Discounted Cash Flow Score: Moderate at 3, indicating average valuation outlook.

- ROE Score: Moderate at 3, showing average efficiency in generating equity profit.

- ROA Score: Favorable at 4, reflecting effective asset utilization.

- Debt To Equity Score: Favorable at 4, indicating lower financial risk.

- Overall Score: Moderate at 3, summarizing average financial standing.

SKYT Rating

- Rating: B+ with a very favorable status.

- Discounted Cash Flow Score: Very unfavorable at 1, signaling potential overvaluation concerns.

- ROE Score: Very favorable at 5, indicating high profitability from shareholders’ equity.

- ROA Score: Very favorable at 5, showing excellent asset efficiency.

- Debt To Equity Score: Very unfavorable at 1, suggesting higher financial leverage risk.

- Overall Score: Moderate at 3, summarizing average financial standing.

Which one is the best rated?

Both Onto and SkyWater share the same overall rating of B+ and moderate overall score of 3. SkyWater excels in ROE and ROA with very favorable scores but has very unfavorable scores in discounted cash flow and debt-to-equity, unlike Onto’s more balanced profile.

Scores Comparison

Here is a comparison of Onto Innovation Inc. and SkyWater Technology, Inc. based on their financial scores:

ONTO Scores

- Altman Z-Score: 34.16, indicating a safe zone with very low bankruptcy risk.

- Piotroski Score: 4, reflecting average financial strength and value potential.

SKYT Scores

- Altman Z-Score: 2.20, placing it in the grey zone with moderate bankruptcy risk.

- Piotroski Score: 5, showing slightly better average financial strength.

Which company has the best scores?

Based on the provided scores, Onto Innovation has a significantly higher Altman Z-Score indicating stronger financial stability. SkyWater Technology has a marginally better Piotroski Score but remains in the average range. Overall, Onto Innovation shows greater safety from bankruptcy risk.

Grades Comparison

Here is a detailed comparison of recent grades assigned to Onto Innovation Inc. and SkyWater Technology, Inc.:

Onto Innovation Inc. Grades

The following table summarizes recent analyst grades for Onto Innovation Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Stifel | Maintain | Hold | 2026-01-14 |

| Needham | Maintain | Buy | 2026-01-06 |

| Jefferies | Maintain | Buy | 2025-12-15 |

| B. Riley Securities | Maintain | Buy | 2025-11-18 |

| Needham | Maintain | Buy | 2025-11-18 |

| Evercore ISI Group | Maintain | Outperform | 2025-11-05 |

| Oppenheimer | Maintain | Outperform | 2025-10-14 |

| Stifel | Maintain | Hold | 2025-10-13 |

| B. Riley Securities | Maintain | Buy | 2025-10-10 |

| Jefferies | Upgrade | Buy | 2025-09-23 |

Onto Innovation has consistently maintained a majority of Buy and Outperform ratings, with some Hold grades, indicating a generally positive analyst outlook.

SkyWater Technology, Inc. Grades

The following table summarizes recent analyst grades for SkyWater Technology, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Needham | Maintain | Buy | 2025-11-06 |

| Piper Sandler | Maintain | Overweight | 2025-11-06 |

| TD Cowen | Maintain | Buy | 2025-11-06 |

| Needham | Maintain | Buy | 2025-08-07 |

| Needham | Maintain | Buy | 2025-05-08 |

| Needham | Maintain | Buy | 2025-02-27 |

| Needham | Maintain | Buy | 2024-11-11 |

| Piper Sandler | Maintain | Overweight | 2024-10-25 |

| Piper Sandler | Maintain | Overweight | 2024-08-08 |

| Needham | Maintain | Buy | 2024-05-09 |

SkyWater Technology’s grades show a consistent pattern of Buy and Overweight ratings, reflecting steady analyst confidence.

Which company has the best grades?

Both Onto Innovation Inc. and SkyWater Technology, Inc. have predominantly Buy-oriented grades, but Onto Innovation includes Outperform ratings, suggesting a slightly stronger analyst conviction. This difference could influence investors seeking more bullish analyst sentiment.

Strengths and Weaknesses

Below is a comparative overview of Onto Innovation Inc. (ONTO) and SkyWater Technology, Inc. (SKYT) based on key business and financial criteria.

| Criterion | Onto Innovation Inc. (ONTO) | SkyWater Technology, Inc. (SKYT) |

|---|---|---|

| Diversification | Strong product mix: Systems & Software dominate with $850M revenue, supported by Parts and Services segments. | More service-oriented: Advanced Technology Services and Wafer Services with less product diversification. |

| Profitability | Positive net margin at 20.43%, ROIC neutral at 8.77%, but WACC unfavorable at 10.66%. | Negative net margin (-1.98%), ROIC low at 3.4%, WACC very high at 19.8%, indicating ongoing losses. |

| Innovation | Growing ROIC trend (+344%), indicating improving operational efficiency and innovation impact despite current value shedding. | Also shows growing ROIC (+171%) but overall value destruction; innovation improving but not yet profitable. |

| Global presence | Established global systems and software footprint implied by large revenue scale. | Smaller scale with focus on specialized technology services, likely more regional. |

| Market Share | Large and growing Systems and Software segment suggests strong market share in semiconductor equipment. | Niche market presence with wafer and technology services; smaller market share in comparison. |

Key takeaways: Onto Innovation shows stronger diversification and profitability with improving innovation metrics, although it currently sheds value relative to cost of capital. SkyWater is less diversified and less profitable, facing higher risks but showing some positive innovation trends. Careful risk management is advised for both, with Onto being the more stable choice currently.

Risk Analysis

Below is a comparative table outlining key risks for Onto Innovation Inc. (ONTO) and SkyWater Technology, Inc. (SKYT) based on the most recent 2024 data.

| Metric | Onto Innovation Inc. (ONTO) | SkyWater Technology, Inc. (SKYT) |

|---|---|---|

| Market Risk | Beta 1.46 (moderate volatility) | Beta 3.49 (high volatility) |

| Debt level | Very low debt (D/E 0.01) | High debt (D/E 1.33) |

| Regulatory Risk | Moderate (semiconductor industry) | Moderate to high (defense & aerospace sector) |

| Operational Risk | Stable operations, 1551 employees | Smaller scale, 702 employees, growth challenges |

| Environmental Risk | Industry standard compliance | Potential higher due to manufacturing scale |

| Geopolitical Risk | Moderate exposure, global supply chains | Elevated due to aerospace/defense clients |

The most significant risks differ notably: SkyWater’s high debt and volatility present elevated financial and market risks, while Onto Innovation’s risks are more balanced but include valuation concerns. SkyWater’s Altman Z-score in the grey zone indicates moderate bankruptcy risk, unlike Onto’s safe zone score, reinforcing cautious stance on SkyWater.

Which Stock to Choose?

Onto Innovation Inc. (ONTO) shows a strong income evolution with a 21.01% revenue growth in 2024 and consistently favorable profitability ratios, including a 20.43% net margin. It maintains very low debt levels and receives a very favorable B+ rating, though some valuation ratios like P/E and P/B appear less attractive.

SkyWater Technology, Inc. (SKYT) reports positive revenue growth of 19.39% in 2024 but struggles with negative net margins and high debt ratios. Its financial ratios are mostly unfavorable, reflecting ongoing value destruction despite improving profitability, yet it also holds a B+ rating with mixed score components.

Investors focused on stable profitability and stronger financial health might find ONTO’s metrics more favorable, while those with higher risk tolerance and seeking potential turnaround opportunities could interpret SKYT’s accelerating growth and improving ROIC as a sign of emerging value. Both companies show growing ROIC but currently shed value relative to cost of capital.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Onto Innovation Inc. and SkyWater Technology, Inc. to enhance your investment decisions: