Home > Comparison > Industrials > NSC vs WAB

The strategic rivalry between Norfolk Southern Corporation and Westinghouse Air Brake Technologies Corporation shapes the competitive landscape of the industrial railroads sector. Norfolk Southern operates as a capital-intensive rail transportation provider, moving diverse freight across a vast U.S. network. In contrast, Westinghouse Air Brake focuses on high-tech rail equipment manufacturing and services globally. This analysis evaluates which business model delivers superior risk-adjusted returns for a diversified portfolio amid evolving industry dynamics.

Table of contents

Companies Overview

Norfolk Southern and Westinghouse Air Brake Technologies dominate critical segments of the U.S. rail industry.

Norfolk Southern Corporation: Leading U.S. Rail Transporter

Norfolk Southern operates one of the largest rail networks, moving raw materials and finished goods across 19,300 route miles in 22 states. Its core revenue stems from freight transportation of agriculture, chemicals, metals, and automotive products. In 2026, the company focuses on optimizing its intermodal network and enhancing port freight capabilities to sustain competitive momentum.

Westinghouse Air Brake Technologies Corporation: Rail Technology Innovator

Westinghouse Air Brake Technologies excels in supplying technology-driven components and services to freight and passenger rail sectors globally. It generates revenue through manufacturing and servicing braking systems, locomotives, and transit vehicles. The firm’s 2026 strategy centers on expanding positive train control technologies and modernizing transit fleets to capture growing public transit demand.

Strategic Collision: Similarities & Divergences

Norfolk Southern emphasizes a broad transportation network, while Westinghouse invests in specialized rail technology and equipment. Both compete primarily in the freight rail ecosystem but target different value chain segments—transportation versus equipment manufacturing. Their distinct focuses translate into diverse investment profiles: one leverages asset-intensive logistics, the other innovation in rail safety and modernization.

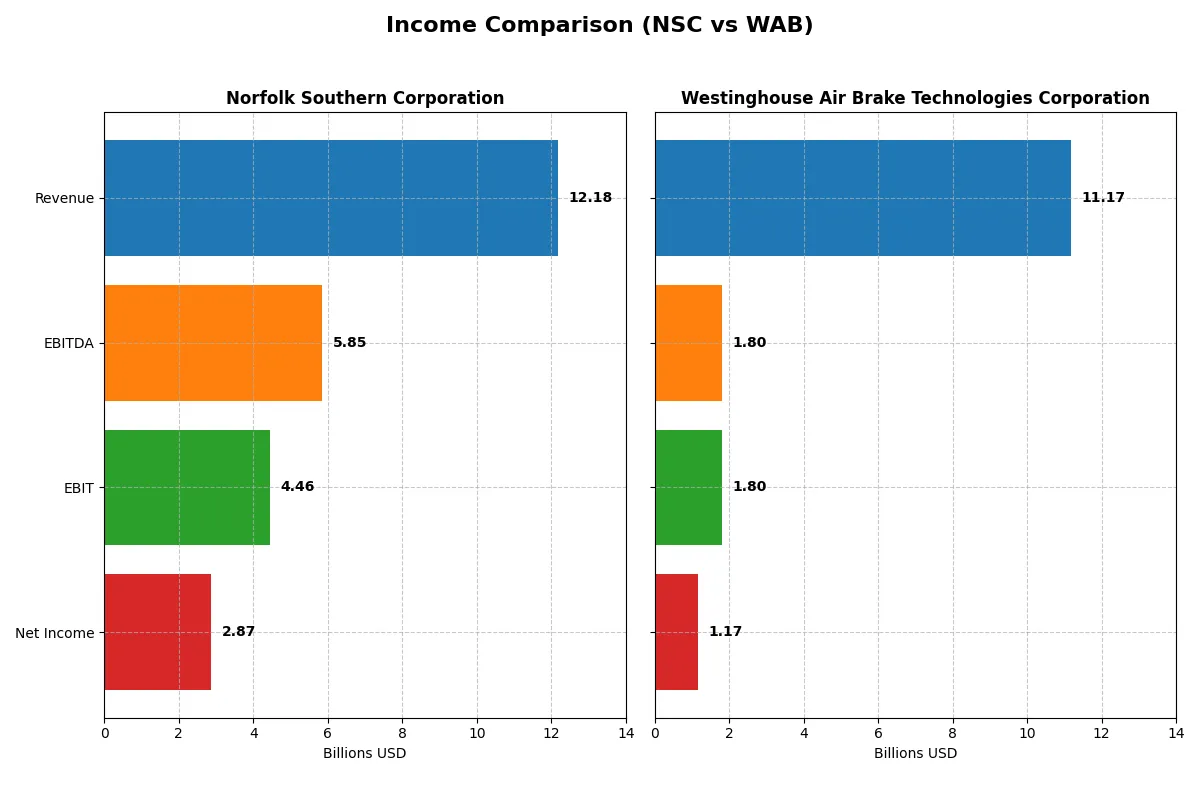

Income Statement Comparison

This table dissects the core profitability and scalability of Norfolk Southern Corporation and Westinghouse Air Brake Technologies Corporation to reveal who dominates the bottom line:

| Metric | Norfolk Southern (NSC) | Westinghouse Air Brake (WAB) |

|---|---|---|

| Revenue | 12.18B | 11.17B |

| Cost of Revenue | 7.01B | 7.36B |

| Operating Expenses | 1.16B | 1.49B |

| Gross Profit | 5.17B | 3.81B |

| EBITDA | 5.85B | 1.81B |

| EBIT | 4.46B | 1.81B |

| Interest Expense | 792M | 225M |

| Net Income | 2.87B | 1.17B |

| EPS | 12.75 | 6.86 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This comparison reveals which company runs a more efficient and profitable business engine through their income statement performance.

Norfolk Southern Corporation Analysis

Norfolk Southern’s revenue remained nearly flat at $12.18B in 2025, while net income grew to $2.87B, reflecting strong margin expansion. The gross margin surged to 42.4%, and net margin reached 23.6%, signaling robust profitability. I see improving earnings momentum with a 10.2% EPS growth, despite mild revenue stagnation.

Westinghouse Air Brake Technologies Corporation Analysis

Westinghouse posted a 7.5% revenue increase to $11.17B in 2025 and a 13% EPS rise, driving net income to $1.17B. Gross margin steadied at 34.1%, and net margin improved to 10.5%. I observe consistent top-line growth and margin gains, highlighting operational leverage and efficient cost control.

Margin Strength vs. Growth Trajectory

Norfolk Southern dominates with superior margins and higher absolute profits, showcasing operational efficiency. Westinghouse outpaces Norfolk Southern in revenue and net income growth rates, illustrating strong expansion and margin improvement. Investors prioritizing steady high profit margins may prefer Norfolk Southern, while growth-focused investors may find Westinghouse’s momentum more compelling.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies analyzed:

| Ratios | Norfolk Southern (NSC) | Westinghouse Air Brake (WAB) |

|---|---|---|

| ROE | 18.5% | 10.5% |

| ROIC | 7.5% | 7.4% |

| P/E | 22.6 | 31.1 |

| P/B | 4.17 | 3.27 |

| Current Ratio | 0.85 | 1.11 |

| Quick Ratio | 0.85 | 0.57 |

| D/E | 1.10 | 0.50 |

| Debt-to-Assets | 37.8% | 25.1% |

| Interest Coverage | 5.06 | 8.02 |

| Asset Turnover | 0.27 | 0.51 |

| Fixed Asset Turnover | 0 | 6.91 |

| Payout Ratio | 42.3% | 14.6% |

| Dividend Yield | 1.87% | 0.47% |

| Fiscal Year | 2025 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as a company’s DNA, revealing hidden risks and operational strengths that shape investor decisions profoundly.

Norfolk Southern Corporation

Norfolk Southern posts a robust 18.48% ROE and a strong 23.59% net margin, signaling effective profitability. Its P/E ratio of 22.59 appears fairly valued, but a high P/B of 4.17 and a low current ratio of 0.85 flag caution. The firm returns value via a 1.87% dividend, balancing shareholder payouts with reinvestment needs.

Westinghouse Air Brake Technologies Corporation

Westinghouse Air Brake shows a moderate 10.5% ROE and 10.48% net margin, reflecting steady but less efficient profitability. Its P/E ratio of 31.11 suggests a stretched valuation relative to profits. The company maintains a conservative debt profile and invests heavily in fixed assets, though its low 0.47% dividend yield indicates limited direct shareholder returns.

Balanced Profitability Meets Valuation Discipline

Norfolk Southern offers stronger profitability with reasonable valuation, while Westinghouse Air Brake trades at a premium with moderate returns and better debt metrics. Investors seeking operational efficiency may prefer Norfolk Southern, whereas those prioritizing financial stability might lean toward Westinghouse Air Brake’s conservative leverage.

Which one offers the Superior Shareholder Reward?

I compare Norfolk Southern Corporation (NSC) and Westinghouse Air Brake Technologies Corporation (WAB) on dividends, payout ratios, and buybacks for 2026. NSC yields 1.87%-2.3% dividends with a payout around 42%-46%, well-covered by free cash flow (FCF). NSC also maintains steady buybacks, enhancing total return. WAB offers a low 0.47%-0.6% yield and a conservative 13%-17% payout ratio, prioritizing reinvestment with robust free cash flow and modest buybacks. NSC’s distribution is generous yet sustainable, balancing dividends and buybacks. WAB’s model favors growth but provides limited immediate income. For investors seeking superior total return in 2026, I favor NSC’s balanced and reliable shareholder reward approach.

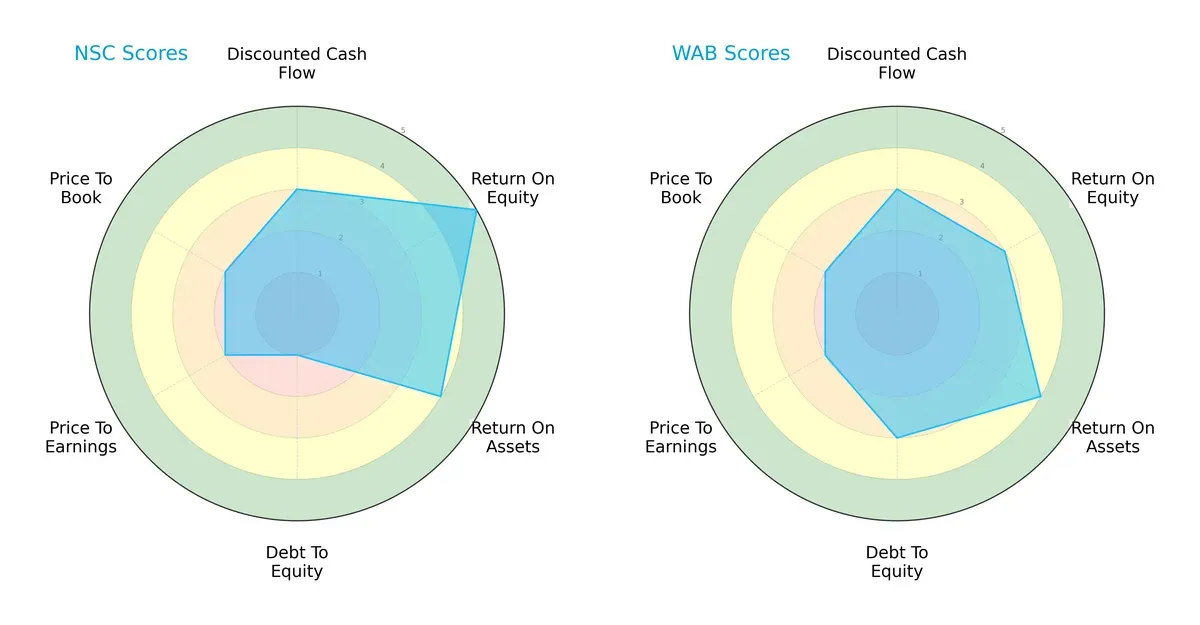

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Norfolk Southern Corporation and Westinghouse Air Brake Technologies Corporation:

Norfolk Southern (NSC) excels in return on equity (ROE 5 vs. 3) and return on assets (ROA 4 vs. 4), reflecting stronger profitability and asset efficiency. However, NSC’s debt-to-equity score (1) signals higher financial risk compared to WAB’s moderate score (3). Both firms share similar discounted cash flow (3) and valuation scores (PE/PB at 2 each). NSC relies on profit generation strength but carries risk from leverage; WAB presents a more balanced financial risk profile.

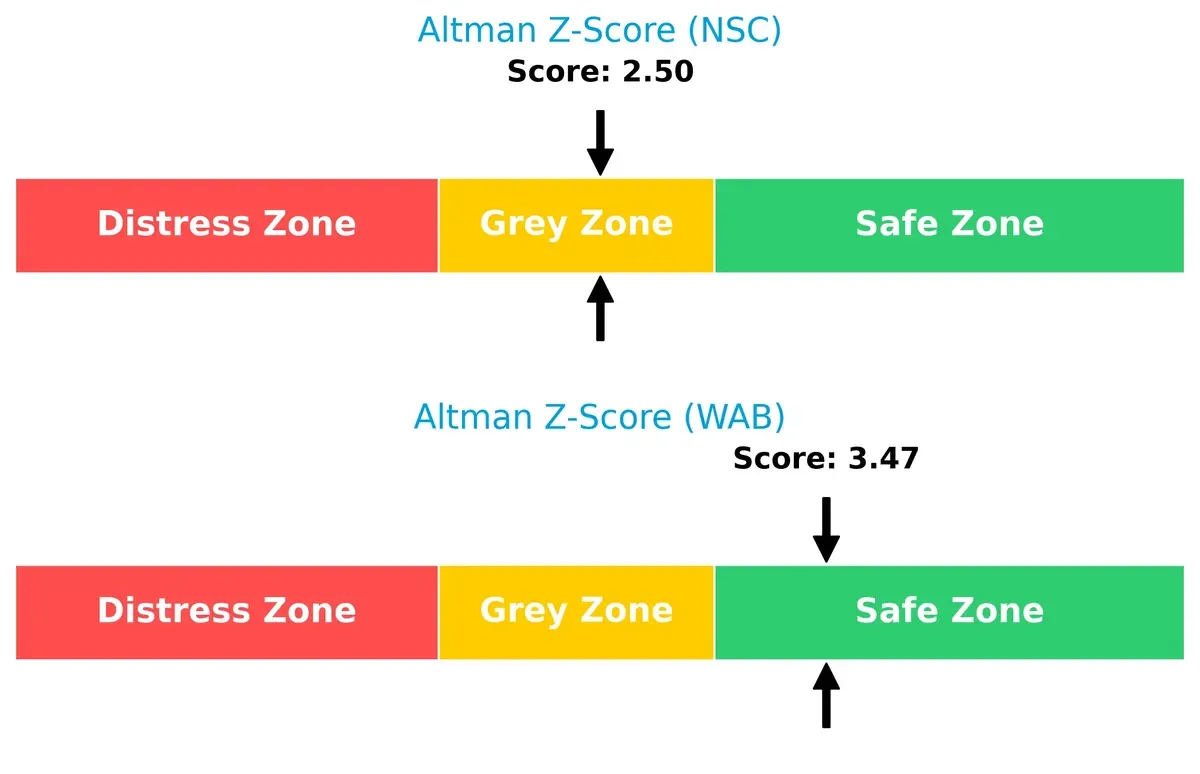

Bankruptcy Risk: Solvency Showdown

Norfolk Southern’s Altman Z-Score of 2.50 places it in the grey zone, indicating moderate bankruptcy risk. Westinghouse Air Brake’s safer 3.47 score suggests stronger solvency and resilience in this cycle:

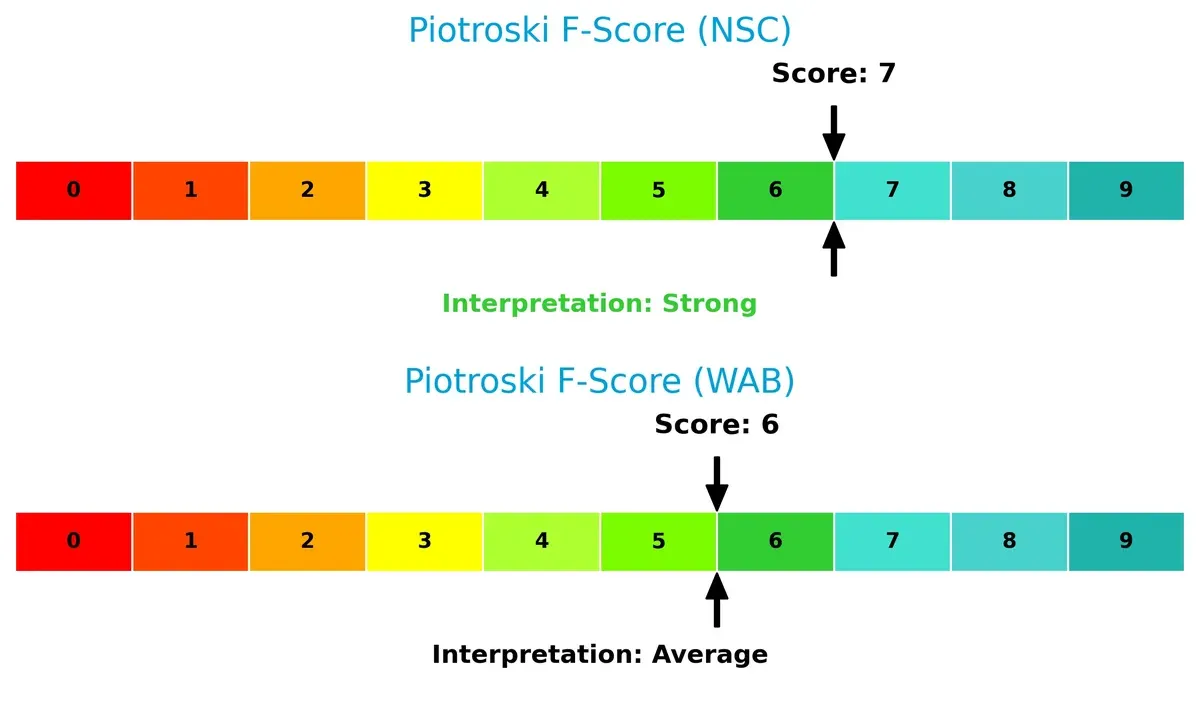

Financial Health: Quality of Operations

Norfolk Southern’s Piotroski F-Score of 7 demonstrates strong financial health and operational quality. Westinghouse Air Brake’s 6 score is average, hinting at some internal weaknesses relative to NSC:

How are the two companies positioned?

This section dissects the operational DNA of NSC and WAB by comparing their revenue distribution across segments and internal dynamics. The final goal is to confront their economic moats to reveal which business model holds the most resilient, sustainable competitive advantage today.

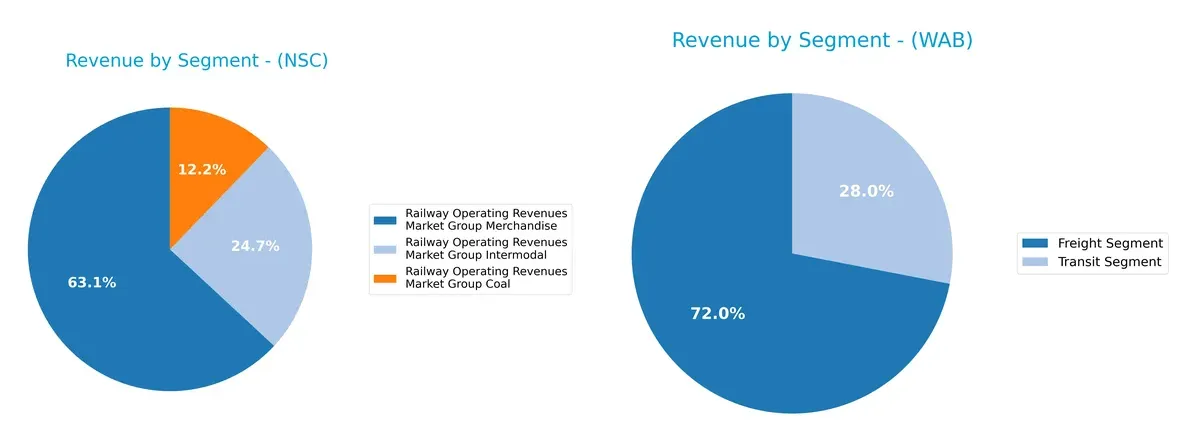

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Norfolk Southern Corporation and Westinghouse Air Brake Technologies diversify income streams and where their primary sector bets lie:

Norfolk Southern leans on three key segments, with Merchandise at $7.68B anchoring its revenue, while Intermodal and Coal contribute $3.01B and $1.49B respectively. Westinghouse Air Brake pivots mainly on two segments, Freight dominates at $8.04B, dwarfing Transit’s $3.13B. Norfolk Southern’s mix suggests balanced exposure across freight types, reducing concentration risk. In contrast, Westinghouse’s reliance on Freight highlights infrastructure dominance but raises dependency concerns.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Norfolk Southern Corporation and Westinghouse Air Brake Technologies Corporation:

Norfolk Southern Corporation Strengths

- Strong net margin at 23.59%

- High ROE of 18.48%

- Favorable interest coverage at 5.63

- Diversified railway revenues across merchandise, coal, intermodal

Westinghouse Air Brake Technologies Corporation Strengths

- Favorable net margin at 10.48%

- Strong interest coverage at 8.02

- Low debt-to-equity ratio at 0.5

- Global geographic diversification with presence in multiple continents

Norfolk Southern Corporation Weaknesses

- Current ratio low at 0.85 signals liquidity risk

- Unfavorable asset and fixed asset turnover ratios

- High debt-to-equity at 1.1

- Price-to-book ratio unfavorable at 4.17

Westinghouse Air Brake Technologies Corporation Weaknesses

- Unfavorable PE ratio at 31.11

- Quick ratio weak at 0.57

- Dividend yield low at 0.47%

- Price-to-book also unfavorable at 3.27

Both companies show solid profitability but differ in financial health and capital structure. Norfolk Southern faces liquidity and asset efficiency challenges, while Westinghouse benefits from lower leverage and global reach but carries higher valuation concerns. These factors shape each firm’s strategic financial positioning.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only thing protecting long-term profits from the erosion of competition. Let’s dissect the moats of Norfolk Southern and Westinghouse Air Brake Technologies:

Norfolk Southern Corporation: Asset-Intensive Network Moat

Norfolk Southern’s moat stems from its extensive rail infrastructure and logistics network. Historically, this manifests in strong gross margins (42.4%) and stable net margins (23.6%). However, declining ROIC versus WACC and a shrinking profitability trend in 2021-2025 threaten this capital-heavy moat in 2026.

Westinghouse Air Brake Technologies Corporation: Innovation-Driven Technology Moat

WAB’s competitive advantage lies in proprietary rail technology and services, supported by growing ROIC and accelerating profitability. Unlike Norfolk, WAB leverages innovation to expand margins (net margin 10.5%) and revenue globally, positioning itself for further growth and market disruption in 2026.

Infrastructure Depth vs. Innovation Agility

Norfolk Southern’s vast physical network offers scale but suffers from value erosion and declining ROIC. WAB shows a narrower moat but improves profitability and returns steadily. I see WAB better equipped to defend and grow its market share in the evolving rail sector.

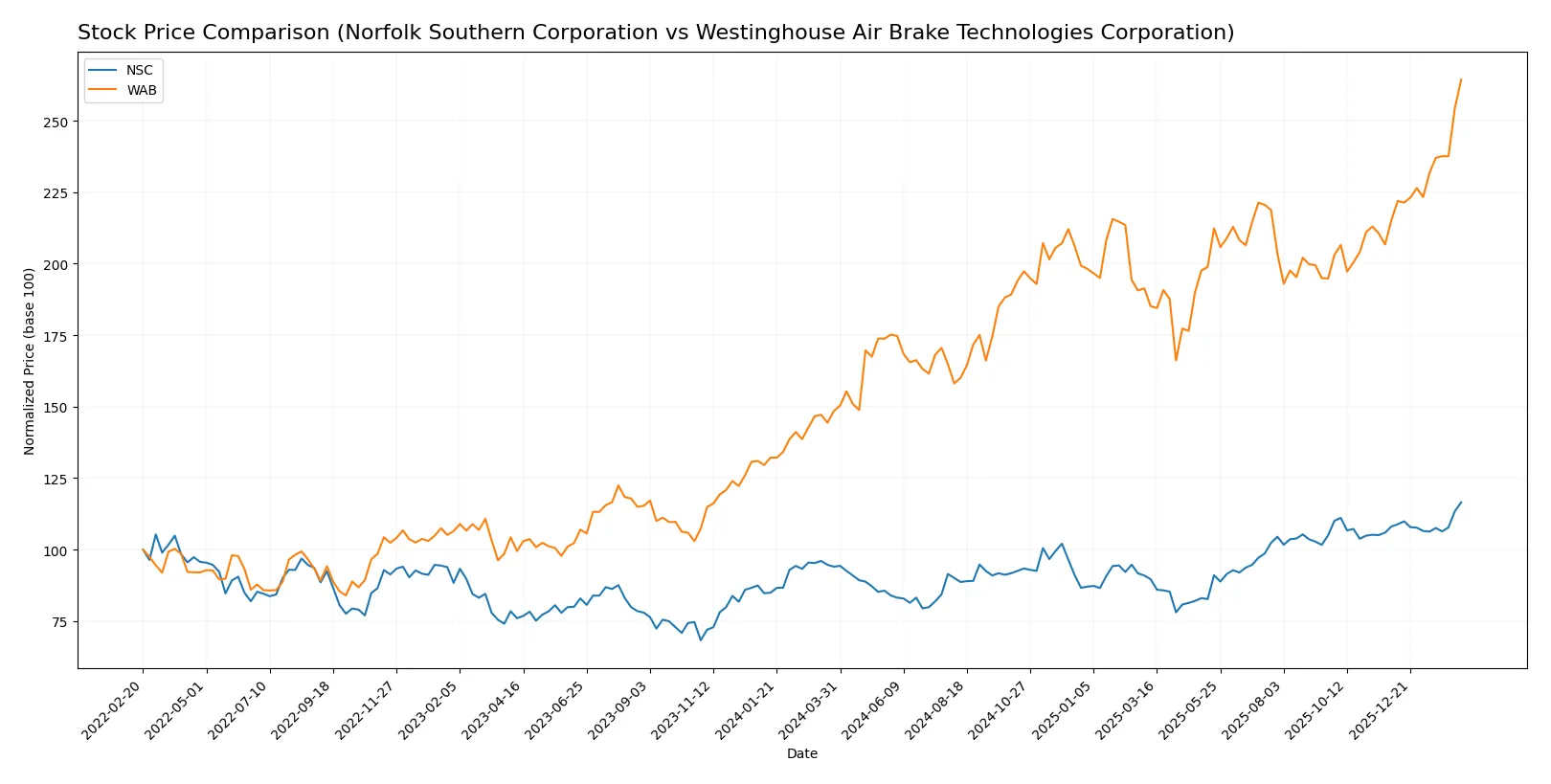

Which stock offers better returns?

The past year reveals distinct bullish trends for Norfolk Southern Corporation and Westinghouse Air Brake Technologies Corporation, with notable price gains and dynamic trading volumes shaping their market trajectories.

Trend Comparison

Norfolk Southern Corporation’s stock rose 23.93% over the past 12 months, showing acceleration and a high volatility level with a standard deviation of 24.82. Its price fluctuated between 210.93 and 314.94.

Westinghouse Air Brake Technologies Corporation’s stock surged 78.09% over the same period, accelerating with a 22.53 standard deviation. The price ranged from 143.78 to 256.06, reflecting strong upward momentum.

Westinghouse Air Brake Technologies outperformed Norfolk Southern with a significantly higher 78.09% gain versus 23.93%, delivering superior market returns over the last year.

Target Prices

Analysts show a moderately bullish consensus for Norfolk Southern Corporation and Westinghouse Air Brake Technologies Corporation.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Norfolk Southern Corporation | 288 | 342 | 312.43 |

| Westinghouse Air Brake Technologies Corporation | 221 | 308 | 267.6 |

Norfolk Southern’s target consensus of 312.43 is slightly below its current price of 314.94, indicating near fair value. Westinghouse’s consensus target of 267.6 exceeds its current price of 256.06, signaling room for upside.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Norfolk Southern Corporation Grades

The following table summarizes recent institutional grades for Norfolk Southern Corporation:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Baird | Maintain | Neutral | 2026-02-02 |

| Citigroup | Maintain | Neutral | 2026-01-30 |

| JP Morgan | Maintain | Neutral | 2026-01-30 |

| Barclays | Maintain | Overweight | 2026-01-30 |

| RBC Capital | Maintain | Sector Perform | 2026-01-30 |

| JP Morgan | Maintain | Neutral | 2026-01-12 |

| Citigroup | Maintain | Neutral | 2026-01-08 |

| Barclays | Maintain | Overweight | 2025-12-16 |

| Deutsche Bank | Downgrade | Hold | 2025-12-11 |

| TD Cowen | Maintain | Buy | 2025-10-24 |

Westinghouse Air Brake Technologies Corporation Grades

The following table summarizes recent institutional grades for Westinghouse Air Brake Technologies Corporation:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Wells Fargo | Maintain | Equal Weight | 2026-02-13 |

| Stephens & Co. | Maintain | Overweight | 2026-02-12 |

| Keybanc | Maintain | Overweight | 2026-02-12 |

| Citigroup | Maintain | Buy | 2026-02-12 |

| Susquehanna | Maintain | Positive | 2026-01-26 |

| JP Morgan | Maintain | Neutral | 2026-01-14 |

| Morgan Stanley | Maintain | Overweight | 2026-01-12 |

| Citigroup | Maintain | Buy | 2026-01-09 |

| Wolfe Research | Upgrade | Outperform | 2026-01-08 |

| Wells Fargo | Maintain | Equal Weight | 2025-12-17 |

Which company has the best grades?

Westinghouse Air Brake Technologies has received consistently stronger grades, including Buy, Overweight, and an upgrade to Outperform. Norfolk Southern shows more Neutral and Hold ratings with fewer Buy grades. This suggests WAB may enjoy more institutional confidence, potentially attracting more investor interest.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing Norfolk Southern Corporation and Westinghouse Air Brake Technologies Corporation in the 2026 market environment:

1. Market & Competition

Norfolk Southern Corporation

- Faces intense competition in U.S. rail transport with pressure on pricing and volume.

Westinghouse Air Brake Technologies Corporation

- Competes globally in rail and transit tech, exposed to innovation cycles and OEM customer dependence.

2. Capital Structure & Debt

Norfolk Southern Corporation

- High debt-to-equity ratio (1.1) signals elevated leverage and financial risk.

Westinghouse Air Brake Technologies Corporation

- More conservative debt profile (0.5 D/E) supports stronger balance sheet stability.

3. Stock Volatility

Norfolk Southern Corporation

- Beta at 1.32 indicates higher volatility than the market, increasing risk in downturns.

Westinghouse Air Brake Technologies Corporation

- Beta near 1.02 shows market-aligned volatility, suggesting more stable stock behavior.

4. Regulatory & Legal

Norfolk Southern Corporation

- Subject to stringent U.S. rail safety and environmental regulations, with potential fines and compliance costs.

Westinghouse Air Brake Technologies Corporation

- Faces regulatory scrutiny in transit safety and emissions standards globally, adding compliance complexity.

5. Supply Chain & Operations

Norfolk Southern Corporation

- Relies heavily on U.S. rail infrastructure; disruptions impact service delivery and revenues.

Westinghouse Air Brake Technologies Corporation

- Dependent on global suppliers and manufacturing; supply chain disruptions can delay projects and increase costs.

6. ESG & Climate Transition

Norfolk Southern Corporation

- Exposure to fossil fuel transport and emissions regulations challenges sustainability goals.

Westinghouse Air Brake Technologies Corporation

- Faces pressure to innovate low-emission technologies amid shifting ESG investor demands.

7. Geopolitical Exposure

Norfolk Southern Corporation

- Primarily U.S.-focused, with limited direct geopolitical exposure.

Westinghouse Air Brake Technologies Corporation

- Global operations increase exposure to trade tensions and political risks in emerging markets.

Which company shows a better risk-adjusted profile?

Norfolk Southern’s highest risk lies in its elevated debt and liquidity constraints, while Westinghouse’s primary concern is market competition and valuation multiples. Westinghouse Air Brake exhibits a stronger balance sheet and safer Altman Z-score, indicating better risk-adjusted stability. Norfolk Southern’s high leverage and below-par current ratio raise red flags, despite robust profitability metrics. These factors justify caution toward NSC’s financial flexibility in volatile markets.

Final Verdict: Which stock to choose?

Norfolk Southern Corporation’s superpower lies in its robust profitability and strong return on equity, making it a cash generator in the rail transport sector. However, its weak liquidity and high leverage pose a point of vigilance. It suits investors with an aggressive growth appetite who can tolerate balance sheet risks.

Westinghouse Air Brake Technologies commands a strategic moat with its specialized technology and improving profitability trajectory. Its balance sheet strength and safer leverage profile offer relative stability compared to Norfolk Southern. WAB fits well within GARP portfolios seeking growth balanced with financial prudence.

If you prioritize consistent profitability and high equity returns, Norfolk Southern is the compelling choice for aggressive growth despite liquidity risks. However, if you seek better balance sheet stability and steady earnings expansion, Westinghouse Air Brake offers superior risk management and growth potential. Both present distinct risk-reward profiles aligned with different investor strategies.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Norfolk Southern Corporation and Westinghouse Air Brake Technologies Corporation to enhance your investment decisions: