MercadoLibre, Inc. (MELI) and Williams-Sonoma, Inc. (WSM) are two prominent players in the specialty retail sector, each with distinct market focuses and innovative approaches. MercadoLibre dominates Latin America’s e-commerce and fintech landscape, while Williams-Sonoma excels in omni-channel home goods retail with a strong brand portfolio. This comparison highlights their strategies and growth potential to help you identify the most compelling investment opportunity. Let’s explore which company stands out for your portfolio.

Table of contents

Companies Overview

I will begin the comparison between MercadoLibre and Williams-Sonoma by providing an overview of these two companies and their main differences.

MercadoLibre Overview

MercadoLibre, Inc. operates online commerce platforms in Latin America, focusing on facilitating e-commerce through its marketplace and financial technology services. The company offers solutions such as Mercado Pago for online payments, Mercado Credito for loans, and Mercado Envios for logistics. Established in 1999 and headquartered in Montevideo, it has positioned itself as a leading player in the Latin American digital commerce space with a market cap of 110B USD.

Williams-Sonoma Overview

Williams-Sonoma, Inc. is an omni-channel specialty retailer based in San Francisco, offering a wide range of home products including cookware, furniture, and home decor under several brands like Pottery Barn and West Elm. Founded in 1956, the company operates over 500 stores primarily in the US and internationally, along with e-commerce platforms. With a market cap of 24B USD, it targets consumers seeking premium home and lifestyle products.

Key similarities and differences

Both companies belong to the specialty retail industry and serve consumer markets, but their business models differ significantly. MercadoLibre focuses on e-commerce and fintech services in Latin America, leveraging technology to facilitate online transactions and logistics. Williams-Sonoma operates a multi-brand retail model with physical stores and e-commerce platforms, primarily in the home goods sector across multiple countries. Their geographic focus and product offerings highlight distinct approaches within consumer cyclical retail.

Income Statement Comparison

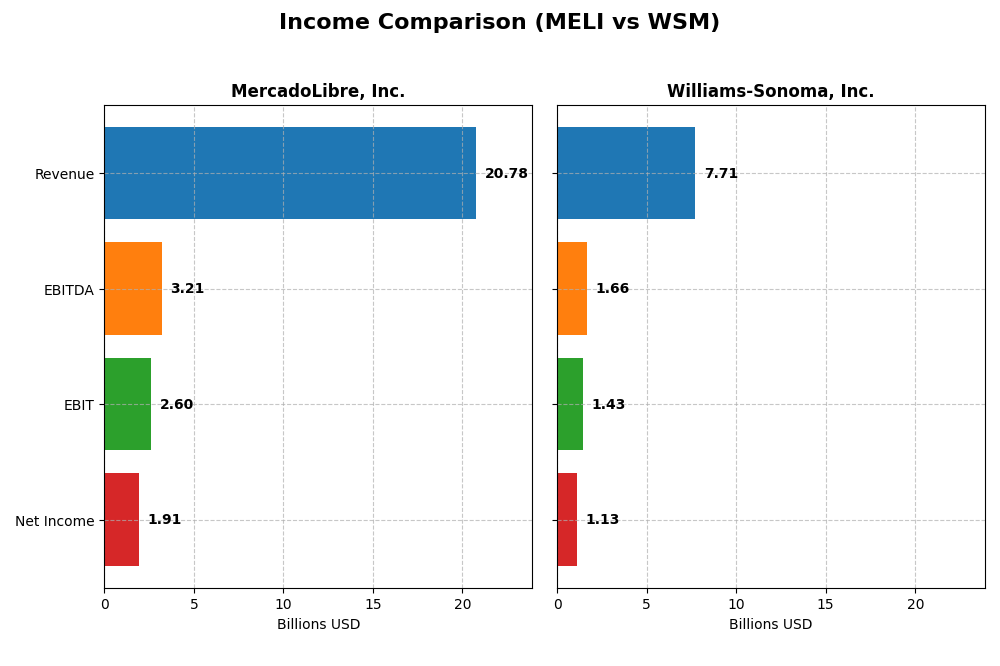

This table compares key income statement metrics for MercadoLibre, Inc. and Williams-Sonoma, Inc. for the most recent fiscal year, highlighting their financial performance.

| Metric | MercadoLibre, Inc. (MELI) | Williams-Sonoma, Inc. (WSM) |

|---|---|---|

| Market Cap | 110.4B | 24.4B |

| Revenue | 20.8B | 7.7B |

| EBITDA | 3.2B | 1.7B |

| EBIT | 2.6B | 1.4B |

| Net Income | 1.9B | 1.1B |

| EPS | 37.69 | 8.91 |

| Fiscal Year | 2024 | 2024 |

Income Statement Interpretations

MercadoLibre, Inc.

MercadoLibre’s revenue and net income have shown substantial growth from 2020 to 2024, with revenue soaring from $3.97B to $20.78B and net income rising from a slight loss to $1.91B. Margins have improved consistently, with a gross margin of 46.09% and net margin of 9.2% in 2024. The latest year saw a strong acceleration in growth, particularly in earnings per share, which nearly doubled.

Williams-Sonoma, Inc.

Williams-Sonoma’s revenue grew moderately over the period, reaching $7.71B in 2024 from $6.78B in 2020, though it slightly declined by 0.5% in the latest year. Net income increased to $1.13B with a net margin of 14.59%, reflecting stable profitability. The latest fiscal year showed an uptick in net margin and earnings per share despite a minor revenue contraction, with EBIT margin improving to 18.55%.

Which one has the stronger fundamentals?

MercadoLibre exhibits stronger fundamentals in terms of rapid revenue and net income growth, supported by expanding margins and robust earnings momentum. Williams-Sonoma, while showing favorable profitability margins and steady net income growth, faced a slight recent revenue decline. Overall, MercadoLibre’s income statement reflects a more dynamic growth profile, whereas Williams-Sonoma presents consistent but slower advancement.

Financial Ratios Comparison

The table below compares key financial ratios of MercadoLibre, Inc. (MELI) and Williams-Sonoma, Inc. (WSM) based on their most recent full fiscal year data for 2024.

| Ratios | MercadoLibre, Inc. (MELI) | Williams-Sonoma, Inc. (WSM) |

|---|---|---|

| ROE | 43.9% | 52.5% |

| ROIC | 17.7% | 29.9% |

| P/E | 45.1 | 23.7 |

| P/B | 19.8 | 12.5 |

| Current Ratio | 1.21 | 1.44 |

| Quick Ratio | 1.20 | 0.74 |

| D/E (Debt-to-Equity) | 1.57 | 0.63 |

| Debt-to-Assets | 27.2% | 25.4% |

| Interest Coverage | 17.2 | 0 (not available) |

| Asset Turnover | 0.82 | 1.45 |

| Fixed Asset Turnover | 8.38 | 3.49 |

| Payout Ratio | 0% | 24.9% |

| Dividend Yield | 0% | 1.05% |

Interpretation of the Ratios

MercadoLibre, Inc.

MercadoLibre shows a mixed financial profile with strong returns on equity (43.92%) and invested capital (17.73%), but faces challenges with high price multiples and debt-to-equity ratio. Liquidity ratios are mostly stable, though leverage remains a concern. The company does not pay dividends, likely reflecting a reinvestment strategy to support growth and innovation in its Latin American commerce and fintech platforms.

Williams-Sonoma, Inc.

Williams-Sonoma exhibits robust profitability with a favorable net margin of 14.59%, return on equity exceeding 52%, and solid returns on invested capital near 30%. While its debt level is moderate and interest coverage excellent, the quick ratio is weak. The company pays dividends with a 1.05% yield, indicating some shareholder returns alongside steady operational performance and controlled leverage.

Which one has the best ratios?

Both companies present slightly favorable overall ratios, but Williams-Sonoma displays stronger profitability and capital efficiency metrics, alongside dividend payments. MercadoLibre excels in certain returns but contends with higher valuation multiples and debt concerns. The performance and risk profiles differ, reflecting their distinct business models and market dynamics.

Strategic Positioning

This section compares the strategic positioning of MercadoLibre and Williams-Sonoma, including market position, key segments, and exposure to technological disruption:

MercadoLibre, Inc.

- Leading online commerce platform in Latin America with strong competitive pressure in e-commerce and fintech sectors.

- Key segments include marketplace commerce, fintech services, logistics, advertising, and digital storefront solutions driving revenue growth.

- High exposure to technological disruption through fintech innovation, digital payments, and logistics platform integration.

Williams-Sonoma, Inc.

- Omni-channel specialty retailer focused on home products with competitive pressure in retail and e-commerce markets.

- Diverse home product segments including Pottery Barn, West Elm, and Williams Sonoma brands, driven by retail and e-commerce sales.

- Moderate exposure via augmented reality platform and e-commerce integration supporting home furnishings and décor sales.

MercadoLibre vs Williams-Sonoma Positioning

MercadoLibre pursues a diversified digital commerce and fintech strategy, leveraging multiple revenue streams, while Williams-Sonoma focuses on a concentrated specialty retail approach centered on lifestyle brands. MercadoLibre’s model emphasizes tech-driven growth; Williams-Sonoma relies on brand portfolio and retail channels.

Which has the best competitive advantage?

Both companies demonstrate very favorable moats with growing ROICs above WACC, indicating durable competitive advantages. Williams-Sonoma shows a higher ROIC premium, suggesting a slightly stronger profitability edge, while MercadoLibre benefits from rapid growth in a dynamic market.

Stock Comparison

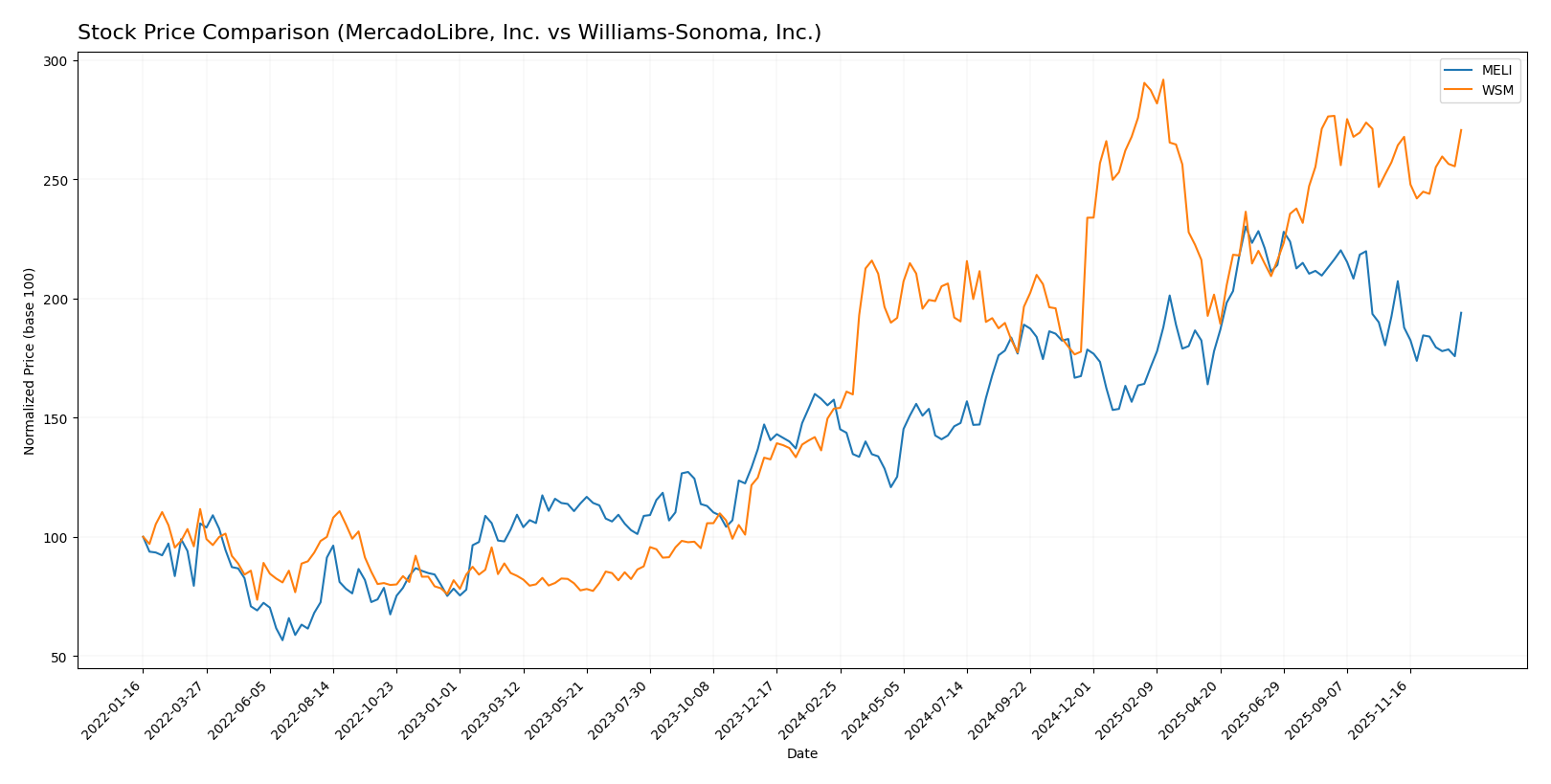

The stock price movements over the past year reveal significant bullish trends for both MercadoLibre, Inc. and Williams-Sonoma, Inc., with notable deceleration in momentum and contrasting recent trading dynamics.

Trend Analysis

MercadoLibre, Inc. (MELI) exhibited a 23.16% price increase over the past 12 months, indicating a bullish trend with deceleration. The stock reached a high of 2,584.92 and a low of 1,356.43, with recent slight neutral movement of 0.8%.

Williams-Sonoma, Inc. (WSM) showed a stronger bullish trend with a 76.06% price increase over the past year, also with deceleration. Its price ranged between 113.05 and 214.6, with a recent moderate 5.26% rise sustaining a slight bullish slope.

Comparing both stocks, Williams-Sonoma delivered the highest market performance over the last 12 months, outperforming MercadoLibre by more than 50 percentage points in price appreciation.

Target Prices

Analysts present a confident target consensus for both MercadoLibre, Inc. and Williams-Sonoma, Inc.

| Company | Target High | Target Low | Consensus |

|---|---|---|---|

| MercadoLibre, Inc. | 2900 | 2700 | 2830 |

| Williams-Sonoma, Inc. | 230 | 175 | 205.75 |

The target consensus for MercadoLibre at 2830 suggests significant upside from the current 2178.41 price, while Williams-Sonoma’s 205.75 consensus indicates a moderate potential increase versus the current 199.04 price.

Analyst Opinions Comparison

This section compares analysts’ ratings and grades for MercadoLibre, Inc. and Williams-Sonoma, Inc.:

Rating Comparison

MELI Rating

- Rating: B-, classified as Very Favorable overall.

- Discounted Cash Flow Score: 3, considered Moderate.

- Return on Equity Score: 5, rated Very Favorable.

- Return on Assets Score: 4, rated Favorable.

- Debt To Equity Score: 1, rated Very Unfavorable for financial risk.

- Overall Score: 3, reflecting a Moderate standing.

WSM Rating

- Rating: B+, classified as Very Favorable overall.

- Discounted Cash Flow Score: 3, considered Moderate.

- Return on Equity Score: 5, rated Very Favorable.

- Return on Assets Score: 5, rated Very Favorable.

- Debt To Equity Score: 2, rated Moderate for financial risk.

- Overall Score: 3, reflecting a Moderate standing.

Which one is the best rated?

Based strictly on provided data, WSM holds a higher rating (B+ vs. B-) with a better return on assets score and a more moderate debt-to-equity profile. Both have equal overall and discounted cash flow scores.

Scores Comparison

Here is a comparison of the Altman Z-Score and Piotroski Score for MercadoLibre, Inc. and Williams-Sonoma, Inc.:

MELI Scores

- Altman Z-Score: 3.46, indicating a safe zone with low bankruptcy risk.

- Piotroski Score: 4, reflecting average financial strength.

WSM Scores

- Altman Z-Score: 7.04, indicating a safe zone with very low bankruptcy risk.

- Piotroski Score: 7, reflecting strong financial strength.

Which company has the best scores?

Williams-Sonoma has higher Altman Z-Score and Piotroski Score values than MercadoLibre, indicating stronger financial health and lower bankruptcy risk based on these metrics.

Grades Comparison

Here is a detailed comparison of the recent grades assigned to MercadoLibre, Inc. and Williams-Sonoma, Inc.:

MercadoLibre, Inc. Grades

The following table summarizes recent grades from reputable grading companies for MercadoLibre, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Wedbush | Maintain | Outperform | 2025-12-19 |

| BTIG | Maintain | Buy | 2025-12-04 |

| UBS | Maintain | Buy | 2025-11-24 |

| BTIG | Maintain | Buy | 2025-11-14 |

| JP Morgan | Maintain | Neutral | 2025-11-03 |

| Morgan Stanley | Maintain | Overweight | 2025-11-03 |

| Barclays | Maintain | Overweight | 2025-10-30 |

| Benchmark | Maintain | Buy | 2025-10-30 |

| Cantor Fitzgerald | Maintain | Overweight | 2025-10-30 |

| Barclays | Maintain | Overweight | 2025-10-21 |

MercadoLibre’s grades predominantly indicate a positive outlook with multiple “Buy,” “Outperform,” and “Overweight” ratings maintained across the last quarter.

Williams-Sonoma, Inc. Grades

The following table summarizes recent grades from reputable grading companies for Williams-Sonoma, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Evercore ISI Group | Maintain | In Line | 2025-12-23 |

| RBC Capital | Maintain | Outperform | 2025-11-21 |

| Telsey Advisory Group | Maintain | Outperform | 2025-11-20 |

| UBS | Maintain | Neutral | 2025-11-20 |

| TD Cowen | Maintain | Buy | 2025-11-20 |

| Citigroup | Maintain | Neutral | 2025-11-20 |

| Telsey Advisory Group | Maintain | Outperform | 2025-11-19 |

| Telsey Advisory Group | Maintain | Outperform | 2025-11-14 |

| Wells Fargo | Maintain | Equal Weight | 2025-11-11 |

| Evercore ISI Group | Maintain | In Line | 2025-10-14 |

Williams-Sonoma’s ratings show a mix of “Outperform,” “Neutral,” and “In Line” grades, indicating a more moderate consensus among analysts.

Which company has the best grades?

MercadoLibre, Inc. holds a stronger consensus with mostly “Buy” and “Outperform” ratings, while Williams-Sonoma, Inc. has a broader range including “Hold” and “Neutral” grades. This suggests MercadoLibre may currently be viewed more favorably by analysts, potentially affecting investor confidence and portfolio decisions accordingly.

Strengths and Weaknesses

Below is a comparative table summarizing the key strengths and weaknesses of MercadoLibre, Inc. (MELI) and Williams-Sonoma, Inc. (WSM) based on their latest financial and operational data.

| Criterion | MercadoLibre, Inc. (MELI) | Williams-Sonoma, Inc. (WSM) |

|---|---|---|

| Diversification | Strong product and service mix: $2.14B product, $18.64B services, including commerce and fintech segments | Well-diversified retail segments: Pottery Barn, West Elm, Williams Sonoma, and others with solid revenue streams |

| Profitability | ROIC 17.73%, Net margin 9.2%, ROE 43.92% – favorable but with high valuation ratios (PE 45.11, PB 19.81) | ROIC 29.89%, Net margin 14.59%, ROE 52.52% – strong profitability and more moderate valuation (PE 23.71, PB 12.45) |

| Innovation | High innovation with strong fintech and e-commerce platform growth, reflected in rapid ROIC growth (+39297%) | Moderate innovation focused on retail brand extensions and e-commerce, ROIC growth +43% |

| Global presence | Leading e-commerce and fintech platform in Latin America with expanding footprint | Primarily US-focused premium home goods retail with growing e-commerce presence |

| Market Share | Dominant in Latin American online commerce and payment solutions | Strong niche market leader in premium home furnishings in the US |

Key Takeaways: MercadoLibre excels in innovation and rapid growth in Latin American e-commerce and fintech, though valuation metrics suggest caution. Williams-Sonoma shows higher profitability, stable growth, and strong brand diversification in premium retail. Both demonstrate durable moats and value creation, suitable for investors with different risk appetites and regional preferences.

Risk Analysis

Below is a comparison table of key risks for MercadoLibre, Inc. (MELI) and Williams-Sonoma, Inc. (WSM) based on the most recent data from 2024:

| Metric | MercadoLibre, Inc. (MELI) | Williams-Sonoma, Inc. (WSM) |

|---|---|---|

| Market Risk | High beta (1.42) indicates above-average volatility in Latin American markets. | Higher beta (1.58) reflects sensitivity to US consumer cyclical sector fluctuations. |

| Debt level | Elevated debt-to-equity ratio (1.57); moderate leverage risk but manageable interest coverage (16.97). | Moderate debt level (DE 0.63) with strong interest coverage (infinite), indicating low financial risk. |

| Regulatory Risk | Significant, due to operations across diverse Latin American countries with evolving e-commerce regulations. | Moderate, mostly US-focused with standard retail regulations. |

| Operational Risk | Complex logistics and fintech platform integration pose execution challenges. | Reliance on omni-channel retail and global store operations may face supply chain disruptions. |

| Environmental Risk | Moderate, with growing focus on sustainable logistics and e-commerce packaging. | Moderate, linked to product sourcing and retail operations sustainability initiatives. |

| Geopolitical Risk | High, exposed to Latin American political instability and currency fluctuations. | Lower, primarily US and developed market exposure with stable geopolitical environment. |

MercadoLibre’s most impactful risks are geopolitical instability and regulatory complexity in Latin America, which could affect growth and profitability. Williams-Sonoma faces operational risks from global supply chains and moderate market volatility but benefits from lower debt and a stable regulatory environment. Caution is advised with MELI due to its higher leverage and market sensitivity.

Which Stock to Choose?

MercadoLibre, Inc. (MELI) shows strong income growth with a 37.53% revenue increase in 2024 and favorable profitability metrics, including a 43.92% ROE and a 17.73% ROIC. Its debt level is moderate, with a net debt to EBITDA of 1.31, and the rating stands at B- with a very favorable outlook.

Williams-Sonoma, Inc. (WSM) reports stable income with a slight revenue decline of -0.5% in 2024 but maintains strong margins and profitability, featuring a 52.52% ROE and a 29.89% ROIC. Its debt is low (net debt to EBITDA 0.08), and it holds a B+ rating with a very favorable perspective.

Investors seeking growth might find MELI appealing due to its rapid income and earnings expansion alongside a solid competitive moat. Conversely, those prioritizing financial stability and higher profitability margins may see WSM as favorable, reflecting its consistent returns and lower leverage.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of MercadoLibre, Inc. and Williams-Sonoma, Inc. to enhance your investment decisions: