Home > Comparison > Technology > TSM vs LRCX

The strategic rivalry between Taiwan Semiconductor Manufacturing Company Limited and Lam Research Corporation shapes the semiconductor industry’s future. Taiwan Semiconductor dominates as a capital-intensive semiconductor manufacturer, providing advanced wafer fabrication globally. In contrast, Lam Research specializes in high-tech semiconductor processing equipment, enabling chip production efficiency. This analysis contrasts their operational models and growth trajectories to identify which offers superior risk-adjusted returns for a diversified portfolio in the evolving technology sector.

Table of contents

Companies Overview

Taiwan Semiconductor Manufacturing Company Limited and Lam Research Corporation play pivotal roles in the semiconductor industry.

Taiwan Semiconductor Manufacturing Company Limited: Global Semiconductor Foundry Leader

Taiwan Semiconductor Manufacturing Company Limited dominates as a leading semiconductor foundry. It generates revenue by manufacturing and selling integrated circuits and semiconductor devices worldwide. In 2026, the company prioritizes advanced wafer fabrication processes and strong customer engineering support to maintain its technological edge.

Lam Research Corporation: Specialized Semiconductor Equipment Provider

Lam Research Corporation specializes in semiconductor processing equipment. It earns revenue by designing and servicing tools essential for integrated circuit fabrication, including etching and deposition systems. The company focuses on enhancing product innovation and global market expansion in 2026 to support semiconductor manufacturing efficiency.

Strategic Collision: Similarities & Divergences

Both companies fuel the semiconductor ecosystem but differ sharply in focus—TSMC operates a manufacturing foundry while Lam provides the equipment enabling chip production. They compete indirectly, with TSMC emphasizing production capacity and Lam advancing fabrication technology. Their distinct roles create complementary yet divergent investment profiles reflecting manufacturing scale versus equipment innovation.

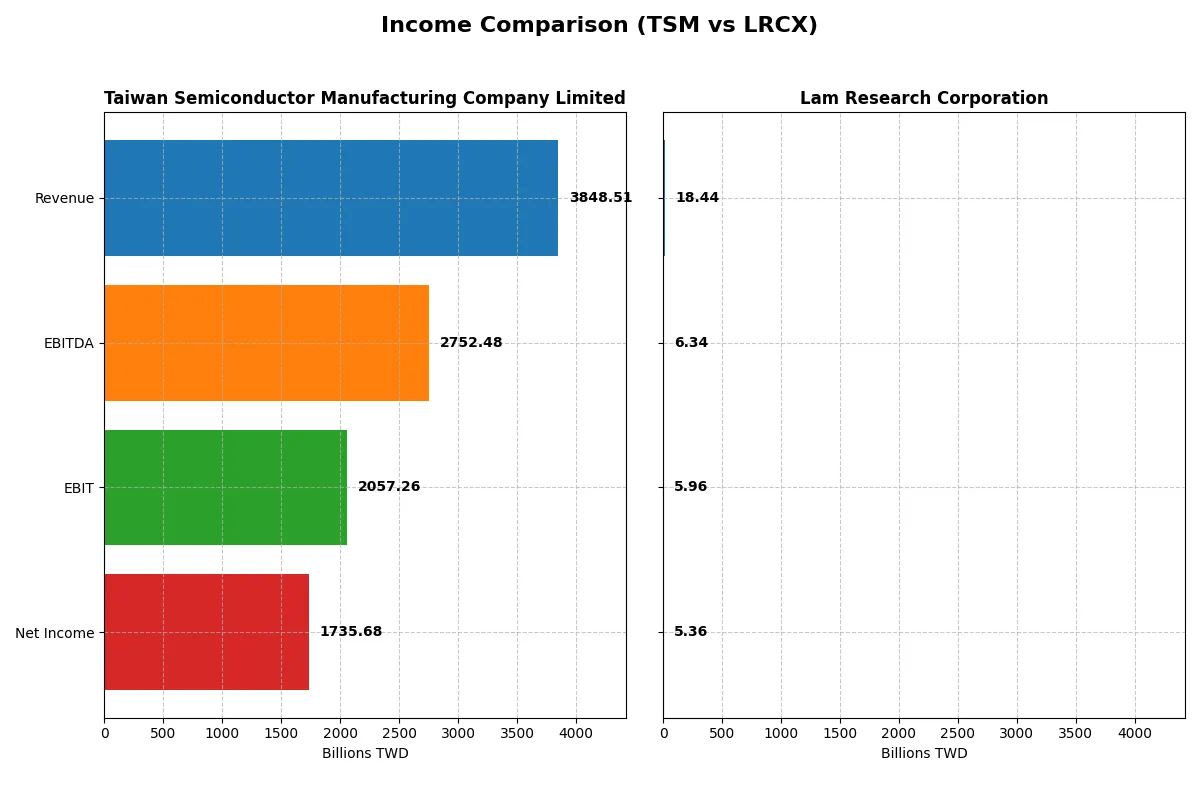

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Taiwan Semiconductor Manufacturing Company Limited (TSM) | Lam Research Corporation (LRCX) |

|---|---|---|

| Revenue | 3.85T TWD | 18.4B USD |

| Cost of Revenue | 1.54T TWD | 9.46B USD |

| Operating Expenses | 349.2B TWD | 3.08B USD |

| Gross Profit | 2.30T TWD | 8.98B USD |

| EBITDA | 2.75T TWD | 6.34B USD |

| EBIT | 2.06T TWD | 5.96B USD |

| Interest Expense | 0 | 178M USD |

| Net Income | 1.74T TWD | 5.36B USD |

| EPS | 334.6 TWD | 4.17 USD |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals the true efficiency and profitability of Taiwan Semiconductor Manufacturing Company and Lam Research Corporation’s business models.

Taiwan Semiconductor Manufacturing Company Limited Analysis

TSM’s revenue surged 33% in 2025 to 3.85T TWD, with net income rising 50% to 1.74T TWD, demonstrating robust growth momentum. Its gross margin stands at an impressive 59.9%, while the net margin reached a strong 45.1%, reflecting excellent cost control and operational efficiency in the latest fiscal year.

Lam Research Corporation Analysis

LRCX increased revenue by 24% to $18.4B in fiscal 2025, while net income jumped 40% to $5.36B, signaling solid growth. The company maintains healthy margins with a 48.7% gross margin and a 29.1% net margin, showing effective expense management and scalable profitability, though below TSM’s levels.

Margin Dominance vs. Revenue Growth

TSM outpaces LRCX in both scale and profitability, boasting a superior 45.1% net margin versus LRCX’s 29.1%, and a more dramatic rise in revenue and net income over recent years. Investors seeking high-margin leadership and rapid expansion may find TSM’s profile more compelling, while LRCX presents steady growth with respectable margins.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Taiwan Semiconductor Manufacturing Company Limited (TSM) | Lam Research Corporation (LRCX) |

|---|---|---|

| ROE | 32.12% | 54.33% |

| ROIC | 24.92% | 33.99% |

| P/E | 28.45 | 23.36 |

| P/B | 9.14 | 12.69 |

| Current Ratio | 2.62 | 2.21 |

| Quick Ratio | 2.42 | 1.55 |

| D/E (Debt-to-Equity) | 0.18 | 0.48 |

| Debt-to-Assets | 12.52% | 22.28% |

| Interest Coverage | 0 | 33.11 |

| Asset Turnover | 0.49 | 0.86 |

| Fixed Asset Turnover | 1.05 | 7.59 |

| Payout ratio | 27.17% | 21.45% |

| Dividend yield | 0.95% | 0.92% |

| Fiscal Year | 2025 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as a company’s DNA, exposing hidden risks and operational strengths crucial for savvy investment decisions.

Taiwan Semiconductor Manufacturing Company Limited

TSM demonstrates strong profitability with a ROE of 32.12% and a high net margin of 45.1%, signaling operational excellence. Its valuation appears stretched with a P/E of 28.45 and P/B of 9.14, above sector averages. Dividend yield is modest at 0.95%, reflecting cautious shareholder returns amid reinvestment in growth and R&D.

Lam Research Corporation

LRCX posts an impressive ROE of 54.33% and solid net margin at 29.06%, underscoring efficient capital use. The stock trades at a reasonable P/E of 23.36 but bears a high P/B of 12.69, indicating premium pricing. Dividend yield of 0.92% remains low; the company prioritizes growth through R&D with a capex-light model.

Valuation Stretch vs. Return on Equity Potency

Both companies deliver favorable profitability and operational metrics, but TSM’s valuation appears more stretched than LRCX’s. LRCX offers a stronger ROE and a more balanced ratio profile. Investors seeking robust returns with measured risk may prefer LRCX’s aggressive capital efficiency, while TSM suits those favoring established scale and reinvestment discipline.

Which one offers the Superior Shareholder Reward?

I see Taiwan Semiconductor Manufacturing Company Limited (TSM) and Lam Research Corporation (LRCX) both pay dividends and execute buybacks, but their approaches differ sharply. TSM yields about 0.95% with a payout ratio near 27%, showing solid free cash flow coverage. Its buyback scale is robust, signaling a balanced distribution and reinvestment strategy. LRCX offers a slightly lower yield around 0.92% with a more conservative payout ratio of 21%, prioritizing higher free cash flow retention and aggressive buybacks—nearly 88% of operating cash flow. Historically in tech capital equipment, buybacks combined with moderate dividends sustain shareholder value best when free cash flow is strong and consistent. Given TSM’s stronger margin profile and sustainable payout, I judge TSM’s distribution model more reliable. For 2026, TSM offers a superior total shareholder return profile, blending dividends and buybacks into enduring value creation.

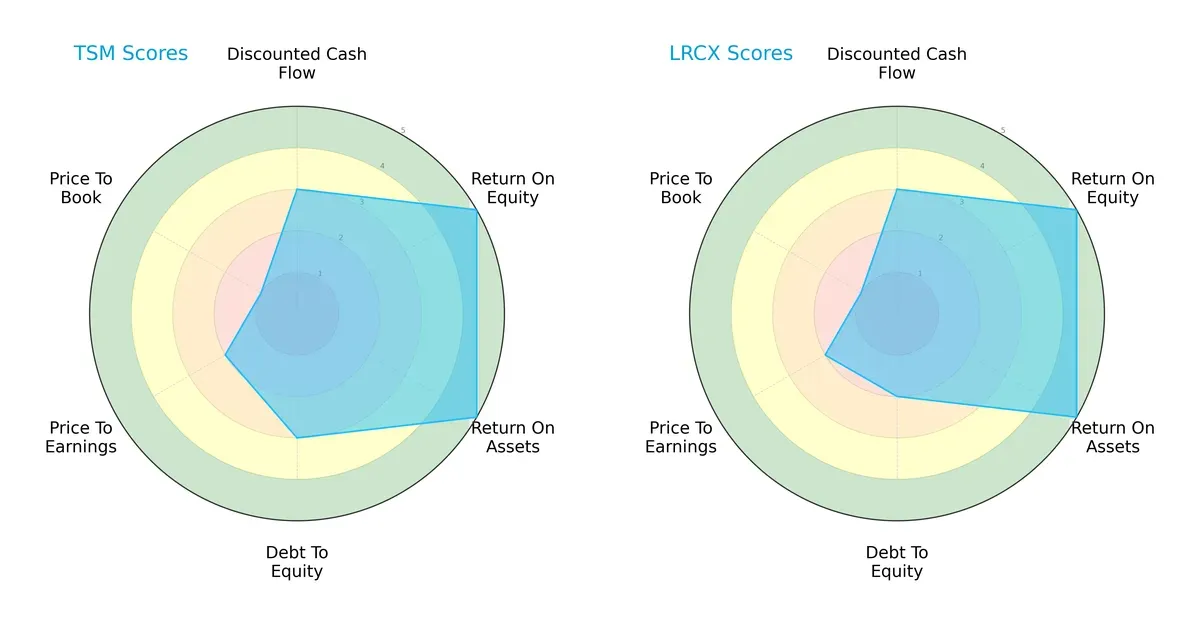

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Taiwan Semiconductor Manufacturing Company Limited and Lam Research Corporation:

Both firms show parity in overall, discounted cash flow, return on equity, and return on assets scores, indicating similar core earnings efficiency. Taiwan Semiconductor holds a moderate debt-to-equity score of 3 versus Lam Research’s 2, suggesting a slightly stronger balance sheet for Lam. Valuation metrics (PE and PB) are weak for both, with Taiwan Semiconductor scoring marginally lower on price-to-book, reflecting potential overvaluation risks. Lam Research’s profile appears more balanced due to its superior leverage metric, while Taiwan Semiconductor relies on operational efficiency as its key edge.

Bankruptcy Risk: Solvency Showdown

The Altman Z-Score gap between Taiwan Semiconductor (15.7) and Lam Research (21.2) confirms both firms sit comfortably in the safe zone for bankruptcy risk in this cycle:

Both companies exhibit robust financial stability, but Lam Research’s substantially higher Z-Score signals an even stronger cushion against financial distress, enhancing its appeal for risk-averse investors.

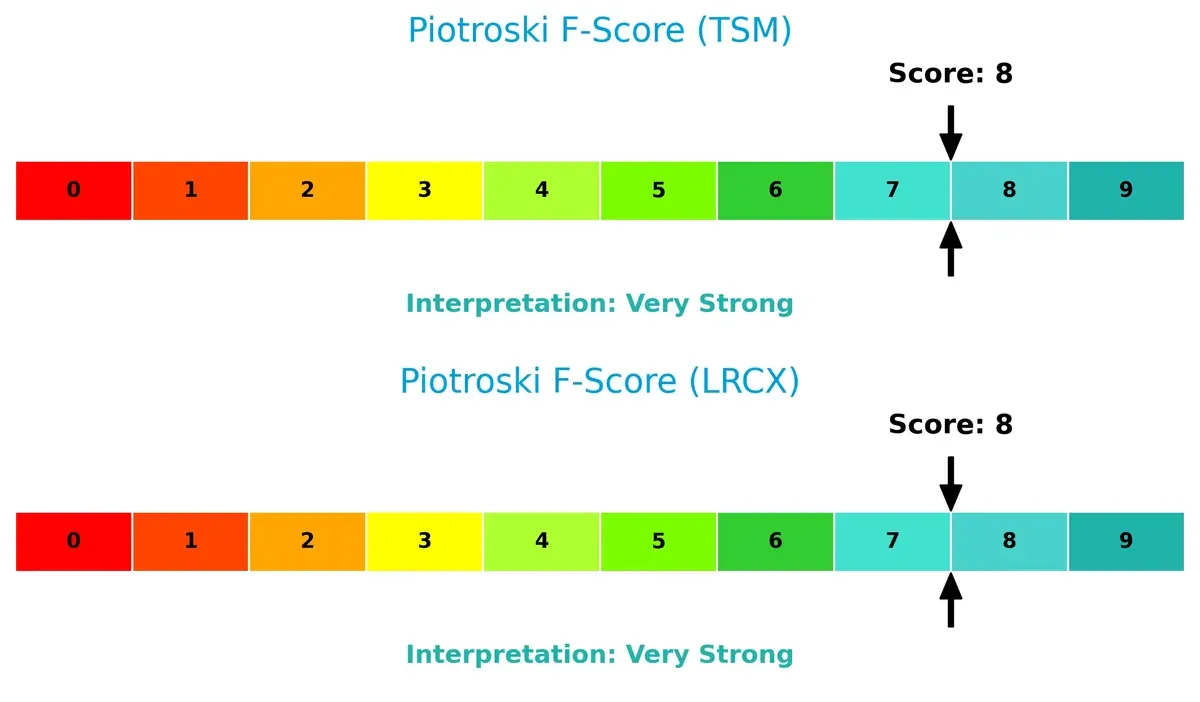

Financial Health: Quality of Operations

Taiwan Semiconductor and Lam Research both score an 8 on the Piotroski F-Score, indicating very strong financial health and operational quality:

This parity reflects solid profitability, liquidity, and efficiency metrics in both firms. Neither shows internal red flags, which supports confidence in their ongoing financial discipline and value creation.

How are the two companies positioned?

This section dissects TSM and LRCX’s operational DNA by comparing revenue distribution and internal strengths and weaknesses. The goal is to confront their economic moats to reveal which model delivers the more durable competitive advantage today.

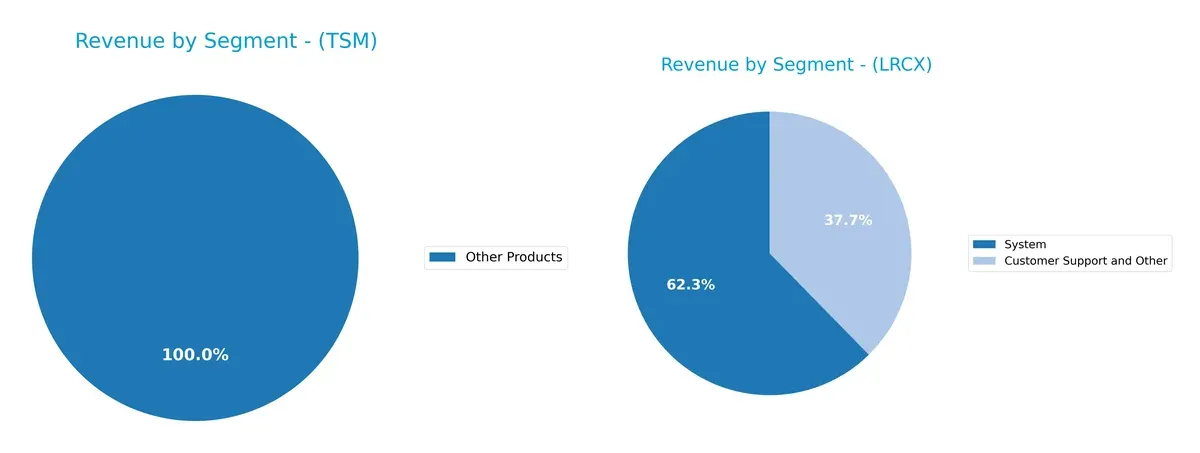

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Taiwan Semiconductor Manufacturing Company Limited and Lam Research Corporation diversify their income streams and where their primary sector bets lie:

Taiwan Semiconductor leans heavily on its Wafer segment, generating over 1.9T TWD in 2022, dwarfing its Other Products revenue of 272B TWD. This concentration signals a dominant infrastructure moat but also poses concentration risk. Lam Research displays a more balanced mix, with System revenue around 11.5B USD and Customer Support near 7B USD in 2025. This diversification supports resilience through aftermarket services and equipment sales, reducing dependence on a single segment.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of TSM and LRCX based on diversification, profitability, financials, innovation, global presence, and market share:

TSM Strengths

- High net margin at 45.1%

- Strong ROE of 32.12%

- Low debt-to-assets at 12.52%

- Favorable current and quick ratios

- Diverse geographic revenue including US and China

- Large wafer segment revenue

LRCX Strengths

- Very high ROE at 54.33%

- Strong ROIC of 34.0%

- Favorable interest coverage ratio

- Balanced debt level with 22.28% debt-to-assets

- High fixed asset turnover of 7.59

- Broad geographic reach including Korea and Taiwan

TSM Weaknesses

- Unfavorable P/E and P/B ratios indicate premium valuation

- Asset turnover at 0.49 is low

- Dividend yield below 1%

- Neutral WACC at 9.73%

- Limited product diversification outside wafer segment

LRCX Weaknesses

- Unfavorable WACC at 12.09% raises capital cost

- Unfavorable P/B ratio of 12.69

- Dividend yield below 1%

- Asset turnover only neutral at 0.86

- Smaller revenue base compared to TSM

TSM’s strengths lie in its strong profitability and solid balance sheet, supported by a dominant wafer business and global footprint. LRCX excels in capital efficiency and return metrics with a broader product and geographic diversification. Both face valuation and yield challenges that could impact their capital allocation and growth strategies.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only true shield protecting long-term profits from relentless competition erosion. Let’s dissect the competitive moats of two semiconductor giants:

Taiwan Semiconductor Manufacturing Company Limited: Scale and Technological Leadership Moat

TSMC leverages unmatched scale and advanced process technology, reflected in a soaring ROIC well above WACC by 15.2%, with a robust 32% ROIC growth. Its dominant foundry position supports stable high margins near 53% EBIT, and ongoing innovation in 2026 promises deeper market entrenchment.

Lam Research Corporation: Specialized Equipment and Customer Intimacy Moat

Lam Research’s moat lies in specialized semiconductor equipment with a ROIC premium of 21.9%, albeit with a modest 5.5% growth trend. Unlike TSMC’s scale, Lam relies on customer stickiness and technological precision, sustaining solid 32% EBIT margins. Expansion into new etch and deposition technologies could disrupt industry dynamics further.

Scale Dominance vs. Precision Engineering: Who Holds the Deeper Moat?

TSMC’s moat is broader, driven by scale economies and continuous tech leadership, fueling faster ROIC growth and margin stability. Lam’s moat is narrower but deeper in niche expertise. Overall, TSMC stands better equipped to defend and expand its market share amid intensifying global competition.

Which stock offers better returns?

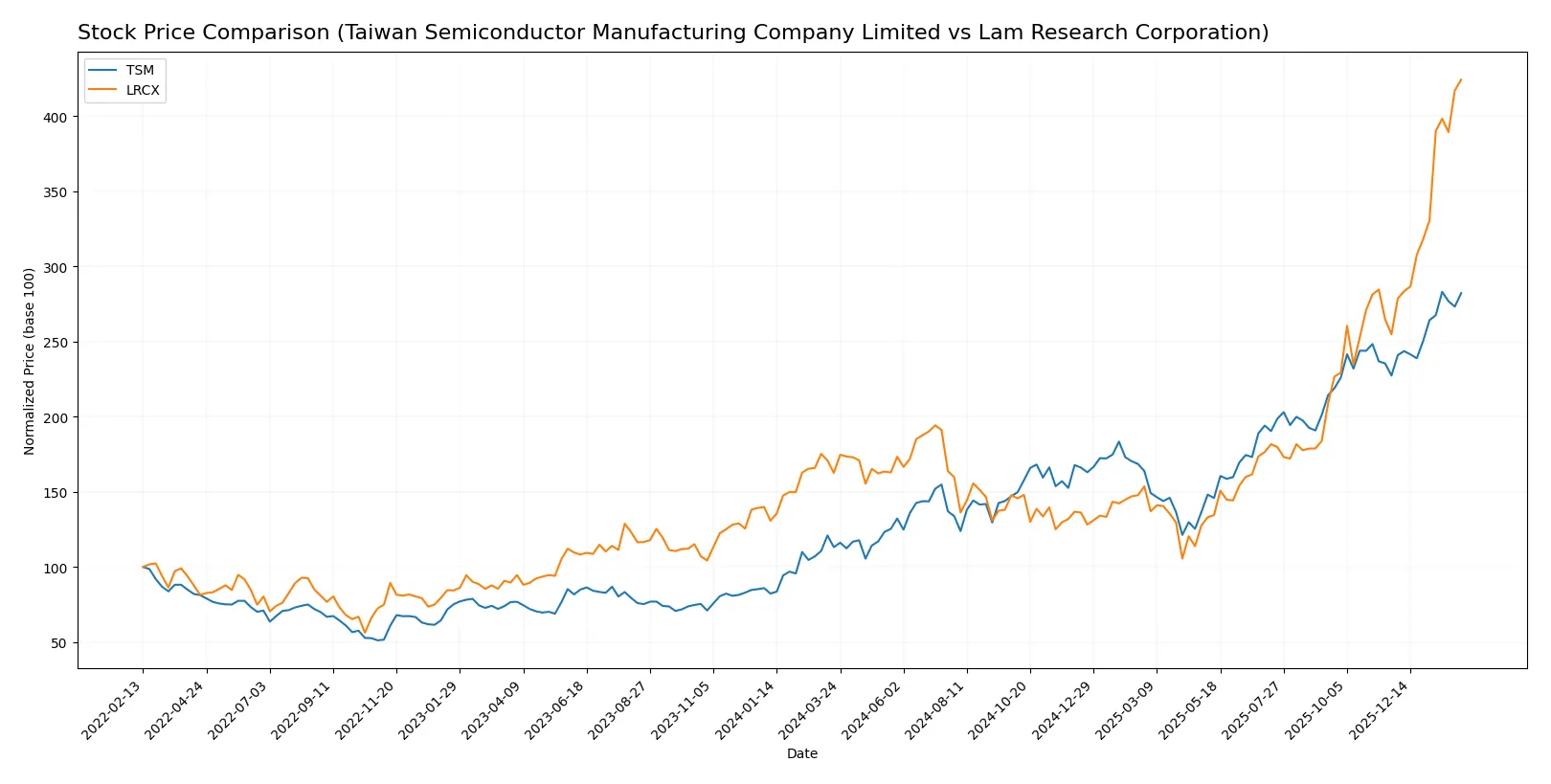

The past year reveals strong bullish momentum for both stocks, with Lam Research showing a sharper rise and more decisive buyer dominance recently.

Trend Comparison

Taiwan Semiconductor’s stock surged 149.2% over 12 months, showing acceleration and a high volatility with a 54.84 std deviation. Its recent 24.1% gain reflects a decelerating but positive trend.

Lam Research outperformed with a 160.96% rise, also accelerating and less volatile at 39.19 std deviation. Recent gains accelerated sharply by 66.49%, supported by strong buyer dominance.

Lam Research delivered higher total returns and stronger recent momentum than Taiwan Semiconductor, driven by accelerating price gains and robust buyer activity.

Target Prices

Analysts present a cautiously optimistic consensus on semiconductor leaders TSM and LRCX.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Taiwan Semiconductor Manufacturing Company Limited | 330 | 450 | 397.5 |

| Lam Research Corporation | 127 | 325 | 266.76 |

The consensus target prices for TSM and LRCX imply upside potential of roughly 16% and 12%, respectively, compared to current prices near 341 and 238. This suggests steady confidence in their semiconductor cycle positioning.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

The following tables summarize recent institutional grades for Taiwan Semiconductor Manufacturing Company Limited and Lam Research Corporation:

Taiwan Semiconductor Manufacturing Company Limited Grades

This table presents the latest grading actions and grades from leading firms.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| TD Cowen | maintain | Hold | 2026-01-16 |

| Barclays | maintain | Overweight | 2026-01-16 |

| Needham | maintain | Buy | 2026-01-15 |

| Bernstein | maintain | Outperform | 2025-12-08 |

| Needham | maintain | Buy | 2025-10-27 |

| Barclays | maintain | Overweight | 2025-10-17 |

| Needham | maintain | Buy | 2025-10-16 |

| Susquehanna | maintain | Positive | 2025-10-10 |

| Barclays | maintain | Overweight | 2025-10-09 |

| Barclays | maintain | Overweight | 2025-09-16 |

Lam Research Corporation Grades

This table shows the most recent grades and actions from prominent institutions.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| UBS | maintain | Buy | 2026-01-29 |

| Wells Fargo | maintain | Overweight | 2026-01-29 |

| JP Morgan | maintain | Overweight | 2026-01-29 |

| RBC Capital | maintain | Outperform | 2026-01-29 |

| Citigroup | maintain | Buy | 2026-01-29 |

| Stifel | maintain | Buy | 2026-01-29 |

| Morgan Stanley | maintain | Equal Weight | 2026-01-29 |

| Needham | maintain | Buy | 2026-01-29 |

| Susquehanna | maintain | Positive | 2026-01-29 |

| Goldman Sachs | maintain | Buy | 2026-01-29 |

Which company has the best grades?

Lam Research Corporation consistently receives Buy or better ratings from multiple top-tier firms. Taiwan Semiconductor’s grades cluster more around Hold to Buy. Investors may view Lam Research’s stronger consensus grades as a sign of greater institutional confidence.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

Taiwan Semiconductor Manufacturing Company Limited

- Dominates foundry with advanced technology but faces intense global competition and capacity constraints.

Lam Research Corporation

- Competes in a niche market for semiconductor equipment with exposure to cyclical demand fluctuations.

2. Capital Structure & Debt

Taiwan Semiconductor Manufacturing Company Limited

- Maintains a conservative debt-to-equity ratio of 0.18, implying strong financial stability and low leverage risk.

Lam Research Corporation

- Higher debt-to-equity ratio of 0.48 reflects more leverage, increasing financial risk but also potential growth capacity.

3. Stock Volatility

Taiwan Semiconductor Manufacturing Company Limited

- Beta of 1.27 indicates moderate volatility, slightly above market average but relatively stable for a tech giant.

Lam Research Corporation

- Beta of 1.78 signals higher sensitivity to market swings, suggesting greater risk for investors seeking stability.

4. Regulatory & Legal

Taiwan Semiconductor Manufacturing Company Limited

- Faces geopolitical regulatory risks due to significant operations in Taiwan and strained US-China relations.

Lam Research Corporation

- Subject to US regulatory environment with risks from export controls and international trade tensions.

5. Supply Chain & Operations

Taiwan Semiconductor Manufacturing Company Limited

- Highly reliant on rare materials and advanced manufacturing processes, vulnerable to supply disruptions.

Lam Research Corporation

- Dependent on global semiconductor manufacturing cycles and supply chain efficiency, sensitive to operational delays.

6. ESG & Climate Transition

Taiwan Semiconductor Manufacturing Company Limited

- Increasing pressure to reduce carbon footprint amid energy-intensive chip production in Taiwan.

Lam Research Corporation

- Actively adopting cleaner manufacturing technologies but still faces challenges in waste and emissions reduction.

7. Geopolitical Exposure

Taiwan Semiconductor Manufacturing Company Limited

- Exposure to Taiwan-China tensions poses a systemic risk to operations and shareholder value.

Lam Research Corporation

- Geopolitical risk mainly from US-China trade tensions impacting supply chains and customer base.

Which company shows a better risk-adjusted profile?

Taiwan Semiconductor’s biggest risk is geopolitical exposure, which threatens its core manufacturing base. Lam Research’s critical risk lies in higher financial leverage and market volatility. Despite this, Lam’s superior asset turnover and strong Altman Z-score suggest it manages operational risk well. Taiwan Semiconductor offers stability but with systemic geopolitical concerns. Overall, Lam Research shows a slightly better risk-adjusted profile given its balance of growth potential and financial strength, despite elevated volatility and debt.

Final Verdict: Which stock to choose?

Taiwan Semiconductor Manufacturing Company Limited (TSM) shines as a cash-generating powerhouse with a durable moat reflected in its strong ROIC growth. Its main point of vigilance lies in a relatively high price-to-book ratio, which could pressure valuation. TSM suits investors eyeing aggressive growth with a focus on operational efficiency.

Lam Research Corporation (LRCX) offers a compelling strategic moat through its commanding position in semiconductor equipment and recurring revenue streams. It presents a safer profile with moderate leverage and superior asset turnover compared to TSM. LRCX fits well in GARP portfolios seeking growth balanced with reasonable risk.

If you prioritize aggressive growth fueled by operational excellence and durable competitive advantage, TSM is the compelling choice due to its superior cash flow generation and expanding profitability. However, if you seek a blend of growth and stability with a strong industry moat and better asset efficiency, LRCX offers better stability and a more balanced risk-return profile.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Taiwan Semiconductor Manufacturing Company Limited and Lam Research Corporation to enhance your investment decisions: