Home > Comparison > Technology > LRCX vs INDI

The strategic rivalry between Lam Research Corporation and indie Semiconductor, Inc. shapes the semiconductor industry’s evolution. Lam Research operates as a capital-intensive leader in semiconductor fabrication equipment, while indie Semiconductor focuses on specialized automotive semiconductor solutions. This contrast highlights a battle between established manufacturing scale and innovative niche growth. This analysis will clarify which company offers a superior risk-adjusted outlook for investors seeking diversified exposure within the technology sector.

Table of contents

Companies Overview

Lam Research and indie Semiconductor command crucial roles in the semiconductor industry’s evolving landscape.

Lam Research Corporation: Semiconductor Equipment Innovator

Lam Research dominates as a leading designer and manufacturer of semiconductor processing equipment. Its revenue stems from advanced systems like ALTUS for tungsten metallization and SABRE for copper interconnects. In 2026, the company focuses on expanding high-precision wafer fabrication tools to meet global chipmakers’ demand for smaller, faster integrated circuits.

indie Semiconductor, Inc.: Automotive Chip Specialist

indie Semiconductor specializes in automotive semiconductors and software, catering to advanced driver assistance and connected car markets. It generates revenue through devices supporting parking assistance, infotainment, and electrification. Its 2026 strategy centers on enhancing photonic components and wireless charging solutions to capture growth in automotive technology integration.

Strategic Collision: Similarities & Divergences

Both firms innovate within semiconductors but diverge sharply—Lam Research invests in capital-intensive fabrication equipment, while indie Semiconductor pursues software-driven automotive applications. Their primary battle lies in the semiconductor value chain’s upstream versus downstream segments. This contrast yields distinct investment profiles: Lam offers scale and stability; indie carries higher volatility but targets fast-growing automotive tech niches.

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Lam Research Corporation (LRCX) | indie Semiconductor, Inc. (INDI) |

|---|---|---|

| Revenue | 18.4B | 217M |

| Cost of Revenue | 9.46B | 126M |

| Operating Expenses | 3.08B | 260M |

| Gross Profit | 8.98B | 90.3M |

| EBITDA | 6.34B | -94M |

| EBIT | 5.96B | -137M |

| Interest Expense | 178M | 9.26M |

| Net Income | 5.36B | -133M |

| EPS | 4.17 | -0.76 |

| Fiscal Year | 2025 | 2024 |

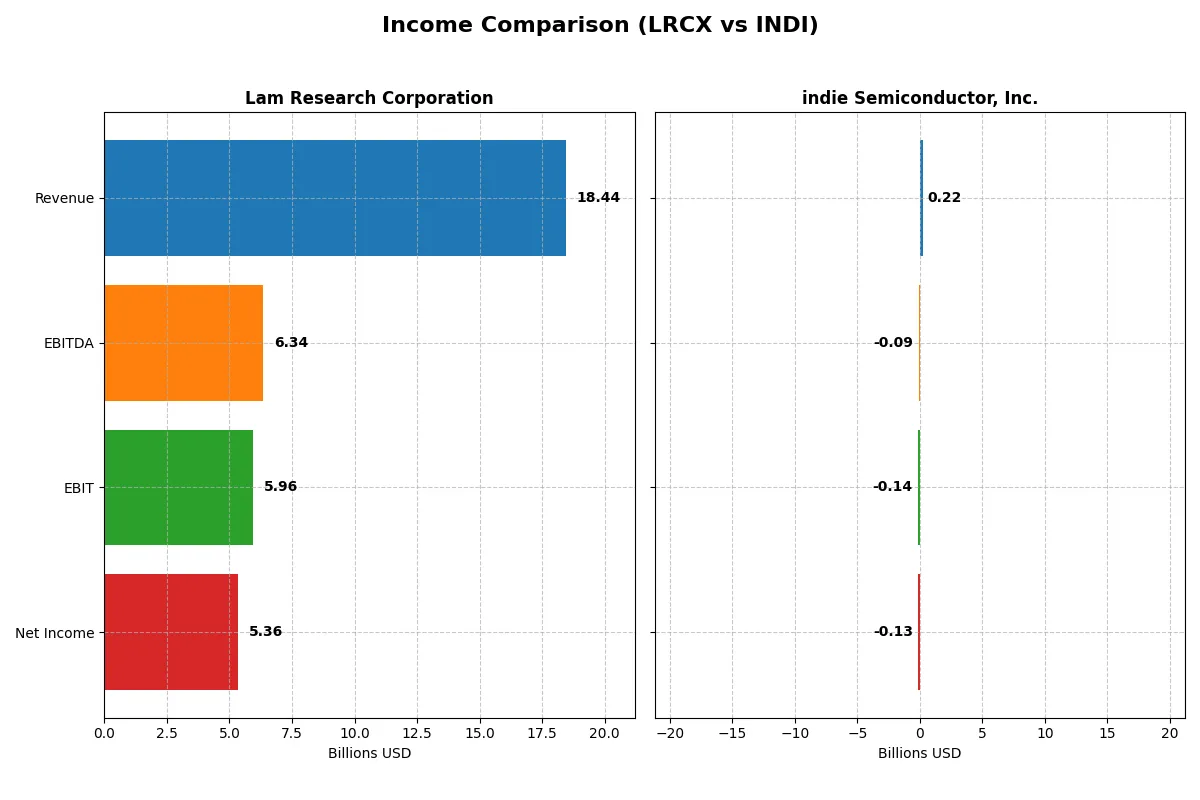

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company runs a more efficient and profitable corporate engine through recent financial performance.

Lam Research Corporation (LRCX) Analysis

LRCX steadily grows revenue, reaching $18.4B in 2025, up 24% year-over-year. Net income climbs to $5.36B, with a strong net margin of 29%. Gross and EBIT margins remain healthy at 49% and 32%, respectively. The company demonstrates momentum with a 31% EBIT growth and solid expense control, reflecting operational efficiency.

indie Semiconductor, Inc. (INDI) Analysis

INDI’s revenue declines slightly by 2.9% to $217M in 2024, but gross profit surges 264% to $90M, showing improving product mix. Despite this, EBIT and net margins remain deeply negative at -63% and -61%, with a net loss of $133M. The company struggles with high operating expenses and negative profitability, though EPS shows modest improvement.

Margin Power vs. Revenue Scale

LRCX clearly outperforms INDI with robust profitability and consistent revenue growth. Lam Research delivers strong margins and expanding earnings, offering operational strength. Indie Semiconductor, while showing some gross profit improvement, remains loss-making and less efficient. Investors seeking stable, profitable growth will find LRCX’s profile more attractive.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Lam Research Corporation (LRCX) | indie Semiconductor, Inc. (INDI) |

|---|---|---|

| ROE | 54.3% (2025) | -31.7% (2024) |

| ROIC | 34.0% (2025) | -19.3% (2024) |

| P/E | 23.4 (2025) | -5.35 (2024) |

| P/B | 12.7 (2025) | 1.70 (2024) |

| Current Ratio | 2.21 (2025) | 4.82 (2024) |

| Quick Ratio | 1.55 (2025) | 4.23 (2024) |

| D/E | 0.48 (2025) | 0.95 (2024) |

| Debt-to-Assets | 22.3% (2025) | 42.3% (2024) |

| Interest Coverage | 33.1 (2025) | -18.4 (2024) |

| Asset Turnover | 0.86 (2025) | 0.23 (2024) |

| Fixed Asset Turnover | 7.59 (2025) | 4.30 (2024) |

| Payout ratio | 21.5% (2025) | 0% (2024) |

| Dividend yield | 0.92% (2025) | 0% (2024) |

| Fiscal Year | 2025 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as a company’s DNA, unveiling hidden risks and operational strengths crucial for informed investment decisions.

Lam Research Corporation

Lam Research displays robust profitability with a 54.33% ROE and a healthy 29.06% net margin, signaling operational excellence. Its valuation metrics—P/E at 23.36 and P/S near 6.7—position the stock in a neutral to slightly stretched range. The firm returns value via dividends, though at a modest 0.92% yield, indicating solid shareholder rewards alongside sustained R&D investment.

indie Semiconductor, Inc.

indie Semiconductor suffers from deep losses, shown by a -31.73% ROE and a steep -61.2% net margin. Its negative P/E of -5.35 reflects earnings challenges but a relatively low P/B of 1.7 suggests valuation neutrality. The company pays no dividends, instead focusing heavily on R&D (over 80% of revenue), reflecting a growth-oriented reinvestment strategy amid operational strains.

Premium Valuation vs. Operational Struggles

Lam Research offers a superior balance of profitability and valuation discipline, with many favorable ratios and consistent shareholder returns. indie Semiconductor’s metrics reveal high risk from persistent losses and negative cash flows. Investors seeking stability gravitate toward Lam, while those with high risk tolerance may consider indie’s growth focus.

Which one offers the Superior Shareholder Reward?

Lam Research Corporation (LRCX) pays a consistent dividend with a yield near 0.9%, supported by a sustainable payout ratio around 21%. Its free cash flow comfortably covers dividends and buybacks, which have been significant, enhancing total shareholder returns. Indie Semiconductor, Inc. (INDI) pays no dividends and suffers persistent losses, negative free cash flow, and a weak earnings profile. It reinvests heavily in R&D and growth but lacks buyback programs. Historically, LRCX’s balanced distribution strategy delivers more reliable, long-term value. I conclude LRCX offers a far superior total return profile for investors in 2026.

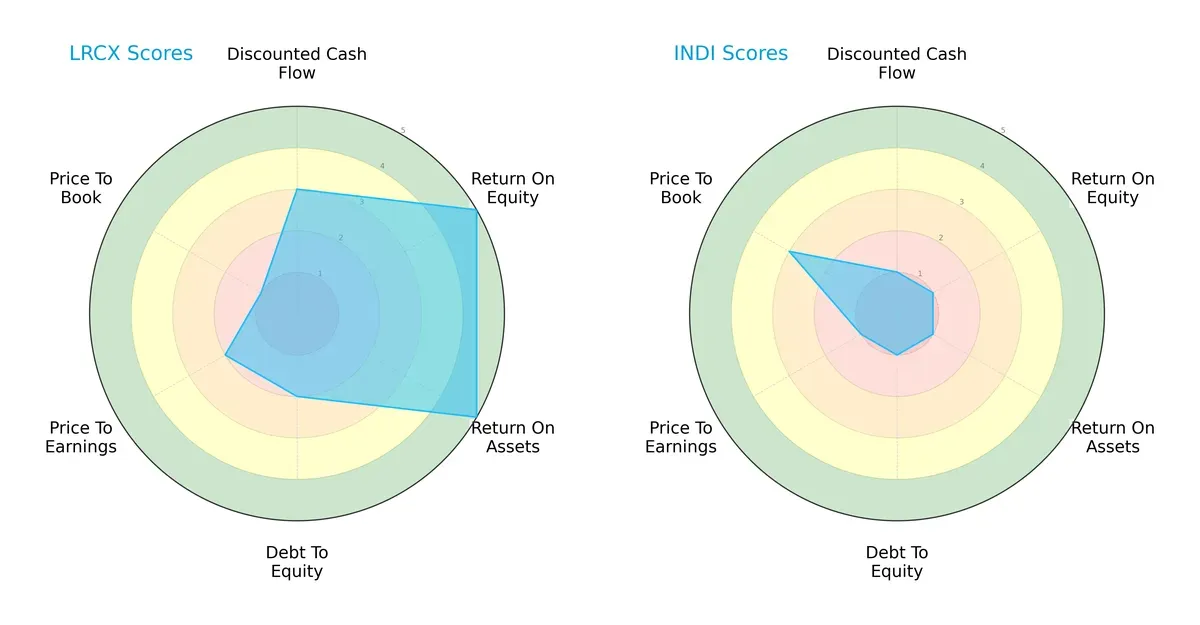

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Lam Research Corporation and indie Semiconductor, Inc.:

Lam Research exhibits a balanced profile with very favorable ROE and ROA scores, signaling efficient profit generation and asset use. Its moderate DCF and debt levels contrast with a weak valuation (P/B). Indie Semiconductor relies heavily on a single edge with uniformly low scores except for a moderate P/B, indicating valuation concerns but poor operational metrics. Lam Research’s diversified strengths offer a more stable investment thesis.

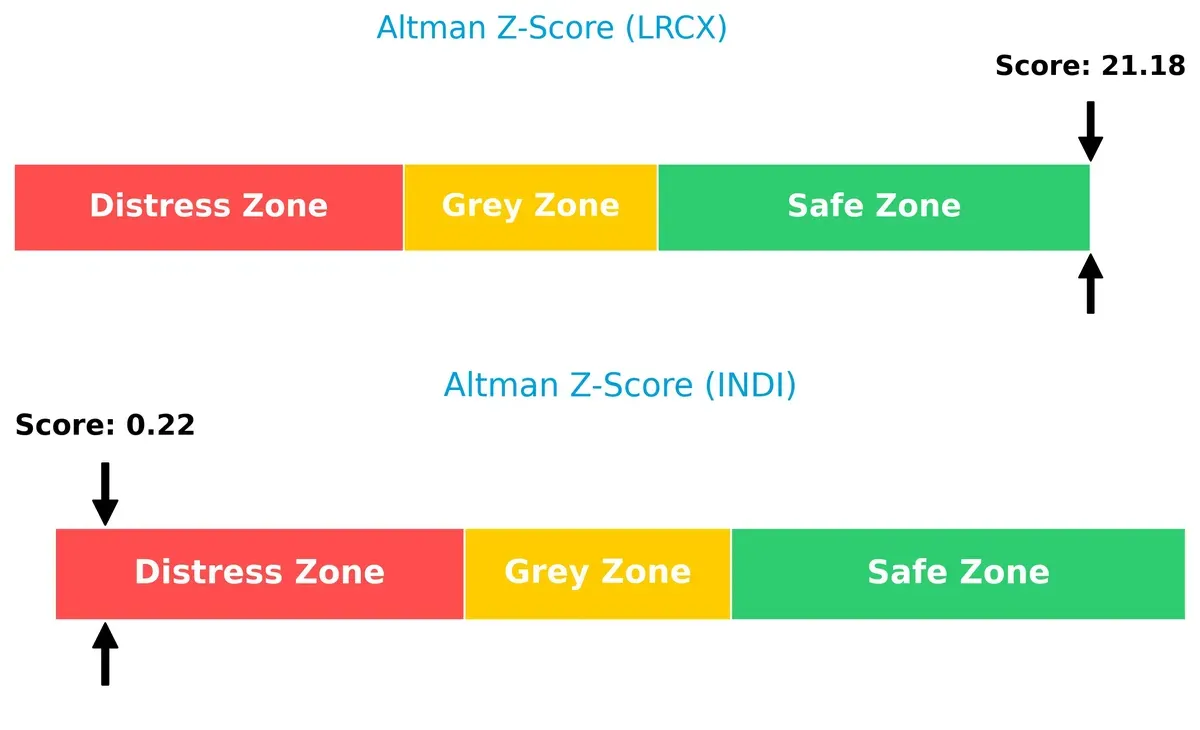

Bankruptcy Risk: Solvency Showdown

Lam Research’s Altman Z-Score of 21.2 places it firmly in the safe zone, while indie Semiconductor’s 0.22 signals distress, implying high bankruptcy risk in this cycle:

Financial Health: Quality of Operations

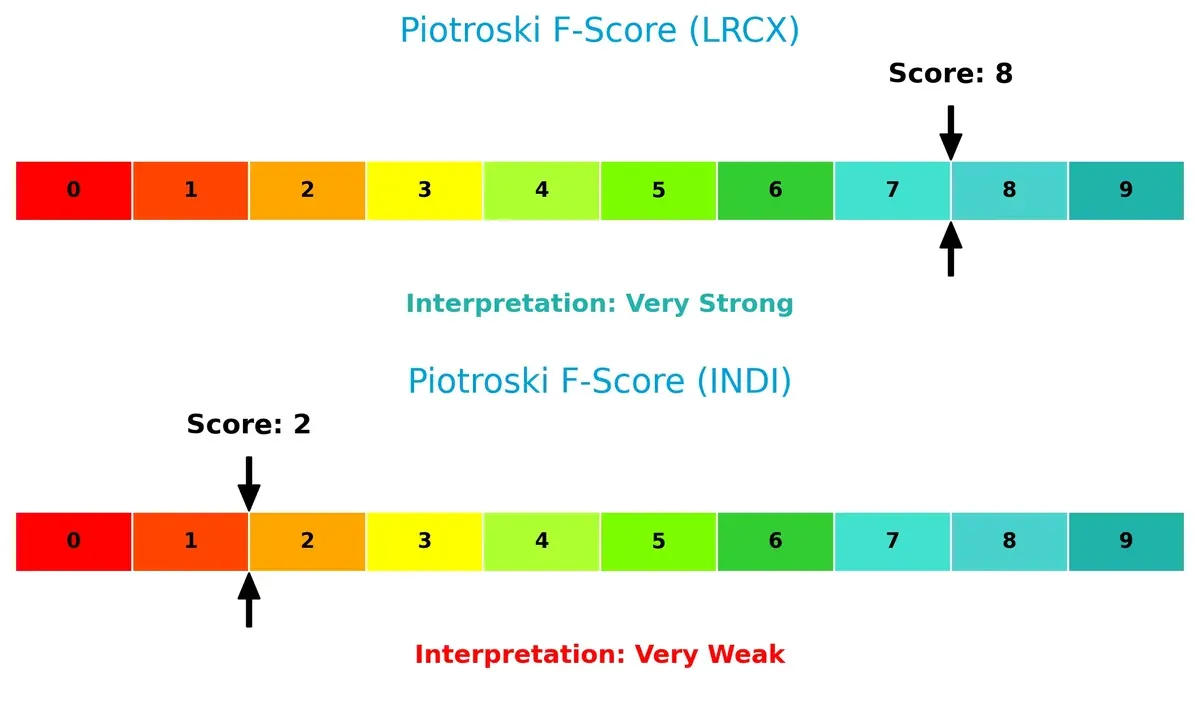

Lam Research scores an 8 on the Piotroski F-Score, indicating very strong financial health. Indie Semiconductor’s score of 2 raises red flags about operational and financial stability:

How are the two companies positioned?

This section dissects the operational DNA of Lam Research and indie Semiconductor by comparing their revenue distribution and internal dynamics. The goal is to confront their economic moats to reveal which model offers the most resilient competitive advantage today.

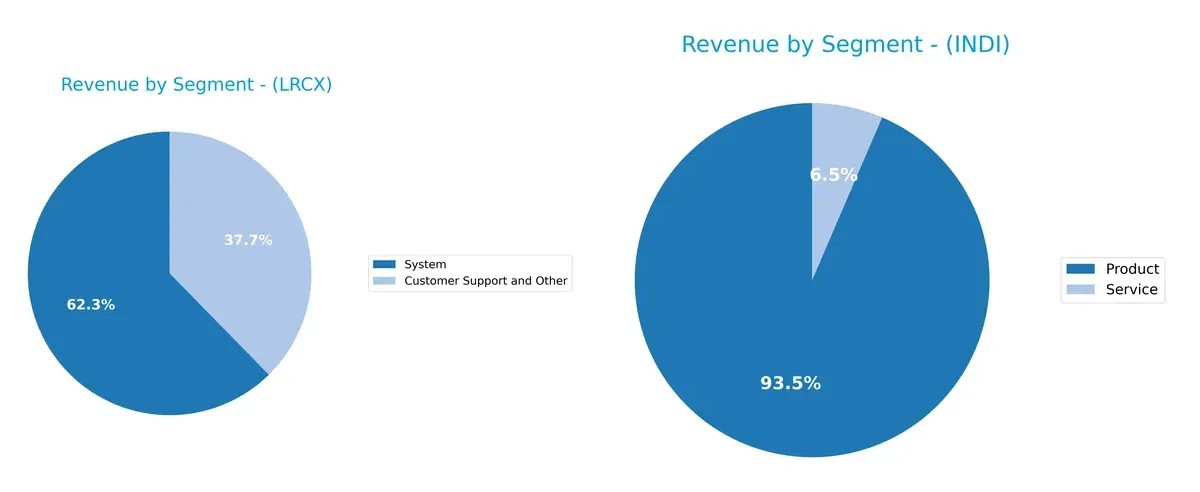

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Lam Research Corporation and indie Semiconductor, Inc. diversify their income streams and reveals where their primary sector bets lie:

Lam Research anchors its revenue in the System segment, generating $11.5B in 2025, nearly doubling the $6.9B from Customer Support. This mix balances recurring support income with high-value systems sales, reducing concentration risk. Indie Semiconductor pivots heavily on Product sales, $203M in 2024, dwarfing its $14M Service revenue. The reliance on a dominant Product segment raises concentration risk but signals strong product-market fit and potential ecosystem lock-in.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Lam Research Corporation and indie Semiconductor, Inc.:

Lam Research Corporation Strengths

- Strong profitability with 29.06% net margin

- High ROE at 54.33% and ROIC of 34.0%

- Favorable liquidity ratios (current 2.21, quick 1.55)

- Global revenue presence including China, Korea, US

- High fixed asset turnover of 7.59 indicates efficient asset use

- Diverse revenue streams from System and Customer Support segments

indie Semiconductor, Inc. Strengths

- Favorable P/E ratio despite negative earnings

- Quick ratio strong at 4.23 indicating good short-term liquidity

- Fixed asset turnover at 4.3 shows some asset efficiency

- Presence in multiple geographies including China and US

- Product revenue significantly larger than service revenue

Lam Research Corporation Weaknesses

- High WACC at 12.05% raises capital cost concerns

- Unfavorable price-to-book ratio at 12.69 suggests overvaluation

- Dividend yield low at 0.92%

- Asset turnover neutral at 0.86, room for improvement

indie Semiconductor, Inc. Weaknesses

- Negative profitability metrics with net margin -61.2% and ROE -31.73%

- Unfavorable interest coverage at -14.8 indicates financial stress

- High debt-to-equity at 0.95, signaling leverage risk

- Low asset turnover at 0.23 implies inefficiency

- No dividend yield, reflecting cash flow issues

- High current ratio of 4.82 may indicate inefficient working capital use

Lam Research exhibits robust profitability and efficient capital use, supporting its global market position. Indie Semiconductor struggles with profitability and operational efficiency, implying challenges in financial stability and asset utilization.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only reliable shield protecting long-term profits from relentless competitive erosion in dynamic sectors like semiconductors:

Lam Research Corporation: Precision Engineering and Scale Moat

Lam Research’s moat stems from its intangible assets and process expertise, reflected in a strong 29% net margin and a 22% ROIC premium over WACC. Its scale and advanced wafer fabrication tools secure high switching costs. In 2026, expanding into emerging markets and next-gen etch technologies could deepen this moat.

indie Semiconductor, Inc.: Emerging Innovation with Fragile Moat

Indie Semiconductor relies on product innovation in automotive chips but lacks Lam’s scale and margin stability, posting a deeply negative ROIC and net margin. Its competitive edge is narrower and more volatile. Future growth hinges on capturing connected car market share, but this remains a risky path.

Scale and Efficiency vs. Innovation Risk

Lam Research owns a wider, more durable moat with consistent value creation and margin strength. Indie Semiconductor’s moat is vulnerable due to negative returns and shrinking profitability. Consequently, Lam is far better positioned to defend and grow its market share in 2026.

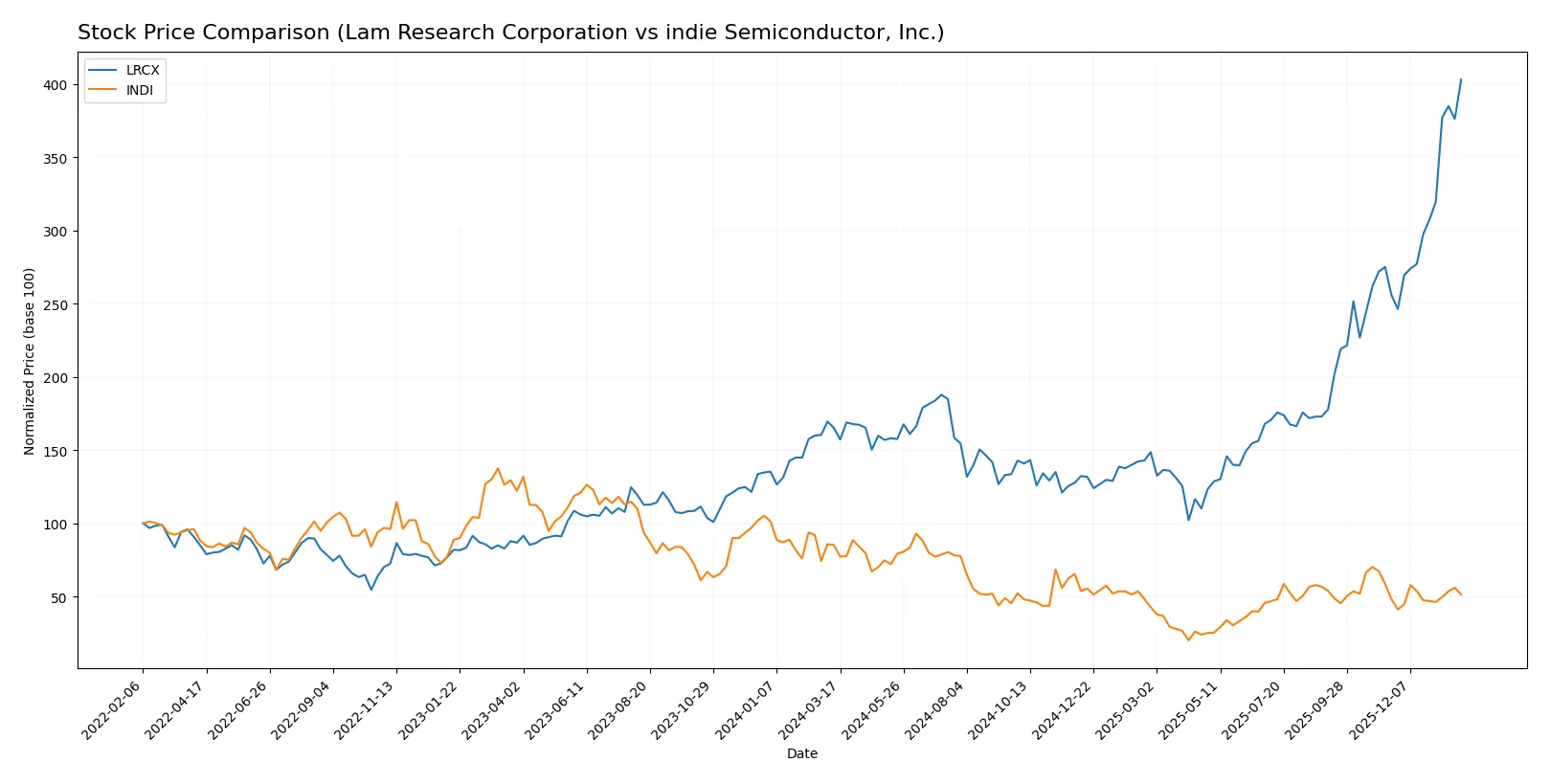

Which stock offers better returns?

Over the past year, Lam Research Corporation surged 144%, showing accelerating bullish momentum, while indie Semiconductor, Inc. declined nearly 40%, reflecting a strong bearish trend.

Trend Comparison

Lam Research’s stock price rose 144.03% over the past 12 months, marking a clear bullish trend with accelerating momentum and high volatility (36.82 std deviation). It hit a low of 59.09 and peaked at 233.46.

indie Semiconductor’s stock dropped 39.79% over the same period, indicating a bearish trend with accelerating downside. Price volatility remained low (1.32 std deviation), fluctuating between 1.6 and 7.43.

Lam Research outperformed indie Semiconductor significantly, delivering strong bullish returns versus a sustained bearish decline in the semiconductor stock.

Target Prices

Analysts present a wide target price range for Lam Research and a firm target on indie Semiconductor.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Lam Research Corp | 127 | 325 | 266.76 |

| indie Semiconductor | 8 | 8 | 8 |

Lam Research’s consensus target of 266.76 suggests upside potential from the current 233.46 price. Indie Semiconductor’s target at 8 doubles its current 4.1 price, indicating strong growth expectations.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Both Lam Research Corporation and indie Semiconductor, Inc. have received multiple institutional grades from reputable sources:

Lam Research Corporation Grades

Here are the recent grades issued by leading financial institutions for Lam Research Corporation:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| UBS | Maintain | Buy | 2026-01-29 |

| Wells Fargo | Maintain | Overweight | 2026-01-29 |

| JP Morgan | Maintain | Overweight | 2026-01-29 |

| RBC Capital | Maintain | Outperform | 2026-01-29 |

| Citigroup | Maintain | Buy | 2026-01-29 |

| Stifel | Maintain | Buy | 2026-01-29 |

| Morgan Stanley | Maintain | Equal Weight | 2026-01-29 |

| Needham | Maintain | Buy | 2026-01-29 |

| Susquehanna | Maintain | Positive | 2026-01-29 |

| Goldman Sachs | Maintain | Buy | 2026-01-29 |

indie Semiconductor, Inc. Grades

The following table shows the recent institutional grades for indie Semiconductor, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| UBS | Maintain | Neutral | 2025-11-10 |

| Benchmark | Maintain | Buy | 2025-06-25 |

| Benchmark | Maintain | Buy | 2025-06-11 |

| Benchmark | Maintain | Buy | 2025-05-21 |

| Benchmark | Maintain | Buy | 2025-05-13 |

| Craig-Hallum | Maintain | Buy | 2025-05-13 |

| Keybanc | Maintain | Overweight | 2025-05-13 |

| Benchmark | Maintain | Buy | 2025-04-09 |

| Benchmark | Maintain | Buy | 2025-02-21 |

| Keybanc | Maintain | Overweight | 2025-02-21 |

Which company has the best grades?

Lam Research Corporation consistently receives strong buy and outperform recommendations from major banks, reflecting high institutional confidence. indie Semiconductor’s grades are mostly buy or overweight but include a neutral rating from UBS, suggesting a more cautious view. Investors may interpret Lam Research’s grades as a stronger vote of confidence in its market position.

Risks specific to each company

The following categories identify critical pressure points and systemic threats facing Lam Research Corporation and indie Semiconductor, Inc. in the 2026 market environment:

1. Market & Competition

Lam Research Corporation

- Dominates semiconductor equipment with a strong market presence and global reach.

indie Semiconductor, Inc.

- Faces intense competition in automotive semiconductor niche with smaller scale and limited market share.

2. Capital Structure & Debt

Lam Research Corporation

- Maintains moderate debt levels (D/E 0.48) with robust interest coverage (33.43), signaling strong financial stability.

indie Semiconductor, Inc.

- Carries higher leverage (D/E 0.95) and negative interest coverage (-14.8), indicating financial stress and refinancing risks.

3. Stock Volatility

Lam Research Corporation

- Beta of 1.78 suggests elevated but manageable stock volatility compared to the S&P 500 benchmark.

indie Semiconductor, Inc.

- Beta of 2.54 indicates very high volatility, increasing investment risk amid market fluctuations.

4. Regulatory & Legal

Lam Research Corporation

- Operates globally with regulatory oversight in multiple jurisdictions but benefits from established compliance frameworks.

indie Semiconductor, Inc.

- Faces evolving automotive and technology regulations with potential legal risks from rapid innovation cycles.

5. Supply Chain & Operations

Lam Research Corporation

- Complex global supply chain with proven resilience but vulnerable to geopolitical tensions and raw material costs.

indie Semiconductor, Inc.

- Smaller scale supply chain may lack diversification, increasing risks from component shortages or disruptions.

6. ESG & Climate Transition

Lam Research Corporation

- Actively integrates ESG initiatives to meet investor and regulatory expectations, bolstering long-term sustainability.

indie Semiconductor, Inc.

- Early-stage ESG programs with potential exposure to regulatory pressure and investor scrutiny on climate risks.

7. Geopolitical Exposure

Lam Research Corporation

- Significant exposure to Asia-Pacific markets, notably China, risking impact from US-China trade tensions.

indie Semiconductor, Inc.

- Limited global footprint but vulnerable to supply chain shocks due to concentration in key regions.

Which company shows a better risk-adjusted profile?

Lam Research’s dominant market position and solid financial health mitigate risks effectively. Indie Semiconductor’s fragile profitability, high leverage, and extreme volatility elevate its risk profile. Lam’s Altman Z-Score of 21.2 vs. indie’s 0.22 confirms superior stability. Market competition pressures indie’s automotive niche, while Lam’s exposure to geopolitical tensions remains manageable for now. Overall, Lam Research offers a markedly better risk-adjusted investment profile in 2026.

Final Verdict: Which stock to choose?

Lam Research Corporation’s superpower lies in its durable competitive advantage, marked by a strong and growing ROIC well above its cost of capital. It efficiently converts invested capital into value, fueling consistent profitability and cash generation. A point of vigilance is its premium valuation metrics, which may pressure returns if growth slows. It suits an Aggressive Growth portfolio focused on quality leadership in semiconductor equipment.

indie Semiconductor’s strategic moat is its heavy investment in R&D, aiming to carve out new markets in semiconductor tech. However, it currently struggles with negative returns and cash flow, reflecting early-stage risks and capital intensity. Compared to Lam, it offers a speculative opportunity with a higher risk profile, fitting a GARP (Growth at a Reasonable Price) portfolio that tolerates volatility for potential breakthrough innovation.

If you prioritize capital efficiency and proven value creation, Lam Research outshines indie Semiconductor due to its strong financial moat and stable growth trajectory. However, if you seek early-stage growth with potential technological leaps and can endure financial instability, indie Semiconductor offers a speculative play. Both cases require careful risk management aligned to your investment horizon and risk tolerance.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Lam Research Corporation and indie Semiconductor, Inc. to enhance your investment decisions: