In the fast-evolving software application industry, Salesforce, Inc. (CRM) and Intuit Inc. (INTU) stand out as leaders, each driving innovation in customer relationship management and financial technology. Both companies serve overlapping markets with complementary solutions, making their strategies and growth prospects worthy of comparison. This analysis aims to help you, the investor, identify which company offers the most compelling opportunity for your portfolio in 2026.

Table of contents

Companies Overview

I will begin the comparison between Salesforce and Intuit by providing an overview of these two companies and their main differences.

Salesforce Overview

Salesforce, Inc. focuses on customer relationship management (CRM) technology that connects companies and customers globally. Its Customer 360 platform delivers integrated experiences through services in sales, service, marketing, commerce, and analytics. The company supports businesses across various industries with flexible platforms and tools, including Slack and Tableau. Headquartered in San Francisco, Salesforce had a market cap of $219B and employs over 76K people as of 2026.

Intuit Overview

Intuit Inc. provides financial management and compliance software and services for consumers, small businesses, and professionals. Its offerings include QuickBooks for business accounting, TurboTax for tax preparation, Credit Karma for personal finance, and ProConnect for professional tax solutions. Based in Mountain View, California, Intuit holds a market cap of $151B and has a workforce of approximately 18.8K employees. The company serves customers primarily in the US, Canada, and internationally.

Key similarities and differences

Both Salesforce and Intuit operate in the software application industry, focusing on solutions that enhance business and financial operations. Salesforce’s model is centered on CRM and customer engagement platforms, while Intuit specializes in financial management and tax-related software. Salesforce’s broader industry reach contrasts with Intuit’s concentration on financial services and compliance. Both companies generate revenue through subscription services but target different core customer needs and market segments.

Income Statement Comparison

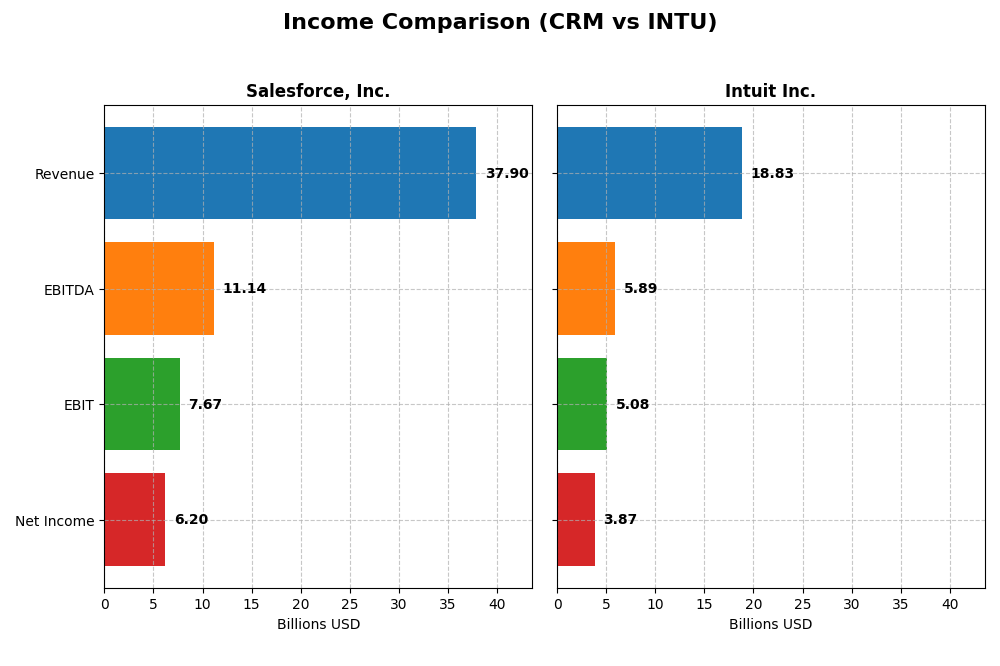

Below is a side-by-side comparison of the most recent fiscal year income statement metrics for Salesforce, Inc. and Intuit Inc.

| Metric | Salesforce, Inc. (CRM) | Intuit Inc. (INTU) |

|---|---|---|

| Market Cap | 219B | 151B |

| Revenue | 37.9B | 18.8B |

| EBITDA | 11.1B | 5.9B |

| EBIT | 7.7B | 5.1B |

| Net Income | 6.2B | 3.9B |

| EPS | 6.44 | 13.82 |

| Fiscal Year | 2025 | 2025 |

Income Statement Interpretations

Salesforce, Inc.

Salesforce has experienced consistent revenue growth from $21.3B in 2021 to $37.9B in 2025, with net income rising from $4.07B to $6.20B over the same period. Margins have generally improved, with a favorable gross margin of 77.19% and net margin of 16.35% in 2025. The most recent year showed solid growth in revenue (+8.7%) and net income (+37.8%), indicating accelerating profitability.

Intuit Inc.

Intuit’s revenue increased steadily from $9.63B in 2021 to $18.8B in 2025, with net income growing from $2.06B to $3.87B. Margins remain strong, with a gross margin of 80.76% and net margin of 20.55% in 2025. The latest fiscal year reflected robust revenue growth of 15.6% and a net income increase of 12.9%, suggesting continued operational efficiency and healthy earnings expansion.

Which one has the stronger fundamentals?

Both Salesforce and Intuit display favorable overall income statement trends, including strong revenue and net income growth, alongside solid margin profiles. Intuit shows higher margins and a greater overall net income growth rate (87.6% vs. 52.2%), while Salesforce demonstrates more significant recent net income margin improvement. Each exhibits strengths, with fundamentals that reflect sustained growth and profitability.

Financial Ratios Comparison

The table below presents the most recent key financial ratios for Salesforce, Inc. and Intuit Inc., offering a side-by-side view of their performance metrics as of their latest fiscal years.

| Ratios | Salesforce, Inc. (CRM) | Intuit Inc. (INTU) |

|---|---|---|

| ROE | 10.13% | 19.63% |

| ROIC | 7.95% | 14.78% |

| P/E | 53.04 | 56.82 |

| P/B | 5.37 | 11.15 |

| Current Ratio | 1.06 | 1.36 |

| Quick Ratio | 1.06 | 1.36 |

| D/E | 0.19 | 0.34 |

| Debt-to-Assets | 11.07% | 17.96% |

| Interest Coverage | 26.49 | 19.93 |

| Asset Turnover | 0.37 | 0.51 |

| Fixed Asset Turnover | 7.03 | 12.54 |

| Payout ratio | 24.80% | 30.73% |

| Dividend yield | 0.47% | 0.54% |

Interpretation of the Ratios

Salesforce, Inc.

Salesforce shows a mixed ratio profile with 43% favorable and 29% unfavorable ratios. Key strengths include a strong interest coverage (28.18) and low debt levels (D/E 0.19). However, high valuations indicated by a PE of 53.04 and PB of 5.37 are unfavorable. The dividend yield is low at 0.47%, suggesting limited income return relative to price.

Intuit Inc.

Intuit presents a more favorable ratio set, with 57% favorable and only 21% unfavorable. It boasts higher profitability and efficiency ratios, such as a 19.63% ROE and 12.54 fixed asset turnover, but also a high PE of 56.82 and PB of 11.15. Dividend yield is slightly higher than Salesforce at 0.54%, but still low in absolute terms.

Which one has the best ratios?

Intuit’s ratios are overall more favorable, with stronger profitability and asset efficiency metrics. Salesforce’s ratios are more balanced but include more unfavorable valuation multiples. Both companies pay dividends with low yields, and Intuit’s higher return metrics suggest a superior financial ratio profile in 2025.

Strategic Positioning

This section compares the strategic positioning of Salesforce, Inc. and Intuit Inc. across Market position, Key segments, and Exposure to technological disruption:

Salesforce, Inc.

- Market leader in CRM software with significant competitive pressure in cloud services.

- Diverse software segments: Sales, Service, Marketing, Commerce, Analytics, and Platform solutions.

- Exposed to disruption via cloud integration, AI-enhanced analytics, and platform expansion.

Intuit Inc.

- Strong player in financial management software with competition in consumer and business segments.

- Four segments focusing on Small Business, Consumer, Credit Karma, and Professional Tax services.

- Faces disruption in financial services and tax preparation through digital and cloud innovations.

Salesforce, Inc. vs Intuit Inc. Positioning

Salesforce has a diversified approach with multiple cloud-based business segments, offering broad enterprise software solutions. Intuit concentrates on financial management and tax-related software, targeting consumers and small businesses, with a narrower but focused portfolio.

Which has the best competitive advantage?

Intuit shows a slightly favorable MOAT by creating value despite declining profitability. Salesforce exhibits a slightly unfavorable MOAT, shedding value but improving profitability, indicating Intuit holds a stronger competitive advantage currently.

Stock Comparison

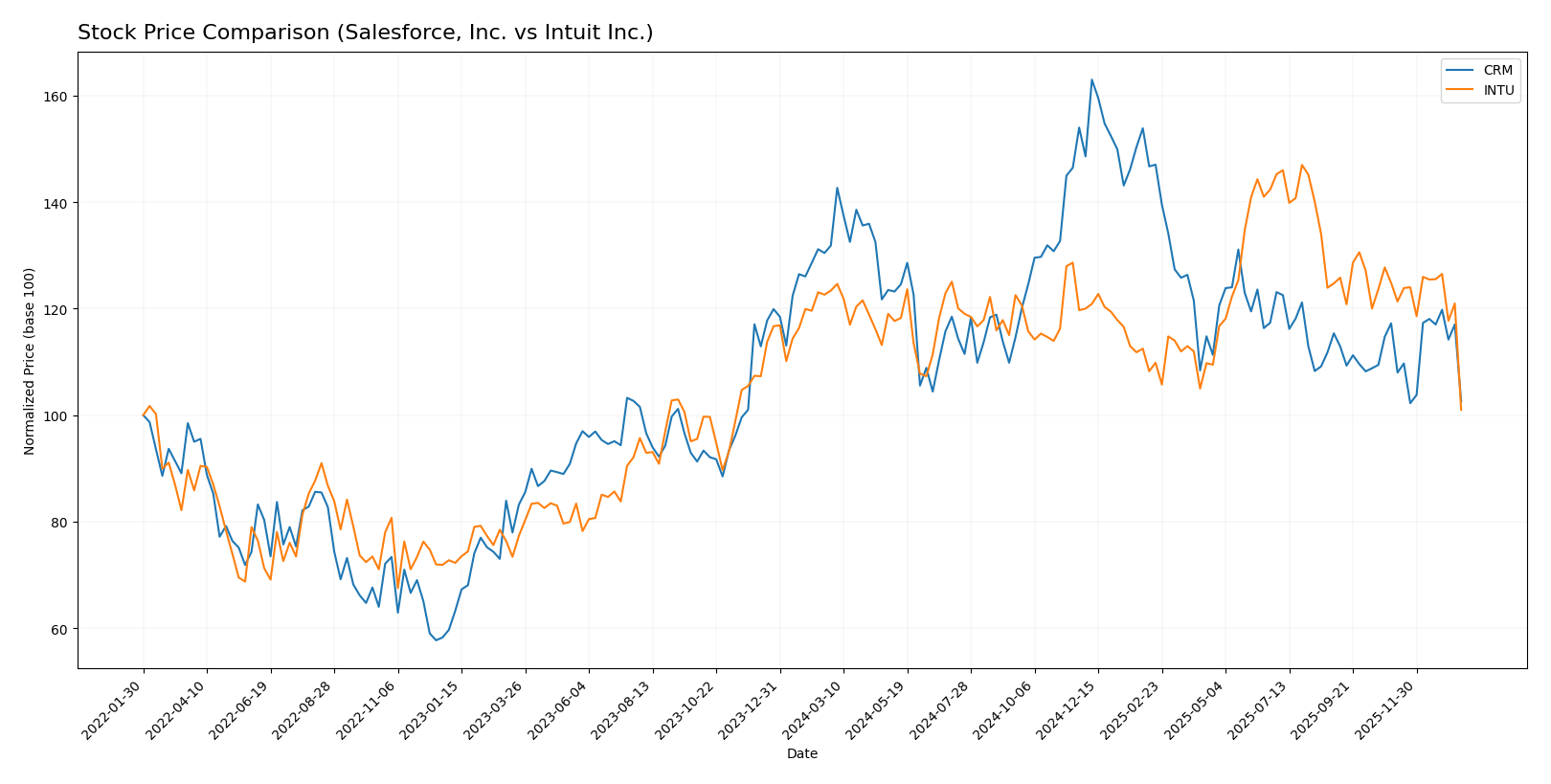

The stock price movements of Salesforce, Inc. (CRM) and Intuit Inc. (INTU) over the past year reveal distinct bearish trends with varying acceleration patterns and trading volumes, highlighting divergent investor sentiment and market dynamics.

Trend Analysis

Salesforce, Inc. (CRM) shows a bearish trend over the past 12 months with a price decline of -22.16%, accompanied by acceleration in this downward movement and moderate volatility (std deviation 31.81). The stock ranged between 361.99 at its peak and 227.11 at its lowest.

Intuit Inc. (INTU) also exhibits a bearish trend with an -18.15% price decrease over the same period, but with deceleration in the downtrend and higher volatility (std deviation 51.62). Its price fluctuated between a high of 785.95 and a low of 540.07.

Comparing both, Salesforce’s stock experienced the larger price drop and an accelerating decline, while Intuit’s trend decelerated despite significant volatility. Overall, Intuit delivered the relatively better market performance over the past year.

Target Prices

Analysts present a bullish consensus for Salesforce, Inc. and Intuit Inc., suggesting significant upside potential.

| Company | Target High | Target Low | Consensus |

|---|---|---|---|

| Salesforce, Inc. | 400 | 250 | 324.17 |

| Intuit Inc. | 880 | 700 | 798.4 |

The consensus target prices for both Salesforce and Intuit are well above their current stock prices of 229.15 and 541.18, respectively, indicating favorable analyst expectations for growth.

Analyst Opinions Comparison

This section compares analysts’ ratings and grades for Salesforce, Inc. and Intuit Inc.:

Rating Comparison

Salesforce, Inc. Rating

- Rating: B+, categorized as Very Favorable by analysts.

- Discounted Cash Flow Score: 4, indicating a Favorable status.

- ROE Score: 4, reflecting Favorable profitability efficiency.

- ROA Score: 4, marked as Favorable for asset utilization.

- Debt To Equity Score: 3, Moderate financial risk level.

- Overall Score: 3, classified as Moderate overall performance.

Intuit Inc. Rating

- Rating: B, also considered Very Favorable.

- Discounted Cash Flow Score: 4, indicating a Favorable status.

- ROE Score: 4, showing Favorable efficiency in generating profit.

- ROA Score: 5, rated Very Favorable, showing superior asset use.

- Debt To Equity Score: 2, indicating a slightly stronger balance sheet.

- Overall Score: 3, also rated Moderate in overall standing.

Which one is the best rated?

Based on the provided data, Salesforce holds a slightly higher overall rating (B+) compared to Intuit (B). Intuit outperforms Salesforce in ROA and Debt To Equity scores, but both have the same overall score and DCF and ROE ratings.

Scores Comparison

The scores comparison between Salesforce, Inc. (CRM) and Intuit Inc. (INTU) is as follows:

CRM Scores

- Altman Z-Score: 5.26, indicating a safe zone from bankruptcy risk.

- Piotroski Score: 7, reflecting strong financial strength.

INTU Scores

- Altman Z-Score: 9.35, indicating a safe zone from bankruptcy risk.

- Piotroski Score: 9, reflecting very strong financial strength.

Which company has the best scores?

Based on the available data, Intuit shows better scores with a higher Altman Z-Score and a superior Piotroski Score compared to Salesforce, indicating stronger financial health and lower bankruptcy risk.

Grades Comparison

Here is a detailed comparison of the latest reliable grades for Salesforce, Inc. and Intuit Inc.:

Salesforce, Inc. Grades

This table summarizes recent grades assigned to Salesforce by major financial institutions:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Barclays | Maintain | Overweight | 2026-01-12 |

| RBC Capital | Maintain | Sector Perform | 2026-01-05 |

| Morgan Stanley | Maintain | Overweight | 2025-12-09 |

| Citigroup | Maintain | Neutral | 2025-12-08 |

| DA Davidson | Maintain | Neutral | 2025-12-05 |

| Citizens | Maintain | Market Outperform | 2025-12-04 |

| Deutsche Bank | Maintain | Buy | 2025-12-04 |

| Wedbush | Maintain | Outperform | 2025-12-04 |

| Northland Capital Markets | Maintain | Market Perform | 2025-12-04 |

| Canaccord Genuity | Maintain | Buy | 2025-12-04 |

Salesforce exhibits predominantly positive grades, with strong endorsements such as Buy, Overweight, and Outperform, reflecting a generally bullish analyst sentiment.

Intuit Inc. Grades

Below is a summary of recent grades provided to Intuit by reputable grading firms:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Wells Fargo | Downgrade | Equal Weight | 2026-01-08 |

| Wells Fargo | Maintain | Overweight | 2025-11-21 |

| RBC Capital | Maintain | Outperform | 2025-11-21 |

| BMO Capital | Maintain | Outperform | 2025-11-21 |

| Evercore ISI Group | Maintain | Outperform | 2025-11-18 |

| RBC Capital | Maintain | Outperform | 2025-09-02 |

| RBC Capital | Maintain | Outperform | 2025-08-22 |

| UBS | Maintain | Neutral | 2025-08-22 |

| Morgan Stanley | Maintain | Overweight | 2025-08-22 |

| Barclays | Maintain | Overweight | 2025-08-22 |

Intuit’s grades are largely positive, with multiple Outperform and Overweight ratings, though a recent downgrade to Equal Weight by Wells Fargo indicates some caution.

Which company has the best grades?

Salesforce holds a greater number of Buy and Outperform ratings, suggesting stronger analyst confidence compared to Intuit, which has several Outperform ratings but also a recent downgrade. This difference could influence investor perceptions of growth potential and risk exposure.

Strengths and Weaknesses

Below is a comparative table outlining the key strengths and weaknesses of Salesforce, Inc. (CRM) and Intuit Inc. (INTU) based on the most recent data available.

| Criterion | Salesforce, Inc. (CRM) | Intuit Inc. (INTU) |

|---|---|---|

| Diversification | Highly diversified product portfolio across CRM, Service Cloud, Integration & Analytics with revenues exceeding $38B in 2025 | Focused on Consumer, Small Business, and Credit Karma segments with $18B+ revenue in 2025; less diversified but specialized |

| Profitability | Net margin at 16.35%, ROIC 7.95% below WACC (9.42%), indicating value destruction but improving profitability | Strong profitability: Net margin 20.55%, ROIC 14.78% well above WACC (9.41%), though ROIC trend is declining |

| Innovation | High investment in cloud platforms and analytics, reflected in strong revenue growth and product expansion | Consistent innovation in financial and tax software, expanding Credit Karma and business solutions segments |

| Global presence | Extensive global footprint with cloud services widely adopted across industries | Growing international presence, primarily focused on U.S. and select markets |

| Market Share | Leading market share in cloud-based CRM solutions with strong brand recognition | Dominant in financial software for small businesses and consumers, competitive in tax preparation software |

Key takeaways: Salesforce shows strong diversification and innovation but faces challenges in value creation despite growing profitability. Intuit offers higher profitability and a favorable financial profile, though its ROIC is declining, warranting cautious monitoring. Both companies have strong market positions in their respective niches.

Risk Analysis

Below is a comparative overview of key risk factors for Salesforce, Inc. (CRM) and Intuit Inc. (INTU) based on the most recent data from 2025-2026.

| Metric | Salesforce, Inc. (CRM) | Intuit Inc. (INTU) |

|---|---|---|

| Market Risk | Beta 1.27, moderate volatility due to tech sector sensitivity | Beta 1.25, similar moderate volatility in tech and financial services |

| Debt level | Debt-to-Equity 0.19, favorable low leverage | Debt-to-Equity 0.34, moderate leverage but manageable |

| Regulatory Risk | Moderate, faces data privacy and software compliance rules | Moderate, subject to financial regulations and tax software compliance |

| Operational Risk | Medium, complexity in integrating multiple platforms like Slack and Tableau | Medium, reliance on cloud services and software updates for tax/finance products |

| Environmental Risk | Low, limited direct environmental impact as a software company | Low, primarily digital services with minimal environmental footprint |

| Geopolitical Risk | Moderate, global customer base exposed to international market fluctuations | Moderate, exposure to North American and international markets with regulatory differences |

Salesforce faces moderate market and operational risks due to its broad enterprise software ecosystem and integration challenges. Intuit’s risks are more concentrated on regulatory and operational compliance, with a strong financial position supported by very high Altman Z-Score (9.35) indicating low bankruptcy risk. Both companies maintain low environmental risks typical of software firms, with manageable debt levels. The most impactful risks remain market volatility and regulatory changes affecting their sectors.

Which Stock to Choose?

Salesforce, Inc. (CRM) shows favorable income growth with an 8.72% revenue increase in 2025 and strong net margin at 16.35%. Its financial ratios are slightly favorable, supported by low debt (D/E 0.19) and a solid interest coverage ratio. However, its ROIC is below WACC, indicating value destruction despite improving profitability. CRM holds a very favorable B+ rating and demonstrates strong financial health with a safe-zone Altman Z-Score of 5.26 and a Piotroski score of 7.

Intuit Inc. (INTU) reports higher income growth at 15.63% revenue increase and superior profitability with a 20.55% net margin. Its financial ratios are favorable overall, with moderate debt (D/E 0.34) and solid interest coverage. INTU’s ROIC exceeds WACC, signaling value creation, though its ROIC trend is declining. The company has a very favorable B rating, an excellent Altman Z-Score of 9.35, and a very strong Piotroski score of 9, reflecting robust financial stability.

Investors prioritizing value creation and strong profitability may find Intuit’s financials and moat evaluation more favorable, whereas those noting improving profitability despite current value destruction might view Salesforce as a potential growth candidate. The choice could depend on whether an investor prefers slightly favorable financial ratios with growth potential or a company with a stronger moat but declining profitability.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Salesforce, Inc. and Intuit Inc. to enhance your investment decisions: