In today’s fast-evolving technology landscape, Okta, Inc. and Informatica Inc. stand out as leaders in software infrastructure, each driving innovation in identity management and data integration. While Okta specializes in secure identity solutions, Informatica focuses on AI-powered data management across cloud environments. Their overlapping markets and cutting-edge strategies make them compelling contenders. Join me as we analyze which company presents the most attractive investment opportunity in 2026.

Table of contents

Companies Overview

I will begin the comparison between Okta and Informatica by providing an overview of these two companies and their main differences.

Okta Overview

Okta, Inc. specializes in identity solutions, serving enterprises, SMBs, universities, non-profits, and governments globally. Its Okta Identity Cloud platform offers a range of security and identity management products, including Single Sign-On, Adaptive Multi-Factor Authentication, and API Access Management. Headquartered in San Francisco, Okta operates in the software infrastructure industry with a market cap of approximately 15.2B USD.

Informatica Overview

Informatica Inc. develops an AI-powered platform to manage and unify data across multi-cloud and hybrid systems at enterprise scale. Its suite includes data integration, API management, data quality, master data management, and governance products designed to support analytics and compliance efforts. Based in Redwood City, Informatica operates in software infrastructure with a market cap near 7.5B USD.

Key similarities and differences

Both Okta and Informatica operate in the software infrastructure sector and serve enterprise clients with technology solutions. Okta focuses on identity and access management, enhancing security through user authentication and lifecycle management. Informatica concentrates on data integration, quality, and governance, providing tools for enterprise data management and compliance. Their business models center on software platforms but address distinct needs within enterprise IT ecosystems.

Income Statement Comparison

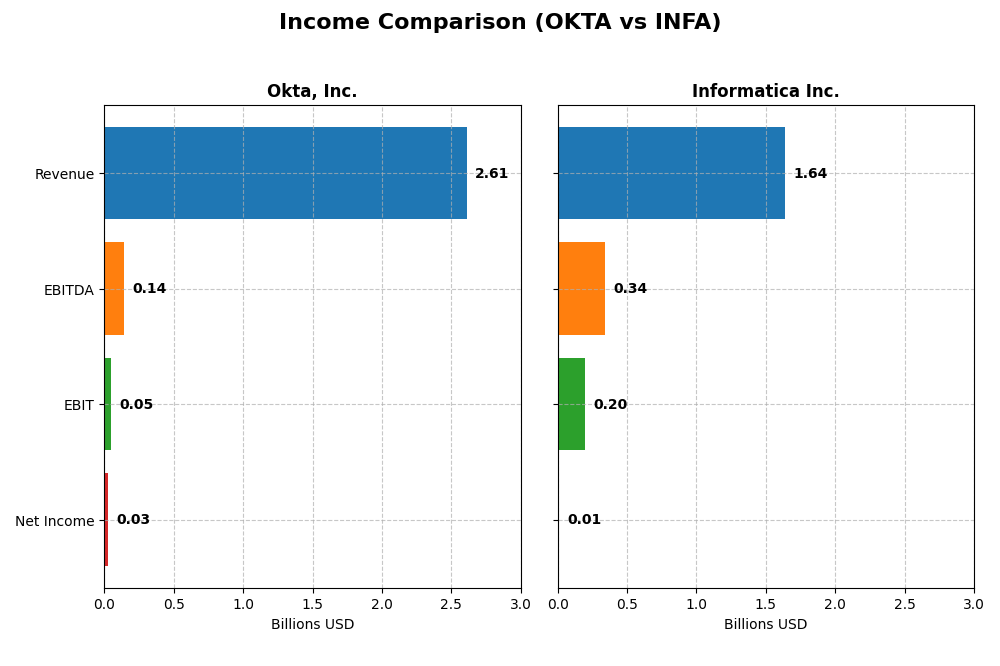

The table below compares the most recent fiscal year income statement metrics for Okta, Inc. and Informatica Inc., providing a snapshot of their financial performance.

| Metric | Okta, Inc. (OKTA) | Informatica Inc. (INFA) |

|---|---|---|

| Market Cap | 15.2B | 7.5B |

| Revenue | 2.61B | 1.64B |

| EBITDA | 139M | 339M |

| EBIT | 51M | 199M |

| Net Income | 28M | 10M |

| EPS | 0.17 | 0.033 |

| Fiscal Year | 2025 | 2024 |

Income Statement Interpretations

Okta, Inc.

Okta demonstrated strong growth in revenue, rising from $835M in 2021 to $2.61B in 2025, with net income improving from a loss of $266M in 2021 to a positive $28M in 2025. Gross margin remained favorable at 76.3%, while net and EBIT margins showed neutral trends. The 2025 fiscal year saw accelerated revenue growth of 15.3% and substantial margin improvements.

Informatica Inc.

Informatica’s revenue increased steadily from $1.32B in 2020 to $1.64B in 2024, with net income recovering from a $168M loss in 2020 to a modest $10M profit in 2024. Gross margin remained strong at 80.1%, complemented by a favorable EBIT margin of 12.2%. However, revenue growth slowed to 2.8% in 2024, despite favorable net margin and EPS improvements.

Which one has the stronger fundamentals?

Okta’s fundamentals reflect rapid revenue and net income growth, with consistently favorable margin expansions and strong recent performance improvements. Informatica shows solid profitability margins but slower revenue growth and a smaller net income base. Both companies have favorable income statement evaluations, yet Okta’s higher growth rates and margin stability suggest relatively stronger fundamentals over the analyzed periods.

Financial Ratios Comparison

The table below presents the most recent key financial ratios for Okta, Inc. and Informatica Inc., offering a straightforward comparison of their fiscal year 2025 and 2024 performances respectively.

| Ratios | Okta, Inc. (2025) | Informatica Inc. (2024) |

|---|---|---|

| ROE | 0.44% | 0.43% |

| ROIC | -0.61% | 0.56% |

| P/E | 570.6 | 787.9 |

| P/B | 2.49 | 3.39 |

| Current Ratio | 1.35 | 1.82 |

| Quick Ratio | 1.35 | 1.82 |

| D/E | 0.15 | 0.81 |

| Debt-to-Assets | 10.1% | 35.2% |

| Interest Coverage | -14.8 | 0.87 |

| Asset Turnover | 0.28 | 0.31 |

| Fixed Asset Turnover | 22.31 | 8.75 |

| Payout Ratio | 0 | 0.12% |

| Dividend Yield | 0 | 0.00015% |

Interpretation of the Ratios

Okta, Inc.

Okta’s financial ratios present a mixed picture, with roughly 43% favorable and 43% unfavorable metrics, resulting in a neutral overall assessment. Strengths include a favorable quick ratio of 1.35, low debt-to-equity of 0.15, and solid interest coverage of 10.2, indicating manageable leverage and liquidity. However, low returns on equity (0.44%) and invested capital (-0.61%) alongside a high price-to-earnings ratio (570.6) raise concerns. Okta does not pay dividends, reflecting either a reinvestment or growth strategy.

Informatica Inc.

No updated financial ratios or key metrics are available for Informatica, preventing a detailed analysis. Consequently, no insights can be provided regarding its profitability, leverage, liquidity, or valuation ratios. Similarly, dividend and shareholder return information is missing, so it is unclear whether the company pays dividends or follows a different capital allocation strategy.

Which one has the best ratios?

Based on the available data, only Okta’s ratios can be evaluated. While Okta shows some favorable liquidity and leverage ratios, its weak profitability and high valuation metrics temper the outlook. Informatica’s lack of accessible financial ratio data precludes a direct comparison, making Okta the only option for ratio-based evaluation at this time.

Strategic Positioning

This section compares the strategic positioning of Okta, Inc. and Informatica Inc. across Market position, Key segments, and Exposure to technological disruption:

Okta, Inc.

- Leading identity solutions provider with moderate competitive pressure in software infrastructure.

- Key segments include subscription-based identity services and technology service revenues.

- Positioned in cloud identity with innovations like passwordless authentication; technology disruption risks exist.

Informatica Inc.

- Data management platform provider with strong focus on enterprise multi-cloud and hybrid environments.

- Diverse data integration, API management, data quality, and governance subscription services.

- Focused on AI-powered data management platform; exposure primarily in evolving data governance and integration tech.

Okta, Inc. vs Informatica Inc. Positioning

Okta concentrates on identity and access management with a subscription-driven model, showing rapid growth in this niche, while Informatica offers a broader data management platform with multiple interoperable products across cloud and hybrid systems. Okta’s specialization may limit diversification compared to Informatica’s varied service suite.

Which has the best competitive advantage?

Based on MOAT evaluation, Okta shows slightly unfavorable positioning due to value destruction despite growing profitability. Informatica’s competitive advantage cannot be assessed due to missing data, precluding a direct comparison of their economic moats.

Stock Comparison

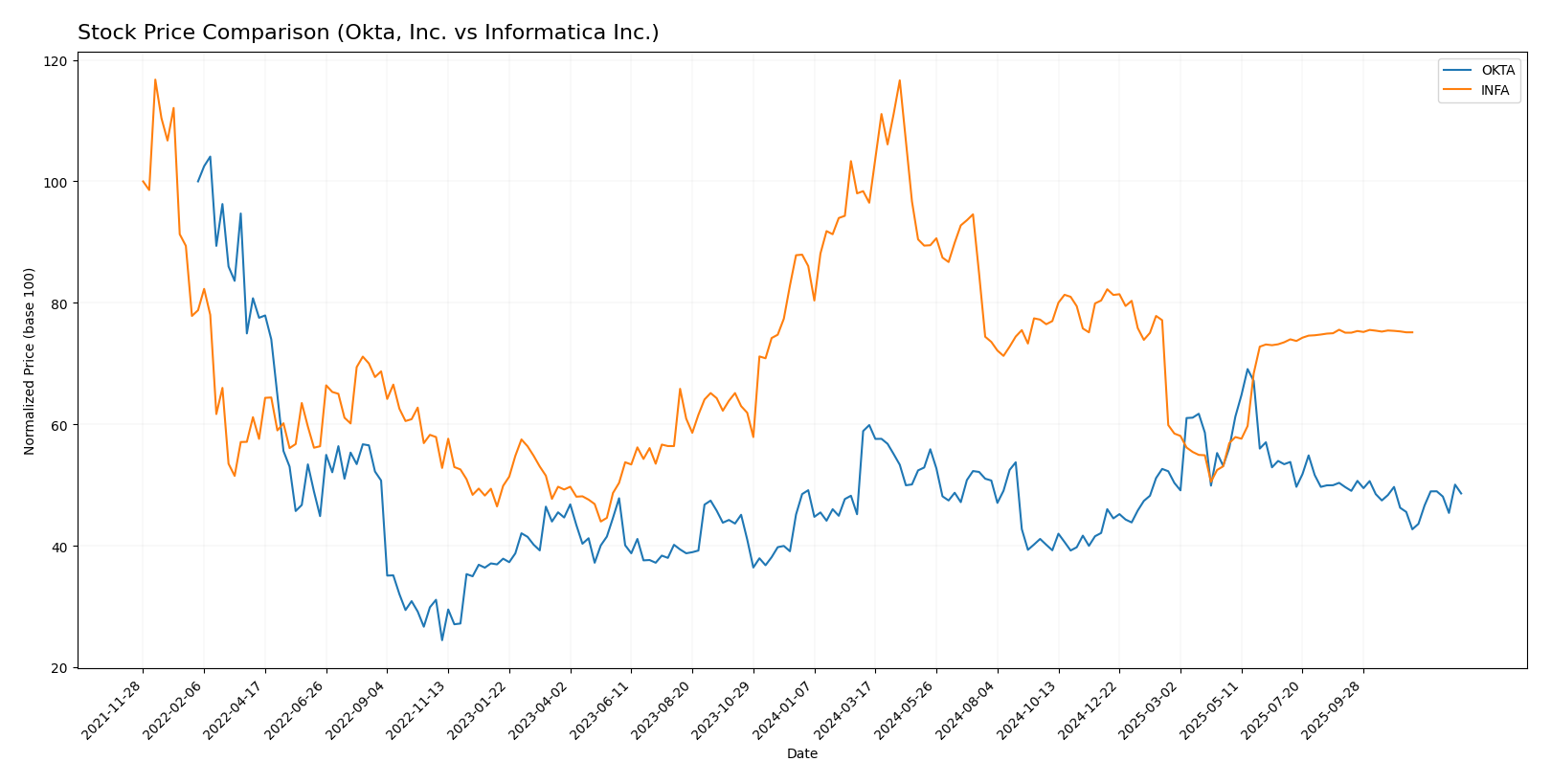

The past year saw Okta, Inc. exhibit a bullish trend with accelerating gains and notable price volatility, while Informatica Inc. faced a bearish trend marked by accelerating declines and lower price fluctuations.

Trend Analysis

Okta, Inc. recorded a 7.58% price increase over the last 12 months, signaling a bullish trend with acceleration and substantial volatility (std dev 11.38). The stock peaked at 127.3 and bottomed at 72.24.

Informatica Inc. showed a 12.68% decline over the same period, reflecting a bearish trend with acceleration and moderate volatility (std dev 4.46). Its highest price was 38.48 and lowest 16.67.

Comparing both, Okta delivered superior market performance with positive growth, while Informatica experienced a pronounced decline during the analyzed year.

Target Prices

The target price consensus from verified analysts shows a positive outlook for both Okta, Inc. and Informatica Inc.

| Company | Target High | Target Low | Consensus |

|---|---|---|---|

| Okta, Inc. | 140 | 60 | 110.67 |

| Informatica Inc. | 27 | 27 | 27 |

Analysts expect Okta’s stock to trade well above its current price of $89.55, suggesting potential upside. Informatica’s target price aligns closely with its current price of $24.79, indicating a stable valuation outlook.

Analyst Opinions Comparison

This section compares analysts’ ratings and grades for Okta, Inc. and Informatica Inc.:

Rating Comparison

Okta, Inc. Rating

- Rating: B, classified as Very Favorable

- Discounted Cash Flow Score: 4, marked as Favorable

- ROE Score: 2, considered Moderate

- ROA Score: 3, considered Moderate

- Debt To Equity Score: 4, marked as Favorable

- Overall Score: 3, considered Moderate

Informatica Inc. Rating

- No rating data available

- No score data available

- No score data available

- No score data available

- No score data available

- No score data available

Which one is the best rated?

Based on the provided data, Okta, Inc. holds a comprehensive rating profile with a “B” rating and favorable scores in discounted cash flow and debt-to-equity metrics. Informatica Inc. lacks any rating or score information, making Okta the better rated by default.

Scores Comparison

This section compares the Altman Z-Score and Piotroski Score of Okta and Informatica to assess their financial health:

Okta Scores

- Altman Z-Score: 4.15; safe zone, indicating low bankruptcy risk.

- Piotroski Score: 8; very strong financial health, suggesting good value.

Informatica Scores

- Altman Z-Score: 1.94; grey zone, indicating moderate bankruptcy risk.

- Piotroski Score: 6; average financial health, suggesting moderate strength.

Which company has the best scores?

Okta has higher Altman Z-Score and Piotroski Score than Informatica, indicating stronger financial health and lower bankruptcy risk based on the provided data.

Grades Comparison

Here is a detailed comparison of the recent grades assigned to Okta, Inc. and Informatica Inc.:

Okta, Inc. Grades

The following table lists recent analyst grades for Okta, Inc. from reputable grading companies.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Stephens & Co. | Upgrade | Overweight | 2026-01-14 |

| Piper Sandler | Maintain | Neutral | 2026-01-05 |

| RBC Capital | Maintain | Outperform | 2026-01-05 |

| Jefferies | Upgrade | Buy | 2025-12-16 |

| Needham | Maintain | Buy | 2025-12-12 |

| BTIG | Maintain | Buy | 2025-12-04 |

| Susquehanna | Maintain | Neutral | 2025-12-03 |

| Cantor Fitzgerald | Maintain | Overweight | 2025-12-03 |

| Canaccord Genuity | Maintain | Buy | 2025-12-03 |

| Scotiabank | Maintain | Sector Perform | 2025-12-03 |

Okta shows a positive trend with multiple upgrades and a consensus rating of “Buy,” reflecting strong analyst confidence.

Informatica Inc. Grades

The following table summarizes recent analyst grades for Informatica Inc. from established grading firms.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Guggenheim | Downgrade | Neutral | 2025-08-07 |

| UBS | Maintain | Neutral | 2025-08-07 |

| Baird | Maintain | Neutral | 2025-05-28 |

| JP Morgan | Downgrade | Neutral | 2025-05-28 |

| RBC Capital | Maintain | Sector Perform | 2025-05-28 |

| Wolfe Research | Downgrade | Peer Perform | 2025-05-28 |

| Wells Fargo | Maintain | Equal Weight | 2025-05-28 |

| Truist Securities | Downgrade | Hold | 2025-05-28 |

| RBC Capital | Maintain | Sector Perform | 2025-05-27 |

| UBS | Maintain | Neutral | 2025-05-16 |

Informatica’s grades show a pattern of downgrades and a consensus rating of “Hold,” indicating cautious analyst sentiment.

Which company has the best grades?

Okta, Inc. has received predominantly positive grades, including multiple “Buy” and “Overweight” ratings, while Informatica Inc. is mostly rated “Neutral” or “Hold,” with several downgrades. This suggests stronger analyst confidence in Okta’s outlook, which may influence investor sentiment towards higher growth or stability expectations.

Strengths and Weaknesses

Below is a comparative overview of key strengths and weaknesses for Okta, Inc. and Informatica Inc., based on their most recent available data.

| Criterion | Okta, Inc. | Informatica Inc. |

|---|---|---|

| Diversification | Low: Revenue mainly from subscription services (2.56B USD in 2025) with minor tech services | Moderate: Mix of subscription and professional services, with over 1.1B USD subscription revenue in 2024 |

| Profitability | Weak: ROIC at -0.61%, net margin 1.07% (unfavorable) | Data unavailable for profitability analysis |

| Innovation | Moderate: High asset turnover (22.31 in fixed assets), indicating efficient use of technology | Data unavailable, but diversified product lines suggest innovation efforts |

| Global presence | Strong: Rapid revenue growth and subscription base suggest expanding global footprint | Likely strong: Established presence with steady subscription and service revenues |

| Market Share | Growing: Subscription revenues up from 796M USD in 2021 to 2.56B USD in 2025 | Stable: Subscription revenue steady over recent years around 1B USD |

Key takeaway: Okta shows rapid growth in subscription revenue and improving profitability trends but still operates at a slight value destruction level. Informatica appears more diversified with steady revenues but lacks detailed profitability data, requiring cautious evaluation.

Risk Analysis

Below is a comparative overview of key risks for Okta, Inc. and Informatica Inc. as of 2025-2026.

| Metric | Okta, Inc. | Informatica Inc. |

|---|---|---|

| Market Risk | Moderate (Beta 0.76, stable tech sector exposure) | Moderate to High (Beta 1.135, more volatile market presence) |

| Debt level | Low (Debt-to-Equity 0.15, favorable) | Unknown (Data unavailable) |

| Regulatory Risk | Moderate (Data privacy and cybersecurity compliance critical) | Moderate (Data governance regulations impact) |

| Operational Risk | Moderate (High reliance on cloud infrastructure) | Moderate (Complex AI platform integration challenges) |

| Environmental Risk | Low (Software sector, limited direct impact) | Low (Software sector, limited direct impact) |

| Geopolitical Risk | Moderate (US-based, international client exposure) | Moderate (US-based, global data regulations affect) |

The most likely and impactful risks involve regulatory compliance and operational challenges. Okta faces pressure from cybersecurity regulations and integration complexity, while Informatica’s risk is elevated by its position in AI data management amid evolving data governance laws. Okta’s low debt and strong financial stability reduce financial risk, unlike Informatica, where financial data gaps increase uncertainty.

Which Stock to Choose?

Okta, Inc. shows a favorable income evolution with strong revenue and profit growth over 2021-2025. Its financial ratios present a mixed picture: profitability metrics like ROE and ROIC are unfavorable, but leverage and liquidity ratios are favorable, and the company has a very favorable B rating. Okta’s debt level is moderate with a net debt to EBITDA of around 3.9, and its Altman Z-Score indicates a safe zone.

Informatica Inc. has a favorable income statement with stable gross and EBIT margins, though its recent revenue growth is modest. The lack of available detailed financial ratios limits a full assessment, but its Altman Z-Score places it in the grey zone, suggesting moderate financial risk. Informatica’s net margin is neutral, and debt appears moderate with a net debt to EBITDA of 2.8.

For investors prioritizing growth and profitability momentum, Okta’s strong income growth and favorable rating might appear more appealing despite some profitability and ROIC weaknesses. Conversely, risk-averse investors who value financial stability and moderate leverage may see Informatica as a more cautious choice given its safer credit risk profile and steadier margins. The final assessment could depend heavily on individual risk tolerance and investment strategy.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Okta, Inc. and Informatica Inc. to enhance your investment decisions: