Home > Comparison > Industrials > PNR vs IEX

The strategic rivalry between Pentair plc and IDEX Corporation defines the trajectory of the industrial machinery sector. Pentair operates as a global water solutions provider focused on filtration and fluid management, while IDEX specializes in applied fluidics and precision technologies across diverse industries. This head-to-head reflects a contest between broad-based industrial solutions and specialized innovation. This analysis aims to identify which company offers a superior risk-adjusted return for portfolio diversification in 2026.

Table of contents

Companies Overview

Pentair plc and IDEX Corporation stand as key players shaping the industrial machinery landscape. Their competitive dynamics reflect broader trends in global fluid and filtration technologies.

Pentair plc: Global Water Solutions Leader

Pentair plc dominates the water solutions market, generating revenue through its Consumer Solutions and Industrial & Flow Technologies segments. It designs and sells residential and commercial pool equipment, water treatment systems, advanced filtration products, and fluid transfer pumps. In 2026, Pentair focuses strategically on expanding integrated water management and sustainable filtration technologies worldwide.

IDEX Corporation: Applied Fluidics and Safety Innovator

IDEX Corporation excels in applied solutions, driven by its Fluid & Metering Technologies, Health & Science Technologies, and Fire & Safety/Diversified Products segments. It manufactures pumps, flow meters, medical devices, and firefighting equipment for diverse industries. The company’s 2026 strategy emphasizes innovation in precision fluidics, life sciences, and safety systems to capture niche market growth.

Strategic Collision: Similarities & Divergences

Both companies compete in fluid handling and industrial machinery but diverge in approach. Pentair prioritizes broad water management and filtration ecosystems, while IDEX targets specialized, high-precision markets including health and safety. Their battleground centers on innovation in fluid technologies and market adaptability. Pentair offers a stable, diversified water portfolio; IDEX provides a sharper focus on technological depth and specialty applications.

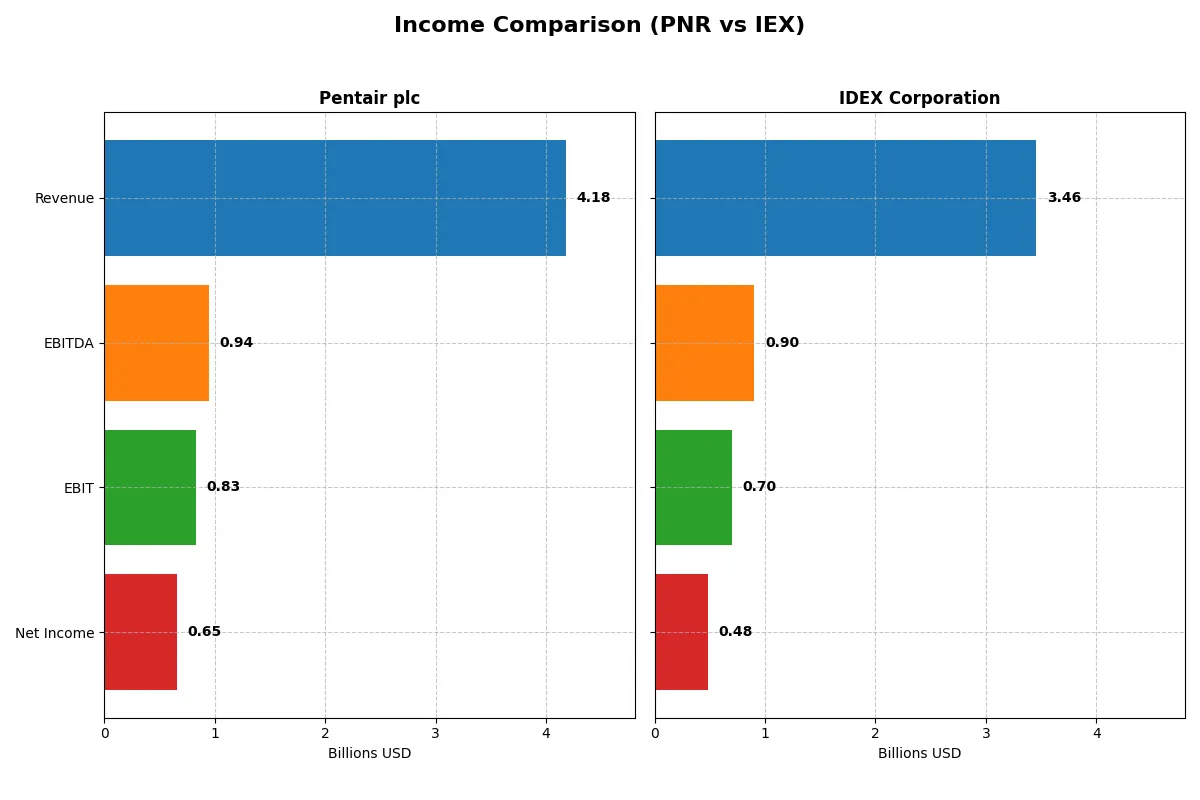

Income Statement Comparison

The following data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Pentair plc (PNR) | IDEX Corporation (IEX) |

|---|---|---|

| Revenue | 4.18B | 3.46B |

| Cost of Revenue | 2.49B | 1.92B |

| Operating Expenses | 833M | 819M |

| Gross Profit | 1.69B | 1.54B |

| EBITDA | 944M | 904M |

| EBIT | 826M | 697M |

| Interest Expense | 69M | 64M |

| Net Income | 654M | 483M |

| EPS | 3.99 | 6.41 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals the true efficiency and profitability of Pentair plc and IDEX Corporation’s corporate engines.

Pentair plc Analysis

Pentair’s revenue shows a steady upward trend, reaching $4.18B in 2025 with net income climbing to $650M. The company sustains healthy margins, boasting a gross margin of 40.5% and a net margin near 15.7%. Its 2025 figures reflect solid operational efficiency and margin expansion, supported by a 5.7% gross profit growth and a favorable 20% EPS growth over five years.

IDEX Corporation Analysis

IDEX’s revenue rises to $3.46B in 2025 with net income at $483M, reflecting moderate growth. It maintains a stronger gross margin at 44.5% but a thinner net margin of 14.0%. Despite a 5.8% revenue increase in 2025, net margin contraction and a 3.5% EPS decline highlight margin pressure. The overall five-year revenue growth of 25% contrasts with a net margin deterioration of 14%.

Margin Discipline vs. Revenue Expansion

Pentair leads in net income growth and margin improvement, showcasing a more efficient and steadily profitable model. IDEX excels in revenue scale and gross margin but suffers from margin compression and EPS setbacks. Investors seeking margin stability may favor Pentair’s disciplined earnings profile over IDEX’s top-line momentum with margin risks.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies analyzed:

| Ratios | Pentair plc (PNR) | IDEX Corporation (IEX) |

|---|---|---|

| ROE | 16.9% | 12.0% |

| ROIC | 12.5% | 8.6% |

| P/E | 26.1 | 27.7 |

| P/B | 4.42 | 3.33 |

| Current Ratio | 1.61 | 2.86 |

| Quick Ratio | 0.95 | 2.02 |

| D/E | 0.42 | 0.00 |

| Debt-to-Assets | 23.9% | 0.01% |

| Interest Coverage | 12.4 | 11.2 |

| Asset Turnover | 0.61 | 0.50 |

| Fixed Asset Turnover | 11.1 | 7.39 |

| Payout ratio | 25.1% | 44.0% |

| Dividend yield | 0.96% | 1.59% |

| Fiscal Year | 2025 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Ratios act as a company’s DNA, uncovering hidden risks and operational strengths that define its investment profile.

Pentair plc

Pentair posts a robust ROE of 16.9% and a net margin of 15.66%, signaling efficient profitability. Its P/E of 26.14 and P/B of 4.42 mark the stock as somewhat expensive. Despite a modest dividend yield of 0.96%, Pentair maintains favorable leverage and liquidity, supporting stable shareholder returns.

IDEX Corporation

IDEX shows a decent net margin of 13.98% but a lower ROE at 12%, reflecting moderate efficiency. The P/E ratio at 27.73 suggests the stock is stretched in valuation. IDEX’s strong liquidity and zero debt profile enhance financial safety, while a 1.59% dividend yield offers modest income to investors.

Premium Valuation vs. Operational Safety

Pentair delivers higher profitability with efficient capital use but trades at a premium valuation. IDEX balances slightly favorable ratios with stronger liquidity and zero leverage. Investors seeking growth with operational efficiency may prefer Pentair; those prioritizing financial safety and income might lean towards IDEX.

Which one offers the Superior Shareholder Reward?

I compare Pentair plc (PNR) and IDEX Corporation (IEX) on dividends, payout ratios, and buybacks. Pentair yields ~0.96% with a conservative 25% payout ratio, supported by strong free cash flow coverage (~3.5x). Its buyback program is moderate but steady. IDEX offers a higher dividend yield (~1.59%) with a 44% payout ratio, indicating more aggressive income distribution. Both sustain buybacks, but IEX’s cash ratio (~1.0) and operating cash flow ratio (>1.1) signal ample liquidity to support these returns. Pentair’s lower payout and robust free cash flow coverage suggest a more sustainable model amid market cycles. I conclude IDEX offers higher immediate yield and buybacks, but Pentair provides a safer, long-term shareholder reward in 2026.

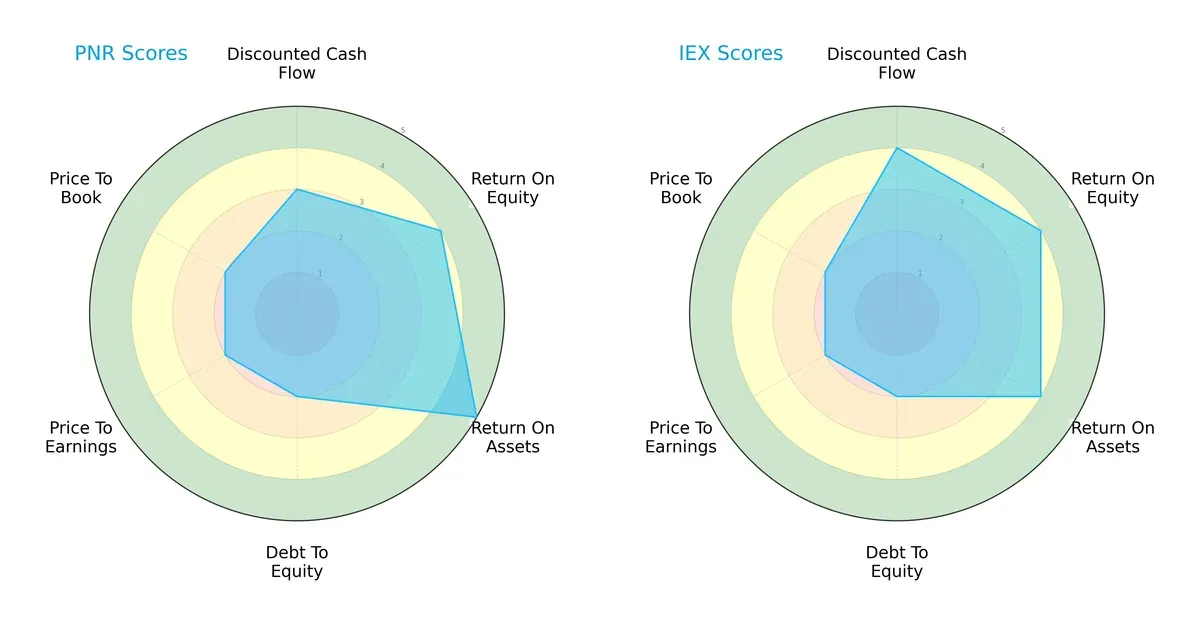

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Pentair plc and IDEX Corporation, highlighting their core financial strengths and weaknesses:

IEX leads with a stronger Discounted Cash Flow score (4 vs. 3) and a slightly lower Return on Assets (4 vs. 5) compared to Pentair. Both share an equal Return on Equity score (4). Pentair excels in asset efficiency but lags in debt management and valuation metrics, scoring 2 across Debt/Equity, P/E, and P/B ratios. IEX also shows weakness in leverage and valuation, matching Pentair’s low scores. Overall, IEX presents a more balanced profile, leveraging cash flow strength, while Pentair relies heavily on asset utilization.

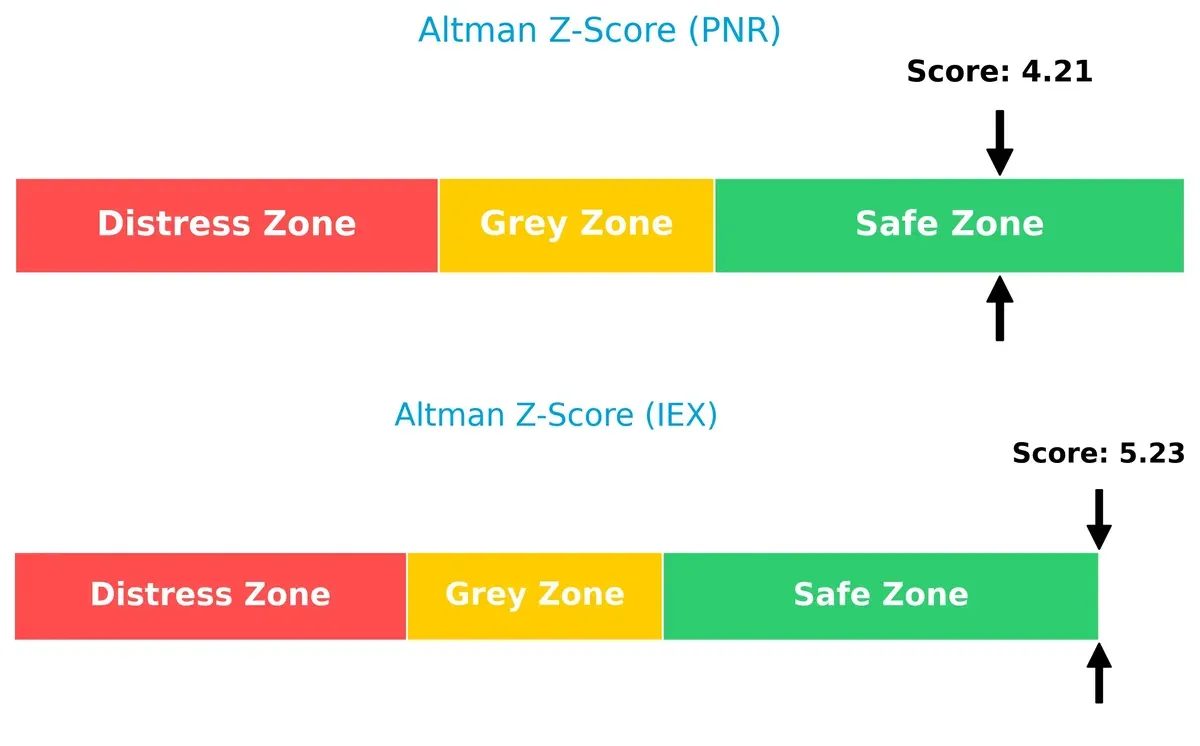

Bankruptcy Risk: Solvency Showdown

Pentair’s Altman Z-Score stands at 4.21, while IDEX scores higher at 5.23; both reside safely above the distress threshold. This spread favors IDEX’s stronger buffer against financial distress in this late-cycle environment:

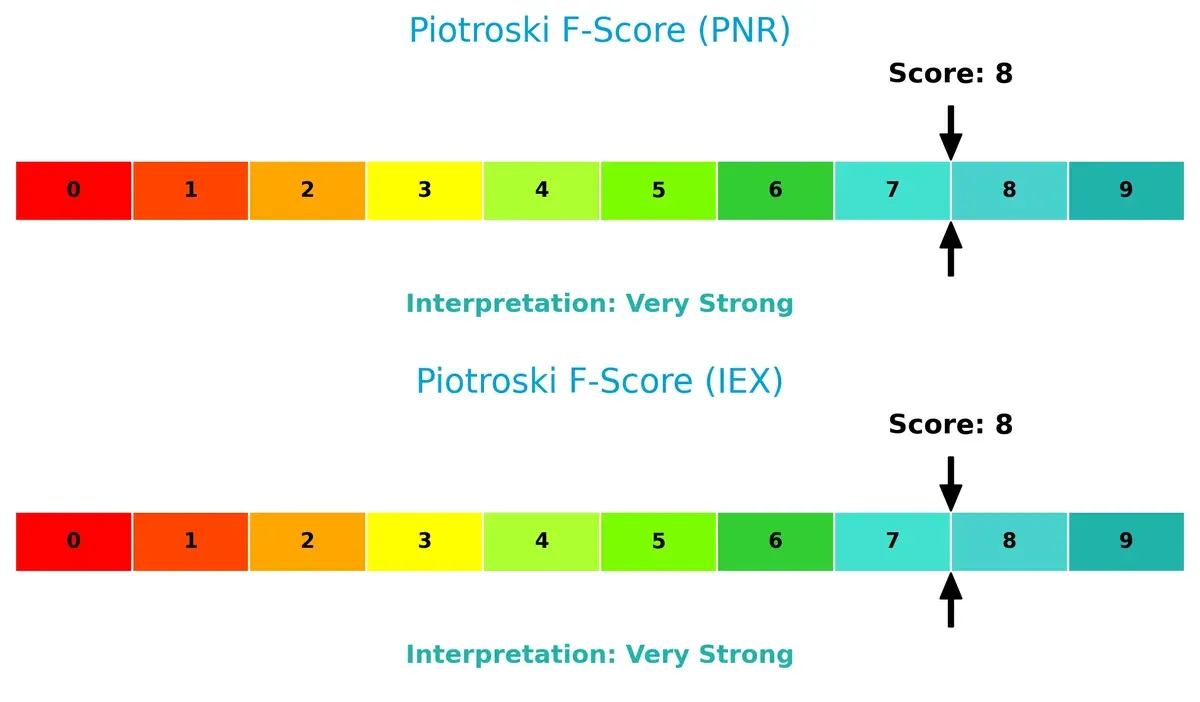

Financial Health: Quality of Operations

Pentair and IDEX both score an impressive 8 on the Piotroski F-Score, signaling very strong internal financial health. Neither shows immediate red flags in profitability, leverage, or liquidity metrics:

How are the two companies positioned?

This section dissects Pentair and IDEX’s operational DNA by comparing their revenue distribution and internal dynamics. The goal is to confront their economic moats and identify which model delivers the most resilient, sustainable competitive advantage today.

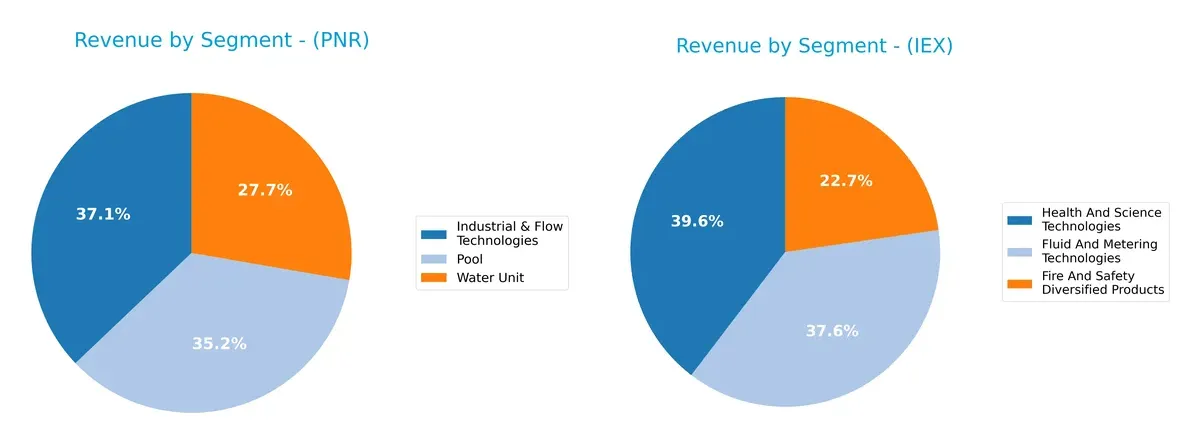

Revenue Segmentation: The Strategic Mix

The following visual comparison dissects how Pentair plc and IDEX Corporation diversify their income streams and where their primary sector bets lie:

Pentair’s 2024 revenue leans on three substantial segments: Industrial & Flow Technologies at $1.51B, Pool at $1.44B, and Water Unit at $1.13B, displaying a balanced but slightly concentrated mix. IDEX pivots around Health and Science Technologies ($1.30B) and Fluid and Metering Technologies ($1.23B), with Fire and Safety products trailing at $744M, showcasing a more diversified portfolio. Pentair’s focus anchors on water and industrial infrastructure, which may imply sector-specific risks, while IDEX’s spread across safety, health, and fluid systems suggests stronger ecosystem lock-in.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Pentair plc and IDEX Corporation:

Pentair plc Strengths

- Diverse revenue streams across Industrial, Pool, and Water units

- Strong profitability with 15.66% net margin

- Favorable ROE at 16.9% and ROIC above WACC

- Solid current ratio of 1.61 and low debt-to-assets at 23.86%

- High fixed asset turnover indicating efficient asset use

IDEX Corporation Strengths

- Diversified product segments including Health, Fire Safety, and Fluid Technologies

- Favorable net margin at 13.98% with neutral ROE and ROIC

- Excellent liquidity shown by current ratio of 2.86 and zero debt ratio

- Robust interest coverage at 10.82 supports debt serviceability

- Consistent revenue growth in key segments like Health and Science

Pentair plc Weaknesses

- Unfavorable valuation multiples: high P/E at 26.14 and P/B at 4.42

- Dividend yield under 1% may deter income-focused investors

- Quick ratio just below 1 signals potential liquidity risk

- Asset turnover is neutral, suggesting room for operational improvement

IDEX Corporation Weaknesses

- High P/E ratio of 27.73 and unfavorable P/B of 3.33

- Asset turnover at 0.5 is weak, indicating less efficient asset deployment

- Dividend yield remains neutral, limiting income appeal

- ROE and ROIC are neutral, showing moderate capital efficiency

Both companies demonstrate commendable diversification and profitability metrics. Pentair shows stronger capital returns and asset efficiency, but faces valuation and liquidity concerns. IDEX maintains excellent liquidity with minimal debt but struggles with asset utilization and valuation. These factors should influence strategic priorities around operational efficiency and capital allocation.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat shields long-term profits from relentless competition and market pressures. Here is how Pentair and IDEX defend their turf:

Pentair plc: Durable Intangible Assets and Brand Equity

Pentair leverages strong brand recognition and proprietary water solutions technology. Its steady 15.7% net margin and 3.5% ROIC premium over WACC confirm value creation. Yet, a declining ROIC trend warns to watch profitability in 2026 amid rising global competition.

IDEX Corporation: Operational Complexity and Diversified Solutions

IDEX’s moat rests on complex, diversified industrial technologies across fluidics and safety sectors. Despite higher gross margins (44.5%), it currently fails to create value, with ROIC below WACC and a steep profitability decline. Expansion into health and science could reverse this trend.

Pentair’s Brand Strength vs. IDEX’s Diversified Complexity

Pentair boasts a deeper moat, consistently generating value despite margin pressures. IDEX’s declining ROIC signals a fragile moat vulnerable to disruption. Pentair is better positioned to defend market share in this cycle.

Which stock offers better returns?

The past year reveals contrasting stock price trajectories: Pentair plc (PNR) shows a strong overall gain with recent weakness, while IDEX Corporation (IEX) endures a yearly loss but rebounds sharply in the last quarter.

Trend Comparison

Pentair plc’s stock rose 16.42% over the past 12 months, marking a bullish trend despite recent deceleration and a 7.14% decline in the last 2.5 months.

IDEX Corporation’s stock dropped 13.18% over the full year, indicating a bearish trend, but the recent 21.74% gain signals strong accelerating recovery since November 2025.

Comparing trends, Pentair delivered the highest annual market performance, although IDEX’s recent surge points to potential momentum going forward.

Target Prices

Analysts maintain a bullish outlook with solid upside potential for both Pentair plc and IDEX Corporation.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Pentair plc | 90 | 135 | 118.56 |

| IDEX Corporation | 220 | 247 | 236.2 |

The consensus target prices suggest 21% upside for Pentair from its current 97.71 USD and 11% upside for IDEX from 211.74 USD. This reflects confidence in their industrial machinery segments despite cyclical risks.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Pentair plc Grades

The following table summarizes recent grades issued by major financial institutions for Pentair plc.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Citigroup | Maintain | Buy | 2026-02-04 |

| Oppenheimer | Maintain | Outperform | 2026-02-04 |

| JP Morgan | Maintain | Overweight | 2026-01-16 |

| Citigroup | Maintain | Buy | 2026-01-12 |

| BNP Paribas Exane | Downgrade | Underperform | 2026-01-07 |

| TD Cowen | Downgrade | Sell | 2026-01-05 |

| Jefferies | Upgrade | Buy | 2025-12-10 |

| Barclays | Downgrade | Equal Weight | 2025-12-04 |

| Oppenheimer | Maintain | Outperform | 2025-11-20 |

| UBS | Maintain | Buy | 2025-10-22 |

IDEX Corporation Grades

The following table summarizes recent grades issued by major financial institutions for IDEX Corporation.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Argus Research | Upgrade | Buy | 2026-02-06 |

| TD Cowen | Maintain | Buy | 2026-02-05 |

| Citigroup | Maintain | Buy | 2026-02-05 |

| DA Davidson | Maintain | Neutral | 2026-02-05 |

| RBC Capital | Maintain | Outperform | 2026-02-05 |

| Stifel | Maintain | Buy | 2026-01-23 |

| Citigroup | Maintain | Buy | 2025-12-08 |

| RBC Capital | Maintain | Outperform | 2025-10-30 |

| Stifel | Maintain | Buy | 2025-10-20 |

| Oppenheimer | Maintain | Outperform | 2025-10-07 |

Which company has the best grades?

IDEX Corporation consistently receives Buy and Outperform ratings without downgrades. Pentair shows mixed grades, including downgrades to Sell and Underperform. This contrast suggests IDEX holds stronger analyst confidence, potentially impacting investor sentiment positively.

Risks specific to each company

The following categories identify critical pressure points and systemic threats facing Pentair plc and IDEX Corporation in the 2026 market environment:

1. Market & Competition

Pentair plc

- Faces intense competition in water solutions and industrial machinery, requiring continuous innovation to maintain market share.

IDEX Corporation

- Competes across diverse segments, needing to balance innovation and specialization to defend its niche markets.

2. Capital Structure & Debt

Pentair plc

- Maintains moderate leverage (D/E 0.42), manageable interest coverage (11.9x), indicating balanced financial risk.

IDEX Corporation

- Virtually no debt (D/E 0.0), strong liquidity; this conservative structure reduces financial risk markedly.

3. Stock Volatility

Pentair plc

- Beta at 1.22 suggests above-market volatility, increasing risk during economic downturns.

IDEX Corporation

- Beta near 0.98 indicates stock moves in line with market, implying moderate volatility risk.

4. Regulatory & Legal

Pentair plc

- Exposure to global water and industrial regulations; regulatory changes could impact compliance costs.

IDEX Corporation

- Faces regulatory scrutiny in health, safety, and environmental standards across multiple industries.

5. Supply Chain & Operations

Pentair plc

- Global supply chain exposes it to disruptions, especially in raw materials for water treatment equipment.

IDEX Corporation

- Diverse product lines increase operational complexity, with risks of bottlenecks and supplier dependencies.

6. ESG & Climate Transition

Pentair plc

- Water sustainability focus aligns with ESG trends but requires continuous investment to meet evolving standards.

IDEX Corporation

- ESG risks present in manufacturing and chemical handling; transition to greener operations is capital intensive.

7. Geopolitical Exposure

Pentair plc

- UK headquartered but global operations expose it to currency and trade tensions.

IDEX Corporation

- US-based with global footprint; geopolitical shifts in trade policy may affect international sales and supply.

Which company shows a better risk-adjusted profile?

Pentair’s primary risk stems from higher stock volatility and competitive pressure in a cyclical sector. IDEX’s greatest risk lies in operational complexity across diverse segments. However, IDEX’s pristine balance sheet and lower volatility underpin a superior risk-adjusted profile. I note Pentair’s beta above 1.2 signals heightened sensitivity to market swings, justifying caution despite solid profitability metrics.

Final Verdict: Which stock to choose?

Pentair plc’s superpower lies in its ability to generate strong returns on invested capital well above its cost of capital. This cash-efficient operator sustains value creation despite a recent dip in profitability. Its moderate leverage and stable income profile make it suited for investors targeting steady, long-term growth with some tolerance for cyclical shifts.

IDEX Corporation’s moat centers on a robust balance sheet with near-zero debt and excellent liquidity, providing a cushion against volatility. Its recurring revenue streams from specialized industrial solutions underpin stable cash flow. Compared to Pentair, IDEX offers a safer harbor for conservative portfolios seeking consistent income and capital preservation.

If you prioritize disciplined capital efficiency and value creation, Pentair outshines as the compelling choice due to its superior ROIC and favorable income growth. However, if you seek stability and lower financial risk in uncertain markets, IDEX offers better resilience and balance sheet strength. Both carry risks, but their profiles cater to distinct investor strategies.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Pentair plc and IDEX Corporation to enhance your investment decisions: