Home > Comparison > Financial Services > MS vs HUT

The strategic rivalry between Morgan Stanley and Hut 8 Corp. shapes the evolving landscape of financial services. Morgan Stanley operates as a diversified financial powerhouse, offering capital markets, wealth, and investment management. In contrast, Hut 8 Corp. focuses on energy-intensive cryptocurrency mining and data center operations. This analysis pits traditional finance against tech-driven innovation to reveal which trajectory delivers superior risk-adjusted returns for a balanced investment portfolio.

Table of contents

Companies Overview

Morgan Stanley and Hut 8 Corp. stand as pivotal players within the financial capital markets, each commanding unique market niches.

Morgan Stanley: Global Financial Powerhouse

Morgan Stanley leads as a diversified financial holding company. It generates revenue through Institutional Securities, Wealth Management, and Investment Management. In 2026, its strategic focus centers on expanding advisory services and enhancing wealth management platforms to capture evolving client needs globally.

Hut 8 Corp.: Bitcoin Mining Innovator

Hut 8 Corp. operates as a vertically integrated Bitcoin mining and energy infrastructure firm. Its core revenue derives from managing large-scale data centers powering Bitcoin mining and AI workloads. The company’s 2026 strategy emphasizes scaling compute capacity while optimizing energy efficiency amid fluctuating crypto markets.

Strategic Collision: Similarities & Divergences

Morgan Stanley pursues a broad financial services model, contrasting with Hut 8’s niche in crypto and energy infrastructure. Their primary battleground is capital markets exposure—Morgan Stanley through advisory and wealth platforms, Hut 8 through crypto asset generation. These distinct profiles offer investors contrasting risk and growth dynamics within financial services.

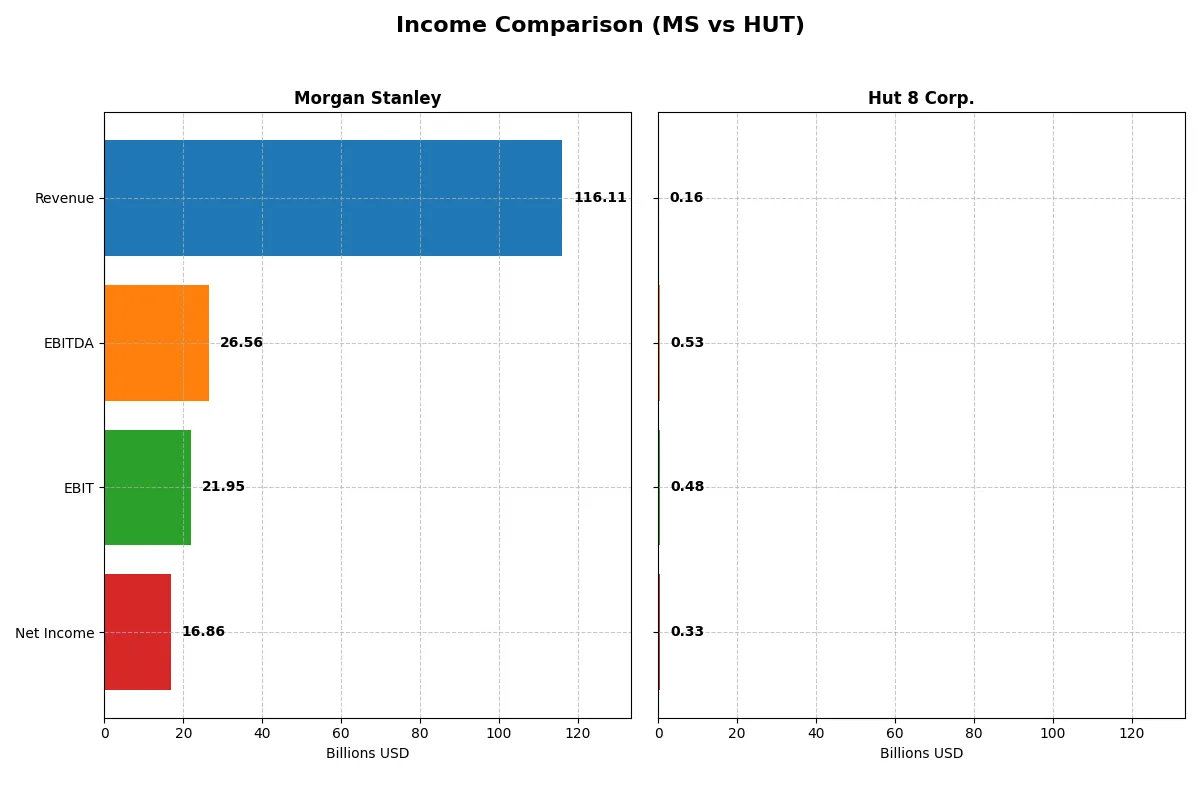

Income Statement Comparison

The following data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Morgan Stanley (MS) | Hut 8 Corp. (HUT) |

|---|---|---|

| Revenue | 116.1B | 162M |

| Cost of Revenue | 49.4B | 87M |

| Operating Expenses | 44.8B | -385M |

| Gross Profit | 66.7B | 76M |

| EBITDA | 26.6B | 529M |

| EBIT | 21.9B | 482M |

| Interest Expense | 49B | 30M |

| Net Income | 16.9B | 332M |

| EPS | 10.34 | 3.71 |

| Fiscal Year | 2025 | 2024 |

Income Statement Analysis: The Bottom-Line Duel

The income statement comparison reveals the true efficiency and profitability of each company’s business engine over recent years.

Morgan Stanley Analysis

Morgan Stanley’s revenue soared from $57.8B in 2021 to $116.1B in 2025, nearly doubling over five years. Net income rose steadily to $16.2B in 2025. The firm maintains robust gross margins around 57%, while net margins improved to 14.5%. Strong momentum in 2025 shows efficiency gains despite a high interest expense ratio of 42%.

Hut 8 Corp. Analysis

Hut 8’s revenue expanded from $40.7M in 2020 to $162M in 2024, a rapid growth trajectory. Net income turned positive in 2023 and surged to $332M by 2024. Gross margin stands at 46.6%, while net margin impressively exceeds 200% due to significant cost and expense reductions. The company exhibits accelerating profitability and operational leverage in the latest year.

Verdict: Scale and Stability vs. Rapid Growth and Volatility

Morgan Stanley commands scale and consistent profitability with stable margins and rising net income, anchoring its financial strength. Hut 8 delivers explosive revenue and profit growth but with more volatility and smaller absolute size. For investors, Morgan Stanley offers dependable earnings power, while Hut 8 presents a high-growth, higher-risk profile.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Morgan Stanley (MS) | Hut 8 Corp. (HUT) |

|---|---|---|

| ROE | 12.8% (2024) | 34.0% (2024) |

| ROIC | 2.5% (2024) | 24.0% (2024) |

| P/E | 14.9 (2024) | 5.6 (2024) |

| P/B | 1.91 (2024) | 1.92 (2024) |

| Current Ratio | 0.66 (2024) | 1.67 (2024) |

| Quick Ratio | 0.66 (2024) | 1.67 (2024) |

| D/E | 3.45 (2024) | 0.35 (2024) |

| Debt-to-Assets | 29.7% (2024) | 22.8% (2024) |

| Interest Coverage | 0.39 (2024) | 15.5 (2024) |

| Asset Turnover | 0.085 (2024) | 0.107 (2024) |

| Fixed Asset Turnover | 4,485 (2024) | 0.67 (2024) |

| Payout Ratio | 46% (2024) | 0% (2024) |

| Dividend Yield | 3.07% (2024) | 0% (2024) |

| Fiscal Year | 2024 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as a company’s DNA, unveiling hidden risks and operational excellence through precise, quantifiable metrics.

Morgan Stanley

Morgan Stanley shows moderate valuation with a P/E of 16.54, indicating a neutral stock price level relative to earnings. Its net margin of 14.52% is favorable, but ROE and ROIC are missing or unfavorable, suggesting profitability challenges. The company rewards shareholders with a 2.17% dividend yield, emphasizing income over reinvestment.

Hut 8 Corp.

Hut 8 impresses with a strong ROE of 33.98% and an extraordinary net margin of 204.38%, signaling high operational efficiency. The stock is attractively valued with a P/E of 5.64, reflecting a favorable price. However, it pays no dividends, likely reinvesting aggressively for growth in a capital-intensive sector.

Operational Efficiency vs. Valuation Appeal

Hut 8 offers a compelling blend of high profitability and attractive valuation, though it lacks shareholder payouts. Morgan Stanley provides steady income through dividends but faces challenges in return metrics. Investors seeking growth may prefer Hut 8’s profile, while income-focused investors might lean toward Morgan Stanley’s steadier returns.

Which one offers the Superior Shareholder Reward?

Morgan Stanley (MS) offers a superior shareholder reward compared to Hut 8 Corp. (HUT) in 2026. MS pays a solid 3.07% dividend yield with a reasonable 46% payout ratio, supported by stable free cash flow and consistent buybacks enhancing total returns. Conversely, HUT pays no dividends and posts negative free cash flow, relying solely on reinvestment and growth. MS’s balanced distribution and buyback strategy deliver a more sustainable, attractive return profile, while HUT’s lack of shareholder distributions and volatile cash flows raise risk for income-focused investors.

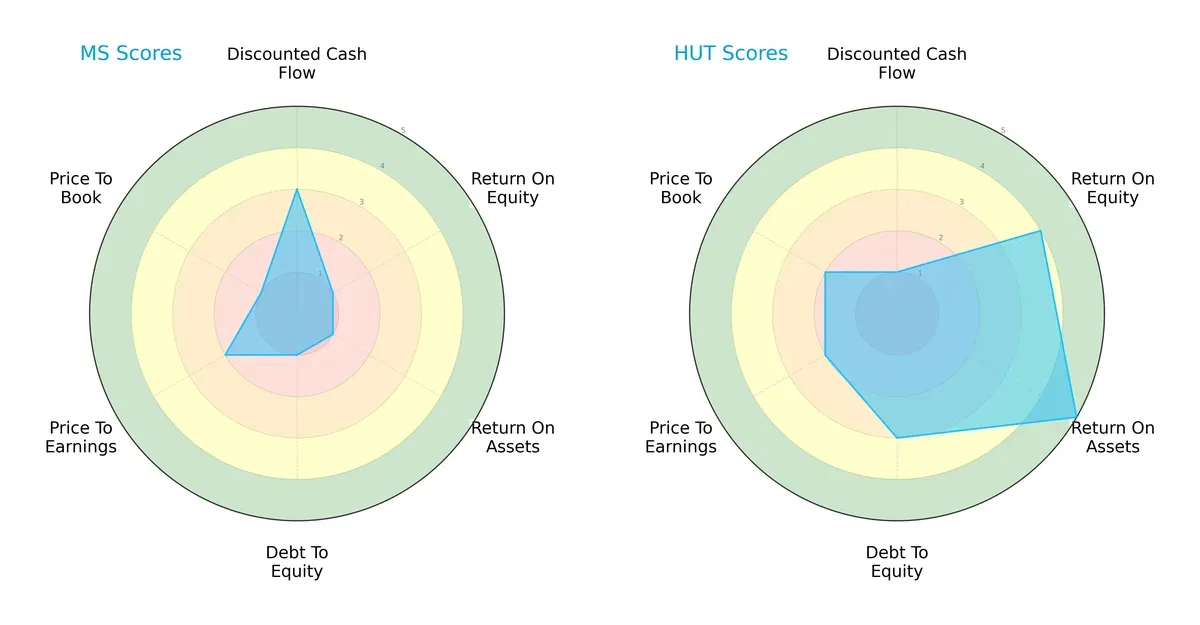

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Morgan Stanley and Hut 8 Corp., highlighting their distinct financial strengths and vulnerabilities:

Morgan Stanley shows moderate strength in discounted cash flow but scores very low on return on equity, return on assets, and debt-to-equity, indicating operational and financial risk. Hut 8 Corp. excels in return on equity and assets, with moderate debt management, but its cash flow score is weak. Hut 8 presents a more balanced profile, relying on operational efficiency, while Morgan Stanley struggles with leverage and profitability metrics.

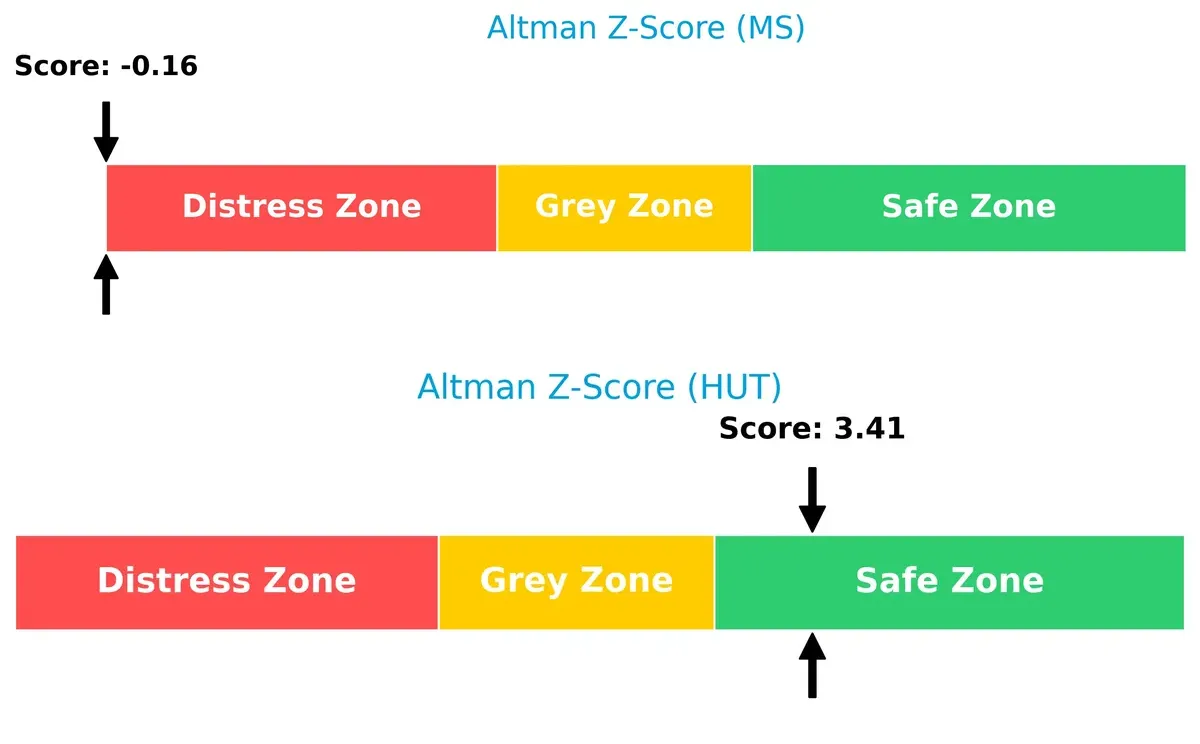

Bankruptcy Risk: Solvency Showdown

Morgan Stanley’s Altman Z-Score falls in the distress zone, signaling high bankruptcy risk, whereas Hut 8 Corp. sits comfortably in the safe zone, implying stronger long-term survival prospects in this cycle:

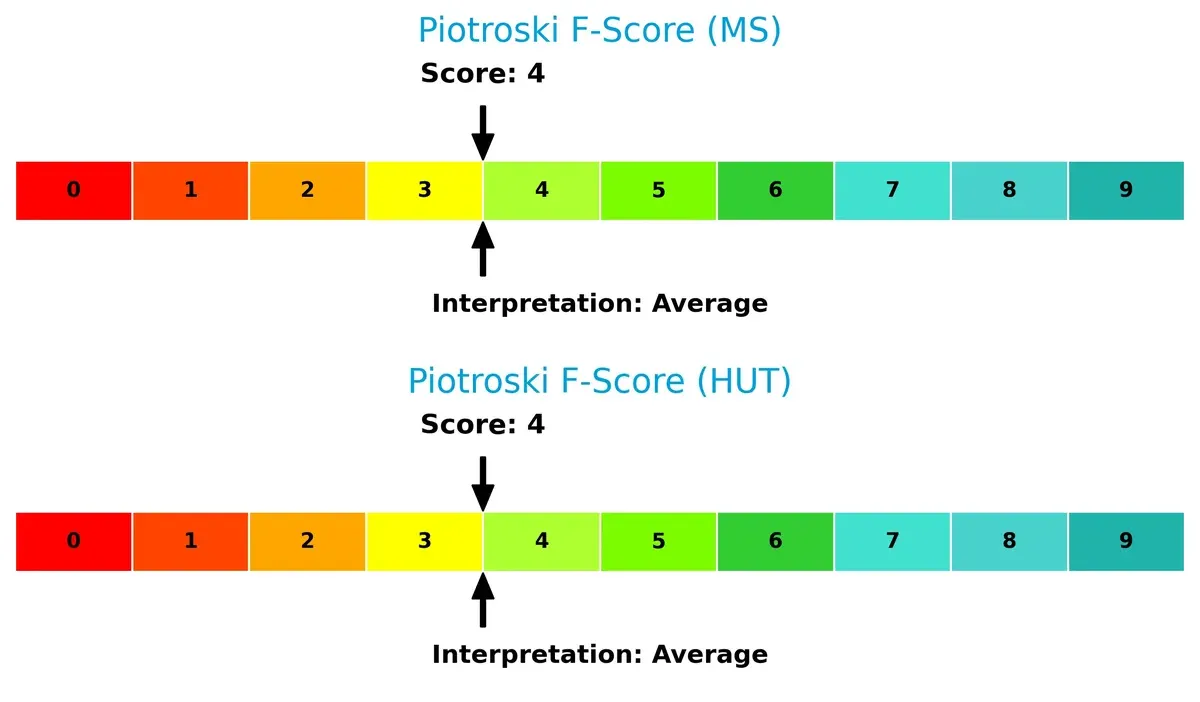

Financial Health: Quality of Operations

Both companies hold an average Piotroski F-Score of 4, indicating moderate financial health. Neither firm currently shows robust internal metrics, but neither displays acute red flags compared to the other:

How are the two companies positioned?

This section dissects the operational DNA of Morgan Stanley and Hut 8 Corp. by comparing their revenue distribution and internal strengths and weaknesses. The goal is to confront their economic moats and identify which model delivers the most resilient, sustainable competitive advantage today.

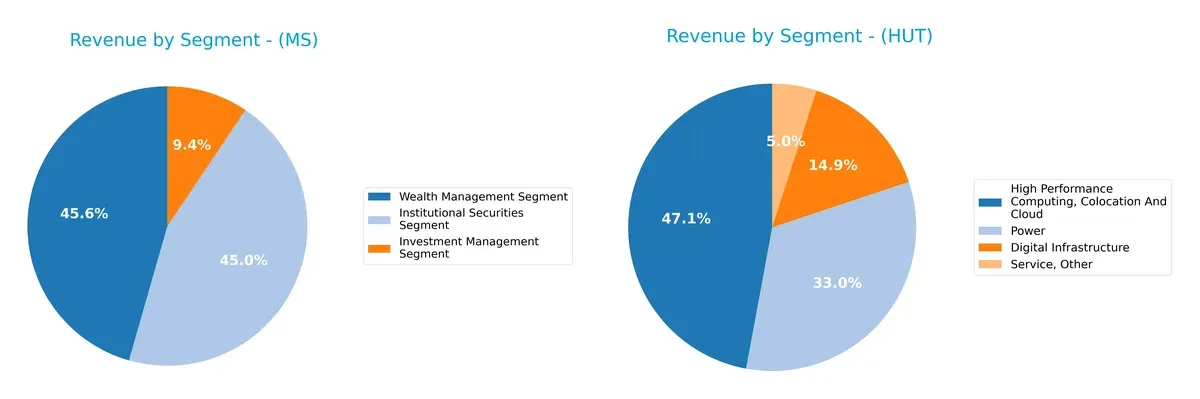

Revenue Segmentation: The Strategic Mix

The following visual comparison dissects how Morgan Stanley and Hut 8 Corp. diversify their income streams and where their primary sector bets lie:

Morgan Stanley anchors its revenue in three robust segments: Wealth Management at $28.4B, Institutional Securities at $28.1B, and Investment Management at $5.9B. This balanced mix diversifies risk across client advisory, trading, and asset management. Hut 8, however, pivots primarily on High Performance Computing, Colocation, and Cloud with $80.7M, complemented by Digital Infrastructure and Power. Hut 8’s concentration in digital mining infrastructure signals niche dominance but exposes it to sector volatility.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Morgan Stanley and Hut 8 Corp:

Morgan Stanley Strengths

- Diversified revenue across Institutional Securities, Wealth Management, and Investment Management

- Strong global presence in Americas, Asia, and EMEA

- Favorable net margin of 14.52%

- Favorable dividend yield at 2.17%

- Low debt-to-assets ratio supports financial stability

Hut 8 Corp. Strengths

- High net margin and ROE indicating strong profitability

- Favorable current and quick ratios reflecting liquidity

- Low debt-to-assets ratio and strong interest coverage

- Favorable P/E ratio suggesting undervaluation

- Revenue diversity in digital infrastructure and HPC segments

Morgan Stanley Weaknesses

- Unfavorable ROE and ROIC raise concerns on capital efficiency

- Unavailable WACC limits cost of capital assessment

- Weak liquidity ratios (current and quick) pose short-term risk

- Low interest coverage ratio indicates potential debt servicing issues

- Unfavorable asset turnover metrics imply low operational efficiency

Hut 8 Corp. Weaknesses

- Unfavorable ROIC and high WACC suggest capital cost challenges

- Unfavorable asset and fixed asset turnover indicate low efficiency

- Absence of dividend yield reduces income appeal

- Geographic revenue concentrated mainly in Canada and US limits global reach

Morgan Stanley’s broad diversification and stable dividend contrast with liquidity and efficiency concerns. Hut 8 shows strong profitability but faces challenges in capital efficiency and geographic concentration. Both companies’ profiles imply distinct strategic priorities in balancing growth and financial discipline.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only barrier that protects long-term profits from relentless competitive erosion. Let’s dissect how Morgan Stanley and Hut 8 Corp. defend their turf:

Morgan Stanley: Diversified Financial Services Moat

Morgan Stanley’s moat stems from its intangible assets and broad client relationships. It shows stable margins and robust revenue growth near 13% in 2025. However, its declining ROIC signals mounting pressure on capital efficiency in 2026.

Hut 8 Corp.: Vertical Integration and Scale Advantage

Hut 8’s moat lies in its cost advantage through vertical integration in Bitcoin mining. It displays explosive revenue growth of 69% and a rapidly rising ROIC, though still below WACC. This suggests improving but fragile profitability amid volatile crypto markets.

Verdict: Intangible Assets vs. Cost Leadership in Transition

Morgan Stanley’s intangible asset moat is deeper, anchored by client trust and diversified services. Hut 8’s cost advantage shows promise but remains a narrower moat due to high capital intensity and market volatility. I see Morgan Stanley better positioned to defend market share over the long term.

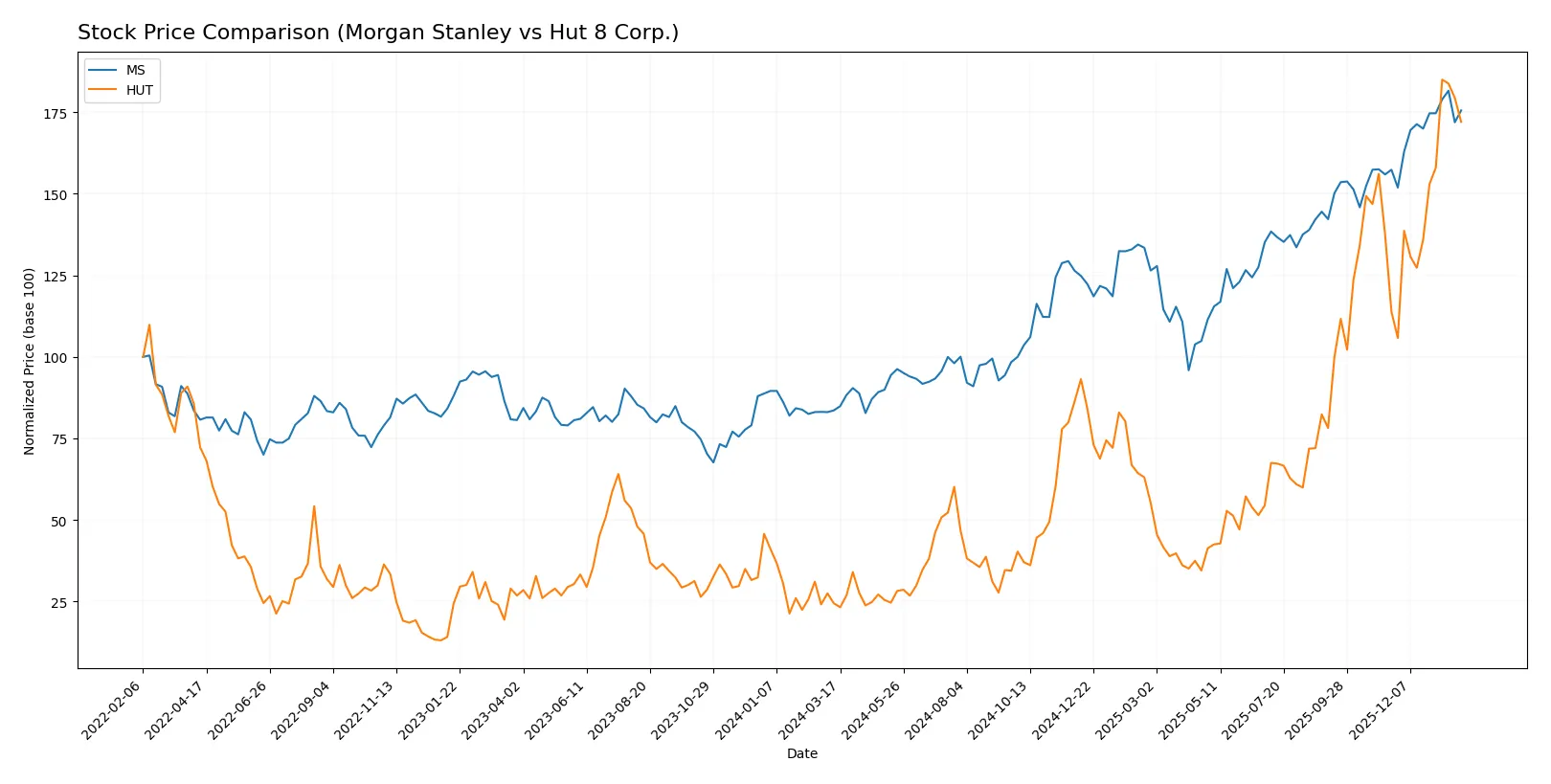

Which stock offers better returns?

Over the past year, Morgan Stanley and Hut 8 Corp. both posted strong price gains, with Hut 8 exhibiting a notably sharper rise and differing trading volume dynamics.

Trend Comparison

Morgan Stanley’s stock rose 110.02% over the past 12 months, showing a bullish trend with accelerating momentum and a high volatility level (std dev 27.48). It reached a peak of 189.09 and a low of 86.19.

Hut 8 Corp. gained 604.04% in the same period, also bullish with accelerating momentum but lower volatility (std dev 13.66). It hit a high of 60.04 and a low of 7.54.

Hut 8 Corp. outperformed Morgan Stanley, delivering the highest market returns over the past year, with a more pronounced price increase and sustained acceleration.

Target Prices

Analysts present a clear upward target consensus for both Morgan Stanley and Hut 8 Corp., signaling positive market expectations.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Morgan Stanley | 165 | 220 | 196 |

| Hut 8 Corp. | 55 | 85 | 70.1 |

Morgan Stanley’s consensus target of 196 exceeds its current price of 183, suggesting upside potential. Hut 8’s consensus target of 70.1 also outpaces its current price of 55.8, indicating expected growth.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Morgan Stanley Grades

Below are the recent grades from established financial institutions for Morgan Stanley:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Keefe, Bruyette & Woods | Maintain | Outperform | 2026-01-16 |

| JP Morgan | Maintain | Neutral | 2026-01-08 |

| Barclays | Maintain | Overweight | 2026-01-05 |

| Keefe, Bruyette & Woods | Maintain | Outperform | 2025-12-17 |

| Wolfe Research | Upgrade | Outperform | 2025-11-24 |

| JP Morgan | Maintain | Neutral | 2025-10-21 |

| Keefe, Bruyette & Woods | Maintain | Outperform | 2025-10-16 |

| Citigroup | Maintain | Neutral | 2025-10-16 |

| Jefferies | Maintain | Buy | 2025-10-16 |

| Evercore ISI Group | Maintain | Outperform | 2025-10-16 |

Hut 8 Corp. Grades

Here are the latest grades from recognized financial firms for Hut 8 Corp.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Keefe, Bruyette & Woods | Maintain | Outperform | 2026-01-27 |

| Needham | Maintain | Buy | 2026-01-16 |

| B. Riley Securities | Maintain | Buy | 2026-01-09 |

| Keefe, Bruyette & Woods | Maintain | Outperform | 2025-12-19 |

| Rosenblatt | Maintain | Buy | 2025-12-18 |

| Canaccord Genuity | Maintain | Buy | 2025-12-18 |

| Needham | Maintain | Buy | 2025-12-18 |

| BTIG | Maintain | Buy | 2025-12-17 |

| BTIG | Maintain | Buy | 2025-11-06 |

| Rosenblatt | Maintain | Buy | 2025-11-05 |

Which company has the best grades?

Both Morgan Stanley and Hut 8 Corp. receive predominantly positive grades from reputable firms. Hut 8 Corp. consistently earns “Buy” and “Outperform,” indicating strong institutional confidence. Morgan Stanley also sees frequent “Outperform” ratings but includes more “Neutral” grades. Investors may view Hut 8’s steadier positive consensus as a signal of higher near-term enthusiasm.

Risks specific to each company

In 2026’s market environment, these categories highlight the critical pressure points and systemic threats facing Morgan Stanley and Hut 8 Corp.:

1. Market & Competition

Morgan Stanley

- Faces intense competition in global capital markets with pressure on fees and advisory services.

Hut 8 Corp.

- Operates in a volatile and rapidly evolving crypto mining sector with fierce competition and technological obsolescence risk.

2. Capital Structure & Debt

Morgan Stanley

- Shows favorable debt-to-equity and debt-to-assets ratios but weak interest coverage at 0.45 signals risk managing debt costs.

Hut 8 Corp.

- Maintains moderate leverage with 0.35 debt-to-equity and strong interest coverage at 16.17, signaling better debt service ability.

3. Stock Volatility

Morgan Stanley

- Beta of 1.20 indicates moderate market sensitivity typical for large financial firms.

Hut 8 Corp.

- Extremely high beta at 6.19 reflects extreme stock price volatility and risk associated with crypto sector.

4. Regulatory & Legal

Morgan Stanley

- Subject to complex global financial regulations and potential legal risks in advisory and trading activities.

Hut 8 Corp.

- Faces emerging regulatory uncertainty in cryptocurrency mining and energy consumption policies.

5. Supply Chain & Operations

Morgan Stanley

- Relies on robust IT and human capital infrastructure; operational risks tied to technology and talent retention.

Hut 8 Corp.

- Dependent on energy supply and hardware availability; vulnerable to energy cost spikes and equipment shortages.

6. ESG & Climate Transition

Morgan Stanley

- Increasing pressure to enhance ESG disclosures and sustainable finance offerings.

Hut 8 Corp.

- Faces significant risks due to high energy consumption and carbon footprint amid tightening climate regulations.

7. Geopolitical Exposure

Morgan Stanley

- Operates globally, exposed to geopolitical tensions impacting financial markets and cross-border transactions.

Hut 8 Corp.

- Mostly U.S.-based but sensitive to geopolitical shifts affecting energy markets and crypto regulations.

Which company shows a better risk-adjusted profile?

Morgan Stanley’s principal risk lies in weak interest coverage and regulatory complexity, while Hut 8 Corp. faces extreme stock volatility and ESG challenges. Despite Hut 8’s operational risks, its strong interest coverage and safe Altman Z-score suggest a better risk-adjusted profile. Hut 8’s recent 9.3% stock drop underscores volatility concerns, yet its financial stability contrasts with Morgan Stanley’s distress-zone Altman Z-score, signaling greater bankruptcy risk.

Final Verdict: Which stock to choose?

Morgan Stanley’s superpower lies in its resilience as a cash-generating financial giant with a strong net margin and steady revenue growth. Its point of vigilance is the strained liquidity profile and interest coverage, which could pressure stability in a rising rate environment. It suits portfolios seeking established financial sector exposure with moderate growth.

Hut 8 Corp. boasts a strategic moat in rapid scalability and operational leverage within the cryptocurrency mining niche, reflected in its robust profitability ratios and improving capital efficiency. Compared to Morgan Stanley, it offers higher growth potential but with elevated volatility and risk. It fits well in portfolios targeting high-growth, tech-adjacent assets with tolerance for swings.

If you prioritize stable cash flow and defensive positioning, Morgan Stanley is the compelling choice due to its entrenched market presence and income consistency. However, if you seek aggressive growth with exposure to emerging blockchain technologies, Hut 8 offers superior upside potential, albeit with greater risk and valuation volatility.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Morgan Stanley and Hut 8 Corp. to enhance your investment decisions: