Home > Comparison > Healthcare > UNH vs HUM

The strategic rivalry between UnitedHealth Group Incorporated and Humana Inc. defines the current trajectory of the healthcare plans industry. UnitedHealth operates as a diversified healthcare giant with broad service segments, including Optum’s technology and pharmacy services. Humana focuses on health and well-being with a strong emphasis on Medicare and specialty benefits. This analysis will identify which business model provides a superior risk-adjusted opportunity for a diversified portfolio in healthcare.

Table of contents

Companies Overview

UnitedHealth Group and Humana stand as pivotal players in the competitive US healthcare plans market.

UnitedHealth Group Incorporated: Healthcare Powerhouse with Diversified Services

UnitedHealth Group dominates as a diversified healthcare company, generating revenue from four segments including UnitedHealthcare and Optum. Its core business lies in consumer health benefit plans and comprehensive care services. In 2026, the company’s strategic focus remains on expanding integrated care delivery and leveraging technology across its Optum segments to drive efficiency and patient outcomes.

Humana Inc.: Specialized Health and Well-being Provider

Humana operates primarily as a health and well-being company, with revenues driven by medical and supplemental benefit plans for individuals and groups. It emphasizes Medicare and Medicaid programs, alongside pharmacy and home health services. The company’s 2026 strategy centers on deepening its specialty health offerings and enhancing care management for chronic conditions to capture an aging population.

Strategic Collision: Similarities & Divergences

Both companies prioritize healthcare plans but differ in approach: UnitedHealth pursues a diversified integrated model combining insurance and care delivery, while Humana focuses on specialized health services with a Medicare emphasis. Their primary battleground is managing chronic care and Medicare membership growth. Investors will note UnitedHealth’s scale and technology integration contrast with Humana’s focused niche and member-centric care approach.

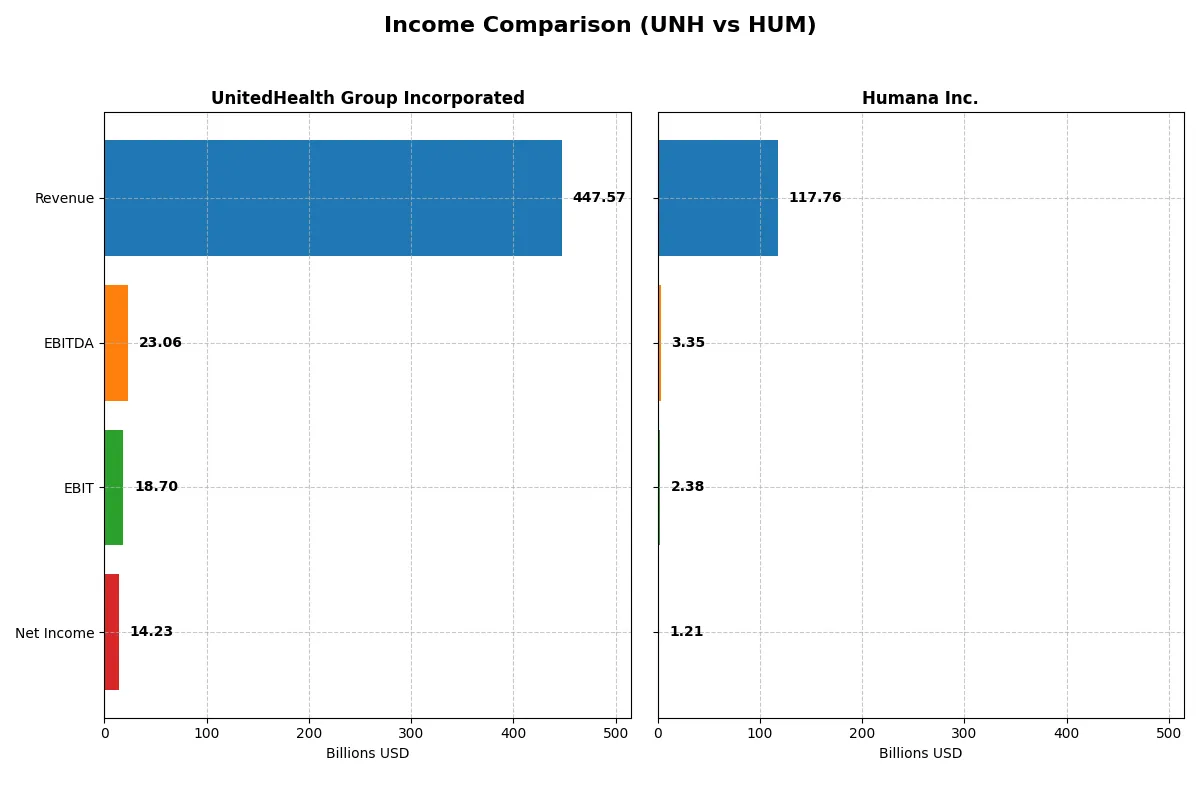

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | UnitedHealth Group (UNH) | Humana (HUM) |

|---|---|---|

| Revenue | 448B | 118B |

| Cost of Revenue | 365B | 0 |

| Operating Expenses | 64B | 116B |

| Gross Profit | 83B | 118B |

| EBITDA | 23B | 3.3B |

| EBIT | 19B | 2.4B |

| Interest Expense | 4B | 0.66B |

| Net Income | 14.2B | 1.2B |

| EPS | 15.66 | 10.01 |

| Fiscal Year | 2025 | 2024 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company converts revenue into profit most efficiently, highlighting their operational strength.

UnitedHealth Group Incorporated Analysis

UnitedHealth’s revenue rose steadily from 287.6B in 2021 to 447.6B in 2025, reflecting robust growth. However, net income fell from 22.4B in 2023 to 14.2B in 2025, indicating margin pressure. Gross margin declined to 18.5% in 2025, and net margin dropped to 3.18%, signaling deteriorating profitability despite revenue momentum.

Humana Inc. Analysis

Humana’s revenue increased from 77.2B in 2020 to 117.8B in 2024, showing solid top-line growth. Net income, however, contracted sharply from 3.4B in 2020 to 1.2B in 2024, reflecting margin compression. The gross margin remains at 100% due to reporting format, but the net margin stood at a low 1.02% in 2024, underscoring weak bottom-line efficiency.

Verdict: Revenue Expansion vs. Margin Sustainability

UnitedHealth dominates in scale and revenue growth but struggles with declining margins and net income contraction. Humana shows similar growth but with even steeper net income declines and lower profitability ratios. For risk-averse investors, UnitedHealth’s size and margin resilience offer a more attractive profile despite recent setbacks.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | UnitedHealth Group Incorporated (UNH) | Humana Inc. (HUM) |

|---|---|---|

| ROE | 14.2% (2025) | 7.4% (2024) |

| ROIC | 9.4% (2025) | N/A |

| P/E | 21.1 (2025) | 25.3 (2024) |

| P/B | 3.0 (2025) | 1.9 (2024) |

| Current Ratio | 0.79 (2025) | 0.0 (2024) |

| Quick Ratio | 0.79 (2025) | 0.0 (2024) |

| D/E | 0.78 (2025) | 0.68 (2024) |

| Debt-to-Assets | 25.3% (2025) | 24.0% (2024) |

| Interest Coverage | 4.7x (2025) | 2.6x (2024) |

| Asset Turnover | 1.45 (2025) | 2.53 (2024) |

| Fixed Asset Turnover | 0.0 (2025) | 39.6 (2024) |

| Payout ratio | 97.2% (2025) | 35.7% (2024) |

| Dividend yield | 4.6% (2025) | 1.4% (2024) |

| Fiscal Year | 2025 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as a company’s DNA, exposing hidden risks and operational excellence behind headline numbers.

UnitedHealth Group Incorporated

UnitedHealth posts a neutral ROE at 14.2% and a modest net margin of 3.18%, signaling steady profitability. Its P/E of 21.1 indicates a fairly valued stock, while a dividend yield of 4.6% rewards shareholders handsomely. The firm balances reinvestment with shareholder returns, maintaining moderate leverage and stable asset turnover.

Humana Inc.

Humana’s ROE is weaker at 7.4%, with a low net margin of 1.02%, reflecting operational challenges. The P/E ratio of 25.3 suggests a stretched valuation. Humana offers a lower dividend yield of 1.4%, implying a cautious payout policy. Despite high asset turnover, the firm’s financial ratios show mixed signals on efficiency and profitability.

Valuation Discipline vs. Profitability Strength

UnitedHealth offers a better balance of profitability and shareholder returns with reasonable valuation metrics. Humana’s higher valuation and weaker profitability ratios indicate greater risk. Investors seeking steady income and operational consistency may find UnitedHealth’s profile more compelling.

Which one offers the Superior Shareholder Reward?

I see UnitedHealth Group (UNH) offers a robust 4.6% dividend yield in 2025 with a nearly 100% payout ratio, signaling a heavy but well-covered commitment to dividends. UNH’s free cash flow comfortably supports this yield at 83.5%, and its buyback program further amplifies returns, showing strong capital allocation. Humana (HUM) yields a modest 1.4% with a 35.7% payout ratio, preserving cash for growth and acquisitions, supported by a solid free cash flow conversion near 80%. However, Humana’s buybacks are less aggressive. I judge UNH’s distribution model more sustainable, blending income and share repurchases, thus offering a superior total shareholder return profile in 2026.

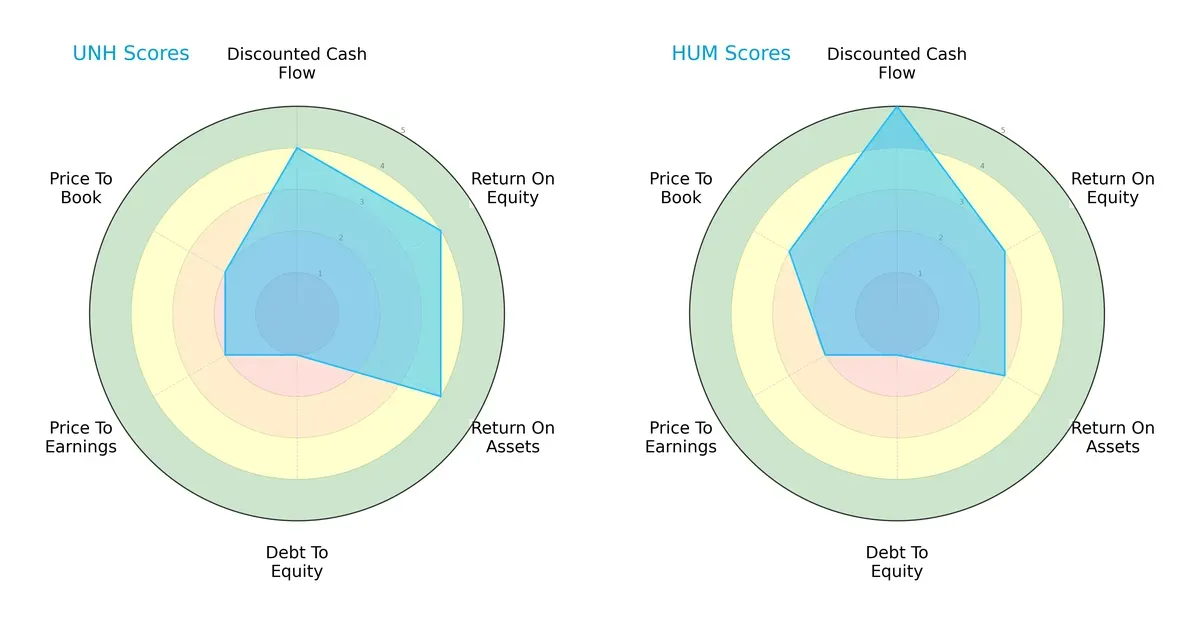

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of UnitedHealth Group and Humana, highlighting their core financial strengths and vulnerabilities:

UnitedHealth Group shows strong operational efficiency with solid ROE and ROA scores of 4 each, outperforming Humana’s moderate 3s. Humana leads in discounted cash flow valuation (5 vs. 4), suggesting better future cash flow prospects. Both firms carry high financial risk with identical weak debt-to-equity scores (1). Valuation metrics favor Humana slightly on price-to-book (3 vs. 2), while UnitedHealth holds a marginal edge on price-to-earnings. UnitedHealth delivers a more balanced profile across profitability and asset utilization, whereas Humana depends heavily on discounted cash flows.

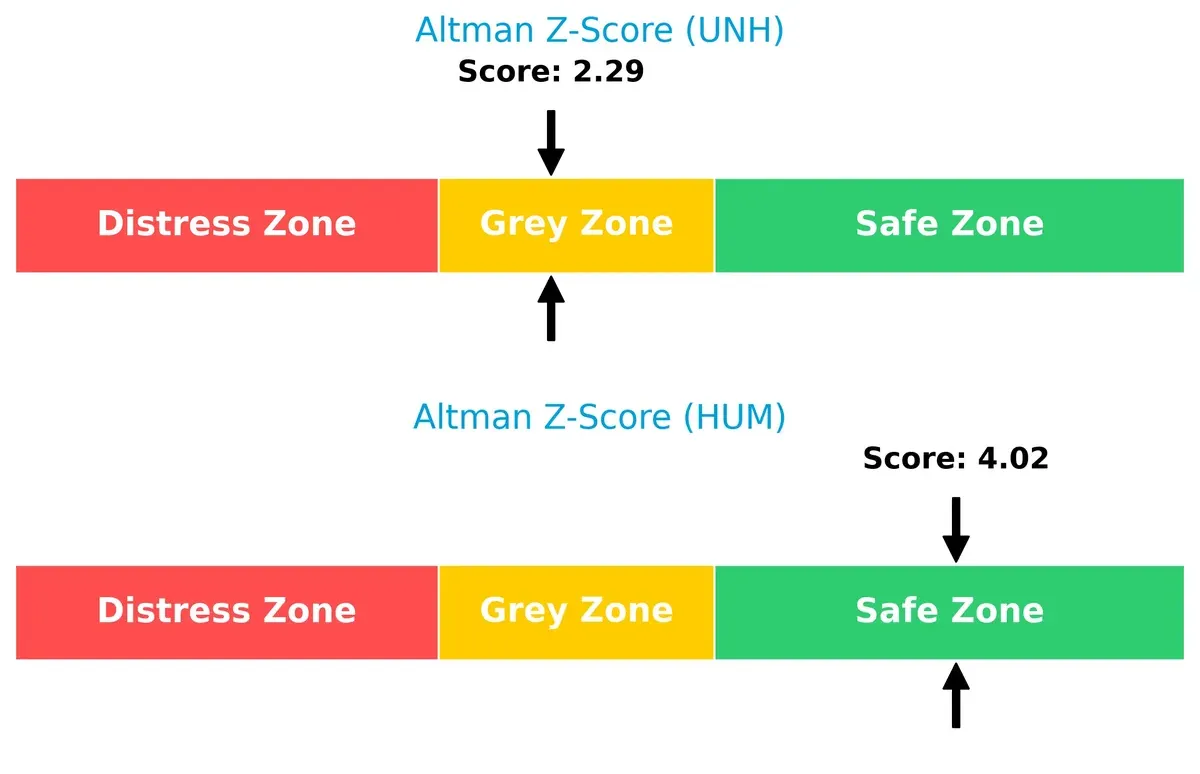

Bankruptcy Risk: Solvency Showdown

The Altman Z-Score gap of nearly 1.7 points puts Humana in a safer zone versus UnitedHealth’s grey area, signaling stronger long-term solvency for Humana:

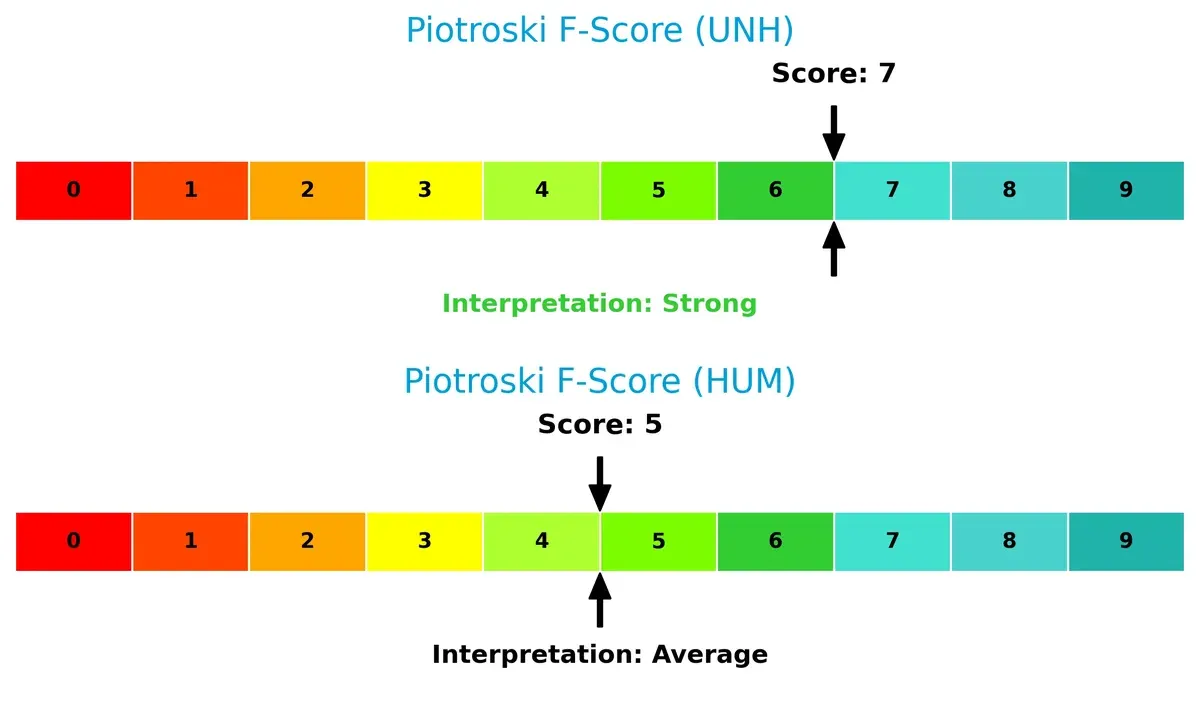

Financial Health: Quality of Operations

UnitedHealth’s Piotroski F-Score of 7 indicates robust financial health, outpacing Humana’s average score of 5 and signaling fewer internal red flags:

How are the two companies positioned?

This section dissects UNH and HUM’s operational DNA by comparing revenue distribution and internal strengths and weaknesses. The goal is to confront their economic moats and identify which model delivers the most resilient competitive advantage today.

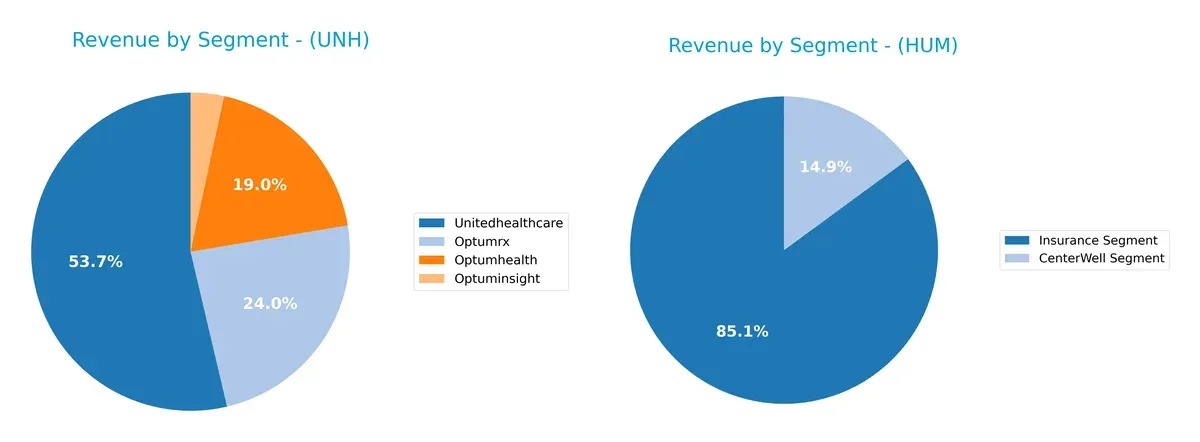

Revenue Segmentation: The Strategic Mix

The following visual comparison dissects how UnitedHealth Group and Humana diversify their income streams and where their primary sector bets lie:

UnitedHealth Group anchors its revenue in UnitedHealthcare at $298B (2024), with significant contributions from OptumRx ($133B) and OptumHealth ($105B), showcasing a broad, integrated ecosystem. Humana, by contrast, pivots mainly on its Insurance Segment at $114B, supplemented by CenterWell at $20B, reflecting less diversification. UnitedHealth’s multi-pronged model reduces concentration risk, while Humana’s reliance on insurance exposes it to sector-specific regulatory pressures.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of UnitedHealth Group Incorporated and Humana Inc.:

UnitedHealth Group Strengths

- Diversified revenue streams across Optumhealth, Optuminsight, Optumrx, and UnitedHealthcare

- Favorable debt-to-assets ratio at 25.32% supports financial stability

- Asset turnover at 1.45 indicates efficient use of assets

- Dividend yield of 4.6% appeals to income-focused investors

Humana Strengths

- Favorable asset turnover at 2.53 and fixed asset turnover at 39.56 show operational efficiency

- Favorable debt-to-assets ratio at 23.98% supports manageable leverage

- Diversified segments including CenterWell and Insurance contribute to revenue mix

UnitedHealth Group Weaknesses

- Unfavorable current and quick ratios at 0.79 raise liquidity concerns

- Net margin low at 3.18%, signaling profitability pressures

- Unfavorable price-to-book ratio at 3.0 suggests possible overvaluation

- Fixed asset turnover at zero indicates potential underutilization

Humana Weaknesses

- Unfavorable net margin at 1.02% and ROE at 7.37% reflect weak profitability

- Zero ROIC points to poor capital efficiency

- Unfavorable P/E at 25.34 may imply overvaluation

- Zero current and quick ratios raise liquidity red flags

UnitedHealth exhibits stronger diversification and more balanced financial health despite some liquidity weaknesses. Humana shows operational efficiency but struggles with profitability and liquidity, which may affect its strategic flexibility.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat alone shields long-term profits from relentless competition and market pressures. Let’s dissect how these companies defend their turf:

UnitedHealth Group Incorporated: Diversified Ecosystem Moat

UnitedHealth exploits a diversified healthcare ecosystem combining insurance and care delivery. Its ROIC exceeds WACC by 4%, indicating value creation despite a declining trend. New Optum services could deepen this moat in 2026.

Humana Inc.: Focused Service Niche Moat

Humana relies on specialized Medicare Advantage plans, a narrower moat than UnitedHealth’s broad platform. Its ROIC lags below WACC by 5.5%, signaling value destruction. Expansion in home health care offers growth potential but also risks margin pressure.

Ecosystem Scale vs. Niche Specialization: Moat Durability Tested

UnitedHealth’s wider ecosystem moat outmatches Humana’s focused niche, evidenced by positive ROIC spread and scale advantages. UnitedHealth is better positioned to defend and grow market share amid intensifying healthcare competition.

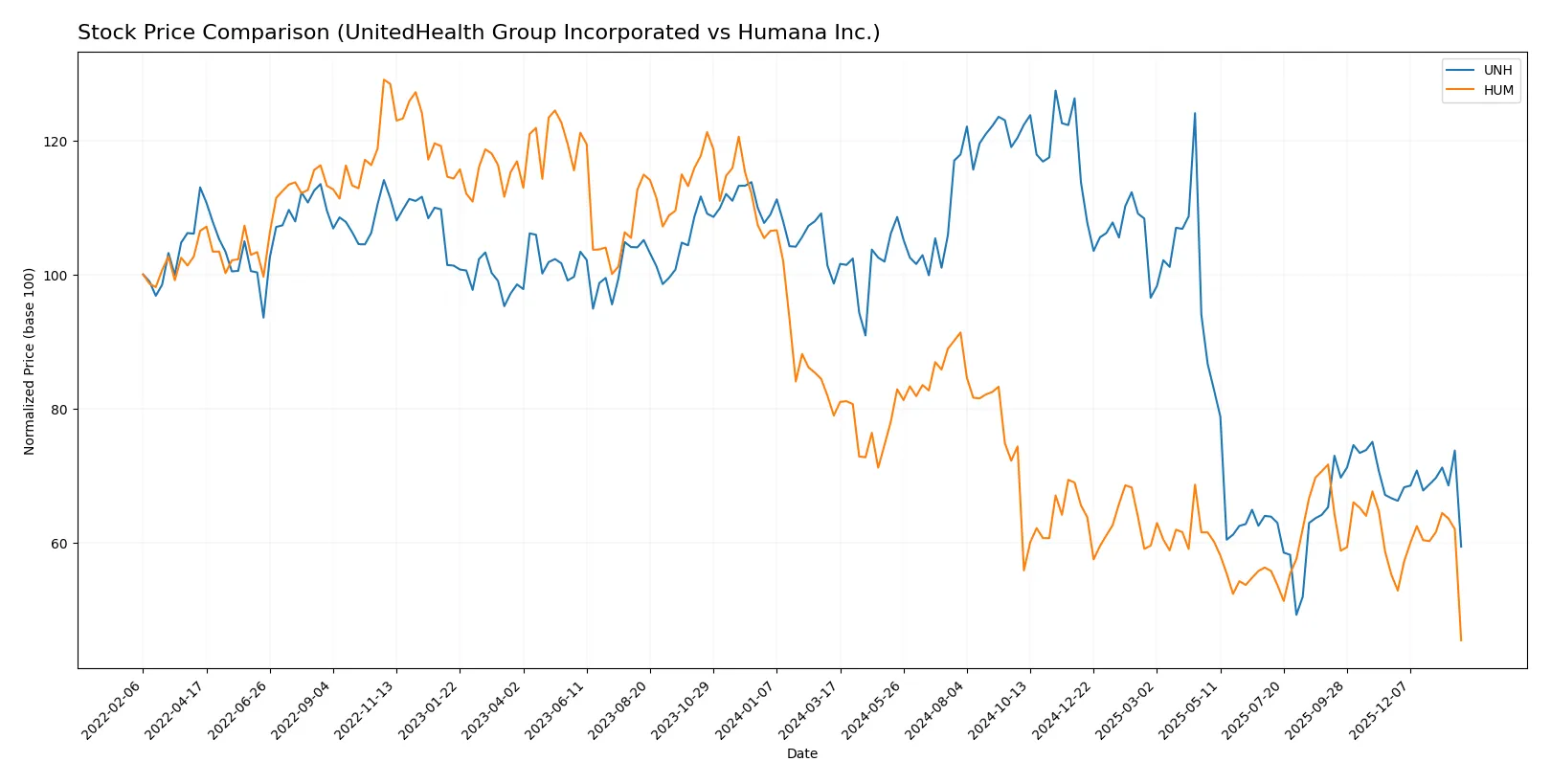

Which stock offers better returns?

Over the past 12 months, both UnitedHealth Group and Humana have experienced significant price declines with accelerating bearish momentum, reflected in notable highs and lows within their trading ranges.

Trend Comparison

UnitedHealth Group’s stock fell 39.79% over the past year, showing a bearish trend with accelerating decline and high volatility (std. dev. 109.55). The stock hit a high of 615.81 and a low of 237.77.

Humana’s shares dropped 42.48% over the same period, also bearish and accelerating, though with lower volatility (std. dev. 44.81). Its trading range spanned from 392.63 to 195.2.

Comparing both trends, UnitedHealth Group slightly outperformed Humana, delivering a smaller overall price decline and higher buyer volume despite strong selling pressure.

Target Prices

Analysts present a cautiously optimistic consensus for UnitedHealth Group and Humana, reflecting confidence in healthcare plan leaders.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| UnitedHealth Group Incorporated | 327 | 444 | 387.88 |

| Humana Inc. | 234 | 345 | 288.5 |

The target consensus for UnitedHealth at $388 exceeds the current $287 price, implying upside potential. Humana’s $289 consensus also suggests substantial room for appreciation from $195.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

This section compares recent analyst grades from leading financial institutions for both companies:

UnitedHealth Group Incorporated Grades

The following table summarizes recent grades issued by major financial institutions for UnitedHealth Group Incorporated.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Wells Fargo | Maintain | Overweight | 2026-01-30 |

| Barclays | Maintain | Overweight | 2026-01-30 |

| Leerink Partners | Maintain | Outperform | 2026-01-28 |

| RBC Capital | Maintain | Outperform | 2026-01-28 |

| UBS | Maintain | Buy | 2026-01-28 |

| Oppenheimer | Maintain | Outperform | 2026-01-28 |

| Jefferies | Maintain | Buy | 2026-01-28 |

| Morgan Stanley | Maintain | Overweight | 2026-01-23 |

| Barclays | Maintain | Overweight | 2026-01-05 |

| TD Cowen | Maintain | Hold | 2025-10-30 |

Humana Inc. Grades

Below is a summary of recent institutional grades for Humana Inc. from recognized financial analysts.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Wells Fargo | Downgrade | Equal Weight | 2026-01-07 |

| Barclays | Maintain | Equal Weight | 2026-01-05 |

| Morgan Stanley | Maintain | Equal Weight | 2025-12-18 |

| Jefferies | Upgrade | Buy | 2025-12-05 |

| Barclays | Maintain | Equal Weight | 2025-11-25 |

| Truist Securities | Maintain | Hold | 2025-11-10 |

| Deutsche Bank | Maintain | Hold | 2025-11-07 |

| B of A Securities | Maintain | Neutral | 2025-10-10 |

| Mizuho | Maintain | Outperform | 2025-10-09 |

| Wells Fargo | Maintain | Overweight | 2025-10-07 |

Which company has the best grades?

UnitedHealth Group consistently receives higher grades such as Overweight, Outperform, and Buy from multiple top-tier firms. Humana’s grades are more mixed, with several Equal Weight and Hold ratings. Stronger grades for UnitedHealth suggest greater institutional confidence, potentially influencing investor sentiment more positively.

Risks specific to each company

The following categories identify critical pressure points and systemic threats facing UnitedHealth Group and Humana in the 2026 market environment:

1. Market & Competition

UnitedHealth Group Incorporated

- Dominates with a 259B market cap and diverse healthcare segments, but faces margin pressure and premium competition.

Humana Inc.

- Smaller scale at 23B market cap, focusing on specialty and retail segments with growth potential but competitive risks.

2. Capital Structure & Debt

UnitedHealth Group Incorporated

- Moderate leverage (D/E 0.78), favorable debt-to-assets ratio (25.3%), but flagged for weak liquidity (current ratio 0.79).

Humana Inc.

- Slightly lower leverage (D/E 0.68) with better debt-to-assets (24%), but current and quick ratios at zero highlight liquidity concerns.

3. Stock Volatility

UnitedHealth Group Incorporated

- Low beta (0.43) suggests defensive stock with stable price movements despite wide trading range.

Humana Inc.

- Similar low beta (0.46) indicates modest volatility; however, narrower price range may limit upside.

4. Regulatory & Legal

UnitedHealth Group Incorporated

- Complex regulatory environment tied to Medicare and Medicaid programs; large scale increases regulatory scrutiny risks.

Humana Inc.

- Also heavily dependent on government contracts, with exposure to policy shifts affecting specialty and long-term care services.

5. Supply Chain & Operations

UnitedHealth Group Incorporated

- Integrated Optum segments improve operational control, but fixed asset turnover at zero signals potential inefficiencies.

Humana Inc.

- Higher fixed asset turnover (39.56) shows operational efficiency, but smaller scale may limit supply chain leverage.

6. ESG & Climate Transition

UnitedHealth Group Incorporated

- Increasing ESG focus required given healthcare’s environmental footprint; scale allows investment in sustainability initiatives.

Humana Inc.

- ESG initiatives less visible, though specialty services offer opportunities to innovate in social responsibility.

7. Geopolitical Exposure

UnitedHealth Group Incorporated

- Primarily US-centric, limiting geopolitical risk but increasing regulatory and political exposure domestically.

Humana Inc.

- Similar US focus, with possible vulnerability to state-level Medicaid program changes amid political shifts.

Which company shows a better risk-adjusted profile?

UnitedHealth’s largest risk is its weak liquidity despite strong market position and diversified operations. Humana’s biggest concern lies in its limited scale and liquidity gaps, raising solvency questions. Overall, UnitedHealth’s lower stock volatility and stronger operational integration suggest a better risk-adjusted profile. However, UnitedHealth’s Altman Z-Score in the grey zone (2.29) versus Humana’s safe zone (4.02) signals caution on near-term financial distress risk, making risk management essential for both.

Final Verdict: Which stock to choose?

UnitedHealth Group’s superpower lies in its robust capital efficiency and consistent value creation, reflected by an ROIC comfortably above its WACC. However, its tight liquidity position signals a point of vigilance. UNH fits well within portfolios seeking aggressive growth backed by operational strength and scale.

Humana’s strategic moat centers on its asset turnover efficiency and stable operating cash flow. While it lacks the same capital value creation as UNH, it offers a comparatively safer profile with a sound balance sheet. HUM suits investors favoring GARP strategies that blend growth potential with reasonable valuation discipline.

If you prioritize aggressive growth and capital efficiency, UnitedHealth outshines with its superior value creation despite some liquidity concerns. However, if you seek better stability with efficient asset use and moderate risk, Humana offers a compelling alternative. Both choices require careful risk management given recent bearish trends.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of UnitedHealth Group Incorporated and Humana Inc. to enhance your investment decisions: