Home > Comparison > Industrials > PNR vs GNRC

The strategic rivalry between Pentair plc and Generac Holdings shapes the industrial machinery sector’s future. Pentair operates as a water solutions powerhouse with diversified fluid treatment products, while Generac specializes in power generation and energy storage systems. This head-to-head pits Pentair’s broad industrial footprint against Generac’s focused innovation in energy resilience. This analysis will identify which company offers superior risk-adjusted returns aligned with evolving industrial demands and portfolio diversification goals.

Table of contents

Companies Overview

Pentair plc and Generac Holdings Inc. both wield significant influence in the industrial machinery sector.

Pentair plc: Global Water Solutions Leader

Pentair plc dominates the water solutions market through its Consumer Solutions and Industrial & Flow Technologies segments. It generates revenue by manufacturing pool equipment, water treatment systems, and fluid handling products worldwide. In 2026, Pentair focuses strategically on expanding advanced membrane filtration and sustainable water management technologies, reinforcing its competitive edge in diversified water applications.

Generac Holdings Inc.: Power Generation Innovator

Generac Holdings Inc. stands out as a leading supplier of power generation equipment and energy storage solutions. It monetizes its business by selling residential and commercial standby generators, portable generators, and clean energy products. The company’s 2026 strategy emphasizes growth in home standby generators, remote monitoring, and integration of clean energy systems under the PWRcell brand, targeting expanding demand for reliable and sustainable power.

Strategic Collision: Similarities & Divergences

Pentair and Generac both operate in critical industrial markets but diverge in product focus—water systems versus power generation. Their primary battleground lies in serving residential and commercial customers with essential infrastructure products. Pentair leans on diversified water technology, while Generac pushes innovation in energy reliability and clean power. This contrast shapes distinct investment profiles: Pentair as a water technology stalwart, Generac as a power sector growth play.

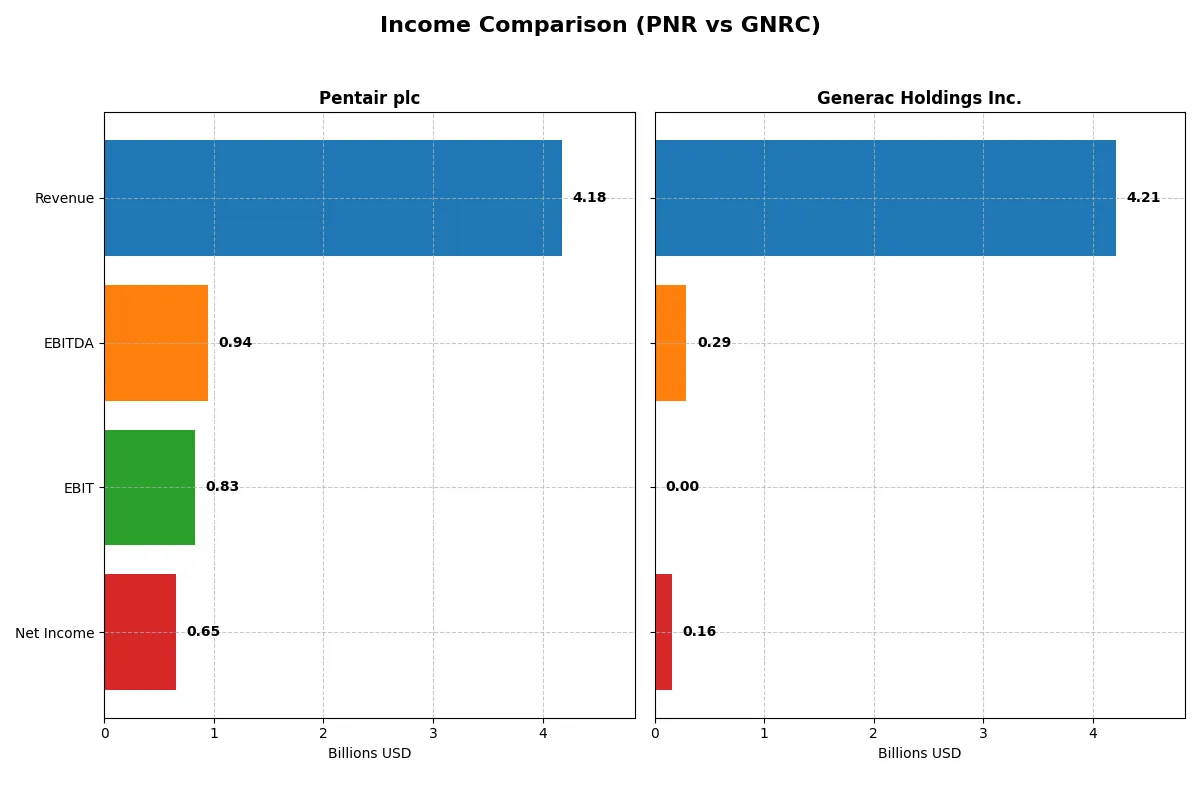

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Pentair plc (PNR) | Generac Holdings Inc. (GNRC) |

|---|---|---|

| Revenue | 4.18B | 4.21B |

| Cost of Revenue | 2.49B | 2.60B |

| Operating Expenses | 833M | 1.32B |

| Gross Profit | 1.69B | 1.61B |

| EBITDA | 944M | 289M |

| EBIT | 826M | 0 |

| Interest Expense | 69M | -71M |

| Net Income | 654M | 160M |

| EPS | 3.99 | 2.73 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison exposes the true operational efficiency and profitability dynamics behind two corporate engines powering their sectors.

Pentair plc Analysis

Pentair’s revenue grew moderately, reaching 4.18B in 2025, with net income climbing to 654M. Its gross margin sustains a healthy 40.5%, while the net margin stands at a robust 15.7%. The company shows steady margin expansion and EPS growth, reflecting disciplined cost control and improving profitability momentum.

Generac Holdings Inc. Analysis

Generac’s revenue slipped slightly to 4.21B in 2025, while net income plunged to 160M, yielding a thin net margin of 3.8%. Gross margin remains favorable at 38.3%, but EBIT margin collapsed to zero, signaling operational inefficiencies. Recent declines in profitability and EPS highlight significant margin pressure and deteriorating income quality.

Margin Resilience vs. Profitability Erosion

Pentair clearly outperforms Generac with superior margin health and consistent net income growth. Pentair’s efficient cost management sustains strong returns, while Generac struggles with shrinking profits despite comparable revenue scale. Investors seeking stability and margin expansion will find Pentair’s profile more attractive amid Generac’s troubling earnings erosion.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Pentair plc (PNR) | Generac Holdings Inc. (GNRC) |

|---|---|---|

| ROE | 16.9% | 0% |

| ROIC | 12.5% | 0% |

| P/E | 26.1 | 50.0 |

| P/B | 4.42 | 0 |

| Current Ratio | 1.61 | 0 |

| Quick Ratio | 0.95 | 0 |

| D/E (Debt to Equity) | 0.42 | 0 |

| Debt-to-Assets | 23.9% | 0% |

| Interest Coverage | 12.36 | -4.09 |

| Asset Turnover | 0.61 | 0 |

| Fixed Asset Turnover | 11.08 | 0 |

| Payout Ratio | 25.1% | 0.18% |

| Dividend Yield | 0.96% | 0.004% |

| Fiscal Year | 2025 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Ratios act as a company’s DNA, unveiling hidden risks and operational strengths that shape its market performance and investor appeal.

Pentair plc

Pentair exhibits strong profitability with a 16.9% ROE and a solid 15.66% net margin, reflecting operational efficiency. Its valuation appears stretched, marked by a 26.14 P/E and 4.42 P/B ratio, above sector norms. Shareholder returns include a modest 0.96% dividend yield, indicating some cash distribution alongside reinvestment in R&D for growth.

Generac Holdings Inc.

Generac shows weak profitability, with a 3.79% net margin and zero ROE, signaling operational challenges. The stock is expensive, trading at a 50.02 P/E, while lacking dividends. Its reinvestment strategy focuses heavily on R&D, but unfavorable ratios and zero liquidity ratios raise red flags on financial health and risk management.

Premium Valuation vs. Operational Safety

Pentair balances favorable profitability and moderate risk despite a stretched valuation. Generac’s high valuation and poor profitability signal elevated risk. Investors seeking stability might lean toward Pentair, while those favoring growth with higher risk may consider Generac’s profile.

Which one offers the Superior Shareholder Reward?

I observe Pentair (PNR) maintains a steady dividend yield near 1%, with a payout ratio around 25%, signaling balanced income and growth. It pairs dividends with moderate buybacks, enhancing total returns sustainably. Generac (GNRC) pays a negligible dividend but aggressively reinvests free cash flow into growth, supported by strong free cash flow per share of $7.5 and buybacks. However, GNRC’s profitability margins and earnings stability lag PNR’s. For 2026, Pentair’s reliable, well-covered dividends and buyback discipline offer a more attractive and sustainable shareholder reward than Generac’s high-growth but riskier reinvestment model.

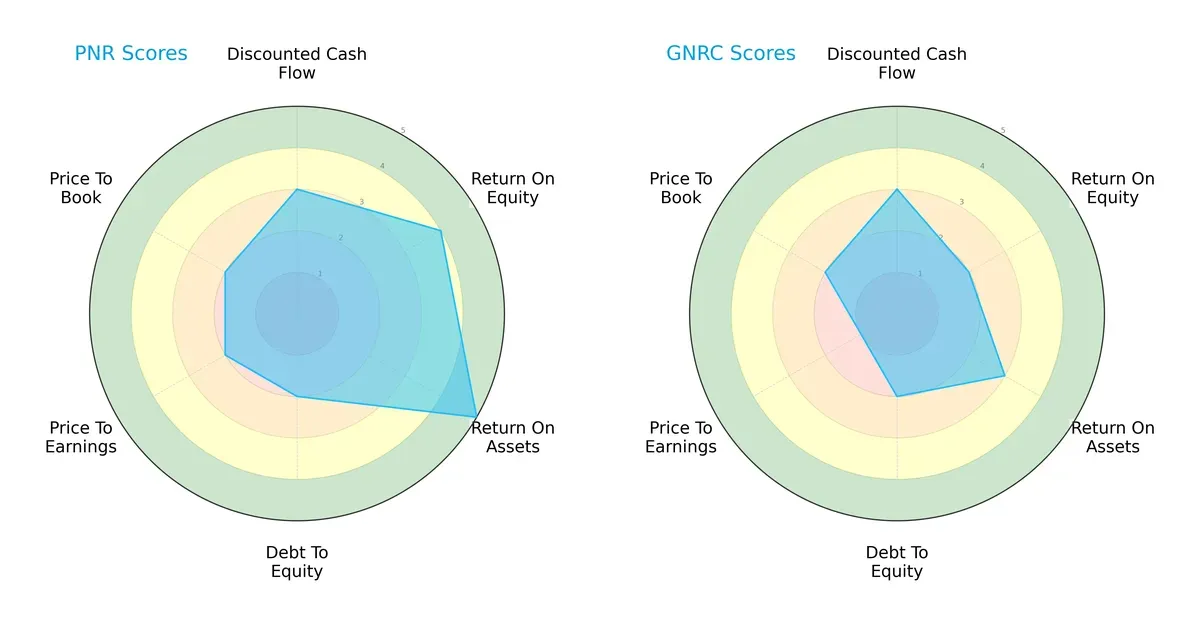

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Pentair plc and Generac Holdings Inc., highlighting their investment strengths and vulnerabilities:

Pentair shows a more balanced profile with strong operational efficiency (ROA 5) and profitability (ROE 4). However, it struggles with leverage and valuation (Debt/Equity 2, PE/PB 2). Generac relies on moderate cash flow (DCF 3) but falls short on profitability (ROE 2) and valuation (PE 1), indicating reliance on a specific edge rather than broad strength.

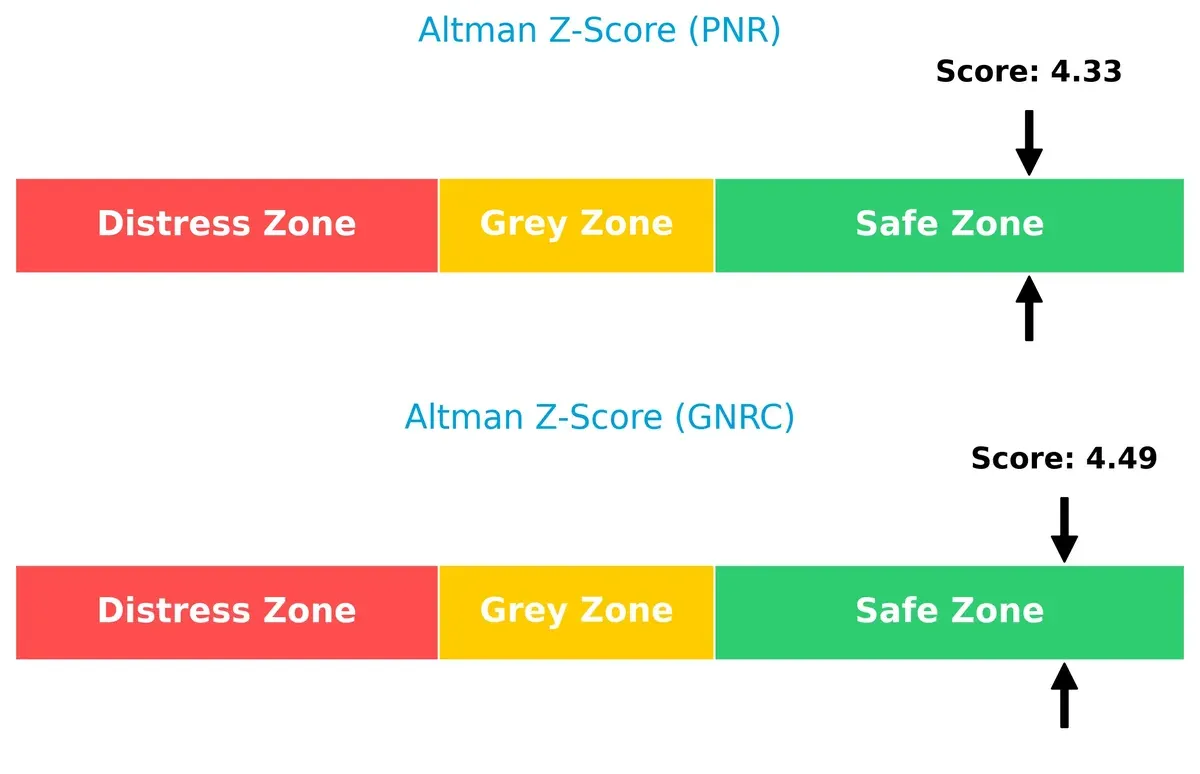

Bankruptcy Risk: Solvency Showdown

Pentair and Generac both reside safely above the distress threshold, but Generac’s slightly higher Altman Z-Score suggests marginally better long-term survival odds in this cycle:

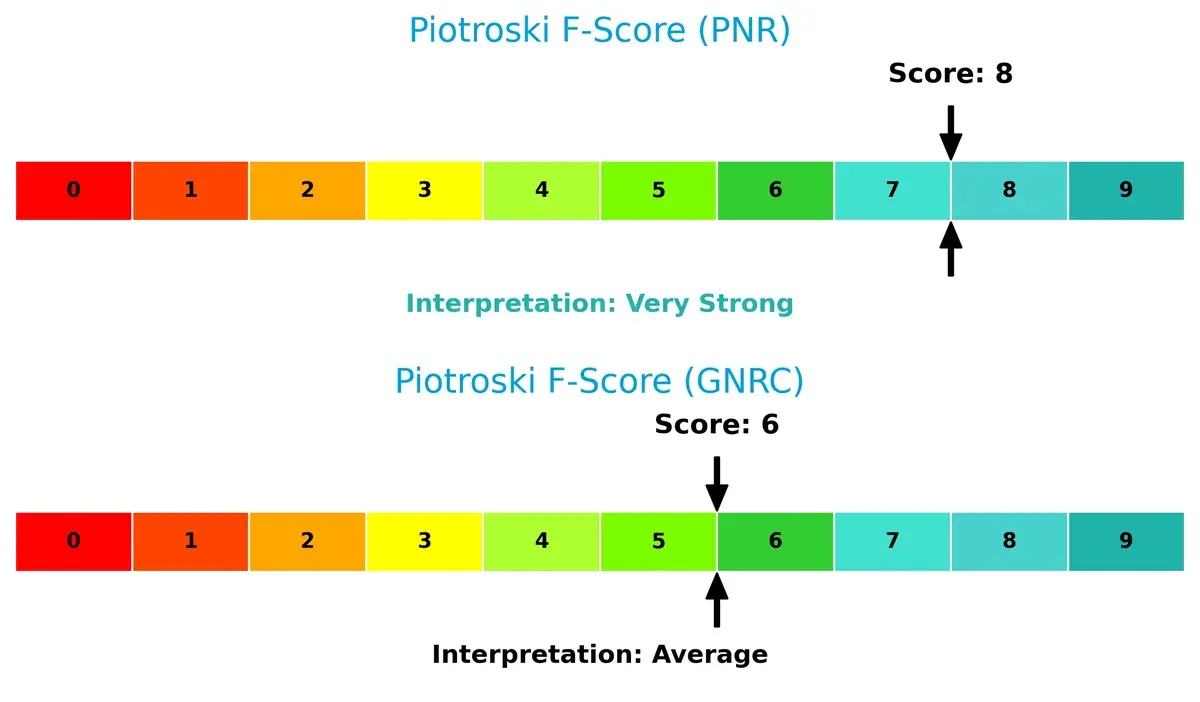

Financial Health: Quality of Operations

Pentair’s Piotroski F-Score of 8 signals robust financial health and efficient internal operations. Generac’s score of 6 points to average strength with potential red flags in financial consistency:

How are the two companies positioned?

This section dissects Pentair’s and Generac’s operational DNA by comparing revenue distribution and internal strengths and weaknesses. The goal is to confront their economic moats and reveal which business model offers the most resilient competitive advantage today.

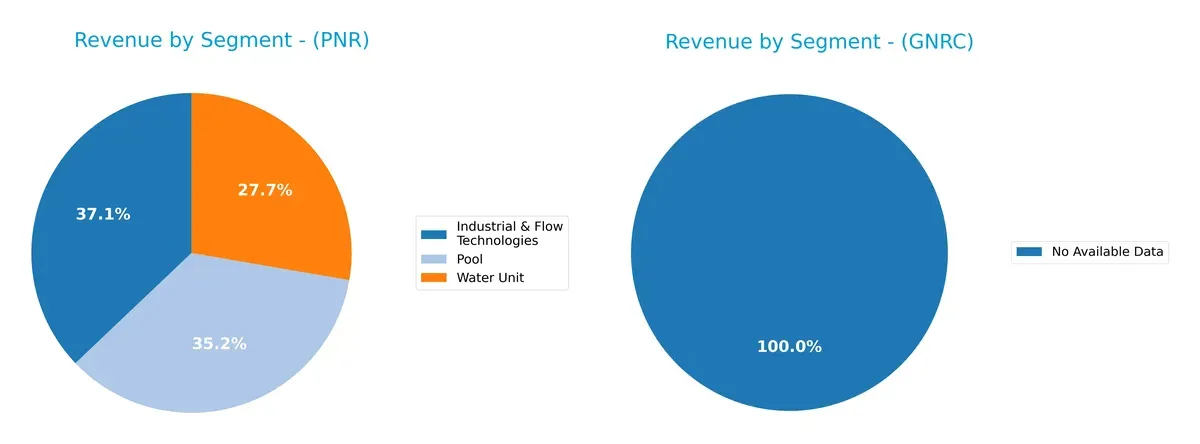

Revenue Segmentation: The Strategic Mix

The following visual comparison dissects how both firms diversify income streams and where their primary sector bets lie:

Pentair plc leans on a balanced portfolio with Industrial & Flow Technologies at $1.51B, Pool at $1.44B, and Water Unit at $1.13B. This diversification cushions it against sector shocks. Generac Holdings lacks available revenue segmentation data, preventing a direct comparison. Pentair’s spread signals ecosystem lock-in across water and industrial markets, reducing concentration risk and enhancing resilience amid market cycles.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Pentair plc and Generac Holdings Inc.:

Pentair plc Strengths

- Diversified revenue streams across Industrial, Pool, and Water segments

- Favorable profitability metrics with net margin 15.66% and ROE 16.9%

- Strong balance sheet with current ratio 1.61 and low debt-to-assets 23.86%

- Global presence including US, Western Europe, and developing countries

Generac Holdings Inc. Strengths

- Favorable price-to-book valuation indicating potential undervaluation

- Low debt levels with favorable debt-to-assets and debt-to-equity ratios

- No reported liabilities reflected in debt metrics

Pentair plc Weaknesses

- Relatively high price-to-earnings ratio at 26.14 may limit valuation upside

- Dividend yield low at 0.96%

- Quick ratio at 0.95 signals moderate short-term liquidity

- Asset turnover neutral, indicating average operational efficiency

Generac Holdings Inc. Weaknesses

- Weak profitability with net margin 3.79%, ROE and ROIC at zero

- Poor liquidity ratios at zero, signaling financial distress

- Negative interest coverage ratio

- Unfavorable asset turnover and no dividend yield

- Extremely high P/E ratio of 50.02 indicates overvaluation risk

Pentair’s strengths lie in diversified operations and solid profitability supported by a sound financial structure. Generac faces significant profitability and liquidity challenges despite a favorable capital structure. These factors crucially influence each company’s capacity to sustain growth and weather industry cycles.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat alone shields long-term profits from relentless competition erosion. Let’s dissect how these two firms defend their turf:

Pentair plc: Diversified Intangible Assets Moat

Pentair leverages a broad portfolio of water solutions and filtration brands, securing customer loyalty and stable margins. Its ROIC exceeds WACC by 3.6%, signaling value creation despite a slight decline. Expansion in developing markets could deepen this moat in 2026.

Generac Holdings Inc.: Product Innovation and Market Niche

Generac’s moat centers on power generation tech and remote monitoring systems. Unlike Pentair, its profitability struggles, with EBIT margin at zero and shrinking net margins. Innovation in clean energy storage offers upside but faces fierce industrial competition next year.

Moat Strength Showdown: Brand Diversification vs. Innovation Edge

Pentair’s tangible value creation and diverse product base form a wider, more resilient moat. Generac’s innovation focus is promising but currently undermined by weak margins and declining returns. Pentair stands better poised to protect market share in 2026.

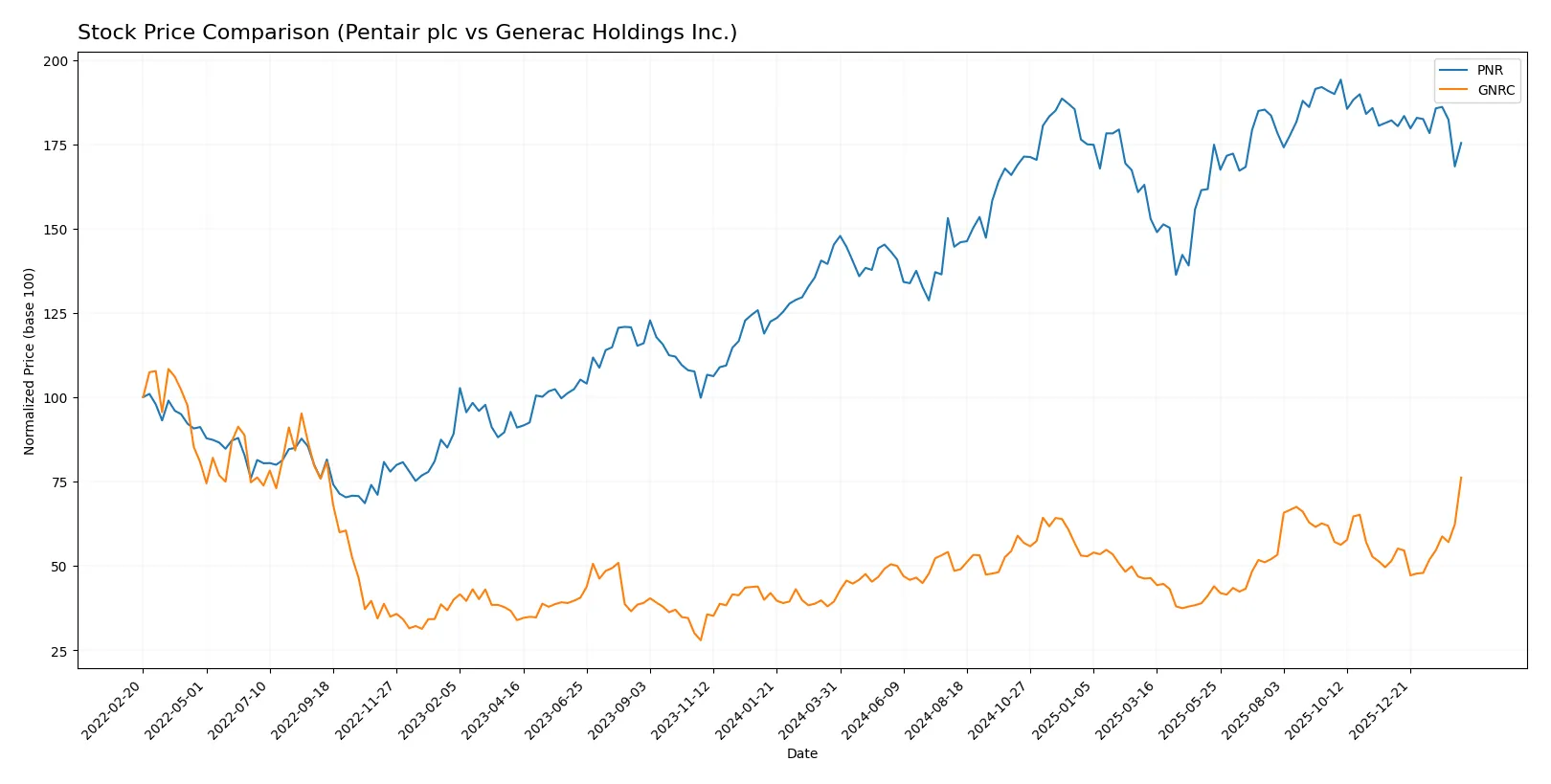

Which stock offers better returns?

Over the past year, Pentair plc and Generac Holdings Inc. displayed significant price movements, with Generac notably accelerating its gains while Pentair’s momentum slowed in recent months.

Trend Comparison

Pentair plc’s stock rose 20.76% over the past year, marking a bullish trend with decelerating momentum. The price ranged from $74.39 to $112.23, showing moderate volatility (10.6% std deviation). Recently, it slipped 3.68%, signaling a short-term bearish phase.

Generac Holdings Inc. surged 93.64% in the past year, reflecting a strong bullish trend with accelerating gains. Price fluctuated between $110.25 and $224.45, with high volatility (22.77% std deviation). Its recent 48.02% increase highlights robust upward momentum.

Generac outperformed Pentair by a wide margin, delivering the highest market returns and accelerating growth, while Pentair’s trend shows relative deceleration and recent weakness.

Target Prices

Analysts present a moderately bullish consensus for both Pentair plc and Generac Holdings Inc.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Pentair plc | 90 | 135 | 118.56 |

| Generac Holdings Inc. | 195 | 292 | 238.89 |

Pentair’s target consensus sits about 17% above its current 101.37 price, signaling upside potential. Generac’s target consensus exceeds its 224.45 share price by roughly 6%, reflecting cautious optimism.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Pentair plc Grades

The following table summarizes recent grades from major institutions for Pentair plc:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Citigroup | Maintain | Buy | 2026-02-04 |

| Oppenheimer | Maintain | Outperform | 2026-02-04 |

| JP Morgan | Maintain | Overweight | 2026-01-16 |

| Citigroup | Maintain | Buy | 2026-01-12 |

| BNP Paribas Exane | Downgrade | Underperform | 2026-01-07 |

| TD Cowen | Downgrade | Sell | 2026-01-05 |

| Jefferies | Upgrade | Buy | 2025-12-10 |

| Barclays | Downgrade | Equal Weight | 2025-12-04 |

| Oppenheimer | Maintain | Outperform | 2025-11-20 |

| RBC Capital | Maintain | Outperform | 2025-10-22 |

Generac Holdings Inc. Grades

Here is a summary of recent institutional grades for Generac Holdings Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Barclays | Maintain | Equal Weight | 2026-02-13 |

| Wells Fargo | Maintain | Overweight | 2026-02-12 |

| Guggenheim | Downgrade | Neutral | 2026-02-12 |

| Guggenheim | Maintain | Buy | 2026-02-10 |

| Barclays | Maintain | Equal Weight | 2026-01-20 |

| Canaccord Genuity | Maintain | Buy | 2026-01-13 |

| Baird | Upgrade | Outperform | 2026-01-09 |

| Citigroup | Upgrade | Buy | 2026-01-08 |

| B of A Securities | Maintain | Buy | 2026-01-07 |

| Wells Fargo | Upgrade | Overweight | 2025-12-19 |

Which company has the best grades?

Pentair plc generally holds higher and more consistent grades, including multiple “Buy” and “Outperform” ratings, despite some downgrades. Generac’s grades are mixed, with several “Equal Weight” and recent downgrades. Investors may perceive Pentair as the stronger option based on these institutional perspectives.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

Pentair plc

- Operates in diversified water and industrial machinery markets with established brands, facing moderate competition.

Generac Holdings Inc.

- Focused on power generation and energy storage, a highly competitive and cyclical sector with innovation pressure.

2. Capital Structure & Debt

Pentair plc

- Maintains a conservative debt-to-equity ratio (0.42), strong interest coverage (11.9), indicating solid financial stability.

Generac Holdings Inc.

- Lacks reported debt ratios and shows negative interest coverage, signaling potential financial risk and weaker capital structure.

3. Stock Volatility

Pentair plc

- Beta of 1.22 suggests moderate volatility, in line with industrial sector norms.

Generac Holdings Inc.

- Beta of 1.81 reflects high volatility, increasing investment risk in turbulent markets.

4. Regulatory & Legal

Pentair plc

- Global operations subject to environmental and safety regulations; compliance well-managed historically.

Generac Holdings Inc.

- Faces strict regulations on emissions and energy efficiency; ongoing legal scrutiny due to product safety recalls.

5. Supply Chain & Operations

Pentair plc

- Broad supplier base with resilient water and flow technology supply chains; some exposure to raw material costs.

Generac Holdings Inc.

- Supply chain complexity rising with energy storage components; vulnerable to semiconductor and raw material shortages.

6. ESG & Climate Transition

Pentair plc

- Strong focus on water sustainability and efficiency solutions, aligning well with climate transition trends.

Generac Holdings Inc.

- Transitioning toward clean energy products but currently reliant on fossil-fuel-based generators, risking ESG criticism.

7. Geopolitical Exposure

Pentair plc

- UK-based with diversified global presence; geopolitical risks include Brexit-related trade challenges.

Generac Holdings Inc.

- US-based with limited international footprint, less exposed but sensitive to domestic policy shifts and tariffs.

Which company shows a better risk-adjusted profile?

Pentair faces moderate market and geopolitical risks but benefits from a strong capital structure, stable operations, and solid ESG alignment. Generac confronts elevated financial risks, higher volatility, and supply chain vulnerabilities, despite growth in clean energy segments. The biggest risk for Pentair is geopolitical complexity affecting global trade. For Generac, financial instability and negative interest coverage dominate. Pentair’s Altman Z-Score and Piotroski Score confirm its safer risk profile. The notable divergence in interest coverage and debt metrics justifies concern over Generac’s financial resilience.

Final Verdict: Which stock to choose?

Pentair plc’s superpower lies in its consistent value creation through efficient capital use. Its slightly declining profitability signals a point of vigilance. This stock fits well in an income-focused or stable growth portfolio where resilience and quality cash flow matter most.

Generac Holdings commands a strategic moat in its recurring revenue model and strong innovation pipeline. While its financials show volatility and weaker margins, it offers higher growth potential with a safety buffer compared to pure high-risk plays. It suits a GARP investor seeking growth balanced with some margin of safety.

If you prioritize steady value creation and operational resilience, Pentair outshines as the compelling choice due to its strong ROIC above WACC and favorable financial health. However, if you seek accelerated growth with a tolerance for earnings volatility, Generac offers better upside potential and momentum despite its weaker profitability profile.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Pentair plc and Generac Holdings Inc. to enhance your investment decisions: