Home > Comparison > Technology > FICO vs SOUN

The strategic rivalry between Fair Isaac Corporation and SoundHound AI, Inc. shapes the future of the technology sector. Fair Isaac operates as a mature, capital-intensive software application leader specializing in analytics and decision management. SoundHound AI, a nimble innovator, focuses on voice AI platforms with a high-growth profile. This analysis will evaluate which company’s trajectory offers superior risk-adjusted returns for a diversified portfolio amid evolving tech demands.

Table of contents

Companies Overview

Fair Isaac Corporation and SoundHound AI, Inc. shape distinct niches within the software application market, each pushing innovation in decision analytics and voice AI.

Fair Isaac Corporation: Pioneer in Decision Analytics

Fair Isaac Corporation anchors its business as a leader in analytic software, generating revenue mainly through its Scores and Software segments. It empowers enterprises by automating decision-making across credit scoring, fraud detection, and customer engagement. In 2026, its strategic focus sharpens on expanding modular software solutions like the FICO Platform to enhance advanced analytics capabilities globally.

SoundHound AI, Inc.: Innovator in Voice AI

SoundHound AI, Inc. defines itself as a front-runner in conversational voice AI, monetizing through its Houndify platform. This platform equips businesses with voice recognition and natural language tools to create tailored voice assistants. In 2026, the company prioritizes scaling its voice AI offerings to deepen integration across diverse industry applications and enhance customer interaction quality.

Strategic Collision: Similarities & Divergences

Both firms thrive on cutting-edge software but diverge sharply in approach: Fair Isaac pursues a modular decision automation ecosystem, while SoundHound champions an open voice AI infrastructure. Their primary battleground lies in embedding AI solutions within customer workflows—financial services for Fair Isaac, and multi-industry voice interfaces for SoundHound. These distinct focuses define their investment profiles: one rooted in proven analytics, the other in emerging voice technology innovation.

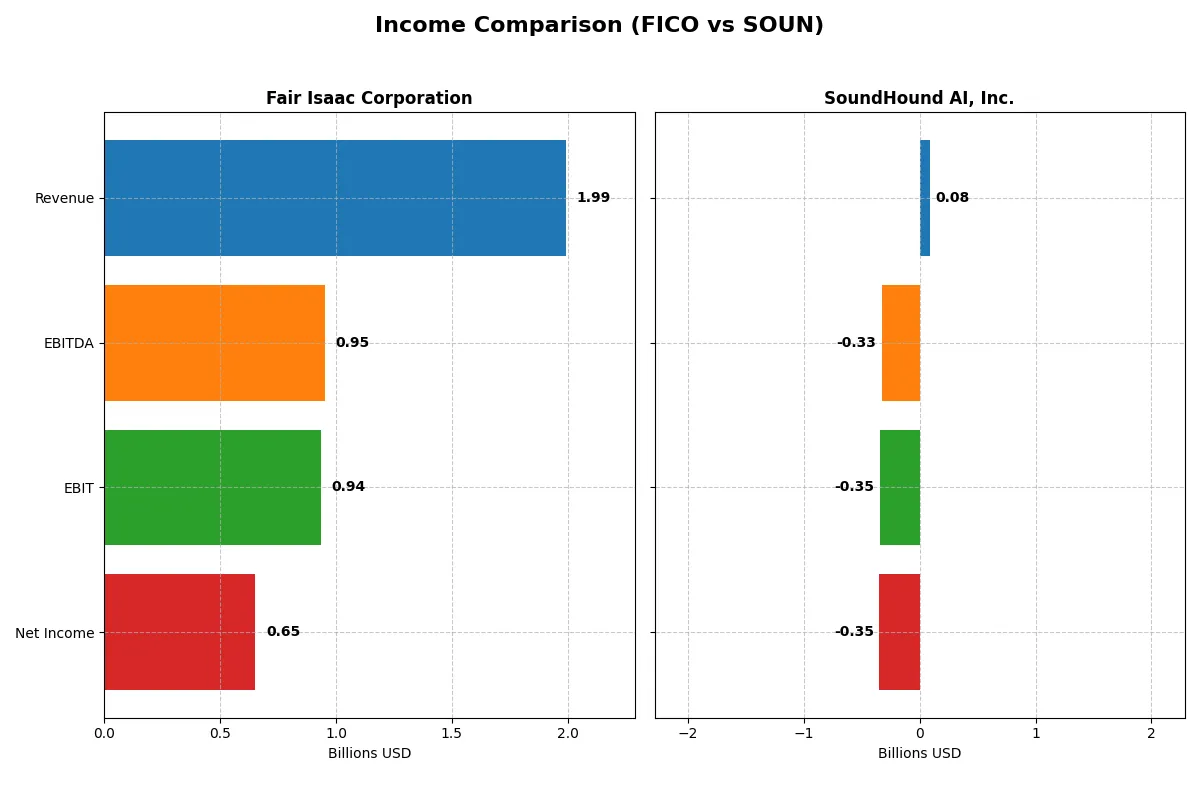

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Fair Isaac Corporation (FICO) | SoundHound AI, Inc. (SOUN) |

|---|---|---|

| Revenue | 1.99B | 85M |

| Cost of Revenue | 354M | 43M |

| Operating Expenses | 712M | 383M |

| Gross Profit | 1.64B | 41M |

| EBITDA | 951M | -329M |

| EBIT | 936M | -348M |

| Interest Expense | 134M | 12M |

| Net Income | 652M | -351M |

| EPS | 26.9 | -1.04 |

| Fiscal Year | 2025 | 2024 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company runs a more efficient and profitable corporate engine in recent years.

Fair Isaac Corporation (FICO) Analysis

FICO’s revenue surged from $1.32B in 2021 to $1.99B in 2025, driving net income growth from $392M to $652M. Its gross margin consistently exceeds 80%, while net margin reached a strong 32.75% in 2025. The company demonstrates impressive momentum with a 15.9% revenue growth and 29.8% EPS growth in the latest year.

SoundHound AI, Inc. (SOUN) Analysis

SOUN expanded revenue from $13M in 2020 to $85M in 2024, an 85% jump last year alone. However, it operates at a significant loss, with a negative net margin of -414% in 2024 and a $351M net loss. Despite healthy gross margins near 49%, high operating expenses erode profitability and weigh on earnings momentum.

Margin Strength vs. Growth Struggles

FICO clearly outperforms with robust profitability, high margins, and steady income growth, reflecting operational efficiency and capital allocation strength. SOUN’s rapid top-line growth contrasts with persistent negative earnings and margin pressure. Investors seeking solid profit generation find FICO’s profile far more attractive than SOUN’s high-risk growth trajectory.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Fair Isaac Corporation (FICO) | SoundHound AI, Inc. (SOUN) |

|---|---|---|

| ROE | -37.3% | -191.9% |

| ROIC | 52.96% | -68.13% |

| P/E | 55.6 | -19.1 |

| P/B | -20.8 | 36.8 |

| Current Ratio | 0.83 | 3.77 |

| Quick Ratio | 0.83 | 3.77 |

| D/E | -1.76 | 0.02 |

| Debt-to-Assets | 165.0% | 0.8% |

| Interest Coverage | 6.92 | -28.05 |

| Asset Turnover | 1.07 | 0.15 |

| Fixed Asset Turnover | 21.20 | 14.28 |

| Payout ratio | 0 | 0 |

| Dividend yield | 0 | 0 |

| Fiscal Year | 2025 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios serve as a company’s DNA, exposing hidden risks and highlighting operational strengths essential for investment insight.

Fair Isaac Corporation

Fair Isaac shows strong operational efficiency with a 32.75% net margin and a high 52.96% ROIC, signaling robust capital use. However, its -37.34% ROE and 0.83 current ratio raise concerns. The stock trades at a stretched 55.64 P/E multiple. It offers no dividends, focusing on reinvestment in R&D and growth.

SoundHound AI, Inc.

SoundHound displays weak profitability with a -414.06% net margin and -68.13% ROIC, reflecting operational challenges. Despite a favorable negative P/E due to losses, its elevated 36.76 P/B ratio suggests overvaluation. The company maintains a strong 3.77 current ratio but delivers no dividends, channeling cash into aggressive R&D development.

Premium Valuation vs. Operational Safety

Fair Isaac balances high valuation with operational strength, while SoundHound suffers from profitability and valuation concerns. Investors seeking operational safety may prefer Fair Isaac’s profile. Those chasing speculative growth face higher risk with SoundHound’s stretched metrics.

Which one offers the Superior Shareholder Reward?

I observe that Fair Isaac Corporation (FICO) pays no dividends but generates robust free cash flow of $31.8 per share in 2025. Its buyback activity is not explicit here but strong FCF supports potential future returns. SoundHound AI, Inc. (SOUN) also pays no dividends and posts negative free cash flow (-$0.32 per share), reflecting ongoing investment in growth. SOUN’s share buybacks appear nonexistent, highlighting a reinvestment strategy over shareholder distributions. FICO’s high margins and stable cash generation outperform SOUN’s prolonged losses and negative operating cash flow. Therefore, FICO offers a more sustainable distribution model and superior total return potential in 2026.

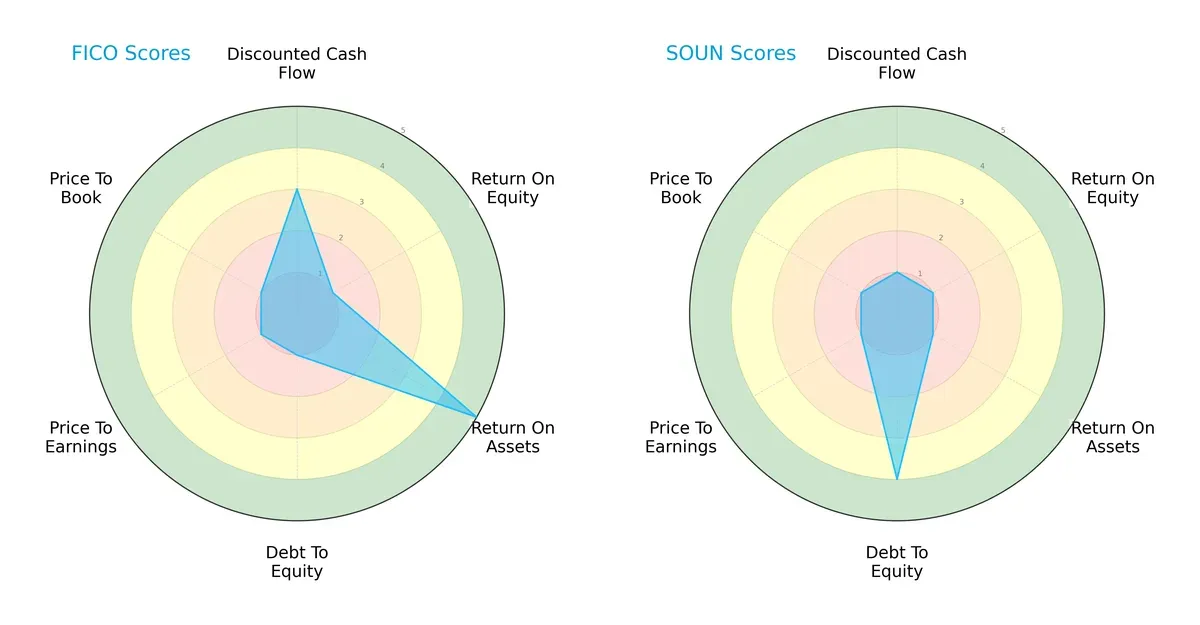

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of both firms, highlighting their core financial strengths and weaknesses:

Fair Isaac Corporation (FICO) demonstrates a more balanced profile with a moderate DCF score (3) and very favorable ROA (5), but weak ROE (1) and heavy debt load (debt/equity score 1). SoundHound AI (SOUN) relies heavily on a strong balance sheet (debt/equity score 4) but scores very low across profitability and valuation metrics. FICO’s asset efficiency contrasts sharply with SOUN’s fragile profitability and valuation outlook.

Bankruptcy Risk: Solvency Showdown

FICO’s Altman Z-Score of 12.2 far exceeds SOUN’s 4.8, signaling superior financial stability and a safer long-term survival position in this economic cycle:

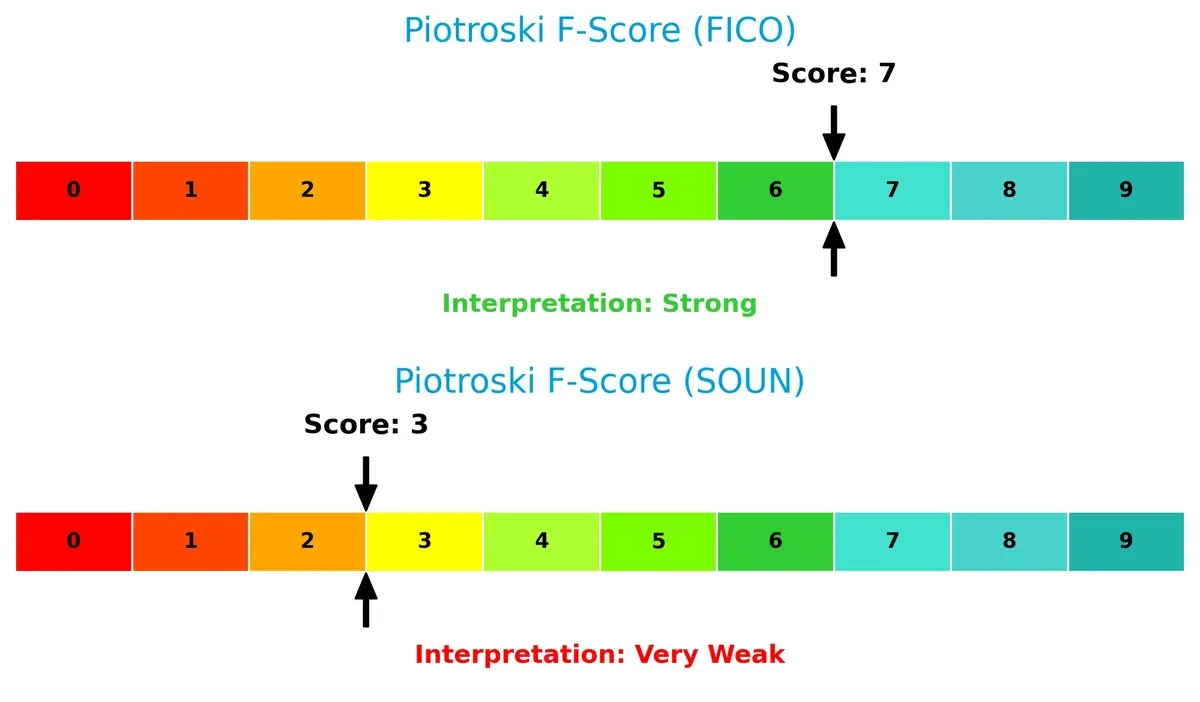

Financial Health: Quality of Operations

FICO’s Piotroski F-Score of 7 indicates strong financial health and operational quality, while SOUN’s 3 flags significant red flags in internal metrics and weaker fundamentals:

How are the two companies positioned?

This section dissects the operational DNA of Fair Isaac Corporation and SoundHound AI by comparing their revenue distribution and internal dynamics. The goal is to confront their economic moats and reveal which business model offers the most resilient, sustainable competitive advantage today.

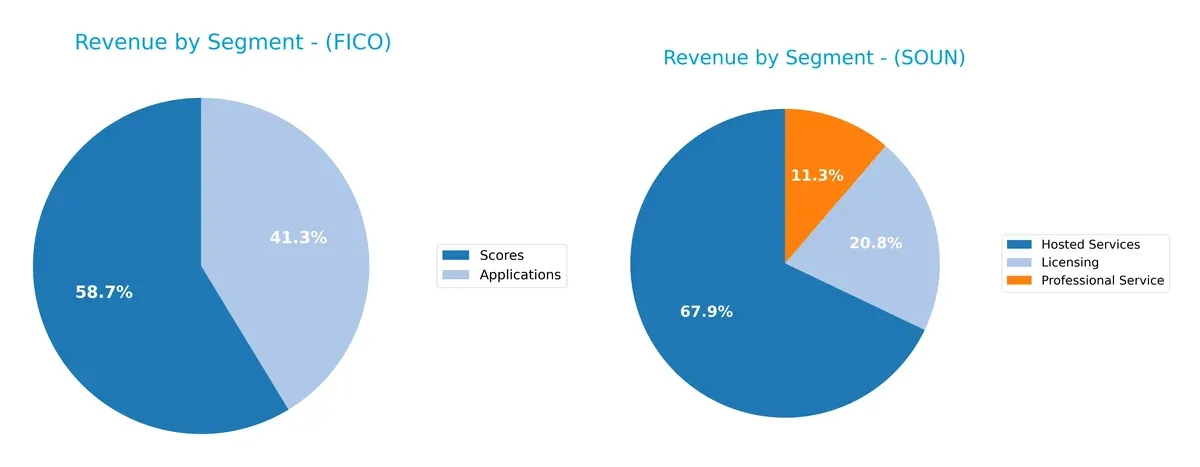

Revenue Segmentation: The Strategic Mix

The following visual comparison dissects how both firms diversify their income streams and where their primary sector bets lie:

Fair Isaac Corporation (FICO) anchors its revenue in two major segments: Scores at $1.17B and Applications at $822M in 2025. This split shows a balanced focus within its financial software ecosystem. In contrast, SoundHound AI, Inc. (SOUN) leans heavily on Hosted Services, which dwarfs Licensing and Professional Service revenues at $57M versus $18M and $9.5M respectively in 2024. FICO’s broader product mix reduces concentration risk, while SOUN’s reliance on Hosted Services signals a strategic bet on cloud infrastructure dominance but with higher exposure to single-segment volatility.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of Fair Isaac Corporation (FICO) and SoundHound AI, Inc. (SOUN):

FICO Strengths

- High net margin at 32.75%

- Strong ROIC of 52.96% surpassing WACC

- Favorable interest coverage at 7.01

- Robust asset and fixed asset turnover ratios

- Diverse revenue streams from applications and scores

- Significant global presence, especially Americas

SOUN Strengths

- Favorable quick ratio indicating liquidity

- Low debt-to-assets ratio at 0.79%

- Positive debt-to-equity ratio

- Favorable fixed asset turnover

- Diversified revenue from hosted services, licensing, and professional services

- Global revenue spread across several countries

FICO Weaknesses

- Negative ROE at -37.34% signals shareholder returns issues

- Unfavorable high debt-to-assets ratio at 164.6%

- Low current ratio of 0.83 raises liquidity concerns

- High P/E of 55.64 may indicate valuation risk

- No dividend yield impacts income investors

- Geographic revenue heavily concentrated in Americas

SOUN Weaknesses

- Negative net margin at -414.06% reflects unprofitability

- Negative ROE and ROIC indicate capital inefficiency

- Elevated WACC at 17.77% increases capital costs

- Negative interest coverage suggests financial distress

- Unfavorable asset turnover limits operational efficiency

- High P/B ratio of 36.76 may suggest overvaluation

FICO demonstrates strong profitability and efficient asset use but faces liquidity and leverage challenges. SOUN struggles with profitability and capital efficiency despite good liquidity and asset turnover. Both companies’ financial profiles highlight distinct strategic priorities and risks in their market approaches.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only true safeguard against long-term profit erosion from competitors. Let’s examine how these firms defend their turf:

Fair Isaac Corporation: Data-Driven Decision Moat

Fair Isaac’s moat stems from high switching costs and proprietary analytics embedded in financial services. Its 43.6% ROIC above WACC and stable 82% gross margin reveal durable profitability. Expansion into AI-enhanced decision platforms in 2026 promises moat deepening.

SoundHound AI, Inc.: Emerging Voice AI Platform

SoundHound’s moat relies on technological innovation and network effects in voice AI, contrasting Fair Isaac’s established legacy. Despite negative margins and value destruction, rapid revenue growth and improving ROIC indicate potential for a stronger competitive position ahead.

Moat Strength Face-Off: Established Analytics vs. Emerging AI Innovation

Fair Isaac commands a wider, more durable moat with consistent value creation and strong financials. SoundHound shows promise through innovation but still struggles to translate growth into profitability. Fair Isaac stands better poised to defend its market share long-term.

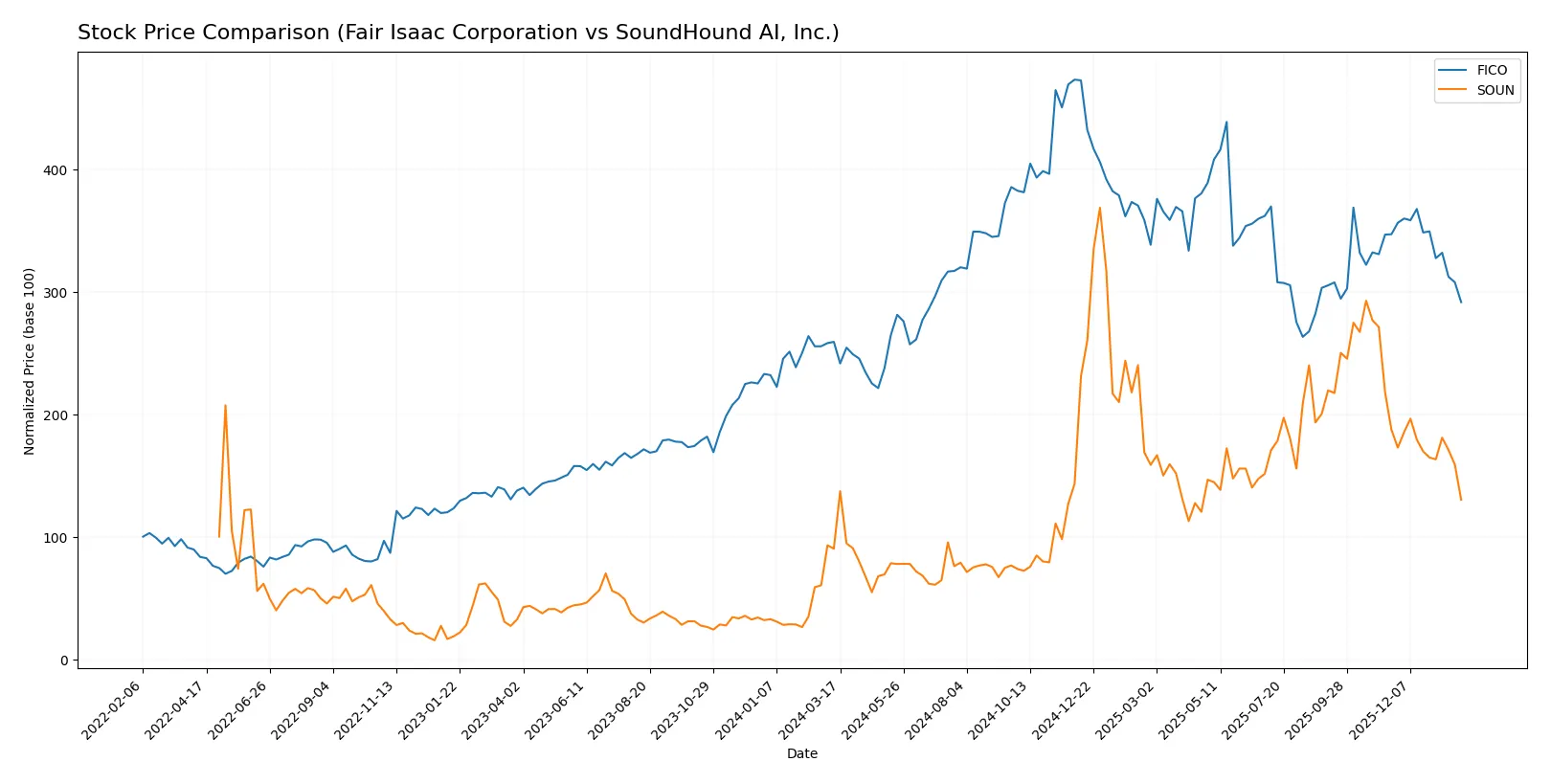

Which stock offers better returns?

The stock price charts reveal divergent trends over the past 12 months, with both companies exhibiting bullish momentum but recent downward shifts in trading dynamics.

Trend Comparison

Fair Isaac Corporation (FICO) shows a 12.51% price increase over the past year, indicating a bullish trend with decelerating momentum. The stock experienced a recent 15.98% decline between November 2025 and February 2026.

SoundHound AI, Inc. (SOUN) delivered a 44.37% gain over the same period, also bullish but with deceleration. Recently, it dropped 30.48%, reflecting a sharper short-term pullback than FICO.

SOUN outperformed FICO in overall market returns over the past year despite both stocks facing recent declines, with SOUN showing the highest price appreciation.

Target Prices

Analysts present a cautiously optimistic consensus for Fair Isaac Corporation and SoundHound AI, Inc.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Fair Isaac Corporation | 1640 | 2400 | 2115 |

| SoundHound AI, Inc. | 11 | 15 | 13.33 |

The target consensus suggests Fair Isaac’s shares could rise ~45% from $1463, reflecting strong confidence in its resilient software franchise. SoundHound’s targets imply a 57% upside from $8.46, signaling high growth expectations amid its AI voice platform innovation.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Fair Isaac Corporation Grades

The following table summarizes recent grades from reputable financial institutions for Fair Isaac Corporation.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Needham | Maintain | Buy | 2026-01-29 |

| Jefferies | Maintain | Buy | 2026-01-16 |

| Wells Fargo | Maintain | Overweight | 2026-01-14 |

| JP Morgan | Maintain | Neutral | 2025-11-06 |

| Baird | Maintain | Outperform | 2025-11-06 |

| Jefferies | Maintain | Buy | 2025-11-06 |

| BMO Capital | Maintain | Outperform | 2025-11-06 |

| Wells Fargo | Maintain | Overweight | 2025-10-14 |

| Barclays | Maintain | Overweight | 2025-10-02 |

| Needham | Maintain | Buy | 2025-10-02 |

SoundHound AI, Inc. Grades

This table presents recent grades from recognized financial analysts for SoundHound AI, Inc.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Piper Sandler | Maintain | Neutral | 2026-01-05 |

| Cantor Fitzgerald | Upgrade | Overweight | 2025-12-12 |

| DA Davidson | Maintain | Buy | 2025-11-18 |

| Piper Sandler | Maintain | Neutral | 2025-11-07 |

| HC Wainwright & Co. | Maintain | Buy | 2025-10-16 |

| HC Wainwright & Co. | Maintain | Buy | 2025-09-17 |

| Wedbush | Maintain | Outperform | 2025-09-11 |

| DA Davidson | Maintain | Buy | 2025-09-10 |

| Ladenburg Thalmann | Upgrade | Buy | 2025-08-11 |

| Wedbush | Maintain | Outperform | 2025-08-08 |

Which company has the best grades?

Fair Isaac Corporation consistently receives Buy, Outperform, and Overweight ratings from multiple firms, suggesting steady institutional confidence. SoundHound AI, Inc. shows a mix of Neutral and Buy ratings, with recent upgrades indicating improving sentiment. Investors may interpret Fair Isaac’s broader consensus as more established market support.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

Fair Isaac Corporation

- Established player in analytics with strong market presence but faces pressure from evolving AI competitors.

SoundHound AI, Inc.

- Emerging AI voice technology firm with high competition and uncertain market adoption rate.

2. Capital Structure & Debt

Fair Isaac Corporation

- High debt-to-assets ratio (165%) signals leverage risk despite favorable interest coverage.

SoundHound AI, Inc.

- Very low debt and strong debt-to-assets profile reduce financial risk but limited capital base.

3. Stock Volatility

Fair Isaac Corporation

- Beta of 1.29 indicates moderate volatility relative to the S&P 500 benchmark.

SoundHound AI, Inc.

- High beta of 2.88 demonstrates significant share price swings and elevated risk.

4. Regulatory & Legal

Fair Isaac Corporation

- Faces standard regulatory risks in data privacy and financial compliance across multiple regions.

SoundHound AI, Inc.

- Emerging regulatory environment for AI voice platforms creates potential compliance uncertainties.

5. Supply Chain & Operations

Fair Isaac Corporation

- Relies on robust software development and data management with established operational processes.

SoundHound AI, Inc.

- Smaller scale operations may face challenges scaling supply chain and tech infrastructure.

6. ESG & Climate Transition

Fair Isaac Corporation

- Moderate ESG risks typical of software firms; climate impact limited but requires transparency.

SoundHound AI, Inc.

- Early-stage company with limited ESG disclosures, raising investor caution on sustainability efforts.

7. Geopolitical Exposure

Fair Isaac Corporation

- Global footprint exposes it to geopolitical tensions affecting data flows and international regulations.

SoundHound AI, Inc.

- Primarily US-focused, minimizing geopolitical risk but less diversified internationally.

Which company shows a better risk-adjusted profile?

Fair Isaac’s most impactful risk is its high leverage, which could strain financial flexibility despite strong operational metrics. SoundHound’s core challenge lies in extreme stock volatility driven by market uncertainty and weak profitability. I see Fair Isaac as having a better risk-adjusted profile due to its stable Altman Z-Score of 12.2 and strong Piotroski score of 7, signaling financial safety and strength. Conversely, SoundHound’s weak Piotroski score of 3 and negative margins reveal significant execution risk. The stark difference in debt-to-assets ratios and volatility trends confirms my concern over SoundHound’s financial and market instability.

Final Verdict: Which stock to choose?

Fair Isaac Corporation’s superpower lies in its enduring economic moat, demonstrated by a robust ROIC well above its cost of capital. It efficiently converts invested capital into value, supported by strong cash flow generation. A point of vigilance remains its stretched liquidity position, which may pressure short-term resilience. This stock suits portfolios targeting steady, aggressive growth fueled by durable profitability.

SoundHound AI’s strategic moat centers on its innovation-driven growth and expanding market presence in AI voice technologies. It offers a higher safety buffer in liquidity compared to Fair Isaac but faces the challenge of ongoing value erosion and unprofitable operations. This makes it a fit for investors with a higher risk appetite pursuing GARP—growth at a reasonable price—hoping for a turnaround.

If you prioritize durable value creation and margin of safety, Fair Isaac outshines due to its proven capital efficiency and stable cash flows. However, if you seek aggressive growth exposure and can tolerate operational risks, SoundHound offers superior upside potential through innovation-led expansion. Both scenarios require cautious risk management given their distinct financial profiles.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Fair Isaac Corporation and SoundHound AI, Inc. to enhance your investment decisions: