Home > Comparison > Healthcare > ELV vs MOH

The strategic rivalry between Elevance Health Inc. and Molina Healthcare, Inc. shapes the healthcare plans sector’s future. Elevance operates as a vast, diversified health benefits provider serving over 100 million members. Molina focuses on government-sponsored programs, targeting low-income populations with a more specialized, community-based model. This analysis pits scale and diversification against focused niche expertise to determine which trajectory delivers superior risk-adjusted returns for a balanced portfolio.

Table of contents

Companies Overview

Elevance Health Inc. and Molina Healthcare, Inc. represent critical players in the US healthcare plans market, shaping access and coverage for millions.

Elevance Health Inc.: Comprehensive Health Benefits Leader

Elevance Health operates as a health benefits company serving 118M people. Its core revenue comes from a broad portfolio combining medical, digital, pharmacy, behavioral, and clinical care solutions. In 2026, it focuses strategically on integrating care journeys and leveraging digital platforms to enhance consumer support and health outcomes.

Molina Healthcare, Inc.: Targeted Medicaid and Medicare Provider

Molina Healthcare specializes in managed health care for low-income families under Medicaid and Medicare programs. It generates revenue mainly from government-sponsored healthcare plans in 18 states. The company’s 2026 strategy emphasizes expanding membership and optimizing services in Medicaid, Medicare, and state marketplace segments.

Strategic Collision: Similarities & Divergences

Both compete in the healthcare plans sector but differ sharply in scale and target demographics. Elevance embraces a broad, integrated ecosystem, while Molina targets underserved, government program beneficiaries. Their primary battleground lies in Medicaid and Medicare expansion. Elevance’s diversified model contrasts with Molina’s focused approach, reflecting distinct risk profiles and growth trajectories.

Income Statement Comparison

This table dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Elevance Health Inc. (ELV) | Molina Healthcare, Inc. (MOH) |

|---|---|---|

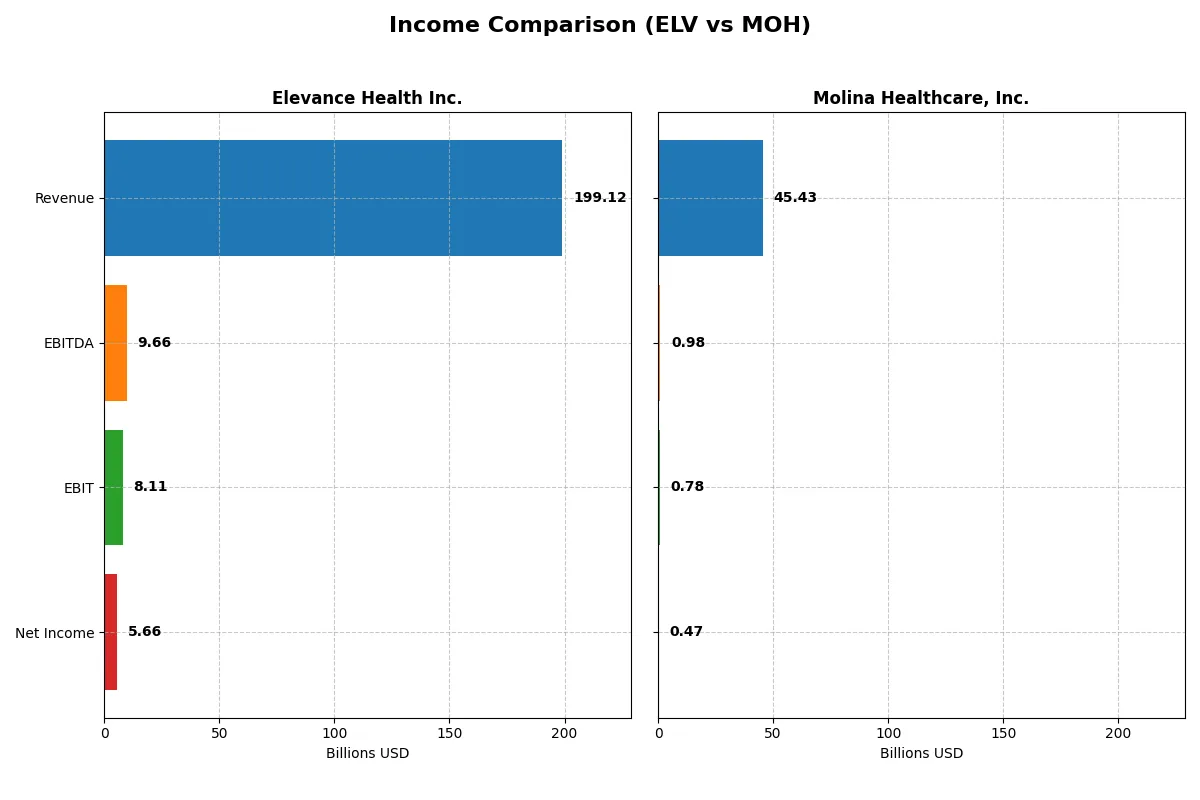

| Revenue | 199.1B | 45.4B |

| Cost of Revenue | 148.2B | 0 |

| Operating Expenses | 42.8B | 44.6B |

| Gross Profit | 50.9B | 0 |

| EBITDA | 9.7B | 976M |

| EBIT | 8.1B | 781M |

| Interest Expense | 1.4B | 192M |

| Net Income | 5.7B | 472M |

| EPS | 25.18 | 8.92 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals the true efficiency and profitability of Elevance Health Inc. and Molina Healthcare, Inc.’s business models.

Elevance Health Inc. Analysis

Elevance Health’s revenue climbs steadily, reaching $199B in 2025, a 12.6% one-year growth and 43.6% over five years. Net income, however, declines slightly to $5.66B in 2025, with net margin contracting to 2.84%. Gross margin remains healthy at 25.6%, but EBIT and net income margins show unfavorable trends, signaling margin pressure despite top-line growth.

Molina Healthcare, Inc. Analysis

Molina Healthcare grows revenue by 11.8% to $45.4B in 2025, a strong 63.6% rise since 2021. Yet, net income fell 28% over five years to $472M, with net margin at just 1.04%. Gross margin collapses to zero in 2025, indicating cost structure challenges. EBIT margin is low but stable, reflecting ongoing margin compression amid revenue gains.

Margin Strength vs. Revenue Expansion

Elevance Health sustains superior gross margins and larger absolute profits, despite recent margin erosion. Molina Healthcare posts faster revenue growth but suffers severe margin deterioration and net income declines. For investors prioritizing profitability and scale, Elevance’s profile offers more consistent margin power and earnings stability. Molina’s growth comes at a high cost to efficiency and bottom-line returns.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Elevance Health Inc. (ELV) | Molina Healthcare, Inc. (MOH) |

|---|---|---|

| ROE | 12.9% | 11.6% |

| ROIC | 7.2% | 7.6% |

| P/E | 13.7 | 19.4 |

| P/B | 1.77 | 2.26 |

| Current Ratio | 1.54 | 1.69 |

| Quick Ratio | 1.54 | 1.69 |

| D/E | 0.73 | 0.97 |

| Debt-to-Assets | 26.4% | 25.4% |

| Interest Coverage | 5.0 | 4.1 |

| Asset Turnover | 1.64 | 2.92 |

| Fixed Asset Turnover | 42.5 | 150.9 |

| Payout ratio | 27.0% | 0% |

| Dividend yield | 1.97% | 0% |

| Fiscal Year | 2025 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as a company’s DNA, exposing hidden risks and operational strengths crucial for investment decisions.

Elevance Health Inc.

Elevance shows a solid 12.9% ROE and a 7.22% ROIC, highlighting moderate profitability. Its P/E of 13.7 signals a fairly valued stock, supported by a 1.54 current ratio and low debt. The 1.97% dividend yield reflects steady shareholder returns without aggressive buybacks, balancing income with operational stability.

Molina Healthcare, Inc.

Molina’s 11.6% ROE and 7.64% ROIC indicate decent profitability, though margins remain thin at 1.04%. The P/E near 19.5 suggests a stretched valuation relative to peers. It maintains a strong liquidity position with a 1.69 current ratio but offers no dividend, implying reinvestment in growth or operations to enhance future returns.

Balanced Stability vs. Growth Stretch

Elevance combines reasonable valuation with solid profitability and shareholder dividends, presenting a balanced risk profile. Molina trades at a premium with no dividends, emphasizing growth but carrying higher valuation risk. Investors seeking steady income and value may prefer Elevance, while those favoring growth might lean toward Molina.

Which one offers the Superior Shareholder Reward?

Elevance Health (ELV) delivers a balanced shareholder reward through a 1.97% dividend yield and a 27% payout ratio, supported by strong free cash flow (FCF) coverage of 74%. Its consistent dividend growth and moderate buybacks complement sustainable value creation. Molina Healthcare (MOH) pays no dividends, focusing entirely on reinvestment and occasional buybacks. MOH’s negative free cash flow and weak operating cash flow ratios raise sustainability concerns. I see ELV’s disciplined distribution and cash flow strength as a more attractive and reliable total return profile for 2026 investors.

Comparative Score Analysis: The Strategic Profile

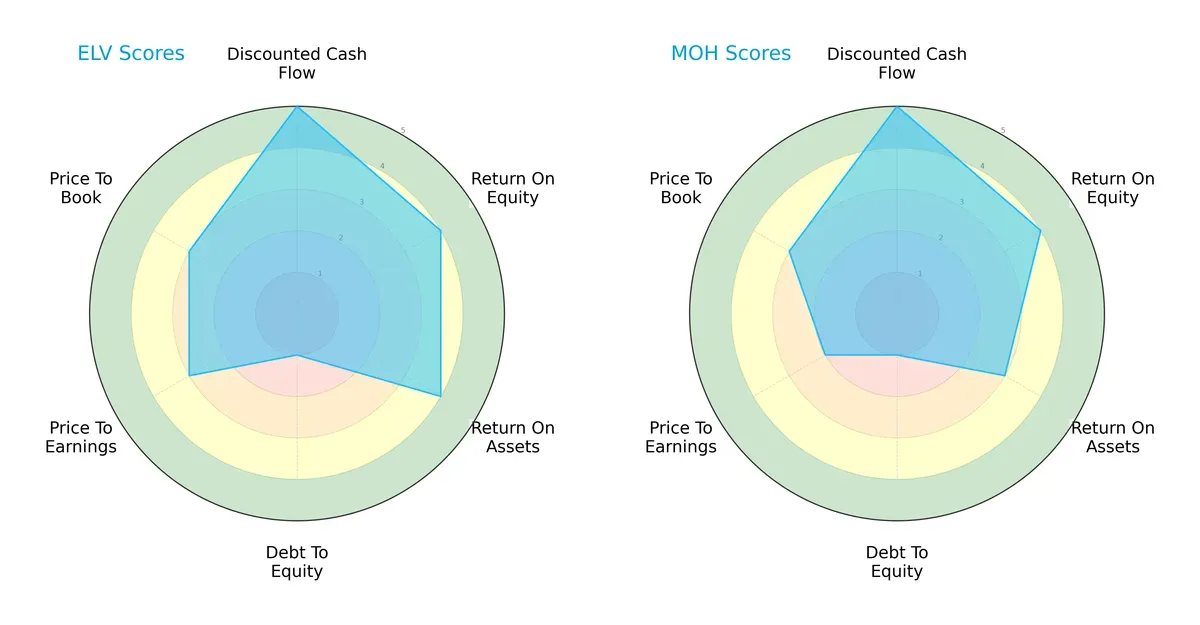

The radar chart reveals the fundamental DNA and trade-offs of Elevance Health Inc. and Molina Healthcare, Inc.:

Elevance Health shows a more balanced profile with strong DCF (5), ROE (4), and ROA (4) scores, but suffers from a very unfavorable debt-to-equity score (1). Molina Healthcare matches Elevance’s DCF and ROE but lags in ROA (3) and valuation metrics, especially P/E (2). Molina relies more on its DCF strength, while Elevance’s operational efficiency stands out.

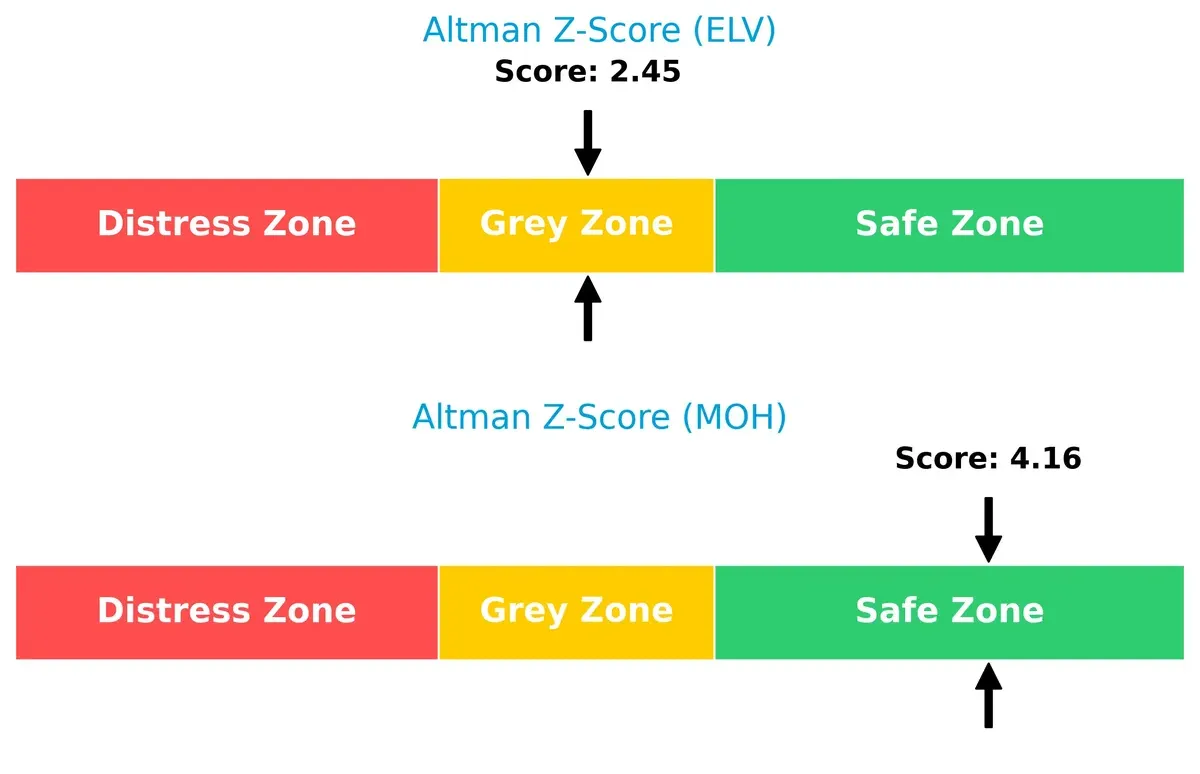

Bankruptcy Risk: Solvency Showdown

Molina Healthcare’s Altman Z-Score of 4.16 places it firmly in the safe zone, indicating robust solvency. Elevance’s 2.45 sits in the grey zone, suggesting moderate bankruptcy risk in this cycle:

Financial Health: Quality of Operations

Both firms share an identical Piotroski F-Score of 5, signaling average financial health. Neither shows critical red flags, but the middling scores caution against complacency:

How are the two companies positioned?

This section dissects the operational DNA of Elevance Health and Molina Healthcare by comparing revenue distribution and internal dynamics. The goal is to confront their economic moats to identify which model offers the most resilient competitive advantage today.

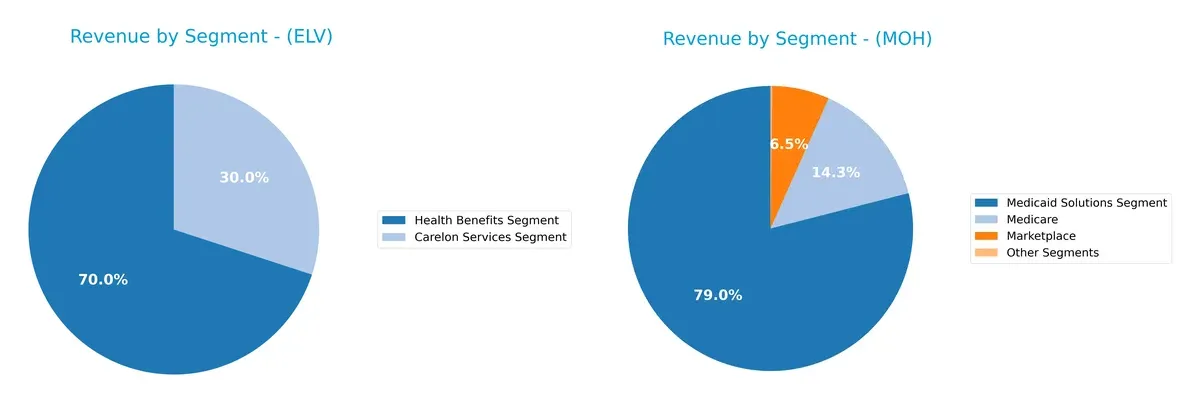

Revenue Segmentation: The Strategic Mix

This comparison dissects how Elevance Health Inc. and Molina Healthcare, Inc. diversify their income streams and reveals their primary sector bets:

Elevance Health anchors its revenue with a dominant Health Benefits Segment at $167B in 2025, complemented by $71.7B from Carelon Services. This mix shows a strategic balance between insurance and services, reducing concentration risk. Molina Healthcare pivots on Medicaid Solutions, generating $30.6B in 2024, with smaller contributions from Marketplace and Medicare. Molina’s narrower focus signals higher dependency but stronger specialization in Medicaid.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of Elevance Health Inc. and Molina Healthcare, Inc.:

Elevance Health Inc. Strengths

- Diverse revenue streams from Carelon Services and Health Benefits segments

- Favorable asset and fixed asset turnover ratios indicating operational efficiency

- Strong interest coverage ratio supports debt servicing

- Favorable WACC and PE ratio show efficient capital cost and valuation

Molina Healthcare, Inc. Strengths

- Favorable asset and fixed asset turnover suggest strong operational performance

- Strong current and quick ratios reflect liquidity strength

- Favorable debt to assets ratio indicates balanced leverage

- Neutral ROIC above WACC implies value creation

Elevance Health Inc. Weaknesses

- Unfavorable low net margin points to profitability pressure

- Neutral ROE and ROIC signify moderate returns

- Neutral debt-to-equity ratio suggests average leverage position

- Neutral PB ratio indicates limited market premium

Molina Healthcare, Inc. Weaknesses

- Unfavorable net margin and zero dividend yield highlight profitability and shareholder return concerns

- Neutral interest coverage ratio poses moderate risk in debt servicing

- Higher PE ratio may imply valuation risk

- Neutral debt-to-equity ratio reflects moderate leverage

Elevance Health’s strengths lie in its diversified revenue and operational efficiency, but its low net margin signals profitability challenges. Molina Healthcare shows operational strengths and liquidity but faces profitability and shareholder yield weaknesses. Both companies exhibit moderate leverage and returns, influencing their strategic financial management.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only reliable shield protecting long-term profits from relentless competitive erosion. Let’s dissect two healthcare players’ moats:

Elevance Health Inc. (ELV): Intangible Assets Moat

Elevance leverages its vast network and brand reputation, driving stable margins and a high ROIC relative to peers. However, its slightly declining profitability signals rising competitive pressures in 2026.

Molina Healthcare, Inc. (MOH): Cost Advantage Moat

Molina exploits cost-efficient Medicaid and Medicare operations, maintaining positive value creation despite margin compression. Its deeper ROIC cushion better resists market disruptions but faces sustainability risks.

Intangible Assets vs. Cost Advantage: Who Defends Better in Healthcare?

Molina’s cost advantage offers a wider moat, delivering consistent value creation despite margin challenges. Elevance’s intangible moat is narrower, with profits under more pressure. Molina stands better poised to defend its market share through operational efficiency in 2026.

Which stock offers better returns?

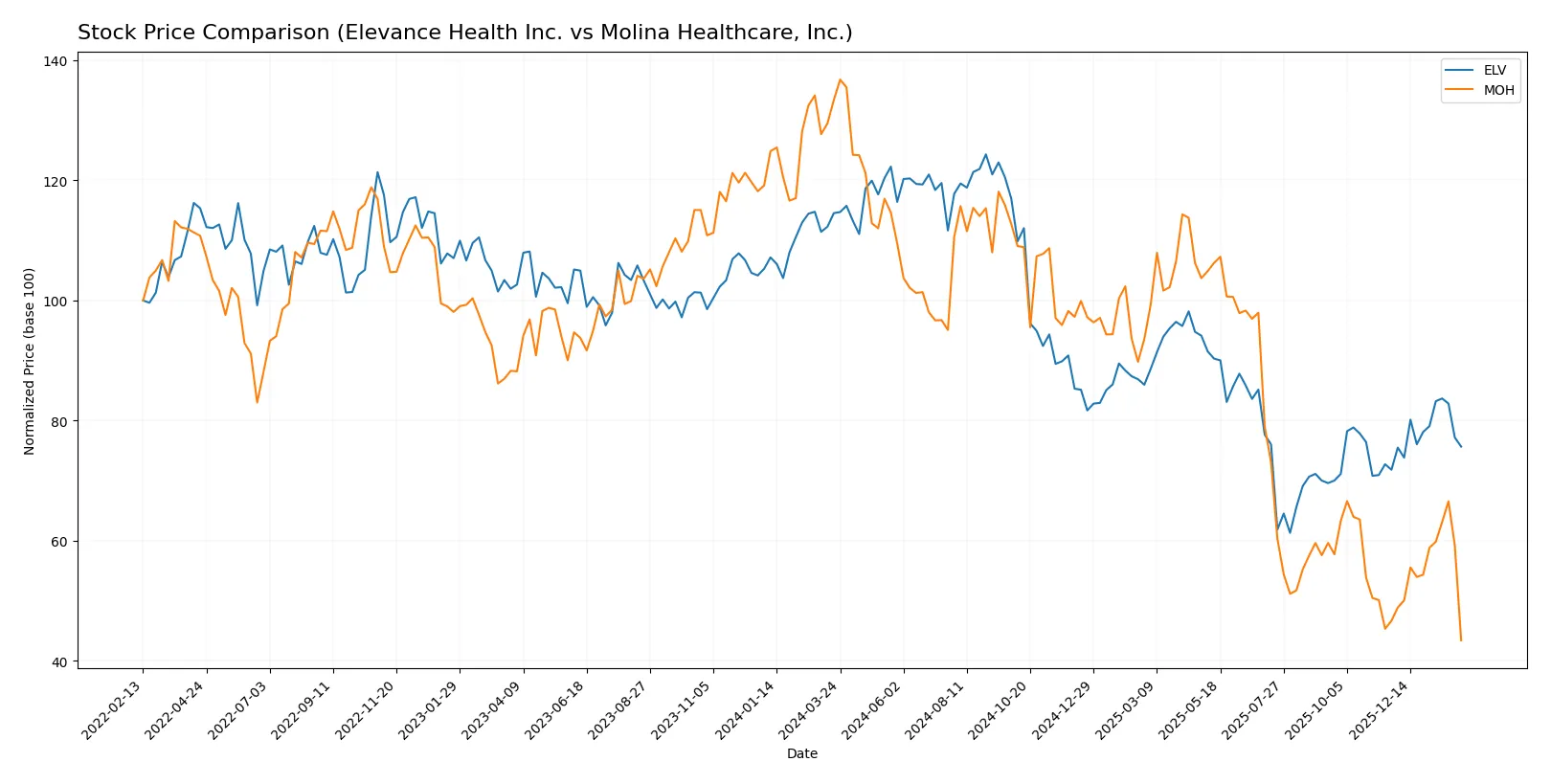

Stock price movements over the past year reveal contrasting dynamics between Elevance Health Inc. and Molina Healthcare, Inc., highlighting divergent recovery patterns and trading volumes.

Trend Comparison

Elevance Health Inc. shows a bearish trend over the past 12 months with a -33.93% price decline and accelerating downward momentum. Its price ranged from 556.89 at the high to 274.66 at the low, signaling strong volatility.

Molina Healthcare, Inc. experienced a more severe bearish trend, dropping -67.43% over the same period with accelerating decline. The stock fluctuated between a high of 414.72 and a low of 131.72, reflecting high volatility as well.

Comparing the two, Elevance Health outperformed Molina Healthcare, delivering a smaller loss and showing a recent positive trend, while Molina’s decline remains more pronounced and sustained.

Target Prices

Analysts provide a cautiously optimistic outlook for Elevance Health Inc. and Molina Healthcare, Inc.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Elevance Health Inc. | 332 | 425 | 387.14 |

| Molina Healthcare, Inc. | 158 | 224 | 181 |

Elevance Health’s consensus target of 387.14 suggests a 14% upside from the current 339 price. Molina Healthcare’s 181 target implies a 37% potential gain despite recent volatility.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

The following section compares recent institutional grades for Elevance Health Inc. and Molina Healthcare, Inc.:

Elevance Health Inc. Grades

This table shows the latest grades from notable financial institutions for Elevance Health Inc.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| JP Morgan | Maintain | Overweight | 2026-02-02 |

| Truist Securities | Maintain | Buy | 2026-02-02 |

| Barclays | Maintain | Overweight | 2026-01-30 |

| Wells Fargo | Maintain | Overweight | 2026-01-30 |

| Guggenheim | Maintain | Buy | 2026-01-29 |

| Guggenheim | Maintain | Buy | 2026-01-22 |

| Wolfe Research | Upgrade | Outperform | 2026-01-08 |

| Wells Fargo | Maintain | Overweight | 2026-01-07 |

| Barclays | Maintain | Overweight | 2026-01-05 |

| Deutsche Bank | Downgrade | Hold | 2025-12-19 |

Molina Healthcare, Inc. Grades

This table presents recent grades from credible institutions for Molina Healthcare, Inc.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Wells Fargo | Maintain | Overweight | 2026-01-07 |

| Barclays | Maintain | Underweight | 2026-01-05 |

| Wells Fargo | Maintain | Overweight | 2025-11-12 |

| UBS | Maintain | Neutral | 2025-10-24 |

| Barclays | Downgrade | Underweight | 2025-10-24 |

| Cantor Fitzgerald | Maintain | Neutral | 2025-10-24 |

| Goldman Sachs | Maintain | Neutral | 2025-10-24 |

| Morgan Stanley | Maintain | Equal Weight | 2025-10-14 |

| Wells Fargo | Maintain | Overweight | 2025-10-07 |

| Bernstein | Maintain | Outperform | 2025-09-05 |

Which company has the best grades?

Elevance Health consistently receives strong buy and overweight ratings, with one recent upgrade. Molina Healthcare shows mixed grades, including several underweights and neutrals. Investors might view Elevance’s consensus as more favorable, reflecting higher confidence from analysts.

Risks specific to each company

In 2026’s complex healthcare market, these categories identify the critical pressure points and systemic threats facing both Elevance Health Inc. and Molina Healthcare, Inc.:

1. Market & Competition

Elevance Health Inc.

- Large scale and diversified portfolio support strong market position but intensifying competition pressures margins.

Molina Healthcare, Inc.

- Smaller scale with niche focus on low-income programs faces intense competition and pricing pressure.

2. Capital Structure & Debt

Elevance Health Inc.

- Moderate debt-to-equity (0.73) and strong interest coverage (5.79) indicate controlled leverage risk.

Molina Healthcare, Inc.

- Higher debt-to-equity (0.97) and weaker interest coverage (4.07) suggest elevated financial risk.

3. Stock Volatility

Elevance Health Inc.

- Beta of 0.503 shows relatively low volatility, offering stability in turbulent markets.

Molina Healthcare, Inc.

- Similar low beta (0.493) but recent 25.5% price drop signals vulnerability to market shocks.

4. Regulatory & Legal

Elevance Health Inc.

- Broad regulatory exposure given size; well-equipped to manage compliance but risks persist.

Molina Healthcare, Inc.

- Regulatory dependence on Medicaid/Medicare programs in 18 states heightens risk of policy shifts.

5. Supply Chain & Operations

Elevance Health Inc.

- Extensive operational scale with 104K employees supports resilience but complexity can cause inefficiencies.

Molina Healthcare, Inc.

- Smaller workforce (18K) improves agility but limits scalability and operational flexibility.

6. ESG & Climate Transition

Elevance Health Inc.

- Emerging ESG initiatives align with investor expectations but full impact on costs remains uncertain.

Molina Healthcare, Inc.

- ESG efforts less publicized, potentially risking reputational and compliance headwinds.

7. Geopolitical Exposure

Elevance Health Inc.

- Primarily US-focused, geopolitical risks are moderate but healthcare policy shifts remain a concern.

Molina Healthcare, Inc.

- Also US-focused with concentrated geographic footprint, increasing vulnerability to state-level political changes.

Which company shows a better risk-adjusted profile?

Elevance Health faces margin pressure but boasts superior capital structure and operational scale, providing a more stable risk profile. Molina’s acute regulatory dependence and recent sharp share price decline expose it to higher volatility and financial risk. Elevated debt and weaker interest coverage at Molina heighten its vulnerability. Elevance’s diversified services and strong interest coverage offer a buffer against cyclical shocks. Molina’s safe-zone Altman Z-score contrasts with Elevance’s grey zone, but overall financial strength and market position favor Elevance in 2026 risk-adjusted terms.

Final Verdict: Which stock to choose?

Elevance Health Inc. (ELV) impresses with its robust operational efficiency and strong asset turnover, reflecting its ability to generate sales from invested capital. Its main point of vigilance is the declining profitability trend, which could pressure future returns. ELV suits investors targeting aggressive growth with a tolerance for cyclical earnings swings.

Molina Healthcare, Inc. (MOH) leverages a strategic moat rooted in efficient capital use and a solid current ratio, offering a comparatively safer financial profile. While its profitability is also under pressure, MOH provides a more stable foundation for investors favoring growth at a reasonable price, balancing risk and potential reward.

If you prioritize operational efficiency and aggressive growth potential, ELV is the compelling choice due to its superior asset utilization and sales generation. However, if you seek better financial stability and a moderate risk profile, MOH offers better stability and a clearer path to value creation despite its declining profit margins.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Elevance Health Inc. and Molina Healthcare, Inc. to enhance your investment decisions: