In the competitive landscape of discount retail, Walmart Inc. and Dollar General Corporation stand out as key players shaping the industry’s future. Both giants serve cost-conscious consumers but adopt distinct strategies in market reach and innovation. By comparing their business models, financial health, and growth prospects, I will help you determine which stock may be a more compelling addition to your investment portfolio. Let’s explore which company offers the best opportunity for savvy investors.

Table of contents

Companies Overview

I will begin the comparison between Walmart Inc. and Dollar General Corporation by providing an overview of these two companies and their main differences.

Walmart Overview

Walmart Inc. operates globally in retail, wholesale, and eCommerce sectors through three main segments: Walmart U.S., Walmart International, and Sam’s Club. The company runs various store formats, including supercenters and warehouse clubs, offering a wide range of products from groceries to electronics. With a market cap near $940B, Walmart is a leader in discount stores and consumer defensive sectors, emphasizing convenience and broad product selection worldwide.

Dollar General Overview

Dollar General Corporation is a discount retailer focused primarily on the southern, southwestern, Midwestern, and eastern US markets. It operates over 18,000 stores, offering consumables, seasonal items, apparel, and home products tailored for everyday needs. With a market cap around $33B, Dollar General serves mainly regional customers with a dense store network, targeting convenience and value in smaller store formats within the consumer defensive sector.

Key similarities and differences

Both Walmart and Dollar General operate in the discount store industry within the consumer defensive sector and provide essential goods including groceries and household products. However, Walmart has a significant global presence with diverse store formats and an extensive eCommerce platform, while Dollar General focuses on regional penetration in the US with smaller stores. Walmart’s scale and product range are considerably larger, whereas Dollar General emphasizes accessibility and convenience through its dense store footprint.

Income Statement Comparison

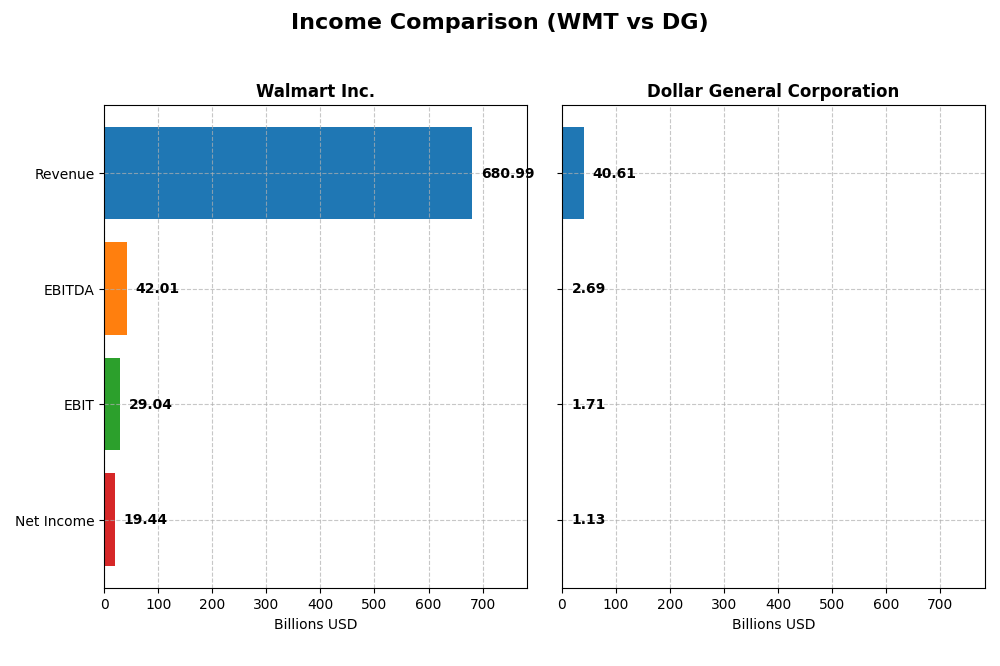

The following table presents a side-by-side comparison of the most recent fiscal year income statement metrics for Walmart Inc. and Dollar General Corporation.

| Metric | Walmart Inc. (WMT) | Dollar General Corporation (DG) |

|---|---|---|

| Market Cap | 940.6B | 32.8B |

| Revenue | 681B | 40.6B |

| EBITDA | 42.0B | 2.7B |

| EBIT | 29.0B | 1.7B |

| Net Income | 19.4B | 1.13B |

| EPS | 2.42 | 5.12 |

| Fiscal Year | 2025 | 2024 |

Income Statement Interpretations

Walmart Inc.

Walmart showed steady revenue growth from $559B in 2021 to $681B in 2025, with net income rising from $13.5B to $19.4B. Gross margin improved favorably to 24.85%, while EBIT and net margins remained stable around 4.26% and 2.85%. The 2025 year saw a 5.07% revenue increase and strong net margin growth of 19.26%, indicating margin expansion and earnings acceleration.

Dollar General Corporation

Dollar General’s revenue increased modestly from $33.7B in 2020 to $40.6B in 2024, but net income declined sharply from $2.7B to $1.1B. Gross margin held favorably at 29.59%, though EBIT and net margins were neutral around 4.22% and 2.77%. The latest year reflected a 4.96% revenue rise but significant declines in EBIT (-29.93%) and net margin (-35.47%), signaling weakening profitability.

Which one has the stronger fundamentals?

Walmart displays stronger fundamentals with consistent revenue and net income growth, improved margins, and a largely favorable income statement evaluation. Dollar General, despite steady revenue gains and good gross margin, suffers from declining net income and margins over the period. Walmart’s favorable margin expansion and earnings growth contrast with Dollar General’s deteriorating profitability metrics.

Financial Ratios Comparison

This table presents a side-by-side comparison of key financial ratios for Walmart Inc. and Dollar General Corporation based on their most recent fiscal year data.

| Ratios | Walmart Inc. (2025) | Dollar General Corp. (2024) |

|---|---|---|

| ROE | 21.36% | 15.18% |

| ROIC | 13.06% | 5.10% |

| P/E | 40.61 | 13.89 |

| P/B | 8.67 | 2.11 |

| Current Ratio | 0.82 | 1.19 |

| Quick Ratio | 0.24 | 0.21 |

| D/E (Debt-to-Equity) | 0.66 | 2.36 |

| Debt-to-Assets | 23.05% | 56.09% |

| Interest Coverage | 10.76 | 6.25 |

| Asset Turnover | 2.61 | 1.30 |

| Fixed Asset Turnover | 4.87 | 2.34 |

| Payout Ratio | 34.41% | 46.12% |

| Dividend Yield | 0.85% | 3.32% |

Interpretation of the Ratios

Walmart Inc.

Walmart shows a mixed ratio profile with favorable returns on equity (21.36%) and invested capital (13.06%), but weak net margin (2.85%) and liquidity ratios (current ratio 0.82, quick ratio 0.24). Debt metrics are generally positive with a favorable debt to assets of 23.05%. Dividend yield is low at 0.85%, reflecting a modest payout and limited shareholder returns.

Dollar General Corporation

Dollar General also presents mixed results, with a favorable return on equity (15.18%) and interest coverage (6.25), but a neutral return on invested capital (5.1%) and unfavorable debt to equity (2.36) and debt to assets (56.09%). Its dividend yield is higher at 3.32%, indicating stronger shareholder returns supported by a reasonable payout ratio.

Which one has the best ratios?

Both companies have a slightly favorable global ratios opinion, but Walmart excels in return metrics and debt management, while Dollar General offers a higher dividend yield and better price-to-earnings valuation. Walmart’s liquidity concerns contrast with Dollar General’s higher leverage, making the comparison dependent on investor priorities.

Strategic Positioning

This section compares the strategic positioning of Walmart Inc. and Dollar General Corporation, focusing on Market position, Key segments, and exposure to disruption:

Walmart Inc.

- Leading global discount retailer with vast scale and competitive pressure from multi-format stores worldwide.

- Diverse revenue streams from Walmart U.S., Walmart International, and Sam’s Club segments driving business.

- Operates extensive eCommerce platforms and digital payment services, facing disruption from digital retail trends.

Dollar General Corporation

- Regional discount retailer focused on 18,190 stores across 47 US states, with lower competitive pressure.

- Concentrated on consumables, apparel, home products, and seasonal categories within the US market.

- Primarily physical stores with limited digital disruption exposure compared to Walmart’s broad tech integration.

Walmart Inc. vs Dollar General Corporation Positioning

Walmart’s diversified global operations and multi-segment revenue contrast with Dollar General’s concentrated US discount store model. Walmart benefits from scale and eCommerce, while Dollar General has a focused footprint with less digital integration, influencing competitive dynamics.

Which has the best competitive advantage?

Walmart demonstrates a very favorable moat with growing ROIC and value creation, indicating durable competitive advantage. Dollar General shows slightly unfavorable moat status with declining ROIC, reflecting challenges in sustaining profitability and competitive edge.

Stock Comparison

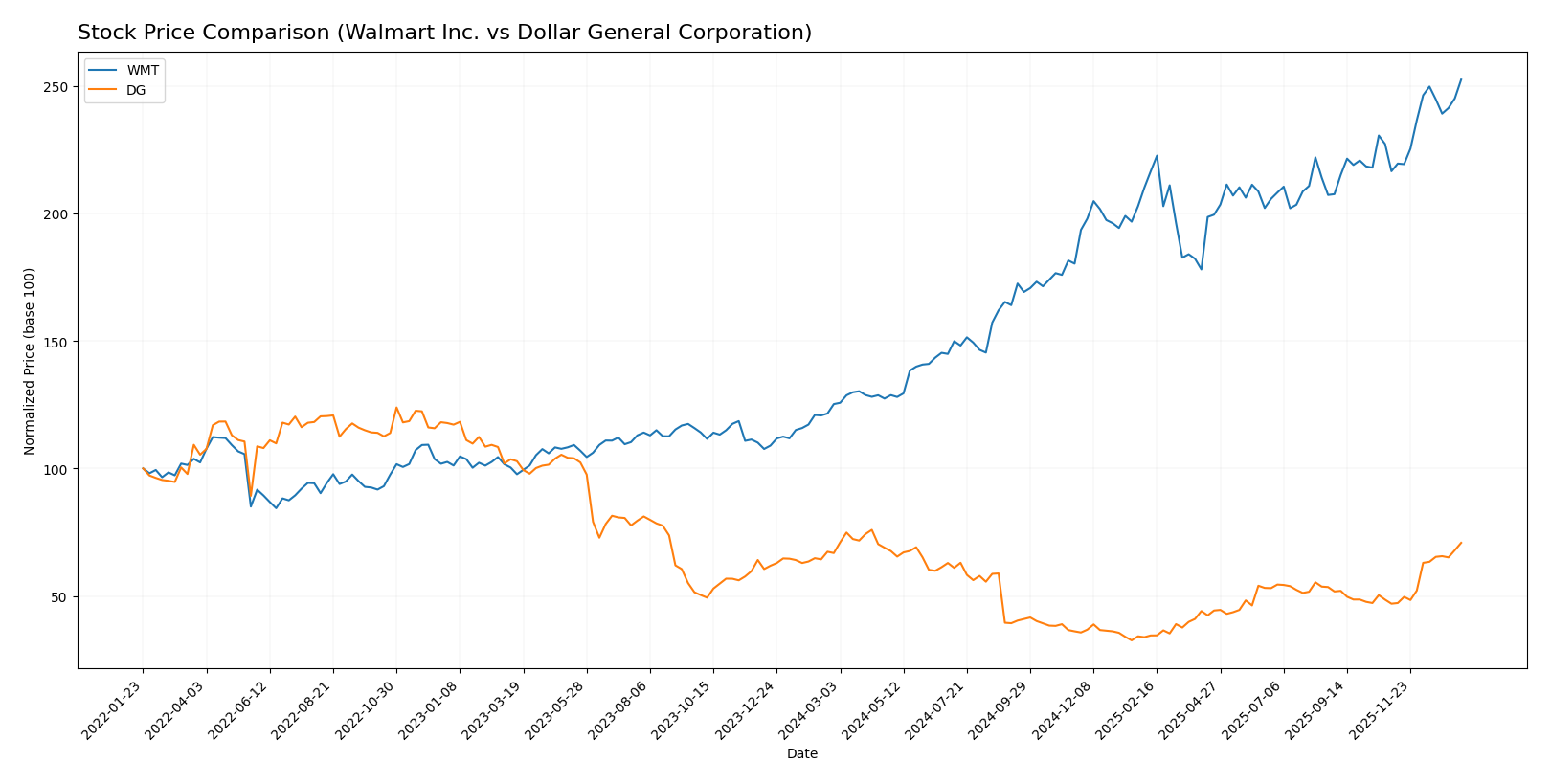

The past year saw Walmart Inc. (WMT) and Dollar General Corporation (DG) both exhibit bullish trends with notable price increases and distinct trading volume dynamics reflecting differing market engagements.

Trend Analysis

Walmart Inc. demonstrated a strong bullish trend over the past 12 months, with a price increase of 101.59%, accelerating upward and a standard deviation of 16.45. The stock hit a high of 117.97 and a low of 58.52, showing robust growth momentum.

Dollar General Corporation’s stock also followed a bullish trend, increasing by 6.03% over the same period with acceleration and a higher volatility at 25.35 standard deviation. The price ranged between 68.44 and 159.55, reflecting moderate growth.

Comparing both, Walmart delivered the highest market performance with a significantly larger price gain, while Dollar General showed less pronounced but still positive appreciation over the year.

Target Prices

Analysts provide a positive target price consensus for both Walmart Inc. and Dollar General Corporation.

| Company | Target High | Target Low | Consensus |

|---|---|---|---|

| Walmart Inc. | 135 | 119 | 125.67 |

| Dollar General Corporation | 170 | 125 | 140.06 |

The consensus target prices suggest moderate upside potential for Walmart and notable upside for Dollar General compared to their current prices of $117.97 and $148.86 respectively. Overall, analysts expect growth but with some range of uncertainty.

Analyst Opinions Comparison

This section compares analysts’ ratings and grades for Walmart Inc. and Dollar General Corporation:

Rating Comparison

Walmart Inc. Rating

- Rating: B-, classified as Very Favorable

- Discounted Cash Flow Score: 2, Moderate valuation

- ROE Score: 5, indicating very favorable profitability

- ROA Score: 4, favorable asset utilization

- Debt To Equity Score: 2, moderate financial risk

- Overall Score: 3, moderate overall financial standing

Dollar General Corporation Rating

- Rating: B, classified as Very Favorable

- Discounted Cash Flow Score: 4, Favorable valuation

- ROE Score: 4, indicating favorable profitability

- ROA Score: 3, moderate asset utilization

- Debt To Equity Score: 1, very unfavorable financial risk

- Overall Score: 3, moderate overall financial standing

Which one is the best rated?

Dollar General has a higher rating (B) and a better discounted cash flow score than Walmart (B- and 2 vs. 4). Walmart, however, has superior ROE and ROA scores. Both share the same overall score. Dollar General’s lower debt to equity score indicates higher financial risk.

Scores Comparison

Here is a comparison of the Altman Z-Score and Piotroski Score for Walmart Inc. and Dollar General Corporation:

Walmart Inc. Scores

- Altman Z-Score: 6.03, in the safe zone indicating very low bankruptcy risk.

- Piotroski Score: 6, rated average for financial strength and value.

Dollar General Corporation Scores

- Altman Z-Score: 2.55, in the grey zone indicating moderate bankruptcy risk.

- Piotroski Score: 8, rated very strong indicating robust financial health.

Which company has the best scores?

Dollar General has a stronger Piotroski Score of 8 versus Walmart’s 6, indicating better financial health. However, Walmart’s Altman Z-Score of 6.03 places it firmly in the safe zone, while Dollar General’s 2.55 is in the grey zone, suggesting higher bankruptcy risk.

Grades Comparison

The following tables summarize the recent reliable grades assigned to Walmart Inc. and Dollar General Corporation by recognized financial institutions:

Walmart Inc. Grades

The table below shows Walmart’s grades from major grading companies in early 2026.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Barclays | Maintain | Overweight | 2026-01-08 |

| Oppenheimer | Maintain | Outperform | 2026-01-08 |

| Mizuho | Maintain | Outperform | 2026-01-05 |

| Bernstein | Maintain | Outperform | 2026-01-05 |

| Wells Fargo | Maintain | Overweight | 2025-12-19 |

| Evercore ISI Group | Maintain | Outperform | 2025-12-16 |

| Evercore ISI Group | Maintain | Outperform | 2025-12-09 |

| Tigress Financial | Maintain | Buy | 2025-12-03 |

| BTIG | Maintain | Buy | 2025-11-21 |

| Morgan Stanley | Maintain | Overweight | 2025-11-21 |

Walmart’s grades consistently indicate positive outlooks with multiple “Outperform,” “Overweight,” and “Buy” ratings maintained over the past two months.

Dollar General Corporation Grades

The table below presents Dollar General’s recent grades from reputable firms.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Barclays | Maintain | Overweight | 2026-01-08 |

| Bernstein | Maintain | Outperform | 2026-01-05 |

| Evercore ISI Group | Maintain | In Line | 2025-12-23 |

| Wells Fargo | Maintain | Equal Weight | 2025-12-19 |

| JP Morgan | Upgrade | Overweight | 2025-12-15 |

| Guggenheim | Maintain | Buy | 2025-12-08 |

| Citigroup | Maintain | Neutral | 2025-12-08 |

| Jefferies | Maintain | Buy | 2025-12-05 |

| Morgan Stanley | Maintain | Equal Weight | 2025-12-05 |

| Evercore ISI Group | Maintain | In Line | 2025-12-05 |

Dollar General has a mix of “Buy,” “Overweight,” and “In Line” or “Equal Weight” ratings, showing some divergence in analyst sentiment.

Which company has the best grades?

Both Walmart and Dollar General have a consensus “Buy” rating, but Walmart’s grades are more uniformly positive with multiple “Outperform” and “Overweight” ratings, reflecting stronger analyst confidence. Dollar General’s ratings include several neutral or “In Line” assessments, indicating a more cautious outlook. Investors may interpret Walmart’s stronger consensus as reflecting higher expected performance or stability.

Strengths and Weaknesses

Below is a comparative overview of key strengths and weaknesses for Walmart Inc. (WMT) and Dollar General Corporation (DG) based on the most recent data.

| Criterion | Walmart Inc. (WMT) | Dollar General Corporation (DG) |

|---|---|---|

| Diversification | Strong diversification with three major segments: Walmart U.S. ($462B in 2025), Walmart International ($122B), and Sam’s Club ($90B). | Less diversified, primarily focused on consumables ($33B in 2024) and smaller apparel, seasonal segments. |

| Profitability | ROIC 13.06% (favorable), ROE 21.36% (favorable), net margin low at 2.85% (unfavorable). | Moderate ROIC 5.1% (neutral), ROE 15.18% (favorable), net margin 2.77% (unfavorable). |

| Innovation | Demonstrates durable competitive advantage with growing ROIC (+43.5%) and value creation (ROIC > WACC by 6.4%). | Declining ROIC (-60.9%) and value destruction (ROIC < WACC), indicating weakening innovation and profitability. |

| Global presence | Large international footprint contributing $122B revenue in 2025, enhancing global market reach. | Primarily U.S.-focused with limited international exposure, restricting global scale. |

| Market Share | Dominant market share with over $574B total revenue in 2025 across segments. | Smaller scale with total revenue around $40B in 2024, focused on discount retail niche. |

Key takeaways: Walmart’s broad diversification, strong global presence, and growing profitability position it as a value creator with a very favorable moat. Dollar General, while profitable on some metrics, faces challenges with declining ROIC and limited diversification, posing higher risk for investors.

Risk Analysis

Below is a comparative table of key risks for Walmart Inc. (WMT) and Dollar General Corporation (DG) based on the most recent data from 2025 and 2024.

| Metric | Walmart Inc. (WMT) | Dollar General Corporation (DG) |

|---|---|---|

| Market Risk | Moderate (Beta 0.66) | Low (Beta 0.26) |

| Debt level | Moderate (Debt-to-Equity 0.66) | High (Debt-to-Equity 2.36) |

| Regulatory Risk | Moderate | Moderate |

| Operational Risk | Moderate (Large-scale ops) | Moderate (Extensive store network) |

| Environmental Risk | Moderate (Retail footprint) | Moderate |

| Geopolitical Risk | Moderate (International ops) | Low-Medium (US-focused) |

Walmart faces moderate market and geopolitical risks due to its global presence, with a manageable debt level and favorable financial stability (Altman Z-Score 6.03). Dollar General carries higher financial risk from significant leverage (Debt-to-Equity 2.36, Altman Z-Score 2.55), despite low market volatility. For investors, Walmart’s balanced risk profile and strong financials contrast with Dollar General’s higher debt and moderate bankruptcy risk despite very strong operational health.

Which Stock to Choose?

Walmart Inc. (WMT) shows a favorable income evolution with 21.79% revenue growth over five years and improving profitability metrics, including a 21.36% ROE. Its financial ratios are slightly favorable, with solid debt metrics and strong interest coverage. The company holds a very favorable rating and demonstrates a very favorable economic moat based on growing ROIC significantly above WACC.

Dollar General Corporation (DG) exhibits a mixed income evolution marked by a 20.34% revenue growth but a notable decline in net income and profitability over the period. Its financial ratios are slightly favorable overall, despite high debt levels and moderate coverage ratios. DG has a very favorable rating score but a slightly unfavorable moat due to declining ROIC below WACC and decreasing profitability.

Investors focused on durable competitive advantages and consistent profitability might find Walmart’s metrics and moat more indicative of stability and value creation. Conversely, those favoring potential value opportunities amid higher leverage and recent earnings volatility could view Dollar General’s profile differently. The choice could thus depend on the investor’s risk tolerance and strategy orientation.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Walmart Inc. and Dollar General Corporation to enhance your investment decisions: