In the dynamic world of technology, Salesforce, Inc. (CRM) and DocuSign, Inc. (DOCU) stand out as key players in the software application industry. Both headquartered in San Francisco, these companies overlap in digital solutions that enhance business efficiency—Salesforce with its comprehensive customer relationship management platform, and DocuSign with its innovative electronic signature and contract lifecycle management tools. This article will explore which company offers the most compelling investment opportunity for you.

Table of contents

Companies Overview

I will begin the comparison between Salesforce and DocuSign by providing an overview of these two companies and their main differences.

Salesforce Overview

Salesforce, Inc. is a leading customer relationship management (CRM) technology provider, offering a comprehensive platform that connects companies with customers globally. Its Customer 360 platform supports sales, service, marketing, commerce, and analytics, enabling businesses across various industries to deliver personalized experiences. Headquartered in San Francisco, Salesforce serves diverse sectors with a flexible platform and integrates tools like Slack and Tableau to enhance collaboration and data insights.

DocuSign Overview

DocuSign, Inc. specializes in electronic signature software and digital agreement management, offering solutions that streamline contract workflows for businesses worldwide. Its platform includes AI-driven contract lifecycle management, interactive forms, identity verification, and industry-specific cloud services. Based in San Francisco, DocuSign targets enterprise, commercial, and small businesses, focusing on simplifying agreement processes and compliance through its cloud offerings and advanced analytics.

Key similarities and differences

Both Salesforce and DocuSign operate in the software application industry, providing cloud-based solutions aimed at improving business processes. Salesforce offers a broader CRM platform encompassing sales, marketing, service, and analytics, while DocuSign focuses specifically on digital agreement and contract management. Salesforce’s larger scale is reflected in its extensive employee base and diverse product suite, whereas DocuSign is more specialized with a narrower product focus and smaller workforce.

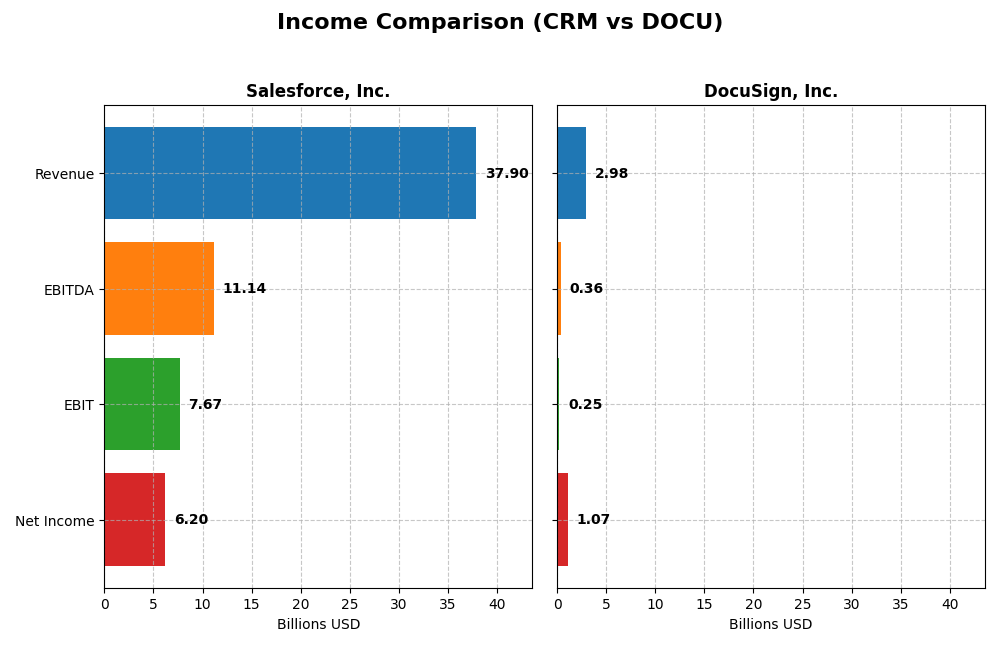

Income Statement Comparison

The table below presents a side-by-side comparison of key income statement metrics for Salesforce, Inc. and DocuSign, Inc. for the fiscal year 2025.

| Metric | Salesforce, Inc. (CRM) | DocuSign, Inc. (DOCU) |

|---|---|---|

| Market Cap | 219B | 12B |

| Revenue | 37.9B | 3.0B |

| EBITDA | 11.1B | 357M |

| EBIT | 7.7B | 249M |

| Net Income | 6.2B | 1.1B |

| EPS | 6.44 | 5.23 |

| Fiscal Year | 2025 | 2025 |

Income Statement Interpretations

Salesforce, Inc.

Salesforce’s revenue grew steadily from 21.25B in 2021 to 37.9B in 2025, with net income expanding from 4.07B to 6.2B over the same period. Margins remained strong, with gross margin at 77.19% and net margin improving to 16.35%. In 2025, growth accelerated, with revenue up 8.72% and net income rising 37.82%, reflecting enhanced operational efficiency and profitability.

DocuSign, Inc.

DocuSign’s revenue increased from 1.45B in 2021 to nearly 3B in 2025, while net income swung from a loss of 243M to a gain of 1.07B. Gross margin stayed robust at 79.12%, with net margin reaching 35.87%. The latest year saw moderate revenue growth of 7.78%, but explosive net margin and EPS growth, indicating a significant turnaround and improved cost control.

Which one has the stronger fundamentals?

Both companies show favorable income statement trends, with Salesforce demonstrating consistent revenue and net income growth and solid margins. DocuSign exhibits remarkable net income and margin improvements, transforming losses into profits with rapid EPS growth. Salesforce’s higher margin stability contrasts with DocuSign’s impressive turnaround, suggesting strong fundamentals for each but in different financial maturity stages.

Financial Ratios Comparison

This table presents the most recent financial ratios for Salesforce, Inc. and DocuSign, Inc., providing a clear comparison of key performance and financial health indicators for fiscal year 2025.

| Ratios | Salesforce, Inc. (CRM) | DocuSign, Inc. (DOCU) |

|---|---|---|

| ROE | 10.13% | 53.32% |

| ROIC | 7.95% | 9.09% |

| P/E | 53.04 | 18.51 |

| P/B | 5.37 | 9.87 |

| Current Ratio | 1.06 | 0.81 |

| Quick Ratio | 1.06 | 0.81 |

| D/E (Debt-to-Equity) | 0.19 | 0.06 |

| Debt-to-Assets | 11.07% | 3.10% |

| Interest Coverage | 26.49 | 128.99 |

| Asset Turnover | 0.37 | 0.74 |

| Fixed Asset Turnover | 7.03 | 7.28 |

| Payout Ratio | 24.80% | 0% |

| Dividend Yield | 0.47% | 0% |

Interpretation of the Ratios

Salesforce, Inc.

Salesforce shows a mix of strengths and concerns in its 2025 ratios. It has favorable net margin, quick ratio, and debt metrics, indicating financial stability and efficient leverage management. However, its high P/E and P/B ratios, along with a low asset turnover, suggest valuation and efficiency challenges. The company pays dividends with a modest yield of 0.47%, reflecting cautious shareholder returns.

DocuSign, Inc.

DocuSign’s 2025 ratios reveal strong profitability with favorable net margin and return on equity, supported by excellent interest coverage and low debt levels. Yet, liquidity ratios are weaker, with a current ratio below 1, signaling potential short-term solvency risks. The firm does not pay dividends, likely prioritizing reinvestment and growth, consistent with its high R&D intensity and share buyback absence.

Which one has the best ratios?

Both companies present a slightly favorable overall ratio profile, each with distinct strengths. Salesforce benefits from solid leverage and liquidity ratios but faces valuation pressures. DocuSign excels in profitability and debt management but shows weaker liquidity metrics. The best ratios depend on investors’ focus on either stability or growth potential.

Strategic Positioning

This section compares the strategic positioning of Salesforce and DocuSign, including their market position, key segments, and exposure to technological disruption:

Salesforce, Inc.

- Leading software application provider with significant market cap and competitive pressure.

- Diverse revenue streams including Sales, Service, Marketing Clouds, Analytics, and Platform services.

- Exposure to technological disruption through integration, analytics, AI, and platform innovation.

DocuSign, Inc.

- Smaller market cap, focused on electronic signature software with moderate competition.

- Concentrated revenue mainly from subscription-based e-signature and related services.

- Adoption of AI and advanced analytics in contract lifecycle management and agreement processes.

Salesforce vs DocuSign Positioning

Salesforce exhibits a diversified business model across multiple cloud services and analytics, offering broad market coverage; DocuSign remains focused on electronic signature and contract management, which may limit market reach but concentrates innovation. Salesforce’s scale offers resilience, while DocuSign’s specialization targets niche solutions.

Which has the best competitive advantage?

DocuSign shows a slightly favorable moat with growing profitability but no strong competitive advantage yet. Salesforce faces slightly unfavorable moat conditions despite increasing ROIC, indicating value destruction but improving profitability trends.

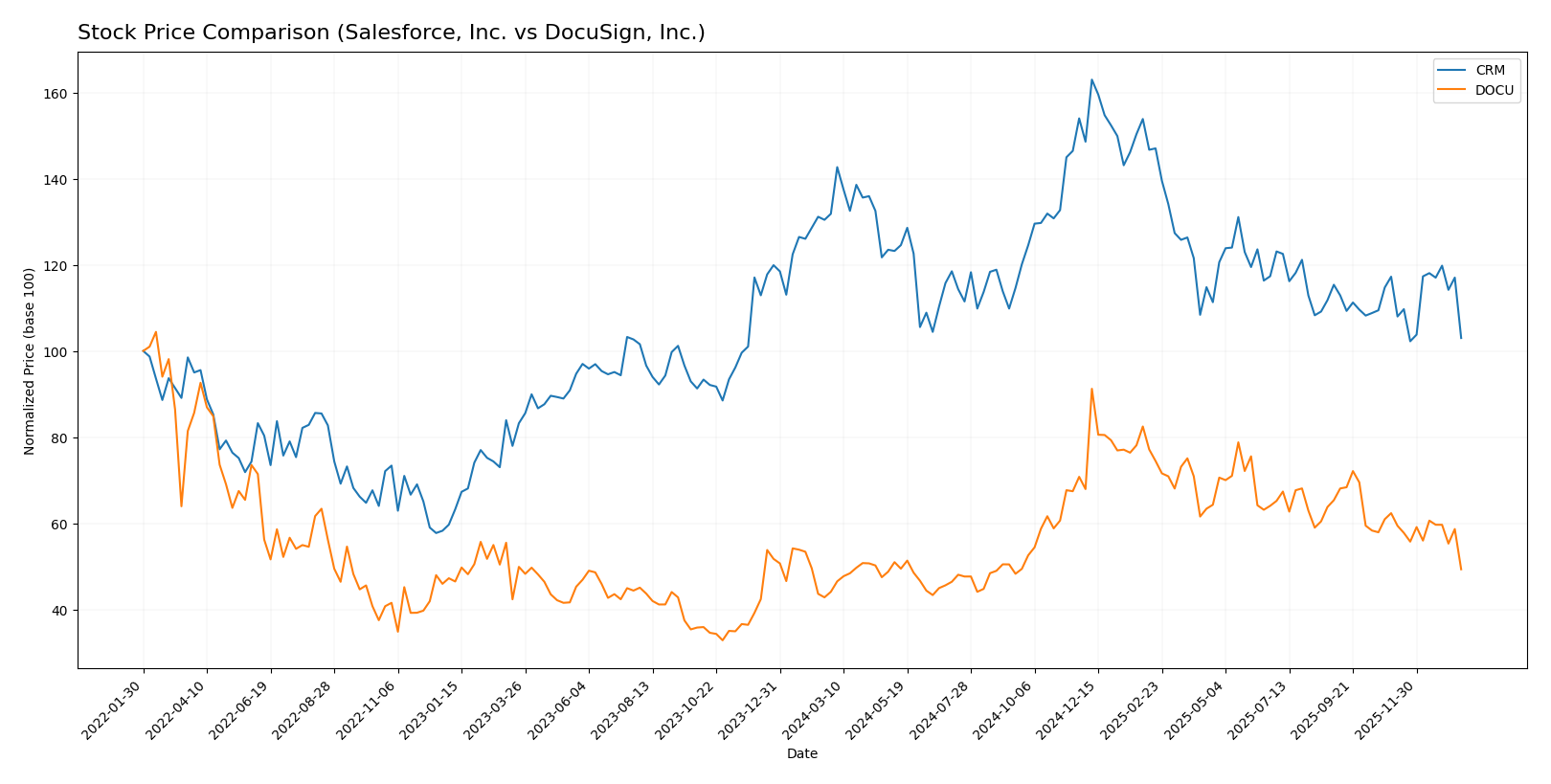

Stock Comparison

The stock price movements over the past 12 months reveal contrasting dynamics: Salesforce, Inc. (CRM) shows a significant bearish trend with price declines accelerating, while DocuSign, Inc. (DOCU) exhibits a bullish trend overall but recent weakness with decelerating gains and recent price drops.

Trend Analysis

Salesforce, Inc. experienced a -21.86% price change over the past year, indicating a bearish trend with accelerating decline. The stock showed high volatility (std deviation 31.79) and a wide price range between 227.11 and 361.99.

DocuSign, Inc. posted an 11.84% price increase over the same period, reflecting a bullish trend with decelerating momentum. Volatility was lower (std deviation 12.97), with prices ranging from 50.84 to 106.99.

Comparing both, DocuSign delivered the highest market performance with a positive 11.84% return versus Salesforce’s -21.86%, despite recent short-term weakness in both stocks.

Target Prices

The consensus target prices for Salesforce, Inc. and DocuSign, Inc. reveal optimistic analyst expectations compared to current market prices.

| Company | Target High | Target Low | Consensus |

|---|---|---|---|

| Salesforce, Inc. | 400 | 250 | 324.17 |

| DocuSign, Inc. | 88 | 70 | 76.86 |

Analysts project Salesforce’s stock to rise significantly from $228.57 to a consensus near $324.17, indicating substantial upside potential. DocuSign’s consensus target of $76.86 also suggests notable appreciation from its current $57.85 price.

Analyst Opinions Comparison

This section compares analysts’ ratings and grades for Salesforce, Inc. and DocuSign, Inc.:

Rating Comparison

Salesforce, Inc. Rating

- Rating: B+ indicating a very favorable overall status.

- Discounted Cash Flow Score: 4, favorable valuation based on cash flow projections.

- ROE Score: 4, favorable efficiency in generating profit from equity.

- ROA Score: 4, favorable asset utilization to generate earnings.

- Debt To Equity Score: 3, moderate financial risk with balanced debt level.

- Overall Score: 3, moderate overall financial standing.

DocuSign, Inc. Rating

- Rating: B indicating a very favorable overall status.

- Discounted Cash Flow Score: 4, favorable valuation based on cash flow projections.

- ROE Score: 4, favorable efficiency in generating profit from equity.

- ROA Score: 4, favorable asset utilization to generate earnings.

- Debt To Equity Score: 3, moderate financial risk with balanced debt level.

- Overall Score: 3, moderate overall financial standing.

Which one is the best rated?

Based strictly on the provided data, Salesforce has a slightly higher rating (B+) compared to DocuSign’s B. Both share identical scores across key metrics, but Salesforce’s overall rating suggests a marginally better analyst sentiment.

Scores Comparison

The scores comparison between Salesforce and DocuSign provides insight into their financial health based on Altman Z-Score and Piotroski Score:

Salesforce Scores

- Altman Z-Score of 5.26, indicating a safe financial zone.

- Piotroski Score of 7, reflecting strong financial strength.

DocuSign Scores

- Altman Z-Score of 4.43, also in the safe zone.

- Piotroski Score of 5, showing average financial health.

Which company has the best scores?

Salesforce has a higher Altman Z-Score and a stronger Piotroski Score than DocuSign, indicating better financial stability and strength based on the provided data.

Grades Comparison

Here is the grades comparison of Salesforce, Inc. and DocuSign, Inc. from recognized grading companies:

Salesforce, Inc. Grades

The following table summarizes recent grades assigned to Salesforce, Inc. by reputable firms:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Barclays | Maintain | Overweight | 2026-01-12 |

| RBC Capital | Maintain | Sector Perform | 2026-01-05 |

| Morgan Stanley | Maintain | Overweight | 2025-12-09 |

| Citigroup | Maintain | Neutral | 2025-12-08 |

| DA Davidson | Maintain | Neutral | 2025-12-05 |

| Citizens | Maintain | Market Outperform | 2025-12-04 |

| Deutsche Bank | Maintain | Buy | 2025-12-04 |

| Wedbush | Maintain | Outperform | 2025-12-04 |

| Northland Capital Markets | Maintain | Market Perform | 2025-12-04 |

| Canaccord Genuity | Maintain | Buy | 2025-12-04 |

Salesforce’s grades consistently show positive outlooks with multiple “Buy,” “Overweight,” and “Outperform” ratings, indicating general analyst confidence.

DocuSign, Inc. Grades

The following table summarizes recent grades assigned to DocuSign, Inc. by reputable firms:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| RBC Capital | Maintain | Sector Perform | 2026-01-05 |

| Evercore ISI Group | Maintain | In Line | 2025-12-05 |

| UBS | Maintain | Neutral | 2025-12-05 |

| Wells Fargo | Maintain | Equal Weight | 2025-12-05 |

| Piper Sandler | Maintain | Neutral | 2025-12-05 |

| RBC Capital | Maintain | Sector Perform | 2025-12-05 |

| JP Morgan | Maintain | Neutral | 2025-12-05 |

| B of A Securities | Maintain | Neutral | 2025-12-05 |

| Needham | Maintain | Hold | 2025-12-05 |

| Baird | Maintain | Neutral | 2025-12-05 |

DocuSign’s grades predominantly fall in the “Neutral,” “Hold,” and “Sector Perform” categories, reflecting a more cautious analyst stance.

Which company has the best grades?

Salesforce, Inc. has received markedly stronger grades compared to DocuSign, Inc., with multiple “Buy” and “Overweight” ratings versus DocuSign’s mostly neutral or hold positions. This may suggest greater analyst confidence in Salesforce’s prospects, potentially influencing investor sentiment accordingly.

Strengths and Weaknesses

Below is a comparison of key strengths and weaknesses of Salesforce, Inc. (CRM) and DocuSign, Inc. (DOCU) based on their recent financial performance, innovation, and market positioning.

| Criterion | Salesforce, Inc. (CRM) | DocuSign, Inc. (DOCU) |

|---|---|---|

| Diversification | Highly diversified product portfolio across CRM, Service, Marketing, Analytics, and Professional Services with revenues exceeding $35B in 2025 | More concentrated business model focused on digital transaction management and e-signature services with revenues around $2.95B in 2025 |

| Profitability | Moderate profitability: Net margin 16.35%, ROIC 7.95% (slightly below WACC 9.42%), shedding value but improving ROIC trend | Higher profitability: Net margin 35.87%, ROIC 9.09% slightly above WACC 8.41%, showing value creation and growing profitability |

| Innovation | Strong continuous innovation with expanding cloud-based platforms and analytics integrations | Focused innovation in digital agreements, subscription growth, and professional services expansion |

| Global presence | Extensive global footprint with wide enterprise adoption and multiple cloud offerings | Growing global presence but more niche market penetration compared to CRM |

| Market Share | Large CRM market leader with significant share and strong platform ecosystem | Leading player in e-signature market but smaller scale and market share compared to CRM |

Key takeaways: Salesforce exhibits strong diversification and market leadership with improving profitability but still faces challenges in value creation. DocuSign shows robust profitability and a favorable moat trend, though with a narrower focus and smaller scale. Both remain attractive but suit different risk and growth profiles.

Risk Analysis

Below is a comparison table of key risks for Salesforce, Inc. (CRM) and DocuSign, Inc. (DOCU) based on the most recent 2025 data:

| Metric | Salesforce, Inc. (CRM) | DocuSign, Inc. (DOCU) |

|---|---|---|

| Market Risk | Beta 1.27, moderate volatility due to tech sector exposure | Beta 0.99, lower volatility but exposure to software market shifts |

| Debt level | Low debt-to-equity 0.19, favorable leverage | Very low debt-to-equity 0.06, very conservative leverage |

| Regulatory Risk | Moderate, due to global operations and data privacy laws | Moderate, especially related to digital signature regulations and compliance |

| Operational Risk | Medium, complexity of cloud platform integration and acquisitions | Medium, reliance on SaaS platform stability and customer retention |

| Environmental Risk | Low, limited direct environmental impact | Low, primarily digital services with minimal environmental footprint |

| Geopolitical Risk | Moderate, global customer base and supply chain exposure | Moderate, international sales and regulatory environments |

The most impactful risks are market volatility for Salesforce, driven by its broad tech exposure and valuation multiples, and regulatory risks for DocuSign, given the evolving nature of digital agreements and data privacy. Both companies maintain strong balance sheets with low debt, reducing financial risk. Operational risks remain relevant but manageable given their technology focus and stable platforms.

Which Stock to Choose?

Salesforce, Inc. (CRM) shows a strong income evolution with an 8.72% revenue growth over one year and a favorable global income statement evaluation at 92.86%. Its financial ratios are slightly favorable, highlighted by a favorable net margin of 16.35% and solid debt metrics, though some valuation ratios are unfavorable. The company’s profitability is increasing, but the MOAT evaluation suggests it is slightly unfavorable due to value destruction, despite a growing ROIC. CRM holds a very favorable rating at B+.

DocuSign, Inc. (DOCU) presents a favorable income evolution with 7.78% revenue growth last year and a favorable overall income statement rating at 85.71%. Its financial ratios are also slightly favorable, supported by a strong net margin of 35.87% and excellent returns on equity, despite some weaker liquidity ratios. DOCU’s MOAT is slightly favorable, indicating increasing profitability but no confirmed competitive advantage. The company is rated very favorable at B.

Investors focused on stability and moderate growth might find Salesforce’s established profitability and solid ratings appealing, while those with a higher risk tolerance or seeking rapid earnings growth may view DocuSign’s strong margins and improving profitability as favorable. The choice could depend on an investor’s preference for established value creation versus growth potential.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Salesforce, Inc. and DocuSign, Inc. to enhance your investment decisions: