Home > Comparison > Technology > DOCU vs MTCH

The strategic rivalry between DocuSign, Inc. and Match Group, Inc. shapes the evolution of the technology sector’s software application industry. DocuSign operates as a capital-intensive provider of digital agreement solutions, while Match Group leverages a high-margin portfolio of dating platforms. This head-to-head reflects a broader contest between scalable service innovation and platform-driven consumer engagement. This analysis will identify which company offers a superior risk-adjusted outlook for a diversified portfolio in 2026.

Table of contents

Companies Overview

DocuSign and Match Group stand as influential players in the software application market with distinct global footprints.

DocuSign, Inc.: Digital Agreement Leader

DocuSign dominates the e-signature software space, generating revenue primarily through its cloud-based digital agreement solutions. It focuses on automating contract lifecycle management and integrates AI-driven tools to enhance agreement workflows. In 2026, its strategic emphasis lies on expanding industry-specific cloud offerings and embedding AI capabilities to maintain its competitive edge.

Match Group, Inc.: Premier Online Dating Platform

Match Group commands the online dating market with its portfolio of brands, including Tinder and OkCupid. Its core revenue engine is subscription-based access to dating services across multiple demographics globally. The company’s 2026 strategy centers on diversifying its brand ecosystem and enhancing user engagement through innovative product development.

Strategic Collision: Similarities & Divergences

Both companies operate within the software applications sector but differ in business philosophy. DocuSign pursues a B2B SaaS model focused on enterprise contract management, while Match Group embraces a consumer subscription model centered on social connectivity. Their primary battleground lies in digital user engagement, yet their investment profiles diverge sharply—DocuSign offers enterprise stability, whereas Match Group bets on consumer market growth and brand diversification.

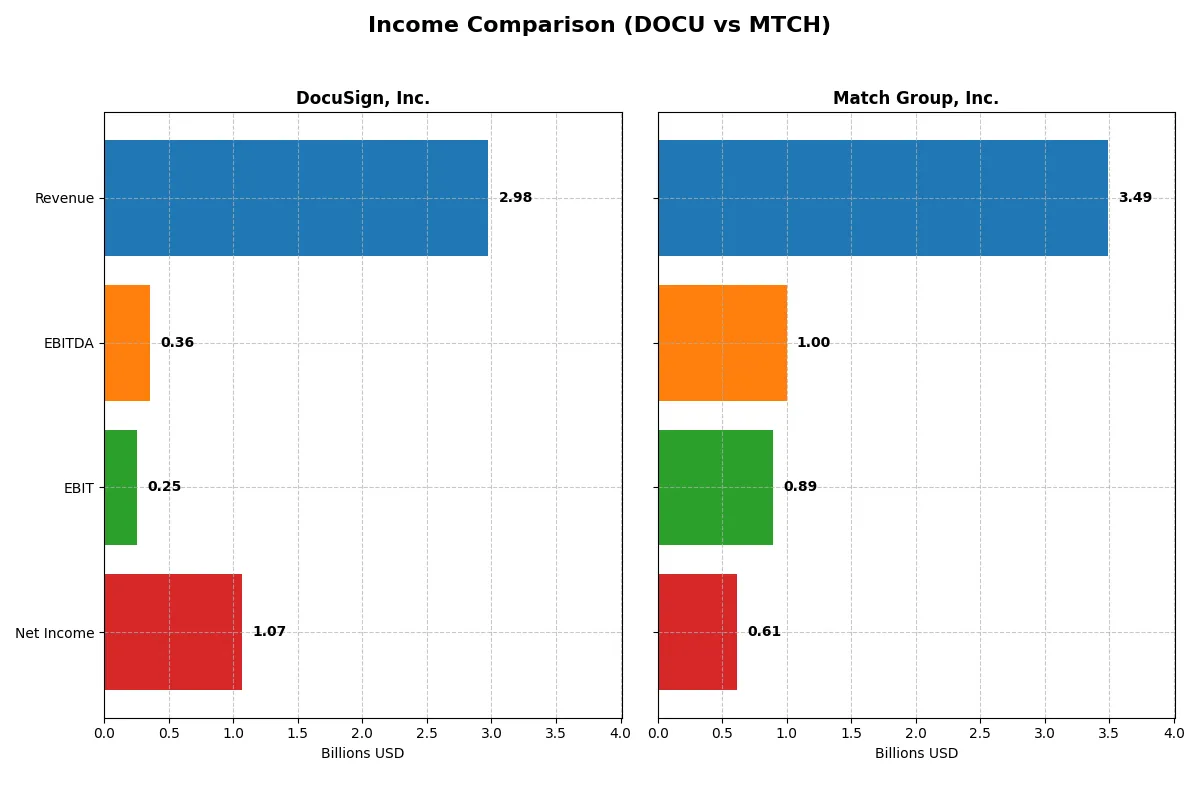

Income Statement Comparison

The following data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | DocuSign, Inc. (DOCU) | Match Group, Inc. (MTCH) |

|---|---|---|

| Revenue | 2.98B | 3.49B |

| Cost of Revenue | 622M | 948M |

| Operating Expenses | 2.16B | 1.67B |

| Gross Profit | 2.36B | 2.54B |

| EBITDA | 357M | 999M |

| EBIT | 249M | 894M |

| Interest Expense | 1.55M | 148M |

| Net Income | 1.07B | 613M |

| EPS | 5.23 | 2.53 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company converts revenue into profit more efficiently and sustains healthier margins.

DocuSign, Inc. Analysis

DocuSign’s revenue climbed steadily from 1.45B in 2021 to 3B in 2025, doubling over five years. Net income shifted from a loss of 243M in 2021 to a strong 1.07B profit in 2025. Gross margin remains robust at 79%, while net margin surged to 36%, signaling impressive margin expansion and operational leverage in the latest fiscal year.

Match Group, Inc. Analysis

Match Group’s revenue grew moderately from 3B in 2021 to 3.49B in 2025, reflecting slower top-line momentum. Net income more than doubled from 277M in 2021 to 613M in 2025. Gross margin stands at 73% with a solid 26% EBIT margin, highlighting efficient cost control despite a modest 0.2% revenue growth in the latest year.

Margin Expansion vs. Revenue Stability

DocuSign dominates margin expansion and bottom-line growth, delivering a striking net margin leap amid strong revenue gains. Match Group exhibits steadier revenue but more moderate margin improvement. For investors prioritizing profitability and efficiency, DocuSign’s accelerating margins and earnings growth offer a more compelling fundamental profile.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | DocuSign, Inc. (DOCU) | Match Group, Inc. (MTCH) |

|---|---|---|

| ROE | 53.3% | -2.4% |

| ROIC | 9.1% | 22.5% |

| P/E | 18.5x | 12.8x |

| P/B | 9.87x | -30.91x |

| Current Ratio | 0.81 | 1.42 |

| Quick Ratio | 0.81 | 1.42 |

| D/E | 0.06 | -15.67 |

| Debt-to-Assets | 3.1% | 89.1% |

| Interest Coverage | 129x | 5.91x |

| Asset Turnover | 0.74 | 0.78 |

| Fixed Asset Turnover | 7.28 | 26.59 |

| Payout Ratio | 0% | 30.4% |

| Dividend Yield | 0% | 2.38% |

| Fiscal Year | 2025 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios serve as a company’s DNA, exposing both hidden risks and operational strengths critical for investment decisions.

DocuSign, Inc.

DocuSign boasts a strong 53.3% ROE and a robust 35.9% net margin, signaling operational excellence. Its P/E of 18.5 indicates a fairly valued stock, though a high P/B near 9.9 signals market skepticism. DocuSign pays no dividend, instead channeling cash into R&D, fueling future growth.

Match Group, Inc.

Match Group shows a mixed picture with a negative ROE of -242% but a solid 17.6% net margin and a low P/E of 12.8, suggesting undervaluation. Its elevated debt-to-assets ratio at 89% flags risk, though a 2.38% dividend yield offers steady shareholder returns. Efficient asset use supports its favorable free cash flow yield.

Growth Potential vs. Financial Stability

DocuSign excels in profitability and reinvestment but struggles with liquidity and valuation concerns. Match Group offers better valuation and dividends but carries significant leverage risk. Investors seeking growth may lean toward DocuSign, while those prioritizing yield and value might prefer Match Group.

Which one offers the Superior Shareholder Reward?

I observe that DocuSign (DOCU) pays no dividends, choosing to reinvest free cash flow—$4.5/share in 2025—into growth and innovation. Match Group (MTCH) offers a 2.38% dividend yield with a 30% payout ratio, supported by strong FCF coverage of 95%. Match also pursues aggressive buybacks, enhancing total returns. DocuSign’s zero dividend and moderate buybacks reflect a growth-first strategy, but its current ratio below 1 signals liquidity risks. Match’s robust dividend, sustainable payout, and buyback intensity deliver a more balanced and sustainable shareholder reward. For 2026, I favor Match Group for superior total return potential and financial stability.

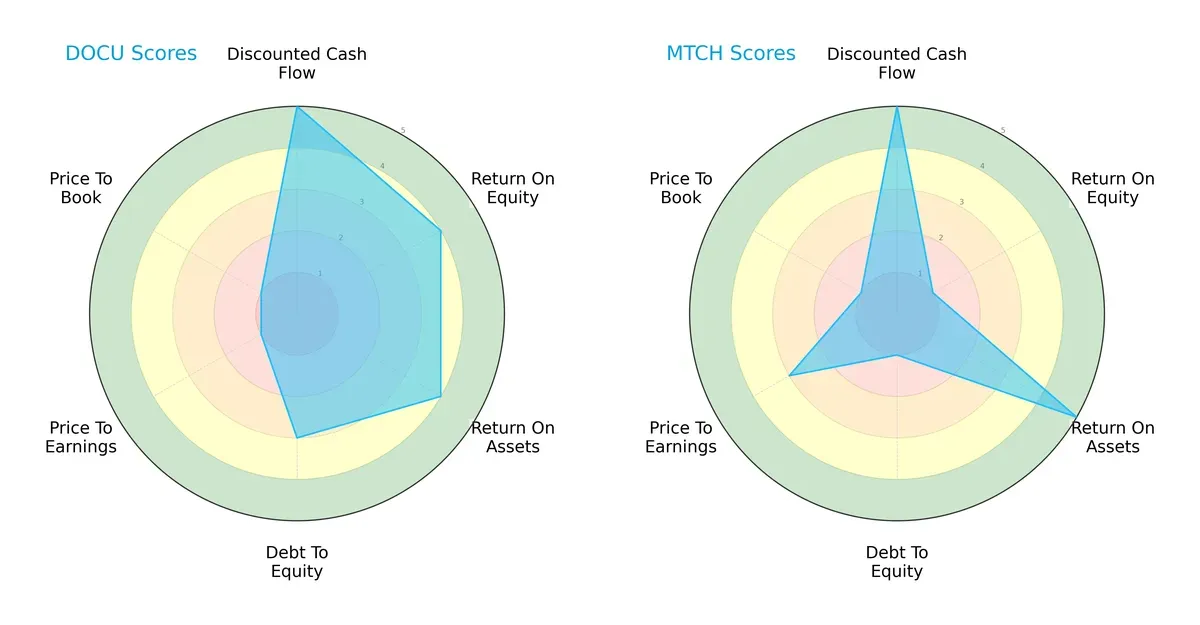

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of DocuSign, Inc. and Match Group, Inc., highlighting their strategic strengths and vulnerabilities:

DocuSign shows a balanced profile with strong DCF (5) and solid ROE (4) and ROA (4) scores, supported by moderate debt management (3). Match Group excels in asset utilization (ROA 5) but suffers from weak equity returns (ROE 1) and high leverage risk (debt-to-equity 1). DocuSign relies on consistent profitability, while Match Group leverages asset efficiency but carries higher financial risk.

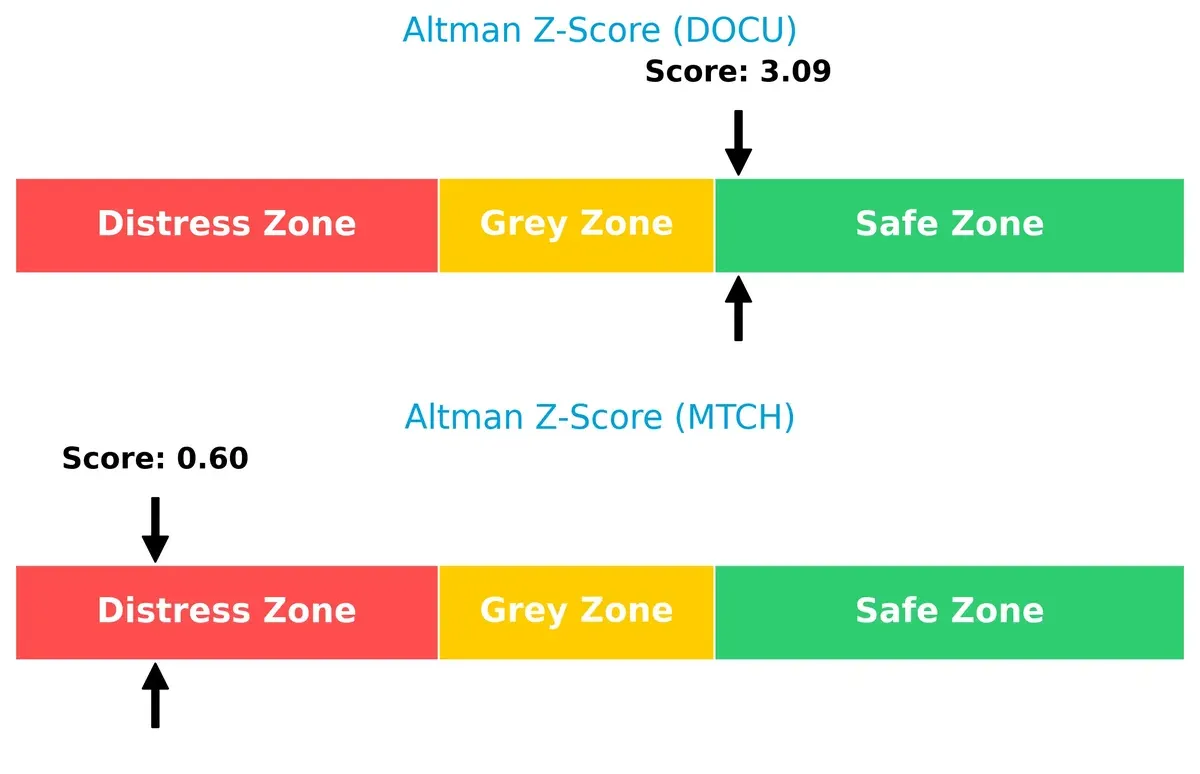

Bankruptcy Risk: Solvency Showdown

DocuSign’s Altman Z-Score of 3.09 places it comfortably in the safe zone, signaling financial stability. Match Group’s 0.60 score falls in distress territory, raising serious solvency concerns for long-term survival in this cycle:

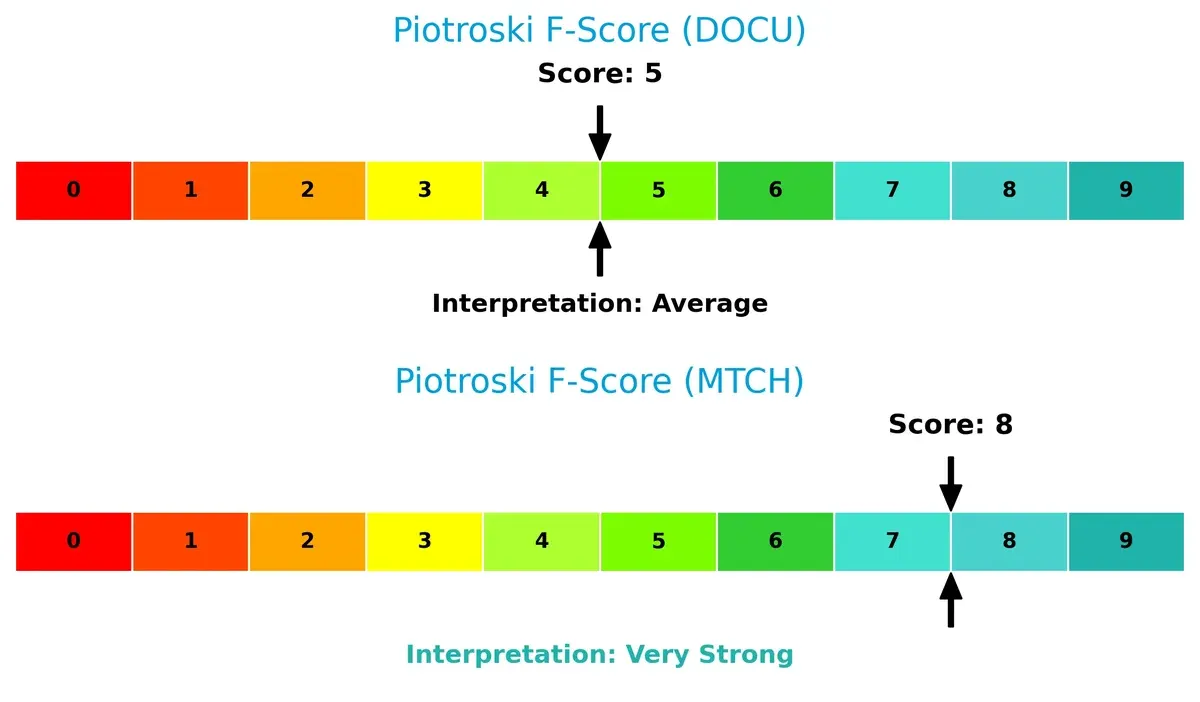

Financial Health: Quality of Operations

Match Group’s Piotroski F-Score of 8 indicates very strong financial health, reflecting robust internal metrics. DocuSign’s score of 5 is average, suggesting some operational weaknesses compared to its peer:

How are the two companies positioned?

This section dissects the operational DNA of DocuSign and Match Group by comparing their revenue distribution and internal dynamics. The goal is to confront their economic moats and identify which model offers the most resilient, sustainable advantage today.

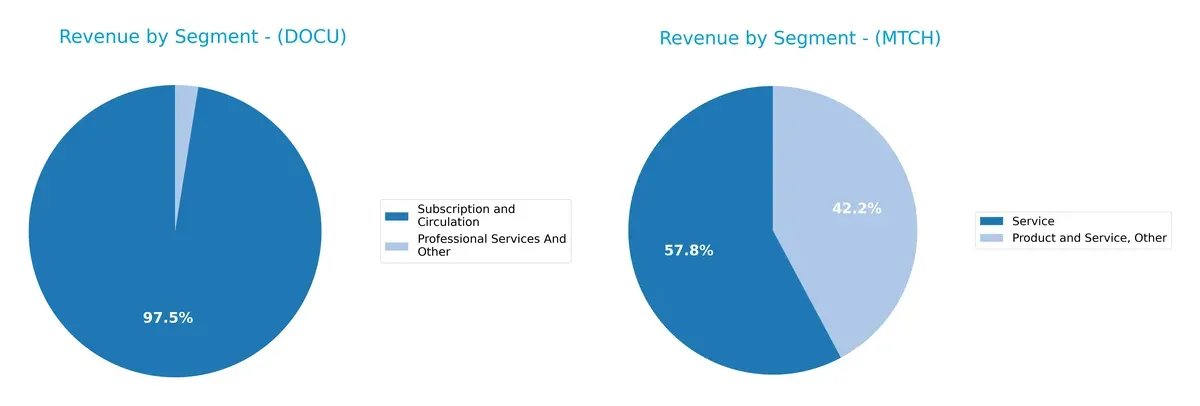

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how DocuSign, Inc. and Match Group, Inc. diversify their income streams and where their primary sector bets lie:

DocuSign anchors revenue with Subscription and Circulation, reaching $2.9B in 2025, while Professional Services remains a minor $75M. This concentration highlights a strong ecosystem lock-in in digital agreements. Conversely, Match Group shows a more fragmented mix with Product and Service ($989M) and Service ($1.36B) segments in 2020, reflecting diversified dating and online service platforms. DocuSign’s focus drives efficiency but risks overreliance; Match Group’s spread cushions sector volatility.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of DocuSign and Match Group based on diversification, profitability, financial health, innovation, global presence, and market share:

DocuSign Strengths

- Strong profitability with 35.87% net margin

- High return on equity at 53.32%

- Low debt-to-equity of 0.06 indicates conservative leverage

- Favorable interest coverage of 160.96

- Consistent US and growing non-US revenue

- High fixed asset turnover at 7.28

Match Group Strengths

- Favorable net margin of 17.59% with strong ROIC at 22.5%

- Lower WACC at 7.81% supports capital efficiency

- Attractive PE ratio of 12.77

- Solid liquidity with 1.42 current and quick ratios

- Diversified revenue streams across multiple segments

- Strong global presence with significant non-US revenue

DocuSign Weaknesses

- Suboptimal liquidity with current ratio at 0.81

- High price-to-book ratio at 9.87 signals overvaluation risk

- Neutral ROIC (9.09%) barely above WACC (8.46%)

- No dividend yield limits income appeal

- Moderate asset turnover at 0.74

Match Group Weaknesses

- Negative ROE at -241.99% raises concerns on equity returns

- High debt-to-assets at 89.06% implies elevated financial risk

- Negative debt-to-equity suggests complex capital structure

- Lower interest coverage of 6.06 compared to DocuSign

- Asset turnover neutral at 0.78 despite favorable fixed asset turnover

DocuSign shows strength in profitability and conservative leverage but faces liquidity and valuation challenges. Match Group benefits from efficient capital use and strong global diversification but carries significant financial risk from high leverage and weak equity returns.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only barrier protecting long-term profits from relentless competition erosion. Let’s dissect the competitive moats of two tech leaders:

DocuSign, Inc.: Workflow Automation with Growing Profitability

DocuSign’s moat stems from intangible assets and switching costs embedded in its e-signature and contract lifecycle management platform. I see margin stability and a soaring net margin growth of 314% over five years. Expansion into AI-driven contract solutions could deepen this moat but the firm still sheds value versus cost of capital.

Match Group, Inc.: Network Effects Powering Dating Dominance

Match Group’s competitive advantage relies on powerful network effects across multiple dating brands, locking in users globally. Its ROIC exceeds WACC by nearly 15%, signaling a robust economic moat. Although near-term revenue growth slows, its strong EBIT margin and expanding international markets sustain its value creation.

Network Effects vs. Switching Costs: The Moat Faceoff

Match Group exhibits a wider and deeper moat with consistent excess returns and strong margin profiles. DocuSign shows promising profitability growth but has yet to achieve sustainable value creation. Match Group stands better equipped to defend and grow its market share in 2026.

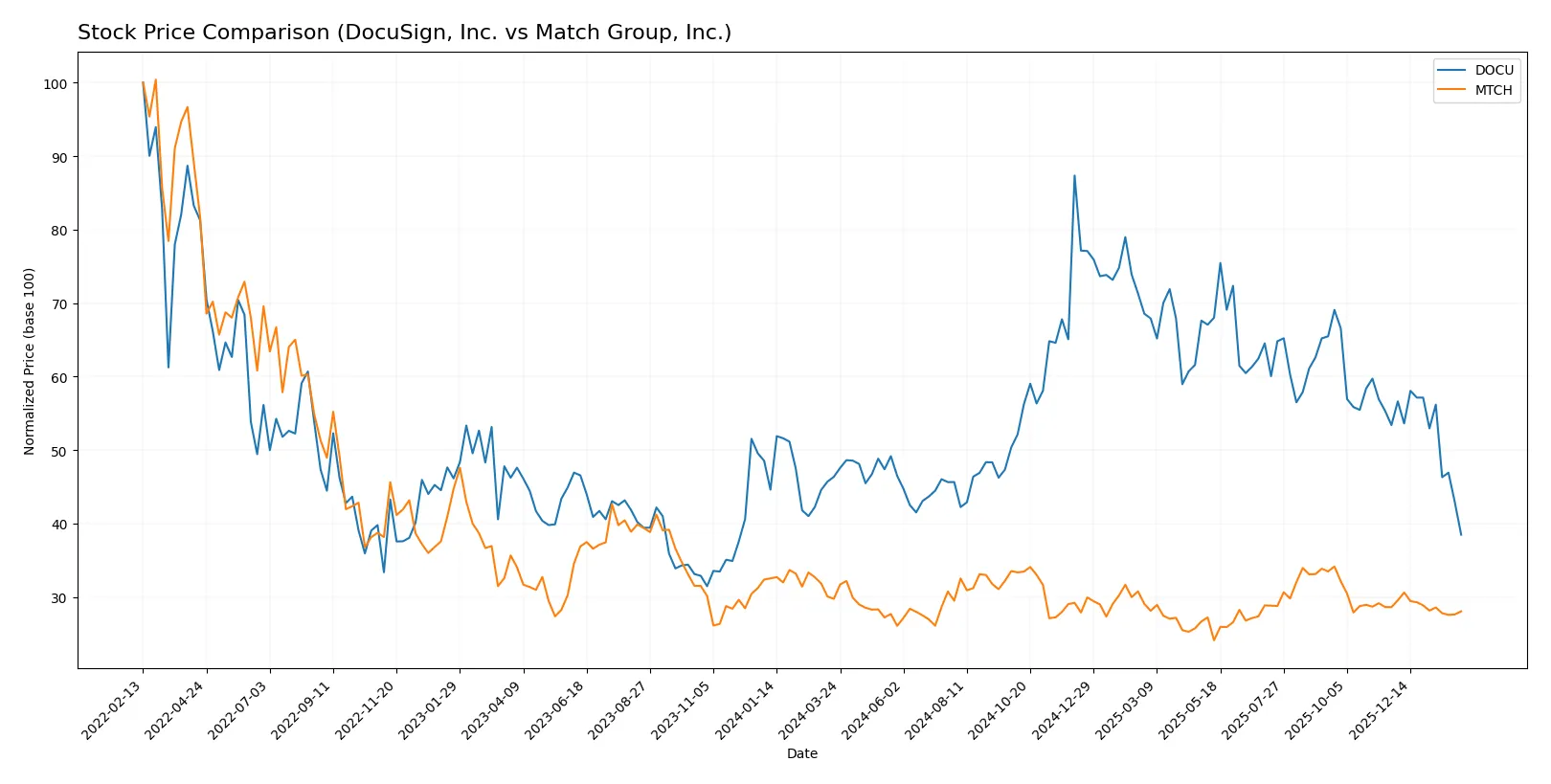

Which stock offers better returns?

Over the past year, both DocuSign, Inc. and Match Group, Inc. faced downward price pressures, with DocuSign showing a sharper decline and more pronounced trading shifts.

Trend Comparison

DocuSign’s stock fell 17.0% over the past year, marking a bearish trend with decelerating losses. It peaked at 107 and bottomed near 47, showing elevated volatility with a 13.07 std deviation.

Match Group’s stock declined 5.7% in the same period, also bearish with deceleration. Its price ranged from 38.5 to 27.2, exhibiting lower volatility at a 2.61 std deviation.

DocuSign underperformed Match Group, delivering the weaker market performance over the past year despite higher volatility and wider price swings.

Target Prices

Analysts present a balanced target price consensus for DocuSign and Match Group, reflecting cautious optimism.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| DocuSign, Inc. | 70 | 88 | 76.86 |

| Match Group, Inc. | 33 | 43 | 36 |

DocuSign’s consensus target at 76.86 significantly exceeds its current 47.13 price, signaling upside potential. Match Group’s 36 consensus also outpaces its 31.63 price, suggesting moderate expected gains.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Here are the latest institutional grades and actions for DocuSign, Inc. and Match Group, Inc.:

DocuSign, Inc. Grades

The table lists recent grades and recommendations from key financial institutions for DocuSign, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| RBC Capital | Maintain | Sector Perform | 2026-01-05 |

| Piper Sandler | Maintain | Neutral | 2025-12-05 |

| RBC Capital | Maintain | Sector Perform | 2025-12-05 |

| B of A Securities | Maintain | Neutral | 2025-12-05 |

| Needham | Maintain | Hold | 2025-12-05 |

| Wedbush | Maintain | Neutral | 2025-12-05 |

| Evercore ISI Group | Maintain | In Line | 2025-12-05 |

| UBS | Maintain | Neutral | 2025-12-05 |

| JP Morgan | Maintain | Neutral | 2025-12-05 |

| Wells Fargo | Maintain | Equal Weight | 2025-12-05 |

Match Group, Inc. Grades

Below are recent grades and recommendations from prominent analysts for Match Group, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| TD Cowen | Maintain | Buy | 2026-02-05 |

| JP Morgan | Maintain | Neutral | 2026-02-04 |

| Truist Securities | Maintain | Hold | 2026-02-04 |

| Morgan Stanley | Maintain | Equal Weight | 2026-01-13 |

| Truist Securities | Maintain | Hold | 2025-11-05 |

| Evercore ISI Group | Maintain | In Line | 2025-11-05 |

| Wells Fargo | Maintain | Equal Weight | 2025-11-05 |

| Morgan Stanley | Maintain | Equal Weight | 2025-10-20 |

| Susquehanna | Maintain | Positive | 2025-08-07 |

| JP Morgan | Maintain | Neutral | 2025-08-06 |

Which company has the best grades?

Match Group, Inc. holds higher ratings overall, including a recent Buy from TD Cowen. DocuSign’s grades mostly cluster around Neutral or Hold. Better grades may indicate stronger institutional confidence and potential investor appeal.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

DocuSign, Inc.

- Faces intense competition in e-signature and contract management software, risking market share erosion.

Match Group, Inc.

- Operates in a crowded dating app space with constant innovation pressure and user engagement challenges.

2. Capital Structure & Debt

DocuSign, Inc.

- Maintains a very low debt-to-assets ratio (3.1%), signaling conservative leverage and manageable financial risk.

Match Group, Inc.

- Carries a high debt-to-assets ratio (89.06%), posing significant financial risk despite favorable interest coverage.

3. Stock Volatility

DocuSign, Inc.

- Exhibits moderate volatility with beta near 1.0, aligning closely with market fluctuations.

Match Group, Inc.

- Shows higher volatility with beta at 1.315, implying greater sensitivity to market swings.

4. Regulatory & Legal

DocuSign, Inc.

- Subject to compliance risks related to digital signatures and data privacy laws globally.

Match Group, Inc.

- Faces regulatory scrutiny over user data protection and evolving online content regulations.

5. Supply Chain & Operations

DocuSign, Inc.

- Relies heavily on cloud infrastructure and software integration partners, exposing it to tech disruptions.

Match Group, Inc.

- Depends on digital platforms with operational risks tied to platform stability and user experience continuity.

6. ESG & Climate Transition

DocuSign, Inc.

- Increasing pressure to enhance ESG disclosures, particularly on data security and energy-efficient data centers.

Match Group, Inc.

- Faces growing expectations on user safety policies and social responsibility in online communities.

7. Geopolitical Exposure

DocuSign, Inc.

- Global footprint subjects it to geopolitical risks affecting cloud services and cross-border data flows.

Match Group, Inc.

- International user base exposes it to regulatory variability and geopolitical tensions impacting operations.

Which company shows a better risk-adjusted profile?

DocuSign’s most impactful risk lies in market competition and operational reliance on cloud partners. Match Group’s critical risk is its heavy debt load coupled with regulatory pressures. Despite DocuSign’s lower debt risk, Match Group’s strong operational metrics and very strong Piotroski score partly offset financial leverage concerns. Overall, DocuSign presents a cleaner balance sheet and moderate volatility, favoring a better risk-adjusted profile in 2026. The extreme leverage and distress-zone Altman Z-Score for Match Group justify caution despite its operational strengths.

Final Verdict: Which stock to choose?

DocuSign’s superpower lies in its impressive efficiency in turning invested capital into profits, demonstrated by a soaring return on equity and rapidly improving profitability. Its main point of vigilance is a weaker liquidity position, which could pressure short-term operations. This stock fits well in an aggressive growth portfolio willing to weather volatility for outsized gains.

Match Group commands a durable strategic moat through its strong brand presence and subscription-based revenue model, ensuring steady cash flow. It offers better liquidity and financial stability compared to DocuSign, but with slower growth momentum. Match Group suits investors focused on GARP—growth at a reasonable price—valuing steady returns and competitive advantages.

If you prioritize rapid profitability expansion and can tolerate liquidity risks, DocuSign stands out due to its accelerating earnings growth. However, if you seek better financial stability and a robust competitive moat with consistent free cash flow, Match Group offers a safer analytical scenario despite modest growth. Each appeals to distinct investor profiles balancing growth and stability.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of DocuSign, Inc. and Match Group, Inc. to enhance your investment decisions: