Home > Comparison > Healthcare > UNH vs CVS

The strategic rivalry between UnitedHealth Group Incorporated and CVS Health Corporation defines the current trajectory of the healthcare plans sector. UnitedHealth operates as a diversified healthcare giant with integrated service segments, while CVS blends retail pharmacy leadership with extensive healthcare benefits. This head-to-head contrasts a vertically integrated model against a retail-driven approach. This analysis aims to reveal which trajectory delivers superior risk-adjusted returns for a diversified portfolio in 2026.

Table of contents

Companies Overview

UnitedHealth Group and CVS Health stand as pillars in the U.S. healthcare sector, shaping insurance and care delivery.

UnitedHealth Group Incorporated: Diversified Healthcare Leader

UnitedHealth Group dominates as a diversified health care company with four segments, including UnitedHealthcare and Optum. It generates revenue primarily through consumer health benefit plans and integrated care services. In 2026, its strategic focus revolves around expanding care delivery networks and optimizing pharmacy services via OptumRx to strengthen competitive advantage.

CVS Health Corporation: Integrated Health Services Provider

CVS Health operates as a leading health services provider combining health care benefits, pharmacy services, and retail clinics. Its revenue engine hinges on pharmacy benefit management and extensive retail pharmacy operations. CVS prioritizes expanding its MinuteClinic footprint and enhancing clinical services to capture more consumer health interactions in 2026.

Strategic Collision: Similarities & Divergences

Both companies pursue vertical integration but differ in approach: UnitedHealth leans on a broad care delivery ecosystem, while CVS integrates retail pharmacy and clinical services. They battle fiercely in pharmacy benefit management and consumer healthcare access. Their investment profiles diverge—UnitedHealth emphasizes diversified service platforms, CVS focuses on retail-healthcare convergence.

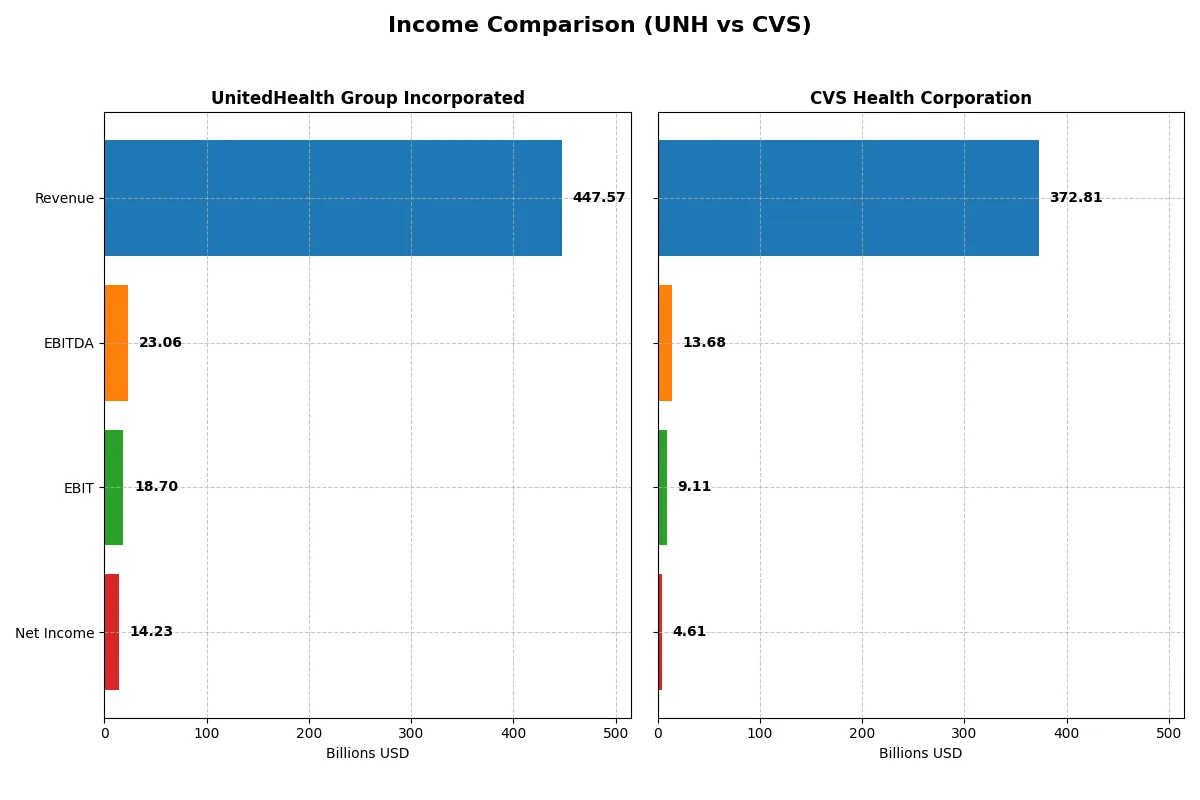

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | UnitedHealth Group (UNH) | CVS Health Corporation (CVS) |

|---|---|---|

| Revenue | 448B | 373B |

| Cost of Revenue | 365B | 321B |

| Operating Expenses | 64B | 43B |

| Gross Profit | 83B | 51B |

| EBITDA | 23B | 14B |

| EBIT | 19B | 9.1B |

| Interest Expense | 4.0B | 3.0B |

| Net Income | 14B | 4.6B |

| EPS | 15.66 | 3.66 |

| Fiscal Year | 2025 | 2024 |

Income Statement Analysis: The Bottom-Line Duel

The following income statement comparison reveals which company converts revenue into profit with greater efficiency and momentum.

UnitedHealth Group Incorporated Analysis

UnitedHealth’s revenue grew strongly by 11.8% in the latest year, reaching $448B, but net income fell slightly to $14.2B. Gross margin contracted to 18.5%, signaling margin pressure despite robust top-line expansion. Operating expenses rose in line with revenue growth, dragging EBIT down 22%, indicating momentum challenges in profitability.

CVS Health Corporation Analysis

CVS posted $373B revenue in 2024, up modestly by 4.2%, while net income halved to $4.6B. Gross margin remained thin at 13.8%, and EBIT dropped 34%, reflecting weaker operational leverage. Expense growth matched revenue, but net margin shrank sharply, highlighting struggles to sustain profitability amid rising costs.

Margin Strength vs. Revenue Growth

UnitedHealth’s superior revenue scale and healthier margins contrast sharply with CVS’s narrower margin and slower growth. Despite recent profit declines, UnitedHealth maintains a stronger fundamental profile with higher operating efficiency. For investors, UnitedHealth’s blend of growth and margin resilience offers a more compelling earnings engine than CVS’s pressured profitability.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | UnitedHealth Group (UNH) | CVS Health (CVS) |

|---|---|---|

| ROE | 14.2% | 6.1% |

| ROIC | 9.4% | 3.6% |

| P/E | 21.1x | 12.2x |

| P/B | 3.0x | 0.75x |

| Current Ratio | 0.79 | 0.81 |

| Quick Ratio | 0.79 | 0.60 |

| D/E (Debt-to-Equity) | 0.78 | 1.10 |

| Debt-to-Assets | 25.3% | 32.7% |

| Interest Coverage | 4.7x | 2.9x |

| Asset Turnover | 1.45 | 1.47 |

| Fixed Asset Turnover | 0 | 12.9 |

| Payout Ratio | 97.2% | 73.1% |

| Dividend Yield | 4.6% | 6.0% |

| Fiscal Year | 2025 | 2024 |

Efficiency & Valuation Duel: The Vital Signs

Ratios act as a company’s DNA, revealing hidden risks and operational excellence beneath headline figures.

UnitedHealth Group Incorporated

UnitedHealth displays a neutral ROE of 14.2% and a modest net margin of 3.18%, indicating steady profitability. Its P/E ratio at 21.1 suggests a fairly valued stock, but a high P/B ratio flags some valuation stretch. The 4.6% dividend yield rewards shareholders while signaling disciplined capital returns.

CVS Health Corporation

CVS posts weaker profitability with a 6.1% ROE and 1.24% net margin, reflecting operational challenges. Its attractive P/E of 12.3 and low P/B of 0.75 mark it as undervalued. The near 6% dividend yield provides steady income, offsetting modest growth prospects amid elevated debt levels.

Balanced Profitability vs. Value Opportunity

UnitedHealth offers stronger returns but trades at a higher valuation with mixed ratio signals. CVS appears cheaper with a better dividend yield but weaker profitability and higher leverage. Risk-tolerant investors may prefer CVS’s value profile, while those prioritizing stable returns might lean toward UnitedHealth.

Which one offers the Superior Shareholder Reward?

UnitedHealth Group (UNH) offers a more balanced and sustainable shareholder reward than CVS Health (CVS). UNH pays a moderate dividend yield of 1.6% in 2025 with a payout ratio near 52%, supported by strong free cash flow coverage (85%). It pairs dividends with an active buyback strategy, enhancing total return. CVS yields a higher 5.97% dividend but at a steep 73% payout ratio and weaker free cash flow coverage (69%), signaling less sustainability. CVS’s buyback activity is lower, reducing total shareholder return potential. Historically in health services, a prudent payout with buybacks like UNH’s sustains growth and shields investors through market cycles. I judge UNH’s combination of dividends and buybacks delivers superior long-term total return in 2026.

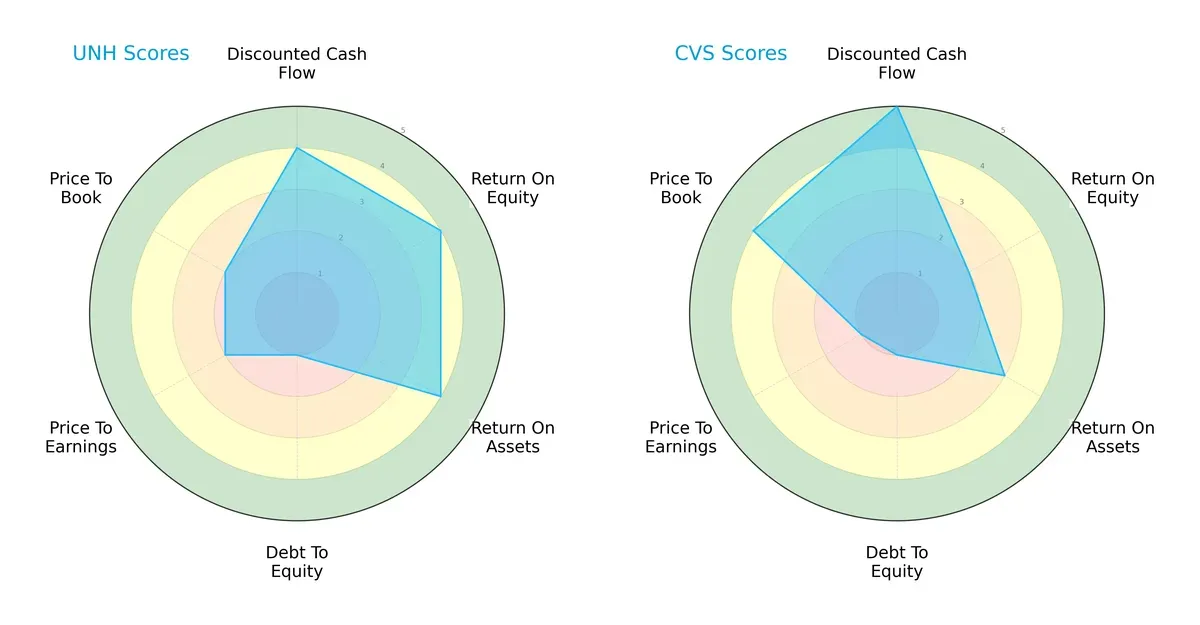

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of both firms, highlighting their financial strengths and valuation nuances:

UnitedHealth Group shows balanced strength in DCF, ROE, and ROA, reflecting operational efficiency. CVS excels in DCF and price-to-book valuation but lags in ROE, indicating reliance on valuation appeal rather than profitability. Both share weak debt-to-equity scores, signaling elevated leverage risks. UnitedHealth’s profile is more balanced; CVS depends on specific valuation advantages.

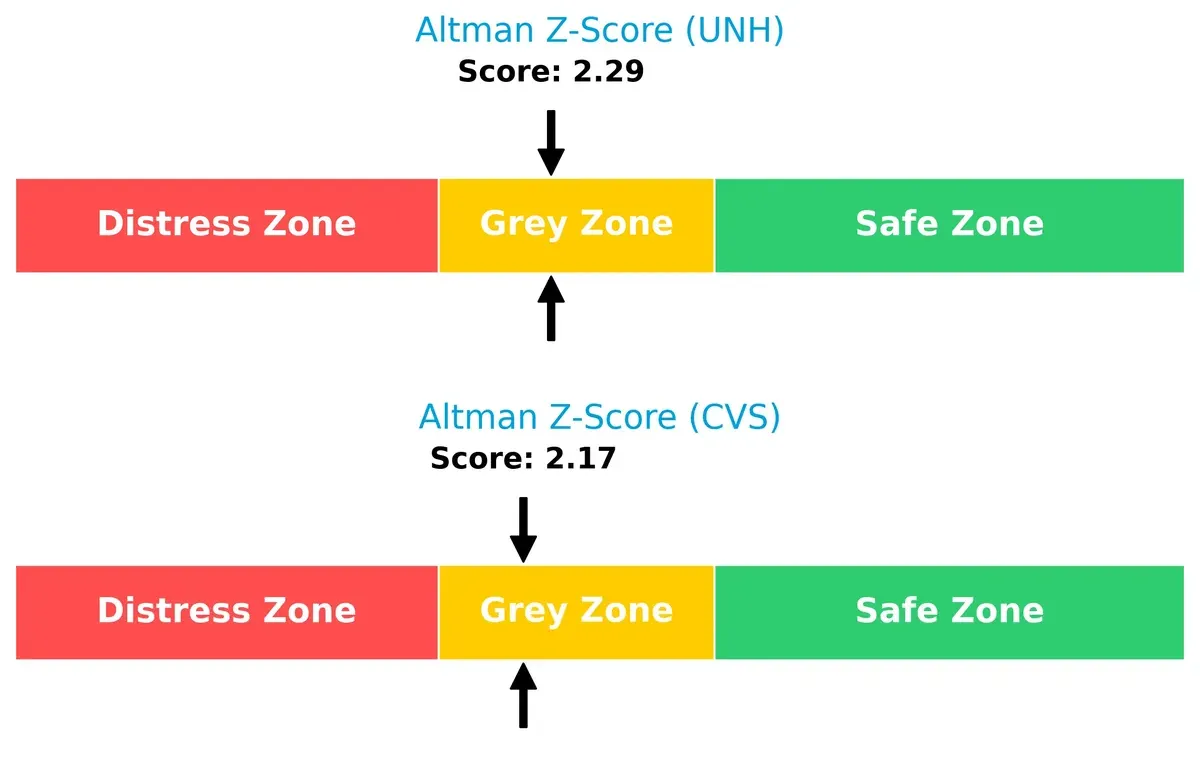

Bankruptcy Risk: Solvency Showdown

The Altman Z-Scores place both companies in the grey zone, implying moderate bankruptcy risk in this cycle:

UnitedHealth’s 2.29 slightly edges CVS’s 2.17, suggesting marginally better financial stability. Neither is in the safe zone, so investors should monitor leverage and liquidity closely.

Financial Health: Quality of Operations

Both firms score a 7 on the Piotroski F-Score, indicating strong operational quality and financial health:

This parity suggests both companies maintain solid profitability, efficient asset use, and prudent capital management, with no immediate red flags in internal metrics.

How are the two companies positioned?

This section dissects the operational DNA of UNH and CVS by comparing their revenue distribution by segment and internal dynamics—strengths and weaknesses. The final objective is to confront their economic moats and identify which business model offers the most resilient competitive advantage today.

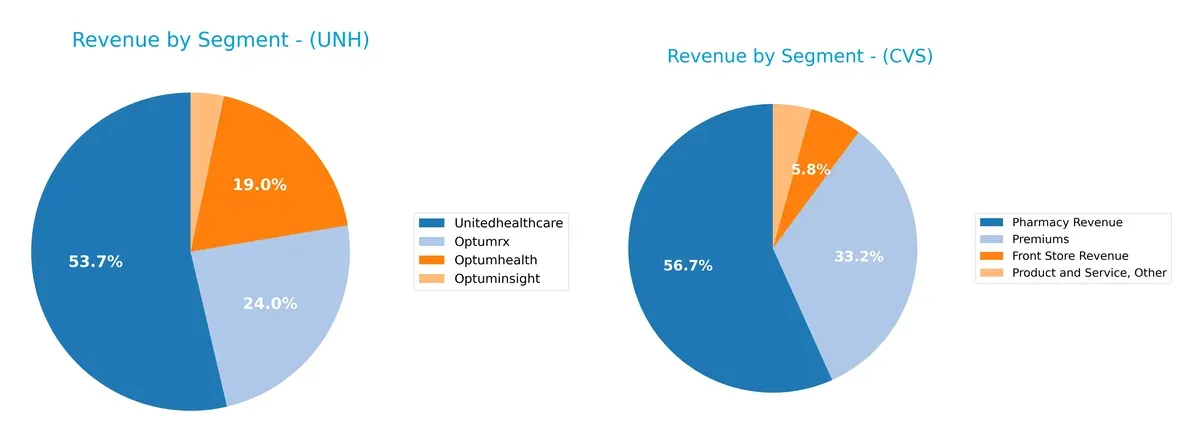

Revenue Segmentation: The Strategic Mix

The following comparison dissects how UnitedHealth Group and CVS Health diversify their income streams and where their primary sector bets lie:

UnitedHealth Group anchors revenue in UnitedHealthcare at $298B, complemented by strong Optum segments totaling $257B, showing a balanced ecosystem approach. CVS Health pivots on Pharmacy Revenue at $210B and Premiums at $123B, but Front Store and other services lag behind. UnitedHealth’s diversification reduces concentration risk, while CVS’s reliance on pharmacy and premiums suggests vulnerability to regulatory shifts and competitive pricing pressures.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of UnitedHealth Group Incorporated (UNH) and CVS Health Corporation (CVS):

UNH Strengths

- Diversified revenue from Optumhealth, Optuminsight, Optumrx, UnitedHealthcare segments

- Favorable WACC at 5.4% supports capital efficiency

- Strong asset turnover at 1.45 indicates efficient use of assets

- Dividend yield of 4.6% appeals to income-focused investors

CVS Strengths

- Favorable valuation metrics with P/E at 12.25 and P/B at 0.75

- High fixed asset turnover at 12.88 shows strong operational efficiency

- Favorable WACC at 4.55% indicates low capital cost

- Diversified revenue including pharmacy, front store, and premiums segments

UNH Weaknesses

- Low current and quick ratios at 0.79 signal liquidity concerns

- Unfavorable net margin at 3.18% limits profitability

- Unfavorable P/B ratio at 3.0 suggests overvaluation risk

- Fixed asset turnover at 0 is a red flag for asset utilization

CVS Weaknesses

- Unfavorable profitability metrics with net margin 1.24%, ROE 6.11%, ROIC 3.61%

- Debt-to-equity at 1.1 and unfavorable D/E ratio indicate higher leverage risk

- Low quick ratio at 0.6 reflects weak short-term liquidity

- Dividend yield neutral at 5.97% lacks strong income incentive

UnitedHealth benefits from scale and diversified segments but faces liquidity and valuation issues. CVS shows operational efficiency and attractive valuation but struggles with profitability and leverage. These contrasts shape each company’s strategic financial priorities going forward.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only reliable defense that protects long-term profits from relentless competition erosion. Let’s dissect the competitive moats of two healthcare giants:

UnitedHealth Group Incorporated: Integrated Healthcare Ecosystem

UnitedHealth’s moat stems from its integrated care delivery and data-driven services. This synergy supports a solid ROIC above WACC, signaling value creation despite a recent dip. Expansion in personalized care and data analytics could deepen its moat in 2026.

CVS Health Corporation: Retail-Pharmacy Network

CVS leverages its extensive retail and pharmacy network as a cost advantage moat. However, its ROIC lags below WACC, indicating value destruction and a weakening competitive edge. Market disruption and digital health advances pose both risks and chances for renewal.

Integrated Care Synergy vs. Retail Footprint Resilience

UnitedHealth’s integrated ecosystem builds a wider, more durable moat than CVS’s retail-pharmacy model, which currently struggles with profitability. UnitedHealth is better positioned to defend and expand market share amid evolving healthcare demands.

Which stock offers better returns?

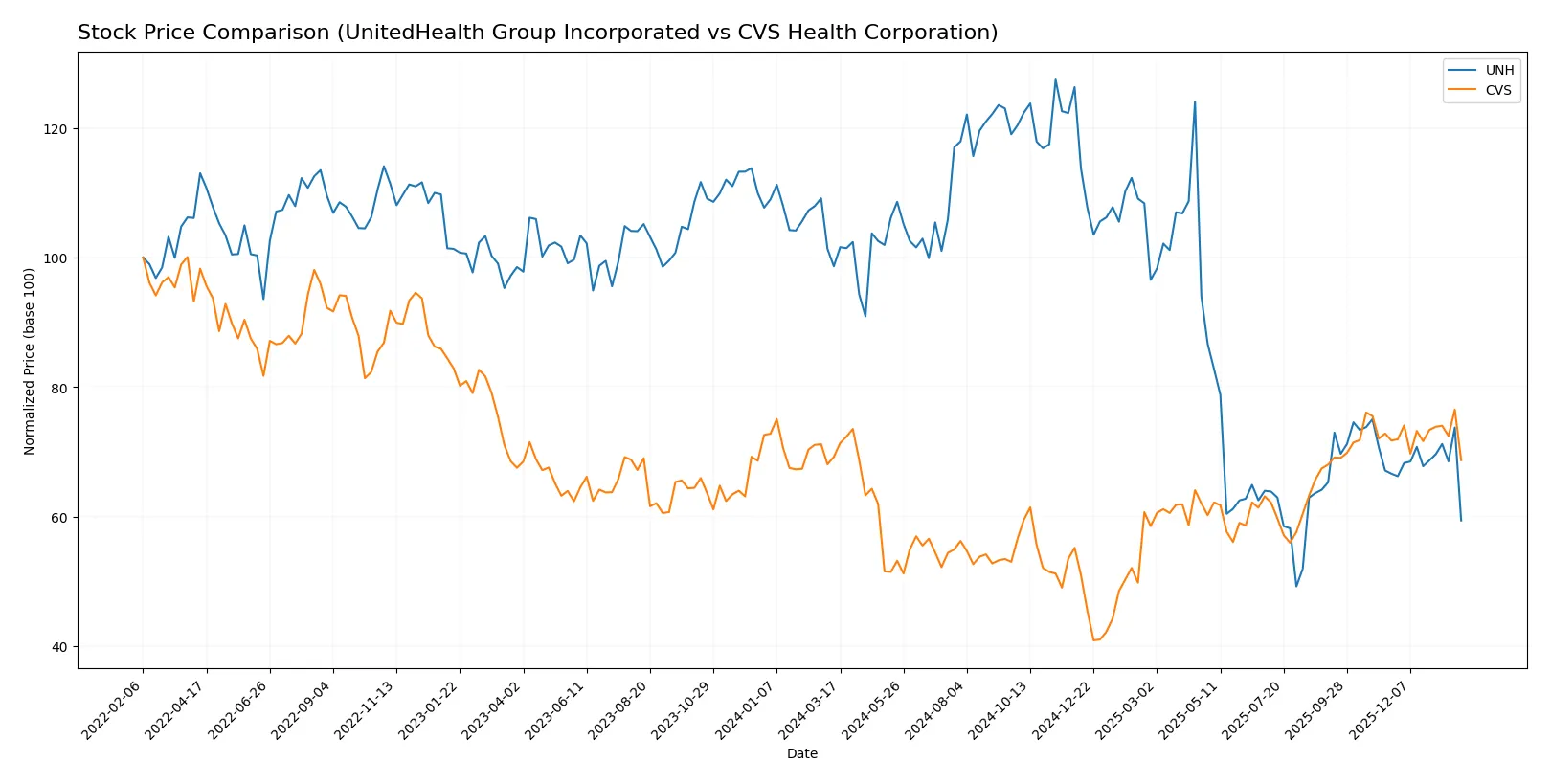

Over the past 12 months, UnitedHealth Group and CVS Health displayed distinct price trajectories marked by significant declines and shifting trading dynamics.

Trend Comparison

UnitedHealth Group’s stock fell sharply by 39.79% over the past year, showing an accelerating bearish trend. The price ranged widely between 238 and 616, reflecting high volatility (std. dev. 109.55).

CVS Health’s stock declined slightly by 0.73%, maintaining a bearish but decelerating trend. The price moved between 44 and 83 with lower volatility (std. dev. 9.38).

UnitedHealth’s decline was far steeper than CVS’s, resulting in CVS delivering the higher market performance over the past year.

Target Prices

Analysts present a moderately bullish target consensus for UnitedHealth Group and a cautiously optimistic outlook for CVS Health.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| UnitedHealth Group Incorporated | 327 | 444 | 387.88 |

| CVS Health Corporation | 90 | 103 | 94.92 |

UnitedHealth’s consensus target at $388 significantly exceeds its current $287 price, indicating upside potential. CVS’s $95 consensus target also surpasses its $75 price, but with less margin, reflecting tempered expectations.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Below is the comparison of recent institutional grades for UnitedHealth Group Incorporated and CVS Health Corporation:

UnitedHealth Group Incorporated Grades

This table summarizes recent grades from major financial institutions for UnitedHealth Group Incorporated.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Wells Fargo | Maintain | Overweight | 2026-01-30 |

| Barclays | Maintain | Overweight | 2026-01-30 |

| Leerink Partners | Maintain | Outperform | 2026-01-28 |

| RBC Capital | Maintain | Outperform | 2026-01-28 |

| UBS | Maintain | Buy | 2026-01-28 |

| Oppenheimer | Maintain | Outperform | 2026-01-28 |

| Jefferies | Maintain | Buy | 2026-01-28 |

| Morgan Stanley | Maintain | Overweight | 2026-01-23 |

| Barclays | Maintain | Overweight | 2026-01-05 |

| TD Cowen | Maintain | Hold | 2025-10-30 |

CVS Health Corporation Grades

This table shows recent institutional grades for CVS Health Corporation from various well-known firms.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Argus Research | Maintain | Buy | 2026-01-28 |

| B of A Securities | Maintain | Buy | 2026-01-27 |

| JP Morgan | Maintain | Overweight | 2025-12-17 |

| Bernstein | Maintain | Market Perform | 2025-12-12 |

| Baird | Maintain | Outperform | 2025-12-10 |

| Truist Securities | Maintain | Buy | 2025-12-10 |

| Morgan Stanley | Maintain | Overweight | 2025-12-10 |

| Barclays | Maintain | Overweight | 2025-12-10 |

| Piper Sandler | Maintain | Overweight | 2025-12-10 |

| Mizuho | Maintain | Outperform | 2025-12-10 |

Which company has the best grades?

UnitedHealth Group consistently receives top-tier ratings like Buy and Outperform from multiple firms. CVS shows a mix of Buy, Overweight, and Outperform ratings but also some Market Perform grades. Investors may view UnitedHealth’s grades as signaling stronger consensus confidence.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

UnitedHealth Group Incorporated

- Dominates diversified healthcare services with strong Optum segments. Faces intense competition in insurance and care delivery.

CVS Health Corporation

- Operates broad health services and retail pharmacy. Competes heavily in pharmacy benefits and walk-in clinics.

2. Capital Structure & Debt

UnitedHealth Group Incorporated

- Moderate debt-to-equity (0.78), favorable debt-to-assets (25.3%). Interest coverage neutral at 4.67x.

CVS Health Corporation

- Higher debt-to-equity (1.1), debt-to-assets 32.75%. Interest coverage weaker at 3.08x, signaling elevated leverage risk.

3. Stock Volatility

UnitedHealth Group Incorporated

- Low beta of 0.425 suggests defensive, stable stock behavior.

CVS Health Corporation

- Slightly higher beta of 0.484 indicates more price sensitivity to market swings.

4. Regulatory & Legal

UnitedHealth Group Incorporated

- Subject to healthcare plan regulations and Medicaid policies. Regulatory shifts could impact margins.

CVS Health Corporation

- Faces scrutiny on pharmacy benefit management and retail clinic operations. Complex regulatory environment.

5. Supply Chain & Operations

UnitedHealth Group Incorporated

- Extensive healthcare network and pharmacy services require robust supply chain. Operational complexity is high but well managed.

CVS Health Corporation

- Heavy reliance on retail distribution and pharmacy supply chain. Vulnerable to disruptions in drug supply and logistics.

6. ESG & Climate Transition

UnitedHealth Group Incorporated

- Increasing focus on sustainable healthcare practices and social responsibility. ESG efforts gaining investor attention.

CVS Health Corporation

- ESG initiatives growing, especially in community health and environmental impact of retail operations.

7. Geopolitical Exposure

UnitedHealth Group Incorporated

- Primarily US-based; limited international exposure reduces geopolitical risk.

CVS Health Corporation

- Also US-centric with minimal global footprint, concentrating risk domestically.

Which company shows a better risk-adjusted profile?

UnitedHealth faces moderate leverage and regulatory risks but benefits from a stable stock and diversified operations. CVS carries higher financial leverage and regulatory pressure but offers a slightly more favorable valuation. Both firms are in the “grey zone” for Altman Z-scores, indicating moderate bankruptcy risk. UnitedHealth’s stronger interest coverage and lower beta suggest a better risk-adjusted profile. Notably, CVS’s higher debt-to-equity and weaker interest coverage raise concerns amid tightening credit conditions.

Final Verdict: Which stock to choose?

UnitedHealth Group’s superpower lies in its consistent value creation through efficient capital allocation and robust asset turnover. Its main point of vigilance is declining profitability, signaling the need to monitor margin pressures closely. It suits investors targeting Aggressive Growth with a tolerance for cyclical swings.

CVS Health’s strategic moat stems from its integrated healthcare services and stable recurring revenue streams. While it carries more financial leverage risk than UnitedHealth, it offers better valuation appeal and a more defensive profile. It fits well in GARP portfolios seeking steady income with moderate growth.

If you prioritize dynamic growth underpinned by strong capital efficiency, UnitedHealth outshines due to its superior ROIC over WACC and operational leverage. However, if you seek relative stability and value with a conservative risk appetite, CVS offers better downside protection despite its weaker profitability. Both demand careful risk management given their margin and leverage challenges.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of UnitedHealth Group Incorporated and CVS Health Corporation to enhance your investment decisions: