Home > Comparison > Healthcare > CVS vs CNC

The strategic rivalry between CVS Health Corporation and Centene Corporation shapes the healthcare plans industry’s evolution. CVS operates a diversified model combining retail, pharmacy services, and health benefits. Centene focuses on managed care for under-insured populations, mainly through government subsidized programs. This analysis contrasts their operational strategies to determine which offers superior risk-adjusted returns for a diversified portfolio navigating healthcare’s complex regulatory landscape.

Table of contents

Companies Overview

CVS Health Corporation and Centene Corporation stand as pivotal players in the US healthcare plans market, shaping access and delivery.

CVS Health Corporation: Integrated Healthcare Giant

CVS Health Corporation dominates as a health services provider with robust segments in health care benefits, pharmacy services, and retail. Its core revenue derives from insurance products, pharmacy benefit management, and retail pharmacy sales. In 2026, CVS focuses strategically on expanding clinical services via its extensive retail footprint and MinuteClinic locations to enhance patient care accessibility.

Centene Corporation: Managed Care Specialist

Centene Corporation operates as a multi-national healthcare enterprise specializing in managed care for under-insured populations. Its revenue engine centers on government-subsidized health plans like Medicaid and Medicare. The 2026 strategy prioritizes broadening specialty services and government program coverage, targeting vulnerable groups with tailored care coordination and social support integration.

Strategic Collision: Similarities & Divergences

Both companies compete within the healthcare plans sector but diverge in approach: CVS emphasizes an integrated care model combining retail and clinical services, while Centene focuses on government-funded managed care for underserved demographics. Their primary battleground lies in market share across public and private health insurance segments. This contrast highlights CVS’s scale-driven diversification versus Centene’s niche specialization, shaping distinct risk and growth profiles.

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines, revealing who dominates the bottom line in their most recent fiscal year:

| Metric | CVS Health Corporation (CVS) | Centene Corporation (CNC) |

|---|---|---|

| Revenue | 373B | 195B |

| Cost of Revenue | 321B | 171B |

| Operating Expenses | 43B | 31B |

| Gross Profit | 51B | 24B |

| EBITDA | 13.7B | -5.1B |

| EBIT | 9.1B | -6.4B |

| Interest Expense | 3B | 678M |

| Net Income | 4.6B | -6.7B |

| EPS | 3.66 | -13.61 |

| Fiscal Year | 2024 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals the true efficiency and profitability of two healthcare giants over recent years.

CVS Health Corporation Analysis

CVS’s revenue climbed steadily, reaching $373B in 2024, yet net income slid to $4.6B, down from $8.3B in 2023. Gross margin weakened to 13.8%, and net margin contracted to 1.24%. The sharp decline in EBIT and net income margins signals operational pressures despite revenue growth, reflecting margin compression and cost challenges.

Centene Corporation Analysis

Centene’s revenue jumped 19.4% to $195B in 2025, with gross profit rising 41.6%. However, net income plummeted to a $6.7B loss, dragging net margin to -3.43%. EBIT margin turned deeply negative at -3.29%, indicating severe profitability issues despite top-line momentum. Rising operating expenses offset revenue gains, eroding bottom-line results.

Margin Stability vs. Growth Struggles

CVS shows more stable but shrinking profitability amid steady revenue gains, while Centene experiences rapid revenue growth offset by heavy losses and negative margins. CVS’s positive net income, though diminished, contrasts sharply with Centene’s deep net losses. For investors, CVS presents a more consistent, albeit challenged, earnings profile versus Centene’s volatile growth with significant profitability risk.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | CVS Health Corporation (CVS) | Centene Corporation (CNC) |

|---|---|---|

| ROE | 6.11% (2024) | -33.44% (2025) |

| ROIC | 3.61% (2024) | -18.85% (2025) |

| P/E | 12.25 (2024) | -3.03 (2025) |

| P/B | 0.75 (2024) | 1.01 (2025) |

| Current Ratio | 0.81 (2024) | 1.10 (2025) |

| Quick Ratio | 0.60 (2024) | 1.10 (2025) |

| D/E (Debt-to-Equity) | 1.10 (2024) | 0.87 (2025) |

| Debt-to-Assets | 32.7% (2024) | 22.7% (2025) |

| Interest Coverage | 2.88 (2024) | -11.24 (2025) |

| Asset Turnover | 1.47 (2024) | 2.54 (2025) |

| Fixed Asset Turnover | 12.88 (2024) | 95.62 (2025) |

| Payout Ratio | 73.1% (2024) | 0% (2025) |

| Dividend Yield | 5.97% (2024) | 0% (2025) |

| Fiscal Year | 2024 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as a company’s DNA, revealing hidden risks and operational excellence that shape investor decisions.

CVS Health Corporation

CVS posts a modest 6.11% ROE and a thin 1.24% net margin, signaling limited profitability. Its valuation appears reasonable with a 12.25 P/E and 0.75 P/B, indicating the stock is fairly valued. CVS supports shareholders with a 5.97% dividend yield, reflecting steady income over aggressive reinvestment.

Centene Corporation

Centene struggles with a negative 33.44% ROE and a -3.43% net margin, highlighting operational challenges. Its P/E stands at -3.03, which is unusual but marked favorable due to accounting factors. The company pays no dividend, prioritizing internal growth and operational turnaround instead.

Balanced Valuation Meets Operational Reality

CVS offers a stable valuation and dividend income despite subdued profitability, while Centene presents a riskier profile with losses but some favorable efficiency metrics. Investors seeking income and stability may lean toward CVS; those willing to tolerate volatility for growth may consider Centene’s turnaround potential.

Which one offers the Superior Shareholder Reward?

I see CVS Health delivers a 5.97% dividend yield with a 73% payout ratio, signaling strong shareholder returns but tight free cash flow coverage. CVS pairs dividends with moderate buybacks, balancing income and capital return. Centene pays no dividends, focusing on growth and free cash flow reinvestment, with aggressive buybacks in recent years. CVS’s distribution is sustainable given stable cash flow despite leverage. Centene’s lack of dividends poses higher risk but potential growth upside. For 2026, I favor CVS for consistent, safer total returns; Centene suits growth-seeking investors willing to accept volatility.

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of CVS Health Corporation and Centene Corporation, highlighting their distinct financial strengths and weaknesses:

CVS shows a more balanced financial profile with strong discounted cash flow (DCF) and price-to-book (P/B) scores. However, it struggles with debt-to-equity and valuation metrics. Centene relies heavily on DCF strength but suffers from weak profitability (ROE, ROA) and the same debt concerns. CVS maintains a broader financial footing, while Centene depends on a singular valuation edge.

Bankruptcy Risk: Solvency Showdown

CVS and Centene both fall into the Altman Z-Score grey zone, indicating moderate bankruptcy risk in this cycle:

CVS’s score of 2.19 versus Centene’s 2.68 suggests both face financial stress but Centene holds a slightly better buffer against insolvency risks, though neither is in a fully safe zone.

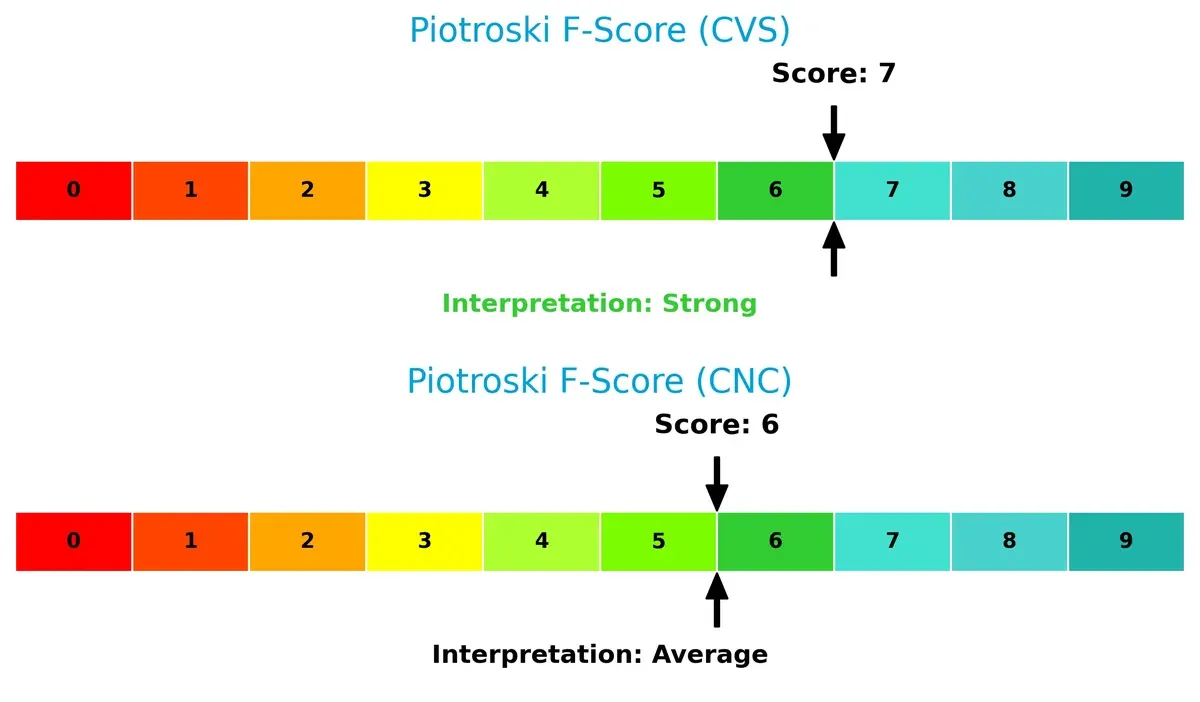

Financial Health: Quality of Operations

CVS leads with a Piotroski F-Score of 7, indicating strong internal financial health compared to Centene’s average score of 6:

CVS’s higher score signals better profitability, liquidity, and efficiency metrics. Centene’s marginally weaker score flags potential internal operational red flags, urging caution for investors seeking robust fundamentals.

How are the two companies positioned?

This section dissects CVS and Centene’s operational DNA by comparing revenue distribution and internal strengths and weaknesses. The goal is to confront their economic moats and identify which model offers the most resilient competitive advantage today.

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how CVS Health Corporation and Centene Corporation diversify their income streams and reveals where their primary sector bets lie:

CVS anchors revenue in Pharmacy ($210B) and Premiums ($123B), with Front Store adding $21.5B, showing a balanced but Pharmacy-heavy mix. Centene pivots on Medicaid ($124B) and Commercial ($33.7B) segments, with a smaller $4.9B Other segment. CVS’s strategy reflects ecosystem lock-in across services and retail, while Centene’s heavy Medicaid reliance poses concentration risk but leverages government healthcare infrastructure dominance.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of CVS Health Corporation and Centene Corporation:

CVS Strengths

- Diversified revenue streams including pharmacy, premiums, and front store segments

- Favorable valuation metrics: PE at 12.25, PB at 0.75

- Asset turnover metrics indicate efficient asset use (1.47 and 12.88)

CNC Strengths

- Favorable capital structure with lower debt-to-assets at 22.67%

- Strong asset turnover ratios (2.54 and 95.62) indicating operational efficiency

- Favorable quick ratio at 1.1 showing liquidity strength

CVS Weaknesses

- Unfavorable profitability metrics: low net margin (1.24%), ROE (6.11%), and ROIC (3.61%)

- Weak liquidity ratios with current ratio 0.81 and quick ratio 0.6

- High debt-to-equity at 1.1 signals leverage risk

CNC Weaknesses

- Negative profitability with net margin -3.43%, ROE -33.44%, and ROIC -18.85%

- Interest coverage negative at -9.46, indicating difficulty covering debt costs

- No dividend yield reflecting lack of shareholder returns

CVS demonstrates strengths in diversification and valuation but suffers from weak profitability and liquidity pressures. Centene shows operational efficiency and a sound balance sheet yet faces severe profitability challenges and debt servicing risks. Both companies must address profitability to sustain competitive positioning.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the critical barrier protecting long-term profits from relentless competition erosion. Let’s dissect the core moats of CVS Health and Centene Corporation:

CVS Health Corporation: Integrated Healthcare Ecosystem

CVS leverages an integrated healthcare model combining retail, pharmacy benefits, and insurance. Its moat shows in stable gross margins despite margin pressures. Expansion into digital health services could either deepen or strain this moat in 2026.

Centene Corporation: Government-Focused Medicaid Specialist

Centene’s moat centers on Medicaid and government program expertise, differentiating it from CVS’s broader model. Despite strong revenue growth, its negative EBIT margin signals profitability challenges. Market expansion into new state programs offers growth but risks margin dilution.

Network Integration vs. Government Program Focus: Moat Strength Showdown

Both CVS and Centene face shrinking ROICs well below WACC, signaling value destruction. However, CVS’s diversified healthcare ecosystem offers a wider moat than Centene’s niche Medicaid focus. CVS is better positioned to defend market share amid evolving healthcare policies.

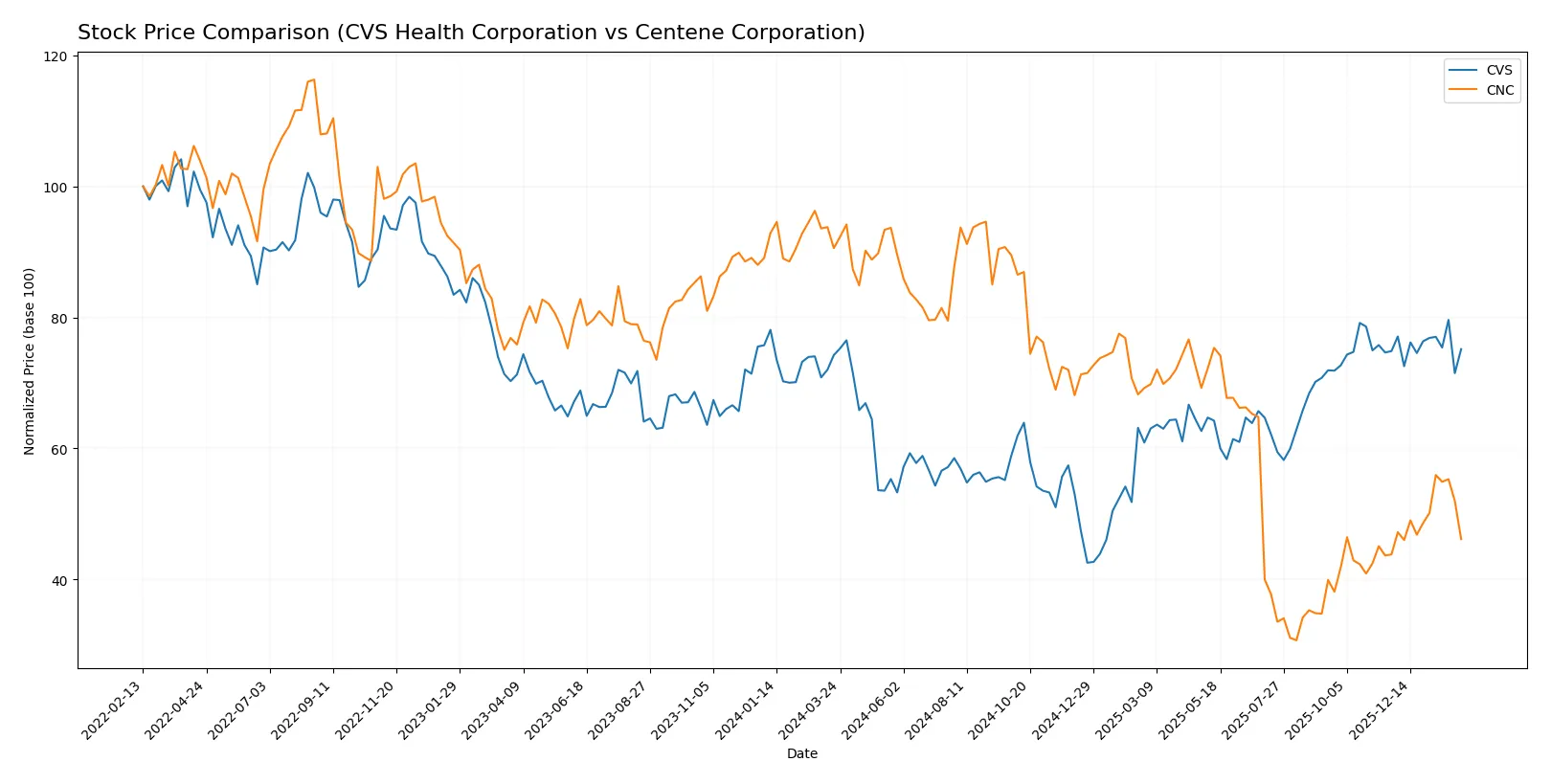

Which stock offers better returns?

Over the past year, CVS Health Corporation showed modest price growth with slowing momentum, while Centene Corporation faced a sharp decline but recently gained upward traction.

Trend Comparison

CVS Health Corporation’s stock increased 1.23% over 12 months, marking a bullish but decelerating trend with prices ranging from 44.36 to 83.01.

Centene Corporation’s stock declined 49.04% over the same period, reflecting a strong bearish trend with accelerating losses despite a recent 5.37% rebound.

Centene’s decline significantly outweighed CVS’s modest gain, positioning CVS as the higher-performing stock in market returns over the past year.

Target Prices

Analysts show a well-defined target consensus for both CVS Health Corporation and Centene Corporation.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| CVS Health Corporation | 90 | 103 | 94.92 |

| Centene Corporation | 38 | 59 | 45.67 |

The consensus target for CVS at $94.92 implies upside potential from the current $78.35 price. Centene’s $45.67 target also suggests moderate gains above its $38.46 market price. Analysts expect steady growth for both healthcare firms.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

CVS Health Corporation Grades

The following table summarizes recent grades from reputable institutions for CVS Health Corporation:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Argus Research | Maintain | Buy | 2026-01-28 |

| B of A Securities | Maintain | Buy | 2026-01-27 |

| JP Morgan | Maintain | Overweight | 2025-12-17 |

| Bernstein | Maintain | Market Perform | 2025-12-12 |

| Morgan Stanley | Maintain | Overweight | 2025-12-10 |

| Truist Securities | Maintain | Buy | 2025-12-10 |

| Barclays | Maintain | Overweight | 2025-12-10 |

| Piper Sandler | Maintain | Overweight | 2025-12-10 |

| Mizuho | Maintain | Outperform | 2025-12-10 |

| UBS | Maintain | Buy | 2025-12-10 |

Centene Corporation Grades

The following table shows recent grades from reputable institutions for Centene Corporation:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Wells Fargo | Maintain | Equal Weight | 2026-01-07 |

| Barclays | Upgrade | Overweight | 2026-01-05 |

| Bernstein | Maintain | Outperform | 2025-11-21 |

| Wells Fargo | Maintain | Equal Weight | 2025-11-12 |

| JP Morgan | Maintain | Neutral | 2025-11-04 |

| Barclays | Maintain | Equal Weight | 2025-11-04 |

| TD Cowen | Maintain | Hold | 2025-10-31 |

| Goldman Sachs | Maintain | Sell | 2025-10-31 |

| Cantor Fitzgerald | Maintain | Neutral | 2025-10-30 |

| Truist Securities | Maintain | Buy | 2025-10-30 |

Which company has the best grades?

CVS Health Corporation generally holds stronger grades, with multiple “Buy” and “Overweight” ratings from top-tier firms. Centene shows a wider range, including “Sell” and “Hold” grades. This contrast may affect investor confidence and perceived stability between the two.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

CVS Health Corporation

- Large scale and diversified retail and services segment supports competitive moats in healthcare plans.

Centene Corporation

- Focused on government-subsidized programs, facing intense competition and margin pressure in Medicaid and Medicare markets.

2. Capital Structure & Debt

CVS Health Corporation

- High debt-to-equity ratio at 1.1 signals leveraged balance sheet, increasing financial risk.

Centene Corporation

- Lower debt-to-equity ratio at 0.87 indicates a somewhat healthier capital structure. Interest coverage negative, raising solvency concerns.

3. Stock Volatility

CVS Health Corporation

- Beta of 0.50 suggests low stock volatility, appealing for risk-averse investors.

Centene Corporation

- Beta of 0.49 also signals low volatility, though recent share price decline raises caution.

4. Regulatory & Legal

CVS Health Corporation

- Regulatory risks in pharmacy benefit management and healthcare services remain elevated.

Centene Corporation

- Heavy reliance on government programs exposes Centene to policy shifts and reimbursement rate risks.

5. Supply Chain & Operations

CVS Health Corporation

- Extensive retail footprint with 9,900 locations offers operational scale but risks from supply disruptions.

Centene Corporation

- Operational focus on managed care limits supply chain risks but depends on provider networks’ stability.

6. ESG & Climate Transition

CVS Health Corporation

- ESG initiatives underway but exposure to pharmaceutical waste and energy use remain challenges.

Centene Corporation

- ESG risks tied to social determinants of health and transparency in government healthcare programs.

7. Geopolitical Exposure

CVS Health Corporation

- Primarily US-based with limited international exposure, reducing geopolitical risk.

Centene Corporation

- Also US-focused but reliant on state Medicaid programs, making it sensitive to regional political changes.

Which company shows a better risk-adjusted profile?

CVS’s greatest risk lies in its leveraged capital structure, which strains financial flexibility. Centene’s critical risk is its negative profitability and weak interest coverage, signaling potential distress. Despite CVS’s leverage, its stronger operational scale and stable cash flows provide a more balanced risk profile. Centene’s negative margins and debt servicing issues heighten its vulnerability. Recent data shows Centene’s interest coverage at -9.46, a red flag for solvency, while CVS maintains positive coverage at 3.08. This evidence positions CVS as the better risk-adjusted investment in 2026.

Final Verdict: Which stock to choose?

CVS Health Corporation’s superpower lies in its robust asset turnover and favorable valuation metrics, signaling operational efficiency despite profitability headwinds. Its point of vigilance is a stretched liquidity position, which raises short-term risk concerns. CVS suits investors with an appetite for stable cash flow and dividend income underpinned by scale.

Centene Corporation’s moat is rooted in its lean balance sheet and efficient capital deployment, reflected in solid asset turnover and low leverage. Relative to CVS, Centene offers a cleaner liquidity profile but wrestles with deeply negative profitability and value creation metrics. It fits portfolios seeking turnaround potential with a tolerance for volatility.

If you prioritize operational scale and steady cash generation, CVS is the compelling choice due to its efficient asset use and valuation appeal. However, if you seek turnaround growth and balance sheet resilience, Centene offers better stability amid restructuring risks. Both require cautious risk management given their value destruction signals.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of CVS Health Corporation and Centene Corporation to enhance your investment decisions: