Home > Comparison > Industrials > CMI vs OTIS

The strategic rivalry between Cummins Inc. and Otis Worldwide defines the trajectory of the industrial machinery sector. Cummins operates as a capital-intensive engine and power systems manufacturer with a diversified global footprint. Otis, in contrast, leads as a high-margin elevator and escalator service provider focused on installation and maintenance. This analysis explores their divergent models to identify which offers superior risk-adjusted returns for a diversified portfolio.

Table of contents

Companies Overview

Cummins Inc. and Otis Worldwide Corporation both anchor critical roles in the industrial machinery market. Their scale and innovation set benchmarks in their respective niches.

Cummins Inc.: Powertrain and Engine Innovator

Cummins Inc. dominates diesel and natural gas engines globally, catering to heavy and medium-duty vehicles plus diverse industrial applications. Its core revenue stems from manufacturing engines, power systems, and components, alongside aftermarket parts and services. In 2026, Cummins focuses strategically on expanding electrified powertrain solutions and emission technologies, reinforcing its competitive advantage in sustainable power.

Otis Worldwide Corporation: Elevators and Escalators Leader

Otis Worldwide specializes in designing, installing, and servicing elevators and escalators worldwide, with a vast network of 34,000 service mechanics. Revenue flows primarily from new equipment sales and ongoing service contracts. In 2026, Otis sharpens its focus on modernization services and expanding its global maintenance footprint, ensuring steady cash flow from its service-oriented business model.

Strategic Collision: Similarities & Divergences

Both companies operate in industrial machinery but pursue distinct business philosophies. Cummins invests heavily in product innovation and electrification, while Otis focuses on service reliability and modernization. Their primary battleground lies in the industrial infrastructure space—power systems versus vertical transportation. This divergence creates unique investment profiles: Cummins offers growth through technology leadership; Otis provides stability via recurring service revenue.

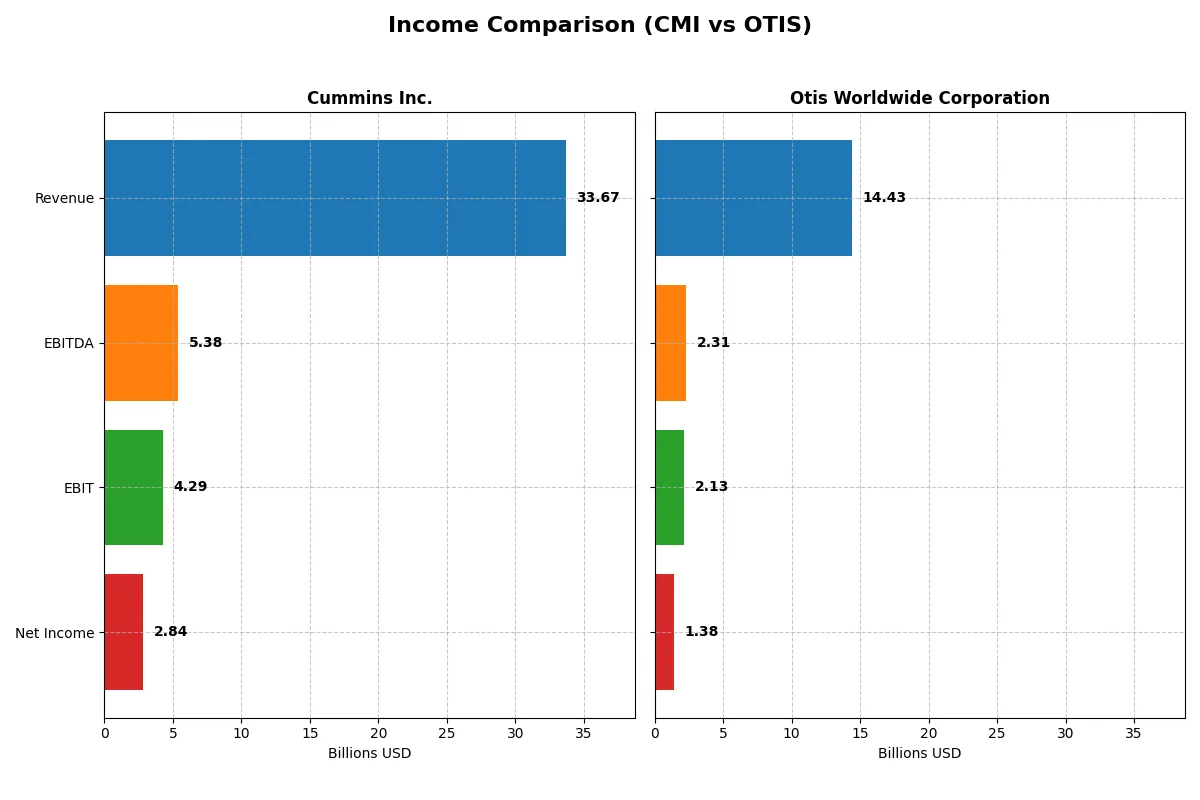

Income Statement Comparison

The following data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | Cummins Inc. (CMI) | Otis Worldwide Corporation (OTIS) |

|---|---|---|

| Revenue | 33.7B | 14.4B |

| Cost of Revenue | 25.2B | 10.1B |

| Operating Expenses | 4.5B | 2.2B |

| Gross Profit | 8.5B | 4.4B |

| EBITDA | 5.4B | 2.3B |

| EBIT | 4.3B | 2.1B |

| Interest Expense | 329M | 196M |

| Net Income | 2.8B | 1.4B |

| EPS | 20.62 | 3.53 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison exposes which company runs a more efficient and profitable corporate engine through their financial results.

Cummins Inc. Analysis

Cummins shows a strong revenue rise from 24B in 2021 to 34B in 2024, with a slight dip to 33.7B in 2025. Net income surged from 2.13B in 2021 to 3.95B in 2024 but declined to 2.84B in 2025. Gross and net margins remain solid at 25.3% and 8.4%, respectively. However, the 2025 drop in net margin and EPS signals a recent hit to profitability momentum.

Otis Worldwide Corporation Analysis

Otis’s revenue hovered near 14B from 2021 through 2025, inching up modestly to 14.43B in 2025. Net income climbed steadily from 1.25B in 2021 to 1.64B in 2024 but fell to 1.38B in 2025. Otis maintains healthier margins than Cummins, with a 30.3% gross margin and 9.6% net margin in 2025. Despite slower top-line growth, Otis’s margin expansion underpins its efficient cost management.

Margin Strength vs. Revenue Growth

Cummins delivers stronger revenue growth but struggles with recent margin compression and net income volatility. Otis shows consistent margin expansion, reflecting operational efficiency despite flat revenue. For investors prioritizing margin stability and steady profitability, Otis’s profile offers more resilience. Cummins appeals more to those seeking growth potential but at higher risk to earnings consistency.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies analyzed:

| Ratios | Cummins Inc. (CMI) | Otis Worldwide Corporation (OTIS) |

|---|---|---|

| ROE | 23.0% | -25.7% |

| ROIC | 12.0% | 40.7% |

| P/E | 24.8 | 24.8 |

| P/B | 5.7 | -6.4 |

| Current Ratio | 1.76 | 0.85 |

| Quick Ratio | 1.16 | 0.77 |

| D/E (Debt-to-Equity) | 0.59 | -1.62 |

| Debt-to-Assets | 21.3% | 82.1% |

| Interest Coverage | 12.1 | 11.2 |

| Asset Turnover | 0.99 | 1.35 |

| Fixed Asset Turnover | 4.84 | 11.13 |

| Payout Ratio | 37.1% | 46.7% |

| Dividend Yield | 1.50% | 1.88% |

| Fiscal Year | 2025 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as a company’s DNA, exposing hidden risks and operational strengths essential for investment decisions.

Cummins Inc.

Cummins posts a robust 23% ROE and a solid 8.44% net margin, reflecting efficient profitability. Its P/E of 24.76 signals a fairly valued stock, though a high P/B of 5.7 raises caution. Cummins balances shareholder returns with a 1.5% dividend, supported by strong capital allocation in R&D (4.1%).

Otis Worldwide Corporation

Otis delivers a mixed picture with an unfavorable -25.7% ROE but an impressive 40.7% ROIC, indicating efficient capital use despite profitability struggles. Its valuation aligns with Cummins at a P/E near 24.9, yet a low current ratio (0.85) flags liquidity risk. Otis returns 1.88% dividend yield, maintaining modest shareholder payouts.

Balanced Efficiency vs. Liquidity Caution

Both companies show slightly favorable global ratios, but Cummins combines solid profitability and liquidity with moderate valuation better. Otis’s high ROIC and dividend may attract growth seekers willing to tolerate liquidity risks. Investors must weigh operational safety versus premium efficiency profiles carefully.

Which one offers the Superior Shareholder Reward?

I compare Cummins Inc. (CMI) and Otis Worldwide Corporation (OTIS) focusing on dividend yields, payout ratios, and buyback intensity for 2025. CMI yields 1.5% with a 37% payout, supported by healthy free cash flow coverage (1.58x), and maintains steady buybacks. OTIS offers a 1.88% yield, a 47% payout ratio, and stronger free cash flow coverage (1.99x). Both deploy buybacks, but OTIS’s capital expenditure is far lighter (0.39/share vs. 8.96/share for CMI), suggesting more cash to return. However, OTIS’s heavy leverage and negative book value raise sustainability risks. I view CMI’s balanced approach as more durable, delivering superior long-term shareholder reward despite a slightly lower yield.

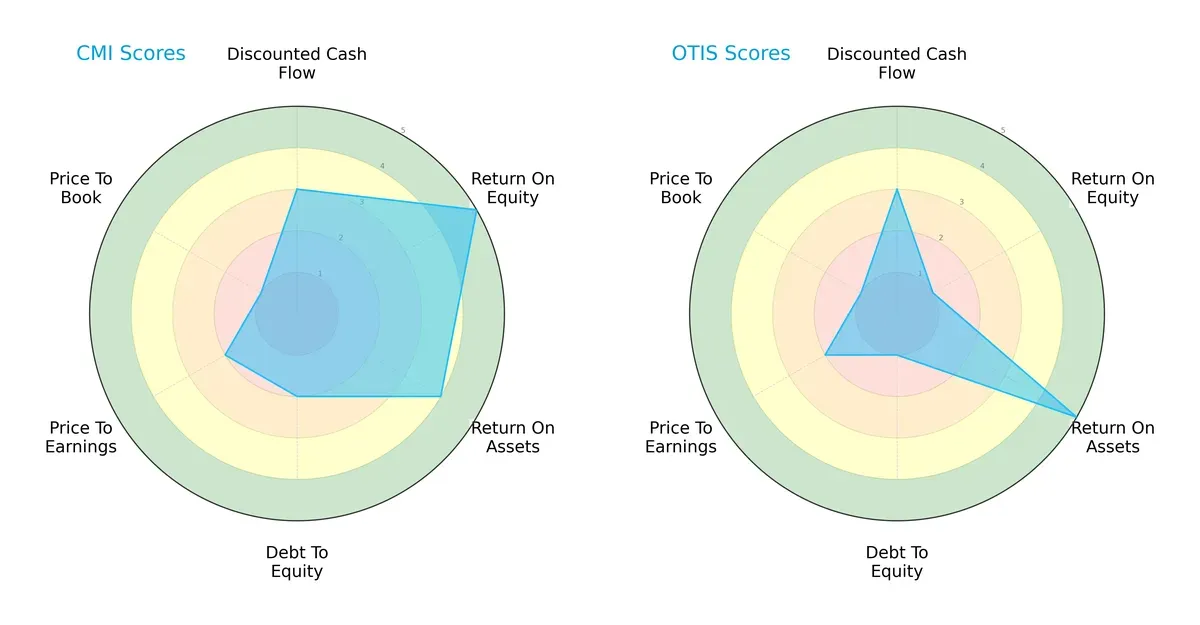

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of Cummins Inc. and Otis Worldwide Corporation, highlighting their distinct operational strengths and valuation challenges:

Cummins shows strong profitability with a very favorable ROE (5) and good ROA (4), but it carries higher financial risk with a weaker debt-to-equity score (2). Otis excels in asset utilization (ROA 5) but suffers from a poor ROE (1) and even weaker debt management (1). Cummins offers a more balanced profile, while Otis leans heavily on operational efficiency despite financial leverage concerns.

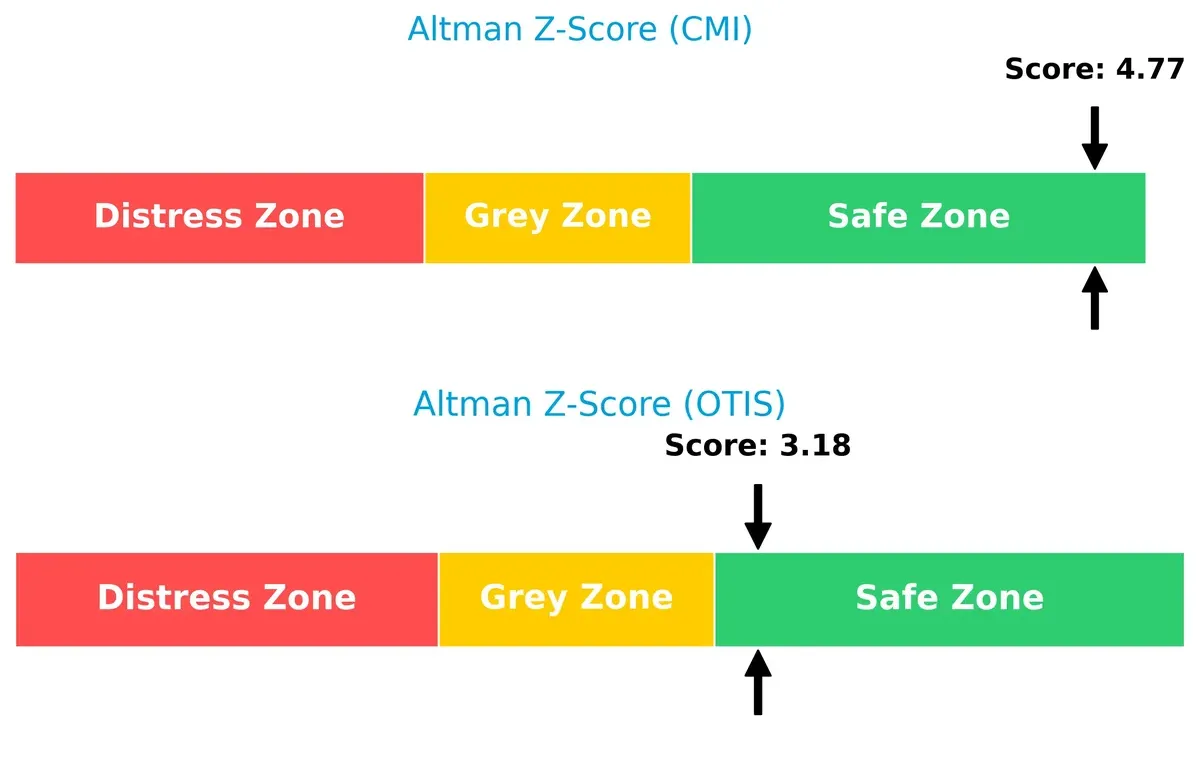

Bankruptcy Risk: Solvency Showdown

Cummins’ Altman Z-Score of 4.77 versus Otis’ 3.18 places both firms safely above distress thresholds, but Cummins holds a significantly stronger buffer for long-term survival in volatile markets:

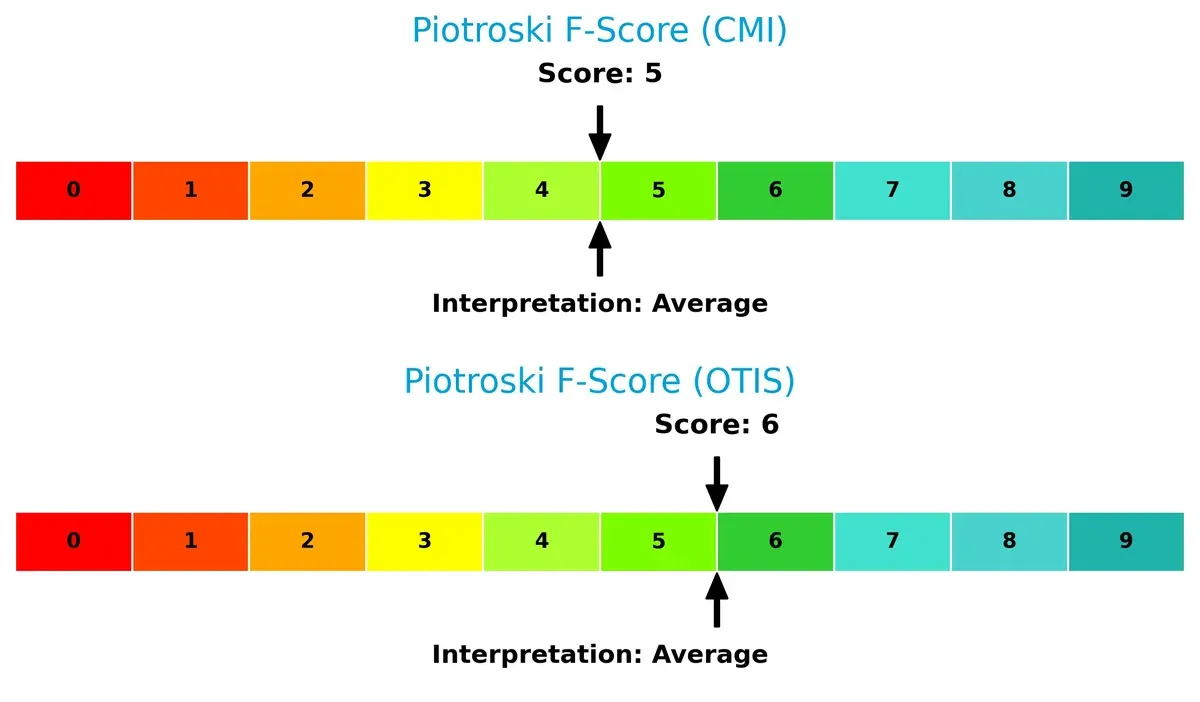

Financial Health: Quality of Operations

Otis edges out Cummins slightly with a Piotroski F-Score of 6 versus 5, indicating marginally better internal financial health. Neither firm raises red flags, but Cummins’ average score suggests room to improve operational efficiencies and balance sheet quality:

How are the two companies positioned?

This section dissects the operational DNA of Cummins and Otis by comparing their revenue distribution and internal dynamics. The goal is to confront their economic moats to reveal which model delivers the most resilient competitive advantage today.

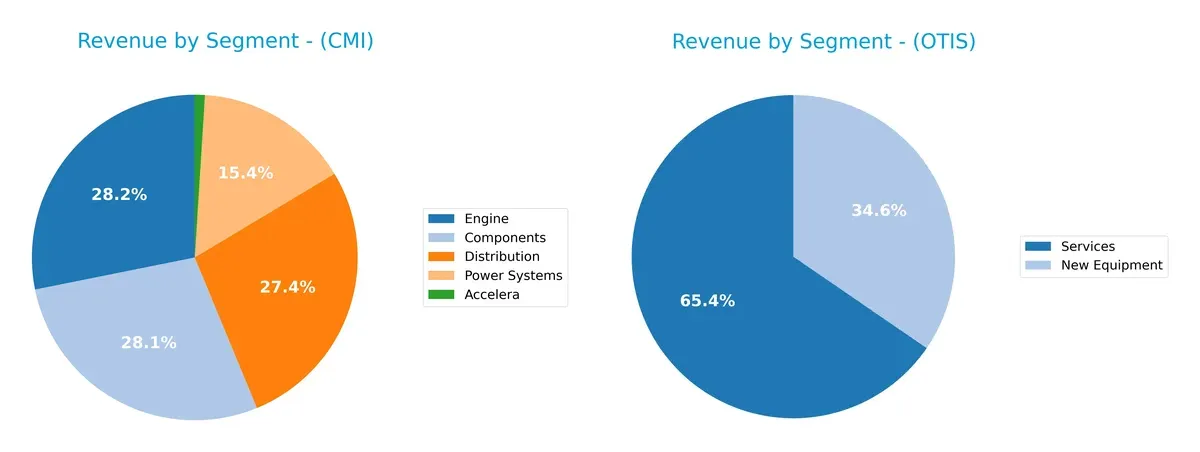

Revenue Segmentation: The Strategic Mix

The following comparison dissects how Cummins Inc. and Otis Worldwide diversify their income streams and reveals where their primary sector bets lie:

Cummins Inc. generates revenue across five key segments, with Engine ($11.7B) and Components ($11.7B) anchoring its mix, showing moderate diversification. Otis leans heavily on two segments: Services ($8.9B) and New Equipment ($5.4B), with Services dwarfing New Equipment. Cummins’ broader segment spread reduces concentration risk, while Otis’s focus on services suggests strong ecosystem lock-in but exposes it to cyclical new equipment demand swings.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of Cummins Inc. and Otis Worldwide Corporation:

Cummins Inc. Strengths

- Diversified revenue across Components, Engine, Distribution, Power Systems

- Favorable ROE and ROIC indicating efficient capital use

- Strong liquidity ratios with current ratio 1.76 and quick ratio 1.16

- Balanced geographical presence with significant US and Non-US sales

- Favorable fixed asset turnover at 4.84

Otis Worldwide Strengths

- High ROIC at 40.74%, showing excellent capital returns

- Favorable WACC and PB ratios reducing cost of capital concerns

- Strong asset turnover and fixed asset turnover, above 1.3 and 11 respectively

- Diversified revenue from New Equipment and Services

- Large revenue base in China and Other regions alongside US

Cummins Inc. Weaknesses

- Negative total segment revenue figures suggest intersegment eliminations or corporate costs

- Unfavorable PB ratio at 5.7 indicating possible overvaluation

- Neutral net margin and PE ratio, limiting profitability signals

- Moderate debt-to-equity ratio at 0.59 with neutral risk profile

- Market share concentration in US might limit global expansion

Otis Worldwide Weaknesses

- Negative ROE of -25.67% signals poor shareholder returns

- Unfavorable liquidity with current ratio 0.85 and quick ratio 0.77, raising short-term risk

- High debt-to-assets at 82.14% indicates significant leverage

- Negative debt-to-equity ratio suggests complex capital structure

- Higher proportion of revenue dependent on few geographic segments

Both companies show strengths in capital efficiency and product diversification but differ markedly in liquidity and leverage profiles. Cummins’ stronger liquidity contrasts with Otis’ higher leverage and weaker short-term financial health, which could impact their strategic flexibility.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat alone protects long-term profits from relentless competitive erosion. Let’s dissect the distinct moats of Cummins and Otis:

Cummins Inc.: Cost Advantage and Innovation in Power Systems

Cummins leverages its cost advantage and deep engineering expertise to maintain stable margins and an ROIC above WACC, though its ROIC trend shows slight decline. Expansion into electrified powertrains could deepen this moat, but competitive pressures in emissions technology pose risks in 2026.

Otis Worldwide Corporation: Service Network and Brand Loyalty

Otis’s moat stems from an extensive global service network and strong brand loyalty, delivering superior ROIC growth versus Cummins. This network effect solidifies recurring revenue streams and operational scale, with modernization services and emerging markets offering promising growth catalysts.

Cost Efficiency vs. Network Strength: The Moat Battle

Otis commands a wider and deeper moat, with ROIC surging 61% versus Cummins’s slight decline, reflecting superior capital efficiency and growing competitive advantage. Otis’s entrenched service ecosystem better defends its market share against disruption in 2026.

Which stock offers better returns?

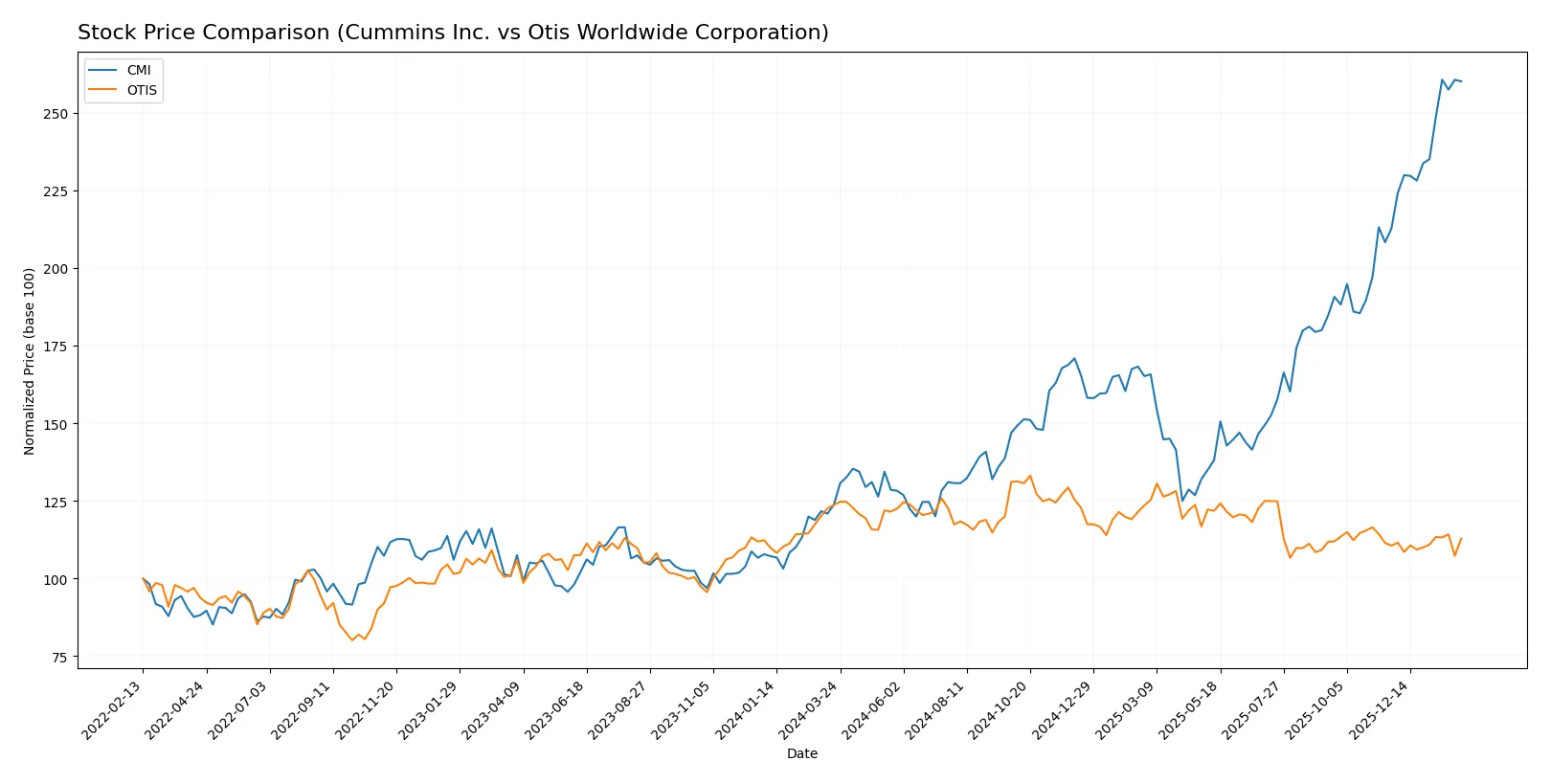

The stock prices of Cummins Inc. and Otis Worldwide show contrasting dynamics over the past year, with Cummins exhibiting strong growth while Otis experienced a decline followed by recent stability.

Trend Comparison

Cummins Inc. posted a 110.21% price increase over the past 12 months, signaling a bullish trend with accelerating momentum and a high volatility level (std dev 79.49). The stock hit a peak of 578.94 and a low of 266.48.

Otis Worldwide’s stock declined by 8.78% over the same period, marking a bearish trend with accelerating downward momentum. Volatility remained low (std dev 4.88), with prices ranging between 84.93 and 106.01.

Comparing these trends, Cummins clearly delivered the highest market performance, outperforming Otis with a robust bullish rally versus Otis’s bearish retreat.

Target Prices

Analysts present a cautiously optimistic consensus for Cummins Inc. and Otis Worldwide Corporation.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Cummins Inc. | 540 | 703 | 606.1 |

| Otis Worldwide Corporation | 92 | 109 | 97.75 |

Cummins trades slightly below its $606 consensus, suggesting upside potential amid solid industrial demand. Otis’s $97.75 target exceeds its current price, reflecting expected growth and steady service revenues.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Cummins Inc. Grades

The following table summarizes the recent institutional grades for Cummins Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Truist Securities | Maintain | Buy | 2026-02-06 |

| Wolfe Research | Downgrade | Peer Perform | 2026-01-26 |

| Barclays | Maintain | Overweight | 2026-01-23 |

| Wells Fargo | Maintain | Overweight | 2026-01-23 |

| JP Morgan | Maintain | Neutral | 2026-01-14 |

| Citigroup | Maintain | Buy | 2026-01-13 |

| Raymond James | Upgrade | Outperform | 2025-12-22 |

| Barclays | Upgrade | Overweight | 2025-12-19 |

| Truist Securities | Maintain | Buy | 2025-12-18 |

| Citigroup | Maintain | Buy | 2025-12-11 |

Otis Worldwide Corporation Grades

The following table summarizes the recent institutional grades for Otis Worldwide Corporation:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| JP Morgan | Maintain | Overweight | 2026-01-16 |

| Wells Fargo | Maintain | Equal Weight | 2025-12-15 |

| Barclays | Maintain | Underweight | 2025-10-30 |

| JP Morgan | Maintain | Overweight | 2025-10-15 |

| Wolfe Research | Upgrade | Outperform | 2025-10-08 |

| Wells Fargo | Maintain | Equal Weight | 2025-10-06 |

| JP Morgan | Maintain | Overweight | 2025-09-18 |

| RBC Capital | Maintain | Outperform | 2025-07-28 |

| Wolfe Research | Upgrade | Peer Perform | 2025-07-25 |

| JP Morgan | Maintain | Overweight | 2025-07-24 |

Which company has the best grades?

Cummins Inc. generally holds stronger grades, including multiple “Buy” and “Outperform” ratings. Otis Worldwide shows more conservative grades, with some “Underweight” and predominantly “Overweight” or “Equal Weight” ratings. Investors may see Cummins as favored by analysts, potentially reflecting higher growth expectations or confidence.

Risks specific to each company

The following categories identify the critical pressure points and systemic threats facing both firms in the 2026 market environment:

1. Market & Competition

Cummins Inc.

- Competes in diverse engine and powertrain markets with strong legacy and innovation in electrification.

Otis Worldwide Corporation

- Focuses on elevators and escalators with large service network but limited product diversification.

2. Capital Structure & Debt

Cummins Inc.

- Maintains moderate debt (D/E 0.59) with favorable interest coverage (13.05).

Otis Worldwide Corporation

- Exhibits high leverage (D/A 82.14%) and negative D/E ratio, indicating complex debt structure risk.

3. Stock Volatility

Cummins Inc.

- Beta of 1.12 indicates moderate market sensitivity and stable trading range.

Otis Worldwide Corporation

- Beta near 1.01 shows market-aligned volatility but price recently declined 1.5%.

4. Regulatory & Legal

Cummins Inc.

- Faces stringent emissions and environmental regulations impacting engine design and manufacturing.

Otis Worldwide Corporation

- Must comply with building safety and accessibility codes internationally, with litigation risk in service contracts.

5. Supply Chain & Operations

Cummins Inc.

- Complex global supply chains for engines and components, exposed to raw material price fluctuations.

Otis Worldwide Corporation

- Relies on extensive service network and parts supply; operational disruptions could affect service continuity.

6. ESG & Climate Transition

Cummins Inc.

- Investing heavily in electrification and emission solutions to meet climate targets.

Otis Worldwide Corporation

- Transition risks moderate; focus on energy-efficient products but slower pace in decarbonization.

7. Geopolitical Exposure

Cummins Inc.

- Global footprint exposes it to trade tensions and tariffs in key markets like China and Europe.

Otis Worldwide Corporation

- International operations face geopolitical risks, but less exposure to volatile commodity markets.

Which company shows a better risk-adjusted profile?

Cummins’ most impactful risk is regulatory pressure on emissions amid its broad global operations. Otis faces significant concerns over its high leverage and weaker liquidity ratios, raising solvency risks. Cummins’ robust interest coverage and safer Altman Z-Score reflect a better risk-adjusted profile. Otis’ elevated debt-to-assets ratio (82%) and unfavorable liquidity signal caution. Recent data show Cummins’ stable current ratio (1.76) contrasts sharply with Otis’ weak 0.85, justifying prudence for Otis investors.

Final Verdict: Which stock to choose?

Cummins Inc. stands out for its unmatched capital efficiency and solid return on equity, creating consistent value despite a slight decline in profitability. Its strong liquidity is a point of vigilance, signaling the need to monitor working capital management. Cummins suits an aggressive growth portfolio seeking durable industrial engines leadership.

Otis Worldwide leverages a formidable strategic moat with its high return on invested capital and expanding profitability, reflecting a sustainable competitive advantage in the elevator sector. Its weaker liquidity compared to Cummins suggests higher caution, but it offers greater stability for portfolios focused on growth at a reasonable price.

If you prioritize robust capital allocation and operational efficiency in industrial manufacturing, Cummins is the compelling choice due to its superior ROE and cash flow quality. However, if you seek a company with a widening moat and improving profitability in infrastructure-related services, Otis offers better stability and a more favorable long-term growth trajectory.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Cummins Inc. and Otis Worldwide Corporation to enhance your investment decisions: