In the rapidly evolving technology sector, CrowdStrike Holdings, Inc. and Veritone, Inc. stand out as innovative players specializing in software infrastructure. CrowdStrike excels in cloud-delivered cybersecurity solutions, while Veritone leads with its artificial intelligence operating system. Both companies target overlapping markets through cutting-edge technology, making their comparison crucial for investors seeking growth with innovation. Join me as we explore which company offers the most compelling investment opportunity today.

Table of contents

Companies Overview

I will begin the comparison between CrowdStrike and Veritone by providing an overview of these two companies and their main differences.

CrowdStrike Overview

CrowdStrike Holdings, Inc. specializes in cloud-delivered protection for endpoints, cloud workloads, identity, and data. Its flagship Falcon platform offers threat intelligence, managed security services, threat hunting, and Zero Trust identity protection. Founded in 2011 and based in Austin, Texas, CrowdStrike serves a global customer base through a direct sales team and channel partners, positioning itself as a leader in cybersecurity infrastructure software.

Veritone Overview

Veritone, Inc. develops AI computing solutions with its aiWARE platform, which employs machine learning and cognitive processes to extract insights from structured and unstructured data. Headquartered in Denver, Colorado, Veritone focuses on media, government, legal, and energy sectors, providing AI-powered analytics and media advertising services. Established in 2014, Veritone operates primarily in the United States and the United Kingdom, offering innovative AI applications across various verticals.

Key similarities and differences

Both companies operate in the technology sector within the software infrastructure industry, leveraging advanced technology to serve business clients. CrowdStrike focuses on cybersecurity and cloud protection services, while Veritone centers on artificial intelligence and data analytics. CrowdStrike’s larger market capitalization and employee base contrast with Veritone’s smaller scale and higher beta, reflecting differing risk profiles and market presence.

Income Statement Comparison

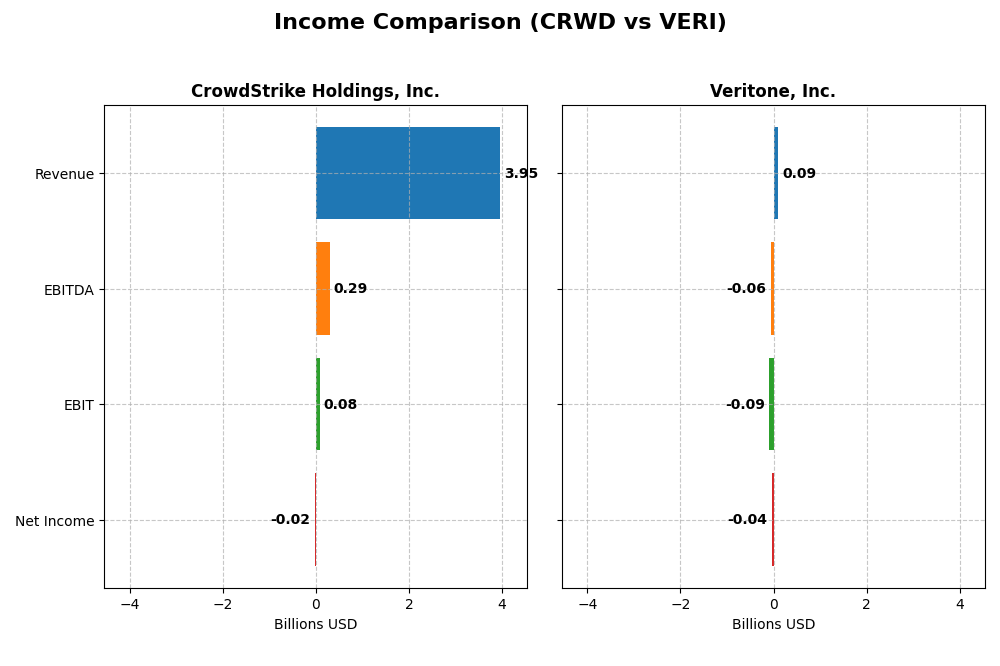

This table presents a side-by-side comparison of key income statement metrics for CrowdStrike Holdings, Inc. and Veritone, Inc. for their most recent fiscal years.

| Metric | CrowdStrike Holdings, Inc. | Veritone, Inc. |

|---|---|---|

| Market Cap | 114.4B | 225M |

| Revenue | 3.95B | 92.6M |

| EBITDA | 295M | -58.8M |

| EBIT | 81M | -88.1M |

| Net Income | -19.3M | -37.4M |

| EPS | -0.08 | -0.98 |

| Fiscal Year | 2025 | 2024 |

Income Statement Interpretations

CrowdStrike Holdings, Inc.

CrowdStrike’s revenue has grown significantly from 874M in 2021 to nearly 4B in 2025, with net income fluctuating from a loss of 93M in 2021 to a profit of 89M in 2024 before a slight loss in 2025. Gross margins remain strong around 75%, but net margins have turned negative recently. The 2025 year shows slowed EBIT and net income growth despite robust revenue gains.

Veritone, Inc.

Veritone’s revenue increased steadily from 58M in 2020 to 100M in 2023 before declining to 93M in 2024. Net income has remained negative throughout, though losses narrowed from -65M in 2023 to -37M in 2024. Gross margin is favorable at 70.6%, but EBIT and net margins remain deeply negative, reflecting ongoing operational challenges. The latest year shows revenue decline but improved net margin and EPS growth.

Which one has the stronger fundamentals?

CrowdStrike demonstrates stronger fundamentals with higher revenues, consistent gross margin strength, and overall favorable long-term income growth despite recent margin pressures. Veritone has favorable margin improvements recently but struggles with profitability and declining revenue. CrowdStrike’s scale and margin stability provide a more robust income statement profile compared to Veritone’s persistent losses and volatility.

Financial Ratios Comparison

This table presents the most recent financial ratios for CrowdStrike Holdings, Inc. and Veritone, Inc., allowing a straightforward comparison of key performance and financial health metrics as of fiscal year 2025 for CrowdStrike and 2024 for Veritone.

| Ratios | CrowdStrike Holdings, Inc. (CRWD) | Veritone, Inc. (VERI) |

|---|---|---|

| ROE | -0.59% | -277.91% |

| ROIC | 0.70% | -58.27% |

| P/E | -5056 | -3.34 |

| P/B | 29.7 | 9.27 |

| Current Ratio | 1.67 | 0.97 |

| Quick Ratio | 1.67 | 0.97 |

| D/E (Debt-to-Equity) | 0.24 | 8.91 |

| Debt-to-Assets | 9.07% | 60.54% |

| Interest Coverage | -4.58 | -7.31 |

| Asset Turnover | 0.45 | 0.47 |

| Fixed Asset Turnover | 4.76 | 8.51 |

| Payout Ratio | 0 | 0 |

| Dividend Yield | 0 | 0 |

Interpretation of the Ratios

CrowdStrike Holdings, Inc.

CrowdStrike shows a balanced ratio profile with 42.86% favorable and 42.86% unfavorable ratios, resulting in a neutral overall evaluation. Strengths include a solid current and quick ratio of 1.67, low debt-to-equity of 0.24, and a favorable fixed asset turnover of 4.76. However, negative net margin (-0.49%), return on equity (-0.59%), and price-to-book of 29.71 raise concerns. CrowdStrike does not pay dividends, reflecting a possible reinvestment strategy or growth focus.

Veritone, Inc.

Veritone’s financial ratios reveal substantial weaknesses, with 78.57% unfavorable and only 14.29% favorable ratios, categorizing the overall profile as very unfavorable. Key issues include a deeply negative net margin (-40.36%), return on equity (-277.91%), and a high debt-to-equity ratio of 8.91. The current ratio stands at a weak 0.97. Veritone also does not pay dividends, likely due to ongoing losses and an emphasis on growth or R&D investments.

Which one has the best ratios?

Between the two, CrowdStrike displays a more balanced financial condition with a neutral overall ratios evaluation, while Veritone suffers from a predominantly unfavorable ratio set. CrowdStrike’s stronger liquidity, lower leverage, and less negative profitability ratios contrast with Veritone’s significant financial weaknesses, making CrowdStrike the company with the relatively stronger ratio profile.

Strategic Positioning

This section compares the strategic positioning of CrowdStrike and Veritone, including market position, key segments, and exposure to technological disruption:

CrowdStrike Holdings, Inc.

- Large market cap of 114B with moderate competitive pressure in cloud security software.

- Focuses on cloud-delivered endpoint protection, subscriptions dominate revenue; professional services secondary.

- Positioned in cloud security with limited direct exposure to AI disruption trends.

Veritone, Inc.

- Small market cap of 225M with high volatility and competitive pressure in AI solutions.

- Diverse AI applications across media, government, and advertising sectors; revenue split among licenses, services, and products.

- Operates AI platform with multiple machine learning features, exposed to rapid AI technology changes.

CrowdStrike vs Veritone Positioning

CrowdStrike’s strategy centers on a concentrated subscription model in cloud security, leveraging scale and direct sales. Veritone pursues diversified AI applications across verticals but operates at a smaller scale with broader segment exposure, impacting operational focus and revenue stability.

Which has the best competitive advantage?

Both companies are currently shedding value relative to their cost of capital. CrowdStrike shows improving profitability with growing ROIC, while Veritone faces declining profitability. Hence, CrowdStrike’s position suggests a slightly stronger economic moat despite current value destruction.

Stock Comparison

The stock price movements of CrowdStrike Holdings, Inc. (CRWD) and Veritone, Inc. (VERI) over the past 12 months reveal distinct bullish trends with significant gains, followed by recent periods of decline and changing trading volumes.

Trend Analysis

CrowdStrike’s stock price increased by 45.71% over the past year, indicating a bullish trend with deceleration and high volatility (std deviation 80.53). The price ranged from 217.89 to 543.01, but recent weeks show a 16.41% decline.

Veritone’s stock price surged 147.22% over the same period, also bullish with deceleration and low volatility (std deviation 1.26). Prices fluctuated between 1.3 and 7.18, yet the recent period shows a sharper 28.91% decrease.

Comparing both, Veritone delivered the highest market performance in the last year despite recent declines, outperforming CrowdStrike’s gains in percentage terms.

Target Prices

Analysts present a clear consensus on target prices for CrowdStrike Holdings, Inc. and Veritone, Inc.

| Company | Target High | Target Low | Consensus |

|---|---|---|---|

| CrowdStrike Holdings, Inc. | 706 | 353 | 553.47 |

| Veritone, Inc. | 10 | 9 | 9.5 |

The consensus target prices suggest significant upside potential for CrowdStrike compared to its current price of 453.88 USD, while Veritone’s target prices imply a moderate increase from its current 4.45 USD. Overall, analysts expect growth but with varying degrees of risk.

Analyst Opinions Comparison

This section compares analysts’ ratings and grades for CrowdStrike Holdings, Inc. (CRWD) and Veritone, Inc. (VERI):

Rating Comparison

CRWD Rating

- Rating: C, categorized as Very Favorable overall rating.

- Discounted Cash Flow Score: 4, assessed as Favorable for valuation.

- ROE Score: 1, rated Very Unfavorable for profit generation efficiency.

- ROA Score: 1, considered Very Unfavorable for asset utilization.

- Debt To Equity Score: 3, Moderate financial risk profile.

- Overall Score: 2, Moderate summary score rating.

VERI Rating

- Rating: C, categorized as Very Favorable overall rating.

- Discounted Cash Flow Score: 5, assessed as Very Favorable valuation.

- ROE Score: 1, rated Very Unfavorable for profit generation efficiency.

- ROA Score: 1, considered Very Unfavorable for asset utilization.

- Debt To Equity Score: 1, Very Unfavorable indicating higher risk.

- Overall Score: 2, Moderate summary score rating.

Which one is the best rated?

Both CRWD and VERI share the same overall rating and score of C and 2, respectively. VERI outperforms CRWD in discounted cash flow score but presents a higher financial risk due to a lower debt-to-equity score.

Scores Comparison

Here is a comparison of the Altman Z-Score and Piotroski Score for CrowdStrike and Veritone:

CRWD Scores

- Altman Z-Score: 12.38, indicating a safe zone, very low bankruptcy risk.

- Piotroski Score: 4, rated as average financial strength.

VERI Scores

- Altman Z-Score: -0.07, in distress zone, high bankruptcy risk.

- Piotroski Score: 3, classified as very weak financial strength.

Which company has the best scores?

Based on the data, CrowdStrike has a significantly stronger Altman Z-Score, indicating better financial stability. Its Piotroski Score is also higher, reflecting better overall financial health than Veritone.

Grades Comparison

This section presents the latest verified grades from reputable grading companies for CrowdStrike Holdings, Inc. and Veritone, Inc.:

CrowdStrike Holdings, Inc. Grades

The table below summarizes the recent grades assigned by major financial institutions to CrowdStrike Holdings, Inc.:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Citigroup | Maintain | Buy | 2026-01-13 |

| BTIG | Maintain | Buy | 2026-01-13 |

| Keybanc | Downgrade | Sector Weight | 2026-01-12 |

| Berenberg | Upgrade | Buy | 2026-01-09 |

| Stephens & Co. | Maintain | Overweight | 2025-12-18 |

| Morgan Stanley | Maintain | Equal Weight | 2025-12-18 |

| Freedom Capital Markets | Upgrade | Buy | 2025-12-11 |

| Citigroup | Maintain | Buy | 2025-12-04 |

| Goldman Sachs | Maintain | Buy | 2025-12-04 |

| Scotiabank | Maintain | Sector Outperform | 2025-12-03 |

Overall, CrowdStrike’s grades mostly range from Buy to Overweight, with a minor recent downgrade from Keybanc, reflecting generally positive analyst sentiment.

Veritone, Inc. Grades

The following table displays recent verified grades given to Veritone, Inc. by financial analysts:

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| D. Boral Capital | Maintain | Buy | 2025-12-09 |

| D. Boral Capital | Maintain | Buy | 2025-12-04 |

| Needham | Maintain | Buy | 2025-12-02 |

| D. Boral Capital | Maintain | Buy | 2025-12-02 |

| D. Boral Capital | Maintain | Buy | 2025-11-07 |

| D. Boral Capital | Maintain | Buy | 2025-10-28 |

| HC Wainwright & Co. | Maintain | Buy | 2025-10-20 |

| D. Boral Capital | Maintain | Buy | 2025-10-15 |

| D. Boral Capital | Maintain | Buy | 2025-09-24 |

| D. Boral Capital | Maintain | Buy | 2025-09-09 |

Veritone’s grades are consistently Buy with no changes, illustrating stable confidence from analysts.

Which company has the best grades?

CrowdStrike Holdings, Inc. has received a broader range of grades with more analyst diversity, including several upgrades and a few downgrades, but mostly positive Buy and Overweight ratings. Veritone, Inc. maintains uniform Buy ratings without variation. For investors, CrowdStrike’s varied grades may indicate nuanced views on growth potential and risk, while Veritone’s stable Buy ratings suggest steady analyst confidence.

Strengths and Weaknesses

Below is a comparative overview of the key strengths and weaknesses of CrowdStrike Holdings, Inc. (CRWD) and Veritone, Inc. (VERI) based on their recent financial and operational data.

| Criterion | CrowdStrike Holdings, Inc. (CRWD) | Veritone, Inc. (VERI) |

|---|---|---|

| Diversification | Primarily focused on cybersecurity subscriptions and professional services; strong subscription growth | More diversified across AI software, licensing, managed services, and advertising, but less focused |

| Profitability | Currently shedding value with negative net margin (-0.49%) and ROE (-0.59%), but improving ROIC trend (0.7%) | Significantly unprofitable with steep negative margins (-40.36%) and ROE (-277.91%), declining ROIC |

| Innovation | High innovation in cybersecurity technology with growing revenue in subscription services (3.76B USD in 2025) | Innovation in AI-driven software and media solutions, but profitability and financial health are weak |

| Global presence | Strong global footprint supported by scalable subscription model | More niche market presence, less global scale and higher financial risk |

| Market Share | Leading position in cybersecurity with rapidly growing revenues | Smaller market share in AI and media sectors with unstable revenue streams |

Key takeaways: CrowdStrike shows promising growth and innovation in a high-demand sector despite current profitability challenges, while Veritone faces significant financial difficulties and weaker profitability despite its diversified product offerings. Caution is advised with Veritone due to its very unfavorable financial ratios and declining returns.

Risk Analysis

The following table summarizes key risk factors for CrowdStrike Holdings, Inc. (CRWD) and Veritone, Inc. (VERI) based on the most recent financial and market data.

| Metric | CrowdStrike Holdings, Inc. (CRWD) | Veritone, Inc. (VERI) |

|---|---|---|

| Market Risk | Moderate beta (1.03), stable growth but competitive sector | High beta (2.05), volatile stock price, smaller market cap |

| Debt level | Low debt-to-equity (0.24), manageable leverage | High debt-to-equity (8.91), significant financial risk |

| Regulatory Risk | Moderate, cybersecurity industry subject to evolving regulations | Moderate, AI and data handling regulations evolving |

| Operational Risk | Established platform, risk from tech disruption | Smaller scale, execution risk in AI platform expansion |

| Environmental Risk | Low direct exposure | Low direct exposure |

| Geopolitical Risk | Moderate, global presence but US-based | Moderate, US and UK operations in sensitive tech sectors |

The most impactful and likely risks are VERI’s high financial leverage and negative profitability metrics, signaling distress and heightened bankruptcy risk. CRWD shows better financial stability but faces competitive and operational risks inherent in cybersecurity. Investors should monitor VERI’s debt management closely and consider CRWD’s valuation and growth sustainability.

Which Stock to Choose?

CrowdStrike Holdings, Inc. (CRWD) has shown strong revenue growth of 29.4% in the past year and 352.1% over five years, with favorable gross margin and a slightly unfavorable but improving ROIC relative to WACC. Its financial ratios are mixed, with solid liquidity and low debt but weak profitability metrics, resulting in a neutral overall ratios evaluation and a very favorable rating.

Veritone, Inc. (VERI) exhibits a declining revenue trend in the latest year with negative profitability and a very unfavorable ROIC trend indicating value destruction. Its financial ratios are mostly unfavorable, including high leverage and poor liquidity, leading to a very unfavorable global ratios opinion despite a very favorable rating driven by discounted cash flow.

Investors focused on growth and improving profitability might find CRWD’s favorable income trends and stable financial health more aligned with their profile, while those accepting higher risk and volatility could interpret VERI’s strong price appreciation and discounted cash flow score as opportunities, albeit with significant caution given its financial challenges.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of CrowdStrike Holdings, Inc. and Veritone, Inc. to enhance your investment decisions: