Home > Comparison > Technology > PLTR vs CRWD

The strategic rivalry between Palantir Technologies Inc. and CrowdStrike Holdings, Inc. shapes the evolution of the technology sector’s software infrastructure landscape. Palantir operates as a data integration and analytics platform for intelligence and enterprise clients, while CrowdStrike leads with cloud-native cybersecurity solutions. This head-to-head highlights a contest between deep data orchestration and comprehensive endpoint security. This analysis aims to reveal which model offers superior risk-adjusted returns for a diversified investor portfolio.

Table of contents

Companies Overview

Palantir Technologies Inc. and CrowdStrike Holdings, Inc. stand as titans in the software infrastructure market, shaping digital defense and data intelligence.

Palantir Technologies Inc.: Master of Data Integration and Intelligence

Palantir dominates the software infrastructure space with platforms like Gotham and Foundry. It generates revenue by enabling government and commercial clients to analyze complex datasets for actionable intelligence. In 2026, Palantir focuses strategically on expanding its AI capabilities and cross-sector deployments to deepen customer reliance on its unified data operating system.

CrowdStrike Holdings, Inc.: Leader in Cloud-Delivered Cybersecurity

CrowdStrike drives growth through its Falcon platform, delivering cloud-based endpoint protection and identity security worldwide. The company’s subscription model fuels recurring revenue from enterprises prioritizing real-time threat intelligence and Zero Trust frameworks. Its 2026 strategy emphasizes scaling cloud modules and enhancing managed security services via direct sales and channel partnerships.

Strategic Collision: Similarities & Divergences

Both companies champion software infrastructure but diverge in approach: Palantir builds a comprehensive data ecosystem while CrowdStrike prioritizes agile, cloud-native cybersecurity. Their primary battleground lies in securing enterprise trust amid rising digital threats. Palantir appeals to clients seeking deep data integration, whereas CrowdStrike’s subscription model favors rapid scalability and broad endpoint coverage. Their investment profiles reflect these distinct market dynamics.

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

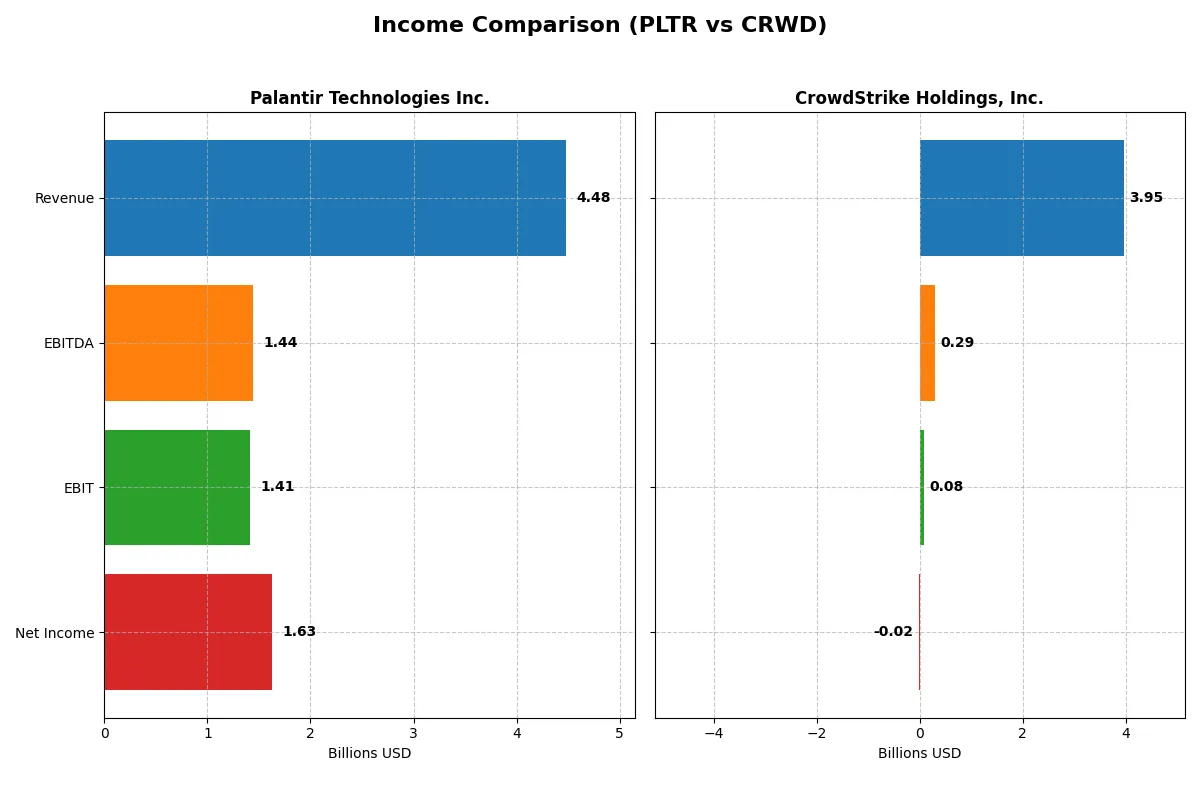

| Metric | Palantir Technologies Inc. (PLTR) | CrowdStrike Holdings, Inc. (CRWD) |

|---|---|---|

| Revenue | 4.48B | 3.95B |

| Cost of Revenue | 789M | 991M |

| Operating Expenses | 2.27B | 3.08B |

| Gross Profit | 3.69B | 2.96B |

| EBITDA | 1.44B | 295M |

| EBIT | 1.41B | 81M |

| Interest Expense | 0 | 26M |

| Net Income | 1.63B | -19M |

| EPS | 0.69 | -0.08 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company runs its business more efficiently and delivers stronger profitability.

Palantir Technologies Inc. Analysis

Palantir shows a powerful revenue surge from 1.54B in 2021 to 4.48B in 2025, with net income exploding from a -520M loss to 1.63B profit. Its gross margin holds a robust 82.4%, and net margin peaks at 36.3%, reflecting exceptional cost control and scalable operations. The 2025 year marks a clear momentum shift, with EBIT growing over 350%.

CrowdStrike Holdings, Inc. Analysis

CrowdStrike’s revenue climbs steadily from 874M in 2021 to 3.95B in 2025, but net income remains negative at -19M in 2025 despite positive growth overall. Gross margin sits at a healthy 74.9%, yet its net margin is slightly negative (-0.5%), indicating tighter profitability and challenging operational leverage. Operating income dipped in 2025, signaling pressure on efficiency.

Margin Dominance vs. Scale Growth

Palantir outperforms CrowdStrike in profitability, with superior margins and a dramatic net income turnaround. CrowdStrike excels in top-line scale but struggles to convert revenue into consistent profit. For investors prioritizing earnings quality and margin strength, Palantir’s profile appears more compelling than CrowdStrike’s growth-at-all-costs model.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | Palantir Technologies Inc. (PLTR) | CrowdStrike Holdings, Inc. (CRWD) |

|---|---|---|

| ROE | 22.0% | -0.6% |

| ROIC | 17.9% | 0.7% |

| P/E | 259.2 | -5055.7 |

| P/B | 57.0 | 29.7 |

| Current Ratio | 7.11 | 1.67 |

| Quick Ratio | 7.11 | 1.67 |

| D/E | 0.031 | 0.241 |

| Debt-to-Assets | 2.6% | 9.1% |

| Interest Coverage | 0 | -4.58 |

| Asset Turnover | 0.50 | 0.45 |

| Fixed Asset Turnover | 17.76 | 4.76 |

| Payout Ratio | 0 | 0 |

| Dividend Yield | 0% | 0% |

| Fiscal Year | 2025 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios serve as a company’s DNA, exposing hidden risks and showcasing operational efficiency and market valuation.

Palantir Technologies Inc.

Palantir delivers strong profitability with a 22% ROE and a robust 36.3% net margin, signaling operational excellence. However, its valuation appears stretched, reflected by a steep P/E of 259 and a high price-to-book of 57. Palantir retains all earnings, reinvesting heavily in R&D to fuel growth rather than paying dividends.

CrowdStrike Holdings, Inc.

CrowdStrike struggles with a negative net margin and ROE, indicating weak profitability but trades at a peculiar negative P/E, suggesting market caution or losses. Its price-to-book is elevated at nearly 30, yet it maintains a healthier current ratio of 1.67. The company focuses on growth through reinvestment instead of dividends.

Premium Valuation vs. Operational Safety

Palantir combines superior profitability with an expensive valuation, reflecting confidence in its growth strategy. CrowdStrike presents a mixed picture with profitability challenges but a more moderate liquidity profile. Investors seeking operational strength may favor Palantir, while those tolerant of risk and volatility might consider CrowdStrike’s profile.

Which one offers the Superior Shareholder Reward?

Palantir Technologies (PLTR) and CrowdStrike Holdings (CRWD) both forgo dividends, focusing on growth and reinvestment. I observe Palantir’s strong free cash flow (0.89/share in 2025) and negligible debt, supporting potential buybacks. Buyback data is absent but Palantir’s cash-rich position and zero payout ratio indicate room for capital returns. CrowdStrike shows robust operating cash flow (5.65/share) but weaker free cash flow conversion (~77%), with higher leverage (debt-to-equity 0.24) limiting buyback capacity. Both prioritize growth over payouts, yet Palantir’s superior cash coverage and conservative leverage promise a more sustainable, shareholder-friendly distribution model. I favor Palantir for a more attractive total return profile in 2026.

Comparative Score Analysis: The Strategic Profile

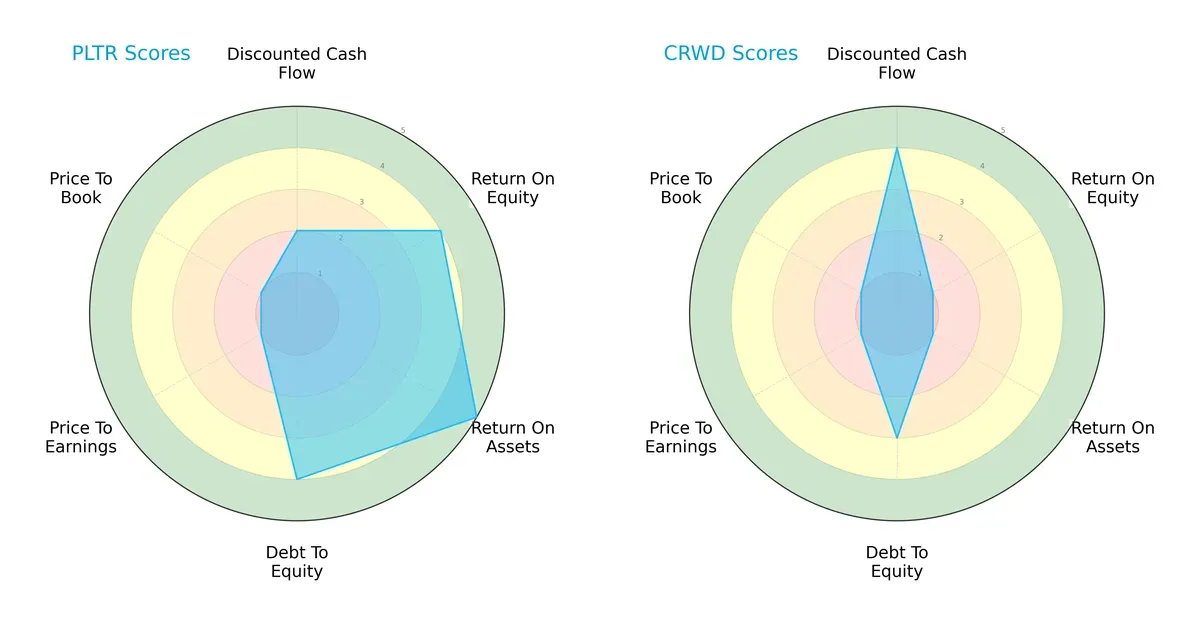

The radar chart reveals the fundamental DNA and trade-offs of Palantir Technologies and CrowdStrike Holdings, highlighting their distinct financial strengths and weaknesses:

Palantir shows a more balanced profile with strong ROE (4) and ROA (5) scores and a favorable debt-to-equity score (4). CrowdStrike relies heavily on discounted cash flow (4) but suffers from weak profitability metrics (ROE 1, ROA 1) and moderate leverage (3). Both face valuation challenges with very unfavorable P/E and P/B scores (1 each). Palantir’s diverse financial strengths contrast with CrowdStrike’s niche edge in cash flow valuation.

Bankruptcy Risk: Solvency Showdown

Palantir’s Altman Z-Score (135.1) vastly exceeds CrowdStrike’s (11.4), placing both safely above distress zones but highlighting Palantir’s exceptional solvency and lower bankruptcy risk in this cycle:

Financial Health: Quality of Operations

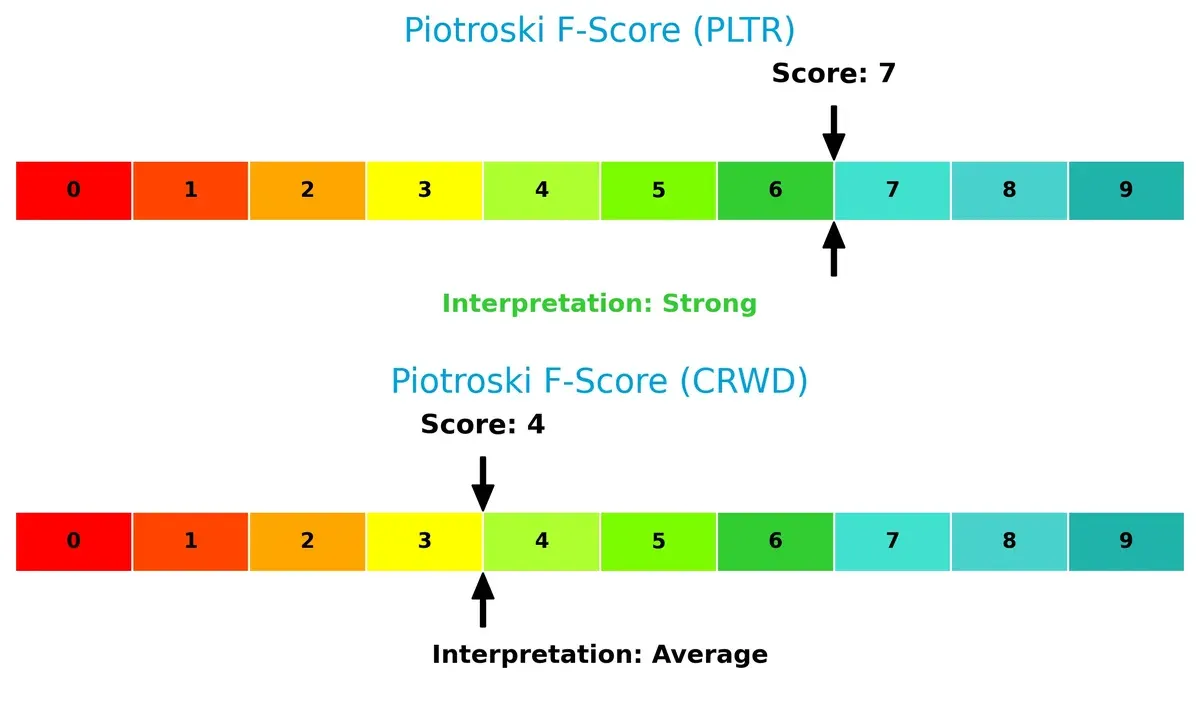

Palantir’s Piotroski F-Score of 7 indicates strong financial health, while CrowdStrike’s score of 4 signals average quality and some internal red flags that warrant caution:

How are the two companies positioned?

This section dissects the operational DNA of Palantir and CrowdStrike by comparing their revenue distribution and internal strengths and weaknesses. The goal is to confront their economic moats and identify which model offers the most resilient and sustainable competitive advantage today.

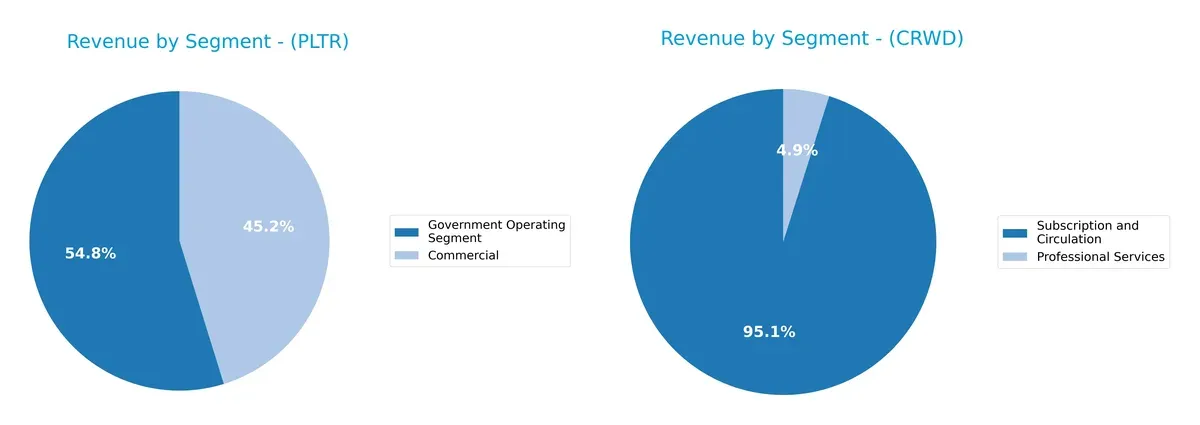

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how Palantir Technologies and CrowdStrike diversify their income streams and reveals their primary sector bets:

Palantir’s revenue splits between Commercial ($1.3B) and Government ($1.57B) segments in 2024, showing a balanced but government-leaning mix. CrowdStrike pivots heavily on Subscription and Circulation ($3.76B) with a smaller Professional Services slice ($192M). Palantir’s dual focus reduces concentration risk, while CrowdStrike’s subscription dominance anchors its ecosystem lock-in and recurring revenue strength.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of Palantir Technologies Inc. and CrowdStrike Holdings, Inc.:

Palantir Strengths

- High net margin at 36.31%

- Strong ROE at 22% and ROIC at 17.95%

- Very low debt ratios and infinite interest coverage

- Diversified revenue from commercial and government sectors

- Growing global presence with significant US and UK sales

- High fixed asset turnover at 17.76

CrowdStrike Strengths

- Favorable P/E despite losses

- Solid current and quick ratios at 1.67

- Moderate debt levels with favorable coverage

- Large subscription revenue driving growth

- Expanding global footprint including Asia Pacific and EMEA

- Good fixed asset turnover at 4.76

Palantir Weaknesses

- Very high P/E (259.19) and P/B (57.02) ratios

- Unfavorable current ratio at 7.11 despite liquidity

- WACC higher than ROIC, indicating costly capital

- No dividend yield

- Moderate asset turnover at 0.5

- Heavy reliance on government contracts

CrowdStrike Weaknesses

- Negative net margin, ROE, and low ROIC

- Negative P/E ratio reflects losses

- Unfavorable asset turnover at 0.45

- No dividend yield

- Interest coverage only neutral at 3.07

- Smaller professional services revenue segment

Overall, Palantir shows strong profitability and conservative leverage but faces valuation and capital cost concerns. CrowdStrike’s growth potential is tempered by unprofitable operations and weaker asset efficiency. Each company balances risk and opportunity differently, shaping distinct strategic priorities.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only true barrier protecting long-term profits from relentless competitive erosion in tech sectors:

Palantir Technologies Inc.: Data Integration & Intelligence Network Moat

Palantir’s moat stems from powerful switching costs and unique data integration across government and enterprise clients. Its 6.2% ROIC above WACC and 214% ROIC growth reflect efficient capital use and margin stability. Expansion of AI-driven platforms in 2026 should deepen this advantage.

CrowdStrike Holdings, Inc.: Endpoint Security Ecosystem Moat

CrowdStrike’s moat relies on a broad security ecosystem with network effects across endpoints and cloud workloads. Unlike Palantir, it currently sheds value with ROIC below WACC but shows improving profitability trends. Growth in Zero Trust and identity protection offers expansion potential in 2026.

Verdict: Data Integration Moat vs. Endpoint Security Ecosystem

Palantir holds a deeper moat, creating consistent value with high ROIC and margin durability. CrowdStrike’s ecosystem is promising but its current value destruction weakens its defense. Palantir is better positioned to maintain market dominance.

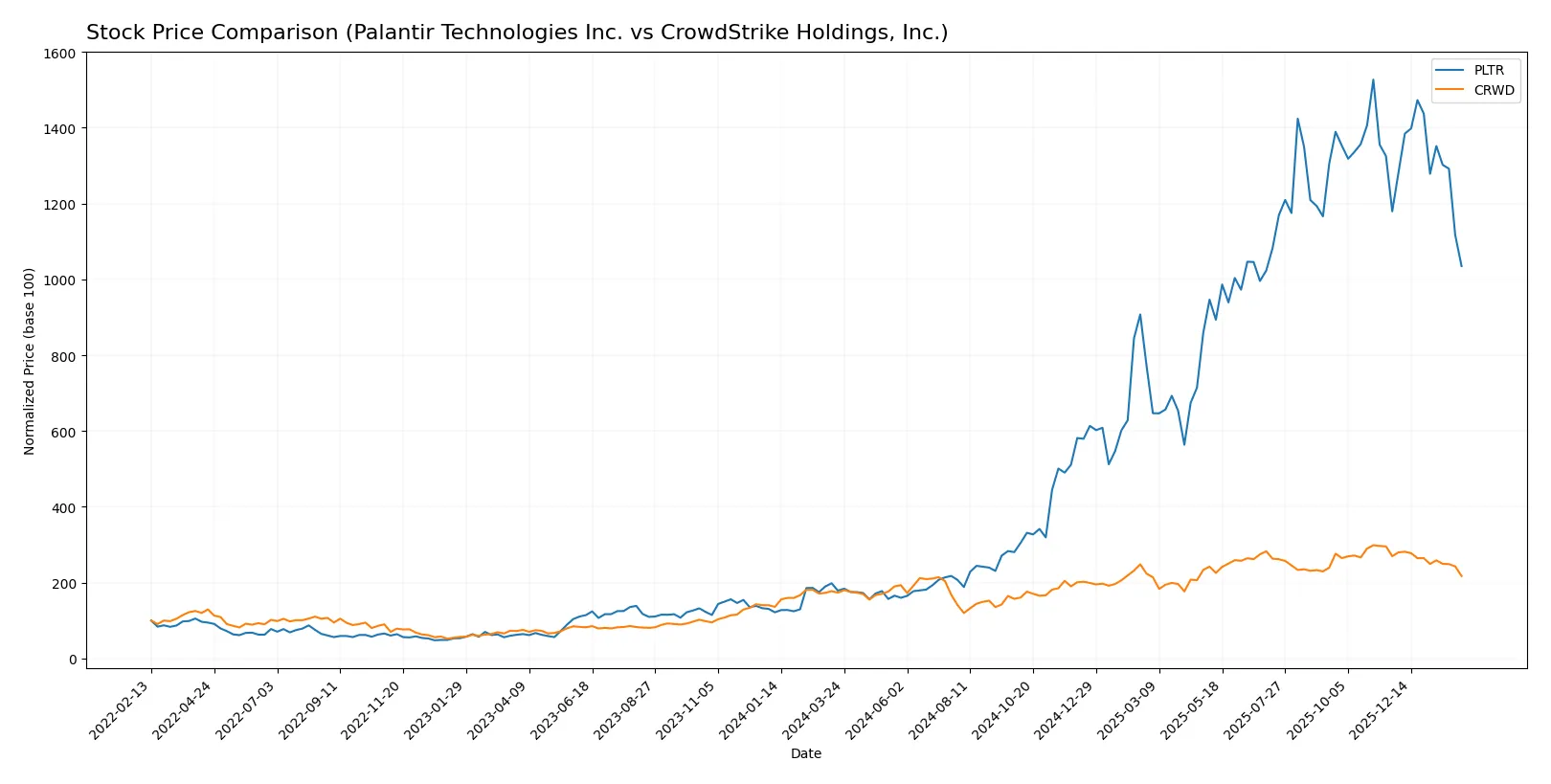

Which stock offers better returns?

Over the past year, Palantir Technologies and CrowdStrike Holdings showed significant price movements with contrasting trading volumes and recent downward shifts.

Trend Comparison

Palantir Technologies’ stock gained 478.54% over the past 12 months, marking a strong bullish trend with decelerating momentum and a high volatility level (std dev 59.53).

CrowdStrike Holdings’ stock rose 25.3% in the same period, also bullish but with decelerating gains and higher volatility (std dev 79.96).

Palantir outperformed CrowdStrike markedly in price appreciation, despite both stocks experiencing recent declines and seller dominance since late 2025.

Target Prices

Analysts present a bullish consensus for Palantir Technologies Inc. and CrowdStrike Holdings, Inc.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| Palantir Technologies Inc. | 180 | 230 | 200.15 |

| CrowdStrike Holdings, Inc. | 353 | 706 | 551.26 |

The target consensus for Palantir exceeds its current price of 136, suggesting upside potential. CrowdStrike’s consensus target of 551 strongly outpaces its current 396 price, indicating robust growth expectations.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

The following tables summarize recent institutional grades for Palantir Technologies Inc. and CrowdStrike Holdings, Inc.:

Palantir Technologies Inc. Grades

This table lists the latest analyst grades assigned to Palantir Technologies Inc. by reputable firms.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| UBS | Maintain | Neutral | 2026-02-03 |

| Citigroup | Maintain | Buy | 2026-02-03 |

| DA Davidson | Maintain | Neutral | 2026-02-03 |

| Citigroup | Upgrade | Buy | 2026-01-12 |

| DA Davidson | Maintain | Neutral | 2025-11-04 |

| RBC Capital | Maintain | Underperform | 2025-11-04 |

| Baird | Maintain | Neutral | 2025-11-04 |

| Goldman Sachs | Maintain | Neutral | 2025-11-04 |

| Mizuho | Maintain | Neutral | 2025-11-04 |

| Morgan Stanley | Maintain | Equal Weight | 2025-11-04 |

CrowdStrike Holdings, Inc. Grades

This table shows recent grades CrowdStrike Holdings, Inc. received from well-known grading companies.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Macquarie | Maintain | Neutral | 2026-01-27 |

| BTIG | Maintain | Buy | 2026-01-13 |

| Citigroup | Maintain | Buy | 2026-01-13 |

| Keybanc | Downgrade | Sector Weight | 2026-01-12 |

| Berenberg | Upgrade | Buy | 2026-01-09 |

| Morgan Stanley | Maintain | Equal Weight | 2025-12-18 |

| Stephens & Co. | Maintain | Overweight | 2025-12-18 |

| Freedom Capital Markets | Upgrade | Buy | 2025-12-11 |

| Citigroup | Maintain | Buy | 2025-12-04 |

| Goldman Sachs | Maintain | Buy | 2025-12-04 |

Which company has the best grades?

CrowdStrike Holdings, Inc. has received more Buy and Overweight ratings than Palantir, which mostly holds Neutral and Equal Weight grades. This suggests stronger institutional conviction in CrowdStrike’s outlook, potentially attracting more investor interest.

Risks specific to each company

The following categories identify critical pressure points and systemic threats facing Palantir Technologies Inc. and CrowdStrike Holdings, Inc. in the 2026 market environment:

1. Market & Competition

Palantir Technologies Inc.

- Faces intense competition in data analytics and AI-driven software markets; high valuation pressures persist.

CrowdStrike Holdings, Inc.

- Competes in a crowded cybersecurity market; struggles with profitability and sustaining growth amid fierce rivals.

2. Capital Structure & Debt

Palantir Technologies Inc.

- Extremely low debt levels (D/E 0.03) support financial stability and flexibility.

CrowdStrike Holdings, Inc.

- Moderate leverage (D/E 0.24) increases financial risk but remains manageable.

3. Stock Volatility

Palantir Technologies Inc.

- High beta (1.69) indicates significant price swings, reflecting market sensitivity.

CrowdStrike Holdings, Inc.

- Lower beta (1.03) suggests more stable trading relative to market benchmarks.

4. Regulatory & Legal

Palantir Technologies Inc.

- Operates with government intelligence contracts, facing sensitive regulatory scrutiny and compliance risks.

CrowdStrike Holdings, Inc.

- Cybersecurity focus exposes it to evolving data privacy laws and regulatory enforcement risks globally.

5. Supply Chain & Operations

Palantir Technologies Inc.

- Relies on software deployment; operational risks are moderate with strong cloud infrastructure.

CrowdStrike Holdings, Inc.

- Dependent on cloud and subscription model; potential operational disruption from tech issues or partner reliance.

6. ESG & Climate Transition

Palantir Technologies Inc.

- Increasing pressure to enhance ESG disclosures and reduce carbon footprint in tech operations.

CrowdStrike Holdings, Inc.

- Faces investor and regulatory demands to strengthen ESG practices, especially in data security and governance.

7. Geopolitical Exposure

Palantir Technologies Inc.

- Exposure to geopolitical risks due to government contracts in multiple countries, including intelligence sectors.

CrowdStrike Holdings, Inc.

- Global customer base exposes it to geopolitical tensions affecting cloud and cybersecurity services delivery.

Which company shows a better risk-adjusted profile?

Palantir’s dominant risk is geopolitical exposure from sensitive government contracts. CrowdStrike’s chief risk lies in weak profitability amid intense competition. Palantir’s robust balance sheet, strong Altman Z-score, and higher Piotroski score underpin a better risk-adjusted profile. CrowdStrike’s financial fragility and operational risks temper its appeal. Recent data confirm Palantir’s stronger financial health despite its market volatility.

Final Verdict: Which stock to choose?

Palantir Technologies Inc. wields a superpower in operational efficiency and value creation, consistently generating returns well above its cost of capital. Its soaring profitability and strong balance sheet support growth, though its sky-high valuation signals a point of vigilance. This stock aligns with aggressive growth portfolios willing to tolerate premium multiples.

CrowdStrike Holdings, Inc. builds its moat on cloud security dominance and predictable recurring revenues. It offers better liquidity and a more moderate valuation profile than Palantir, providing relative safety. CrowdStrike suits investors seeking Growth at a Reasonable Price (GARP) with a focus on steady expansion despite current profitability challenges.

If you prioritize rapid value creation and can stomach elevated valuation risk, Palantir outshines as a growth engine with proven capital efficiency. However, if you seek better stability and a strategic foothold in cybersecurity with a more tempered price, CrowdStrike offers a compelling, albeit less profitable, alternative. Both present distinct scenarios tailored to different risk appetites and investment horizons.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of Palantir Technologies Inc. and CrowdStrike Holdings, Inc. to enhance your investment decisions: