Home > Comparison > Technology > CRWD vs FFIV

The strategic rivalry between CrowdStrike Holdings, Inc. and F5, Inc. defines the trajectory of the software infrastructure sector. CrowdStrike operates as a cloud-delivered cybersecurity leader with subscription-based growth, while F5 combines hardware and software to secure multi-cloud applications. This head-to-head pits innovative cloud-native scalability against established multi-cloud delivery expertise. This analysis will reveal which model offers superior risk-adjusted returns for a diversified portfolio in 2026.

Table of contents

Companies Overview

CrowdStrike and F5 represent two major players in the software infrastructure sector, each shaping digital security and application delivery worldwide.

CrowdStrike Holdings, Inc.: Cloud-Delivered Cybersecurity Leader

CrowdStrike dominates cloud-based endpoint and workload protection. Its core revenue comes from subscriptions to the Falcon platform, delivering threat intelligence and Zero Trust identity protection. In 2026, the company focuses on expanding its cloud modules and managed security services to deepen market penetration and enhance its security ecosystem.

F5, Inc.: Multi-Cloud Application Security and Delivery Specialist

F5 leads with multi-cloud application security and delivery solutions, combining hardware and software innovations. Its revenue engine relies on sales of BIG-IP appliances, software products, and professional services aimed at securing enterprise applications. The strategic emphasis remains on integrating with public cloud providers and expanding its DDoS and application security offerings in 2026.

Strategic Collision: Similarities & Divergences

Both firms target security but diverge in approach: CrowdStrike emphasizes a cloud-native subscription model, while F5 blends hardware-software solutions across hybrid environments. Their battleground centers on enterprise demand for agile, scalable security amid rising cyber threats. CrowdStrike offers a pure-play cloud growth story; F5 leans on hybrid infrastructure strength, defining distinct investment profiles rooted in contrasting market philosophies.

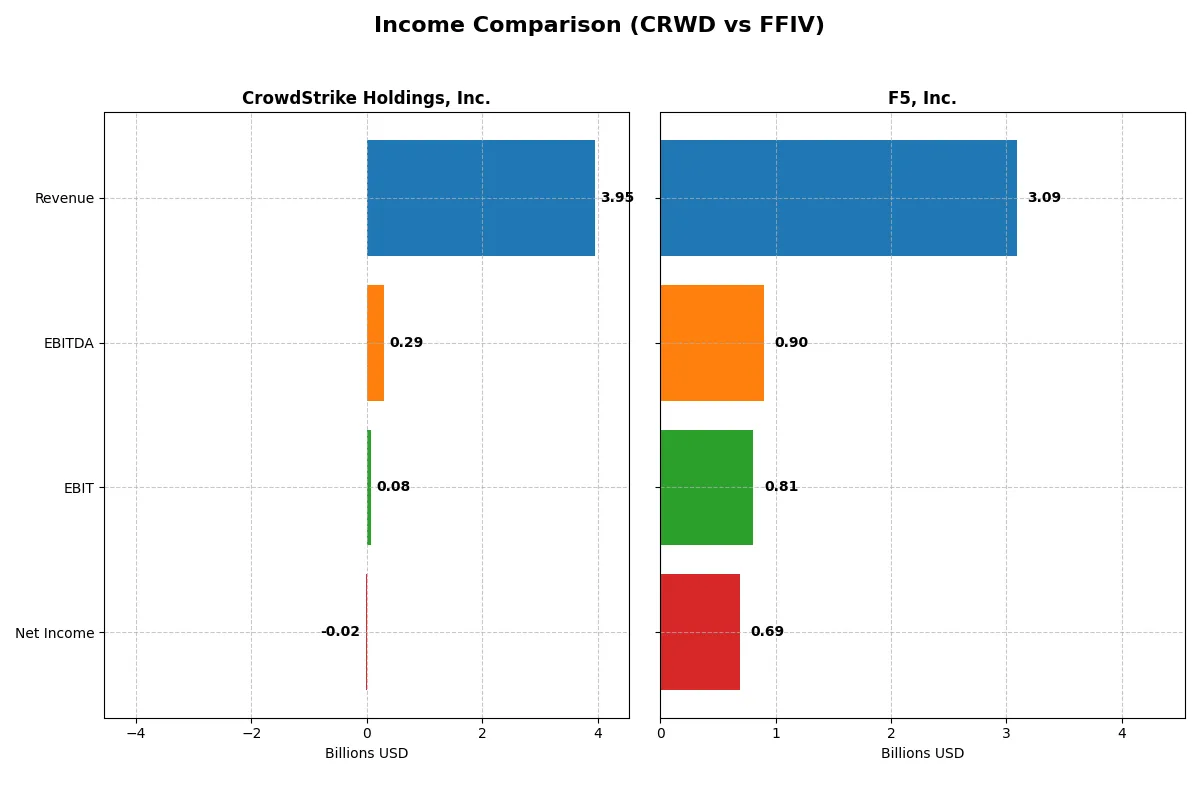

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | CrowdStrike Holdings, Inc. (CRWD) | F5, Inc. (FFIV) |

|---|---|---|

| Revenue | 3.95B | 3.09B |

| Cost of Revenue | 991M | 564M |

| Operating Expenses | 3.08B | 1.76B |

| Gross Profit | 2.96B | 2.52B |

| EBITDA | 295M | 901M |

| EBIT | 81M | 808M |

| Interest Expense | 26M | 0 |

| Net Income | -19M | 692M |

| EPS | -0.08 | 11.95 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals which company operates a more efficient and profitable corporate engine over recent years.

CrowdStrike Holdings, Inc. Analysis

CrowdStrike shows rapid revenue growth, reaching $3.95B in 2025 from $874M in 2021, a 352% surge. However, net income swings from a $234M loss in 2022 to a slight $-19M loss in 2025, reflecting uneven profitability. Its gross margin remains strong near 75%, but net margin turned negative in 2025, signaling rising costs outpacing revenue gains.

F5, Inc. Analysis

F5 posts steady revenue growth, hitting $3.09B in 2025 from $2.6B in 2021, a more modest 19% rise. It maintains robust profitability with a 22.4% net margin in 2025, supported by an 81.7% gross margin and a 26.2% EBIT margin. Consistent net income growth to $692M underscores disciplined cost control and operational efficiency.

Margin Dominance vs. Growth Ambition

F5 clearly outperforms CrowdStrike in profitability and margin stability, boasting superior net and EBIT margins alongside consistent earnings growth. CrowdStrike impresses with explosive revenue growth but struggles to convert scale into profits, posting a negative net margin. Investors prioritizing earnings quality will favor F5’s disciplined profit profile over CrowdStrike’s aggressive top-line expansion.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies compared below:

| Ratios | CrowdStrike Holdings, Inc. (CRWD) | F5, Inc. (FFIV) |

|---|---|---|

| ROE | -0.59% (2025) | 19.28% (2025) |

| ROIC | 0.70% (2025) | 13.99% (2025) |

| P/E | -5056 (2025) | 26.91 (2025) |

| P/B | 29.71 (2025) | 5.19 (2025) |

| Current Ratio | 1.67 (2025) | 1.56 (2025) |

| Quick Ratio | 1.67 (2025) | 1.51 (2025) |

| D/E | 0.24 (2025) | 0.06 (2025) |

| Debt-to-Assets | 9.07% (2025) | 3.65% (2025) |

| Interest Coverage | -4.58 (2025) | N/A (2025) |

| Asset Turnover | 0.45 (2025) | 0.49 (2025) |

| Fixed Asset Turnover | 4.76 (2025) | 9.02 (2025) |

| Payout ratio | 0% (2025) | 0% (2025) |

| Dividend yield | 0% (2025) | 0% (2025) |

| Fiscal Year | 2025 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Financial ratios act as a company’s DNA, unveiling hidden risks and operational strengths behind the numbers.

CrowdStrike Holdings, Inc.

CrowdStrike displays negative profitability with ROE at -0.59% and net margin at -0.49%, signaling operational challenges. Its valuation metrics are stretched, with a favorable negative P/E but an unfavorable PB of 29.7. The company pays no dividends, instead investing heavily in R&D, reflected in a 27.2% R&D-to-revenue ratio.

F5, Inc.

F5 shows strong profitability, boasting a 19.3% ROE and a 22.4% net margin, indicating efficient capital use. Its P/E of 26.9 and PB of 5.2 suggest a moderately expensive valuation. F5 returns value via stable dividends and buybacks, supported by a solid free cash flow yield of 4.9%, balancing growth and shareholder payouts.

Operational Strength vs. Growth Investment

F5 offers a healthier blend of profitability and reasonable valuation, with more favorable ratios overall. CrowdStrike’s negative returns and high valuation highlight riskier growth bets. Investors seeking operational safety may prefer F5, while those focused on aggressive expansion might consider CrowdStrike’s reinvestment model.

Which one offers the Superior Shareholder Reward?

I observe that CrowdStrike (CRWD) pays no dividends and reinvests heavily in growth, with zero payout ratio and no share buybacks. Conversely, F5 (FFIV) also pays no dividends but generates robust free cash flow (~$15.7B per share in 2025) and maintains a disciplined capital allocation with minimal debt (debt-to-equity 0.06). F5’s strong EBIT margin (~26%) and consistent free cash flow conversion (95%) fund its modest buyback program, enhancing shareholder value. CrowdStrike’s negative net margins and sky-high valuation multiples (P/FCF ~91) raise sustainability concerns. I conclude F5 offers a superior total return profile in 2026 due to its balanced capital return and operational strength.

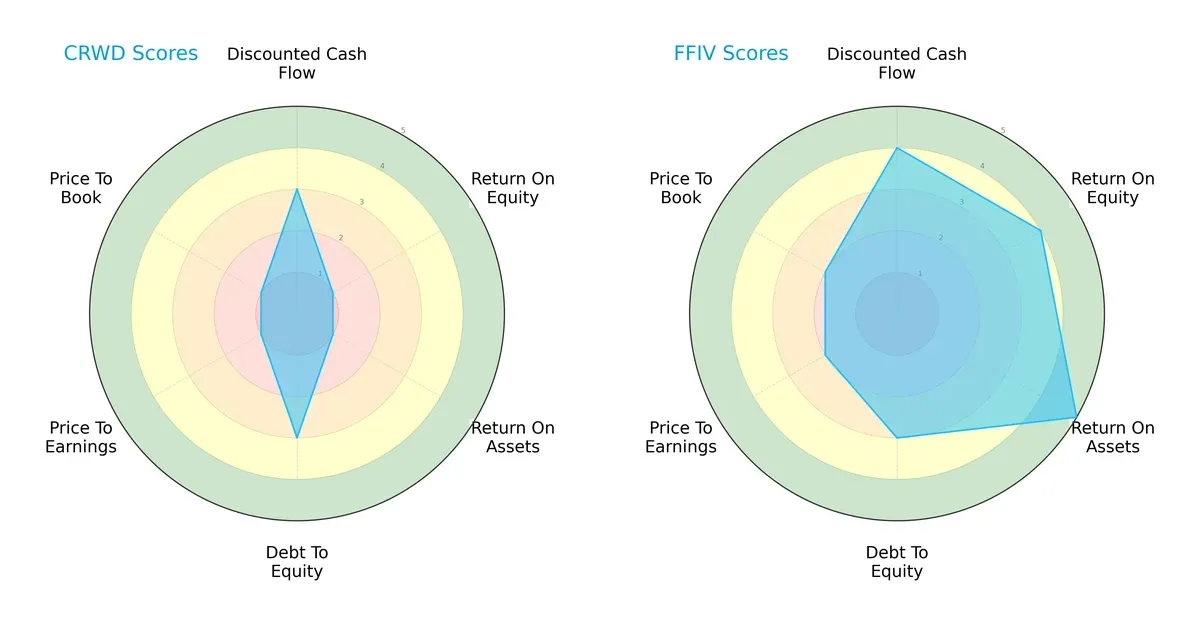

Comparative Score Analysis: The Strategic Profile

The radar chart reveals the fundamental DNA and trade-offs of CrowdStrike Holdings, Inc. and F5, Inc., highlighting their key financial strengths and weaknesses:

F5, Inc. shows a more balanced financial profile with strong returns on equity (4) and assets (5), and solid discounted cash flow (4). CrowdStrike relies heavily on moderate DCF (3) and debt management (3) but suffers from very low ROE (1) and ROA (1), reflecting operational challenges. Valuation metrics favor F5 moderately, underscoring its attractive pricing relative to earnings and book value. Overall, F5 dominates with a robust, well-rounded score set, whereas CrowdStrike’s profile hinges on a few moderate edges but lacks operational efficiency.

Bankruptcy Risk: Solvency Showdown

The Altman Z-Score difference highlights a clear solvency advantage for CrowdStrike, with a score of 12.77 versus F5’s 5.32, both in the safe zone but reflecting different financial resilience levels:

CrowdStrike’s exceptionally high Z-Score signals a very low bankruptcy risk, suggesting strong liquidity and low financial distress probability. F5’s score, while solidly safe, indicates moderate risk compared to CrowdStrike. In this cycle, CrowdStrike offers superior long-term survival odds despite operational weaknesses.

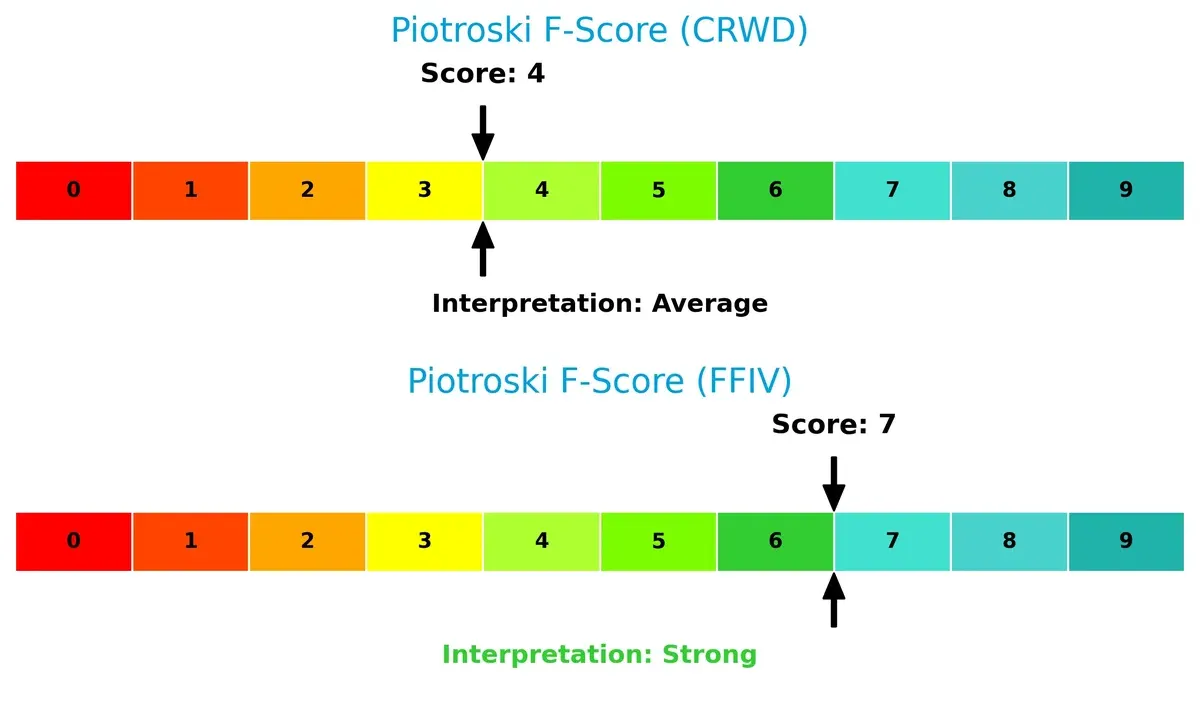

Financial Health: Quality of Operations

Piotroski F-Score analysis reveals F5’s stronger internal financial health with a score of 7, compared to CrowdStrike’s average 4, indicating differing quality in profitability, leverage, and efficiency:

F5 demonstrates a robust operational foundation and fewer red flags, reflecting effective capital allocation and earnings quality. CrowdStrike’s average score suggests caution, highlighting potential internal weaknesses and areas needing improvement before matching F5’s financial strength. Investors should weigh these operational quality differences carefully.

How are the two companies positioned?

This section dissects the operational DNA of CrowdStrike and F5 by comparing their revenue distribution and internal dynamics. The goal is to confront their economic moats and identify the more resilient, sustainable competitive advantage today.

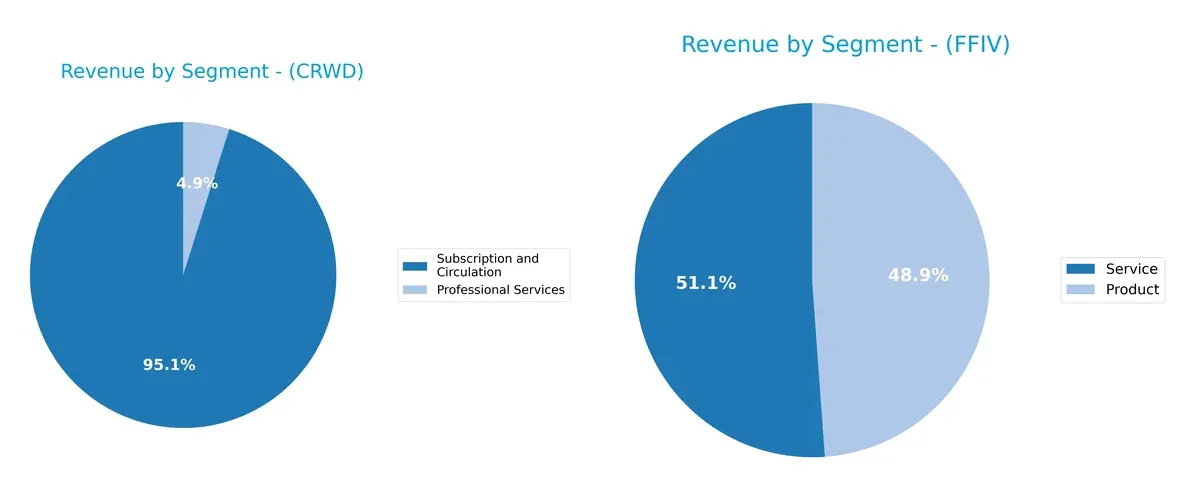

Revenue Segmentation: The Strategic Mix

This comparison dissects how CrowdStrike and F5 diversify their income streams and highlights their primary sector bets:

CrowdStrike anchors 3.76B in subscription revenue, dwarfing its 192M in professional services, showing a strong SaaS focus with low diversification risk. F5 splits evenly between 1.51B product and 1.58B service revenues, reflecting a balanced hardware-software ecosystem. CrowdStrike’s model pivots on recurring digital security, while F5 leverages infrastructure dominance but faces complexity in maintaining dual segments.

Strengths and Weaknesses Comparison

This table compares the strengths and weaknesses of CrowdStrike Holdings, Inc. and F5, Inc.:

CrowdStrike Strengths

- Strong subscription revenue of 3.76B in 2025

- Favorable liquidity ratios with current and quick ratio at 1.67

- Moderate debt levels with debt-to-assets at 9.07%

- Growing global presence with 2.68B US revenue and expanding Asia Pacific and EMEA sales

- Solid fixed asset turnover at 4.76

F5 Strengths

- Balanced revenue from products (1.51B) and services (1.58B) in 2025

- High profitability with net margin 22.42% and ROE 19.28%

- Very low debt levels with debt-to-assets at 3.65%

- Strong interest coverage ratio at infinity

- Wide geographic diversification across Americas, Asia Pacific, and EMEA

- Superior fixed asset turnover of 9.02

CrowdStrike Weaknesses

- Negative profitability metrics with net margin -0.49% and ROE -0.59%

- ROIC (0.7%) below WACC (8.6%), indicating poor capital returns

- High price-to-book ratio at 29.71 signals valuation concerns

- Unfavorable asset turnover at 0.45

- No dividend yield

- High PE ratio negative but flagged favorable due to losses

F5 Weaknesses

- Unfavorable PE (26.91) and PB (5.19) ratios suggesting valuation risk

- Asset turnover weak at 0.49

- No dividend yield

- Net margin and ROIC favorable but some valuation multiples are stretched

The comparison shows CrowdStrike excels in subscription growth and liquidity but struggles with profitability and capital efficiency. F5 delivers strong profitability, better capital returns, and geographic diversification, though some valuation metrics appear elevated. Both companies face challenges with asset turnover and lack dividend payouts, which may influence long-term investor considerations.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only defense preserving long-term profits from relentless competition erosion. Let’s dissect the competitive moats of two tech giants:

CrowdStrike Holdings, Inc.: Innovation-Driven Platform Moat

CrowdStrike thrives on network effects and intangible assets powering its Falcon platform. Its high gross margins reflect pricing power, but negative net margins signal reinvestment for growth. Expansion into identity and Zero Trust protection in 2026 could deepen its moat despite current value destruction.

F5, Inc.: Proven Operational Efficiency Moat

F5 leverages cost advantage and a diversified product portfolio in multi-cloud application security. Its strong ROIC well above WACC and robust net margins showcase efficient capital use. Continued cloud partnerships and software innovation position F5 to expand its durable moat in 2026.

Verdict: Network Effects vs. Operational Mastery

F5 outperforms CrowdStrike with a wider moat, demonstrated by consistent value creation and superior profitability. While CrowdStrike’s innovation offers growth potential, F5’s operational efficiency better defends its market share amid intensifying competition.

Which stock offers better returns?

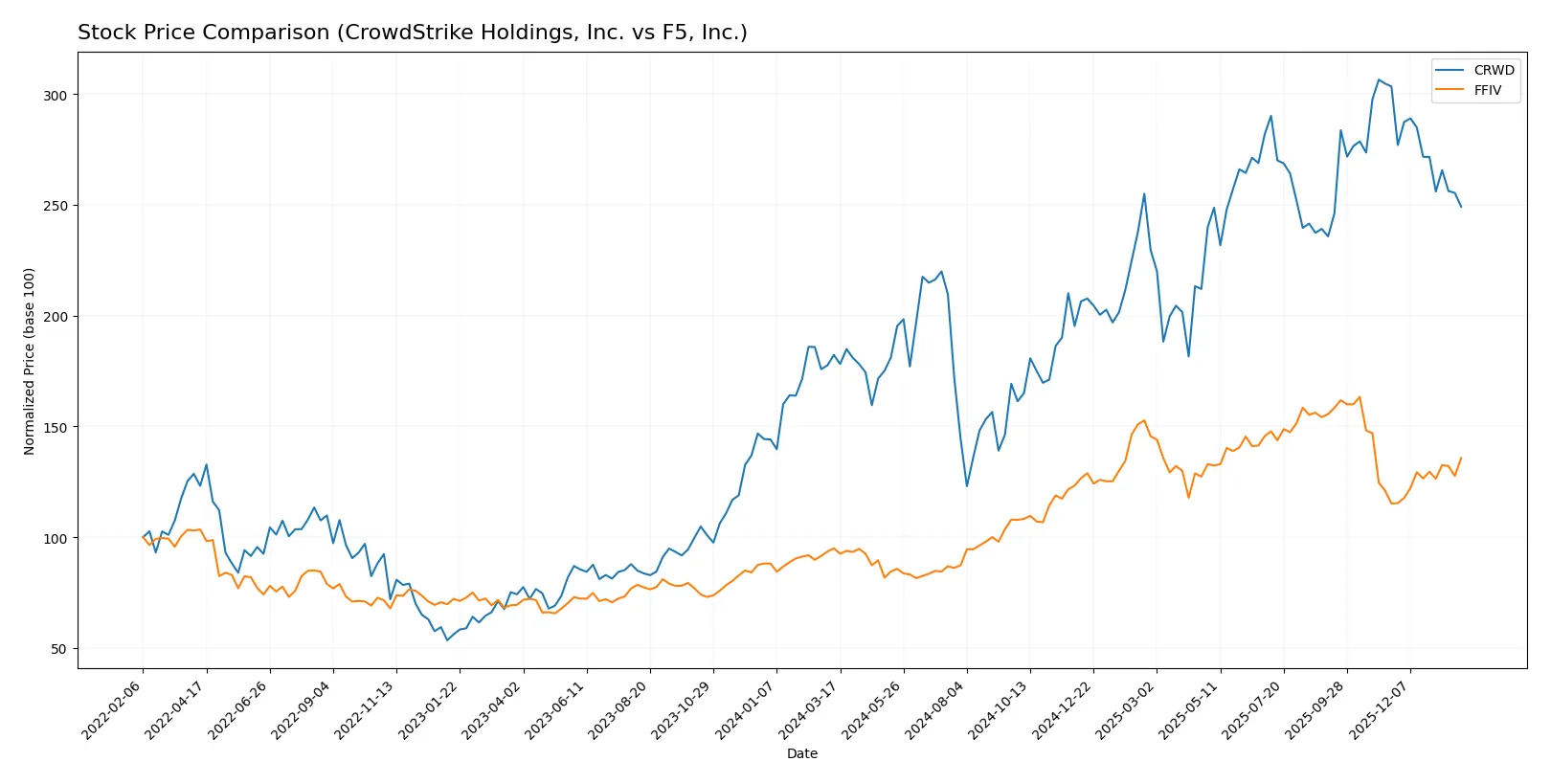

Over the past year, CrowdStrike and F5 exhibited strong price gains with contrasting recent momentum and trading volume dynamics.

Trend Comparison

CrowdStrike’s stock rose 36.72% over 12 months, reflecting a bullish but decelerating trend. It reached a high of 543.01 and showed recent weakness with a -17.88% decline.

F5’s stock gained 42.85% over the same period, maintaining bullish momentum with acceleration. It hit a high of 331.75 and posted a recent 17.78% rally.

F5 outperformed CrowdStrike overall, driven by accelerating gains and stronger buyer dominance in recent trading.

Target Prices

Analysts present a varied but optimistic target price consensus for CrowdStrike Holdings and F5, Inc.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| CrowdStrike Holdings, Inc. | 353 | 706 | 551.26 |

| F5, Inc. | 295 | 352 | 330.67 |

CrowdStrike’s consensus target sits approximately 25% above its current price of 441, signaling strong growth potential. F5’s consensus is roughly 20% above its 276 current price, indicating moderate upside expected by analysts.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

The following tables summarize recent institutional grades for CrowdStrike Holdings, Inc. and F5, Inc.:

CrowdStrike Holdings, Inc. Grades

This table shows the latest grading actions and ratings from key financial institutions.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Macquarie | Maintain | Neutral | 2026-01-27 |

| BTIG | Maintain | Buy | 2026-01-13 |

| Citigroup | Maintain | Buy | 2026-01-13 |

| Keybanc | Downgrade | Sector Weight | 2026-01-12 |

| Berenberg | Upgrade | Buy | 2026-01-09 |

| Stephens & Co. | Maintain | Overweight | 2025-12-18 |

| Morgan Stanley | Maintain | Equal Weight | 2025-12-18 |

| Freedom Capital Markets | Upgrade | Buy | 2025-12-11 |

| Citigroup | Maintain | Buy | 2025-12-04 |

| Goldman Sachs | Maintain | Buy | 2025-12-04 |

F5, Inc. Grades

This table presents recent rating updates from reputable grading companies for F5, Inc.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Needham | Maintain | Hold | 2026-01-28 |

| Piper Sandler | Maintain | Overweight | 2026-01-28 |

| Goldman Sachs | Maintain | Neutral | 2026-01-28 |

| Barclays | Maintain | Equal Weight | 2026-01-28 |

| RBC Capital | Maintain | Outperform | 2026-01-28 |

| JP Morgan | Upgrade | Overweight | 2026-01-15 |

| Piper Sandler | Upgrade | Overweight | 2026-01-05 |

| RBC Capital | Upgrade | Outperform | 2026-01-05 |

| Morgan Stanley | Maintain | Equal Weight | 2025-12-17 |

| Morgan Stanley | Maintain | Equal Weight | 2025-10-28 |

Which company has the best grades?

CrowdStrike holds predominantly Buy and Overweight ratings from multiple firms. F5 generally receives more Hold, Equal Weight, and Overweight grades with fewer Buy equivalents. Investors may view CrowdStrike as having stronger institutional conviction based on these grade patterns.

Risks specific to each company

The following categories identify critical pressure points and systemic threats facing both firms amid the 2026 market environment:

1. Market & Competition

CrowdStrike Holdings, Inc.

- Faces intense competition in cloud security with rapid innovation demands.

F5, Inc.

- Competes in multi-cloud application delivery with strong incumbents and evolving customer needs.

2. Capital Structure & Debt

CrowdStrike Holdings, Inc.

- Maintains moderate leverage with debt-to-assets at 9.07%, manageable but warrants monitoring.

F5, Inc.

- Exhibits lower leverage at 3.65% debt-to-assets, supporting financial flexibility.

3. Stock Volatility

CrowdStrike Holdings, Inc.

- Beta near 1.03 suggests market-level volatility, heightened by growth stock dynamics.

F5, Inc.

- Beta of 0.98 indicates slightly below market volatility, reflecting stable cash flows.

4. Regulatory & Legal

CrowdStrike Holdings, Inc.

- Subject to cybersecurity regulations and evolving data privacy laws globally.

F5, Inc.

- Faces regulatory challenges related to multi-cloud security compliance and export controls.

5. Supply Chain & Operations

CrowdStrike Holdings, Inc.

- Relies heavily on cloud infrastructure partnerships; operational risk from platform outages.

F5, Inc.

- Depends on hardware and software supply chains; potential disruption amid global tech component shortages.

6. ESG & Climate Transition

CrowdStrike Holdings, Inc.

- ESG practices evolving; pressure to reduce data center energy consumption.

F5, Inc.

- Increasing focus on sustainable operations and energy-efficient product design.

7. Geopolitical Exposure

CrowdStrike Holdings, Inc.

- Global customer base exposes it to US-China tensions impacting cybersecurity markets.

F5, Inc.

- International sales subject to geopolitical risks in Europe and Asia Pacific regions.

Which company shows a better risk-adjusted profile?

F5, Inc. demonstrates a superior risk-adjusted profile, driven by robust profitability and stronger financial stability. CrowdStrike’s primary risk lies in its negative profitability and high valuation multiples, while F5’s main concern is hardware supply chain fragility. The contrast in profitability ratios and debt structure highlights F5’s relative resilience in a volatile 2026 technology market.

Final Verdict: Which stock to choose?

CrowdStrike’s superpower lies in its rapid revenue growth and innovation-driven R&D, fueling future market disruption. However, its current profitability challenges and value destruction remain points of vigilance. It fits an aggressive growth portfolio willing to tolerate near-term volatility for long-term potential.

F5 stands out with a durable moat built on consistent free cash flow and strong returns on invested capital. Its higher profitability and financial stability offer a safer harbor compared to CrowdStrike. This stock suits a GARP investor seeking steady growth with reasonable risk.

If you prioritize high-growth exposure and can withstand earnings volatility, CrowdStrike presents a compelling scenario due to its innovation edge. However, if you seek better stability and proven capital efficiency, F5 outshines with its durable competitive advantage and robust profitability, commanding a premium but offering lower risk.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of CrowdStrike Holdings, Inc. and F5, Inc. to enhance your investment decisions: