Home > Comparison > Technology > MDB vs CPAY

The strategic rivalry between MongoDB, Inc. and Corpay, Inc. shapes the infrastructure software landscape. MongoDB operates as a developer-focused, cloud-enabled database platform, while Corpay specializes in payment solutions with a global footprint. This battle highlights a contrast between innovative software services and established payment networks. This analysis aims to reveal which company’s business model offers superior risk-adjusted returns for a diversified portfolio in today’s evolving technology sector.

Table of contents

Companies Overview

MongoDB and Corpay stand as pivotal players in the software infrastructure landscape, each shaping distinct niches.

MongoDB, Inc.: Cloud-Native Database Pioneer

MongoDB dominates the database platform sector with its multi-cloud database-as-a-service offering, MongoDB Atlas. Its revenue stems primarily from commercial licenses and cloud subscriptions, serving enterprise clients globally. In 2026, MongoDB sharpens its strategic focus on expanding cloud adoption and enhancing hybrid deployment capabilities to capture evolving enterprise data needs.

Corpay, Inc.: Global Payment Solutions Leader

Corpay commands a unique position in corporate payment technology, generating revenue through vehicle and corporate payment solutions worldwide. It caters to diverse sectors, offering fuel cards, accounts payable automation, and travel expense management. The 2026 strategy emphasizes broadening international reach and innovating cross-border payment technologies to streamline corporate cash flow management.

Strategic Collision: Similarities & Divergences

Both companies operate in software infrastructure but contrast sharply in business philosophy: MongoDB centers on an open, flexible data platform, while Corpay builds a specialized, closed payment ecosystem. Their primary battleground lies in serving enterprise operational needs—data management versus payment processing. These divergent focuses create distinct investment profiles, reflecting MongoDB’s growth in cloud scalability against Corpay’s steady expansion in financial services.

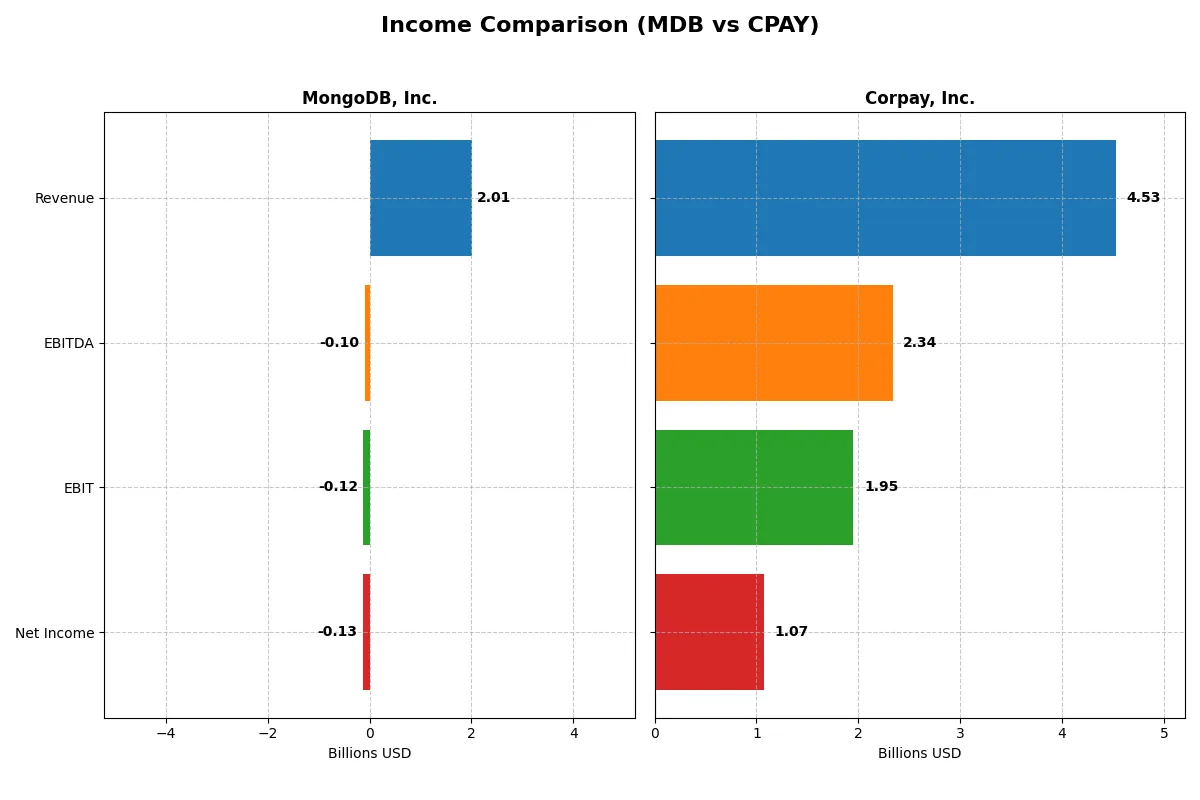

Income Statement Comparison

This data dissects the core profitability and scalability of both corporate engines to reveal who dominates the bottom line:

| Metric | MongoDB, Inc. (MDB) | Corpay, Inc. (CPAY) |

|---|---|---|

| Revenue | 2.01B | 4.53B |

| Cost of Revenue | 535M | 1.36B |

| Operating Expenses | 1.69B | 1.21B |

| Gross Profit | 1.47B | 3.17B |

| EBITDA | -97M | 2.34B |

| EBIT | -124M | 1.95B |

| Interest Expense | 8.1M | 404M |

| Net Income | -129M | 1.07B |

| EPS | -1.73 | 15.25 |

| Fiscal Year | 2025 | 2025 |

Income Statement Analysis: The Bottom-Line Duel

This income statement comparison reveals the true efficiency and profitability of MongoDB, Inc. and Corpay, Inc. over recent years.

MongoDB, Inc. Analysis

MongoDB’s revenue soared from $590M in 2021 to $2.0B in 2025, reflecting strong growth momentum. Despite a solid gross margin near 73%, it reports consistent net losses, though net margin improved to -6.4% in 2025. Operating expenses scale with revenue, yet persistent negative EBIT signals ongoing profitability challenges.

Corpay, Inc. Analysis

Corpay’s revenue expanded from $2.8B in 2021 to $4.5B in 2025, maintaining a robust gross margin close to 70%. It delivers strong operating and net margins of 43.1% and 23.6%, respectively, in 2025. Profitability remains solid with positive EBIT and net income growth, though net margin slightly declined over one year.

Verdict: Growth Potential vs. Established Profitability

MongoDB leads in revenue growth and margin expansion but struggles with profitability. Corpay boasts impressive margins and consistent net income, though its growth pace is more moderate. For investors, MongoDB’s profile suits those prioritizing rapid scale, while Corpay appeals to those valuing sustainable earnings and margin strength.

Financial Ratios Comparison

These vital ratios act as a diagnostic tool to expose the underlying fiscal health, valuation premiums, and capital efficiency of the companies analyzed:

| Ratios | MongoDB, Inc. (MDB) | Corpay, Inc. (CPAY) |

|---|---|---|

| ROE | -4.64% | 27.55% |

| ROIC | -7.36% | 8.78% |

| P/E | -158x | 20x |

| P/B | 7.32x | 5.43x |

| Current Ratio | 5.20 | 0.98 |

| Quick Ratio | 5.20 | 0.98 |

| D/E | 0.01 | 2.58 |

| Debt-to-Assets | 1.06% | 37.86% |

| Interest Coverage | -26.7x | 4.83x |

| Asset Turnover | 0.58 | 0.17 |

| Fixed Asset Turnover | 24.78 | 9.59 |

| Payout ratio | 0% | 0% |

| Dividend yield | 0% | 0% |

| Fiscal Year | 2025 | 2025 |

Efficiency & Valuation Duel: The Vital Signs

Ratios act as a company’s DNA, uncovering hidden risks and revealing operational excellence crucial for investment decisions.

MongoDB, Inc.

MongoDB posts negative returns on equity (-4.64%) and invested capital (-7.36%), signaling operational struggles. Its price-to-earnings ratio is negative but favorable due to losses, while a high price-to-book (7.32x) indicates valuation stretch. The firm retains cash with no dividends, focusing heavily on R&D (30% of revenue) to fuel growth.

Corpay, Inc.

Corpay delivers robust profitability with a 27.55% ROE and a solid net margin of 23.62%. Its P/E of 19.7x is reasonable, reflecting moderate valuation. The company carries higher debt (debt/equity 2.58) but maintains positive free cash flow and no dividends, likely reinvesting in business operations for expansion.

Growth Focus vs. Profitability Strength

MongoDB’s high R&D investment contrasts with Corpay’s strong profitability and more balanced valuation. Corpay offers a better risk-reward balance through consistent returns, while MongoDB fits investors prioritizing innovation despite near-term losses.

Which one offers the Superior Shareholder Reward?

MongoDB, Inc. (MDB) does not pay dividends and shows no buyback activity, focusing on reinvestment for growth despite persistent losses and negative margins. Corpay, Inc. (CPAY) also pays no dividends but delivers strong profitability with robust free cash flow (18.5/share in 2025) and consistent buybacks implied by improving leverage. CPAY’s distribution philosophy balances growth and shareholder returns more sustainably. I conclude CPAY offers a superior total return profile for 2026 investors, combining operational strength with prudent capital allocation.

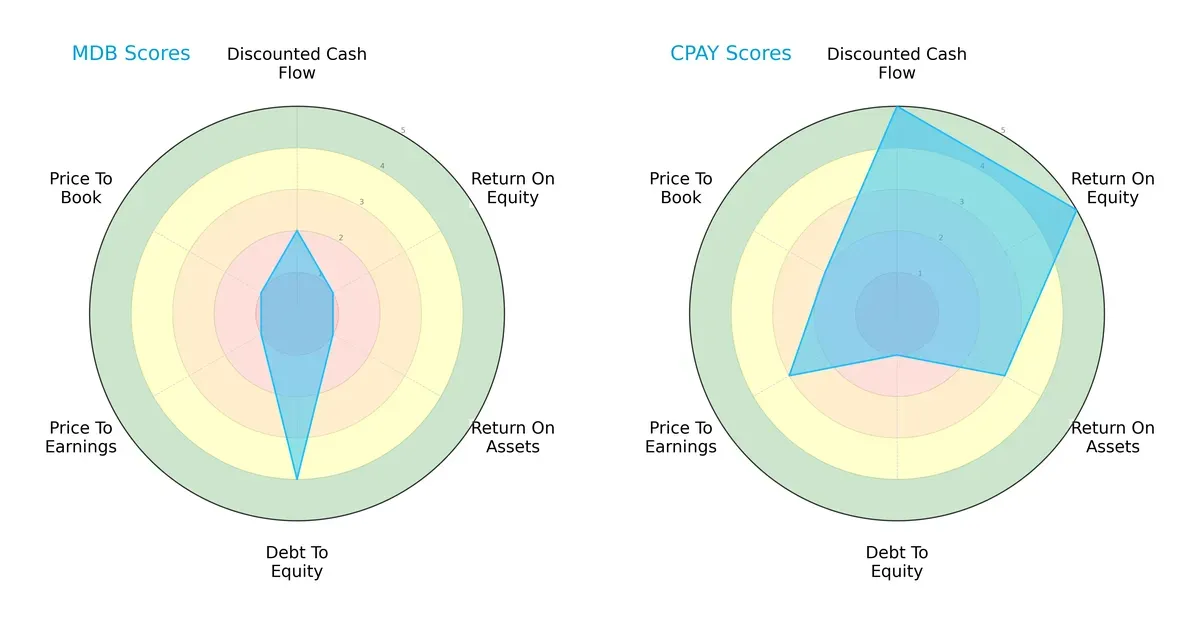

Comparative Score Analysis: The Strategic Profile

The radar chart exposes the fundamental DNA and trade-offs of MongoDB, Inc. and Corpay, Inc., highlighting their distinct financial strengths and vulnerabilities:

Corpay leads with a robust discounted cash flow (5 vs. 2) and superior return on equity (5 vs. 1) and assets (3 vs. 1). MongoDB counters with a stronger debt-to-equity score (4 vs. 1), signaling lower leverage risk. However, MongoDB’s valuation metrics lag, showing weakness in price-to-earnings and price-to-book ratios (1 vs. 3 and 1 vs. 2). Corpay’s profile is more balanced, leveraging operational efficiency and valuation, while MongoDB depends heavily on its conservative capital structure.

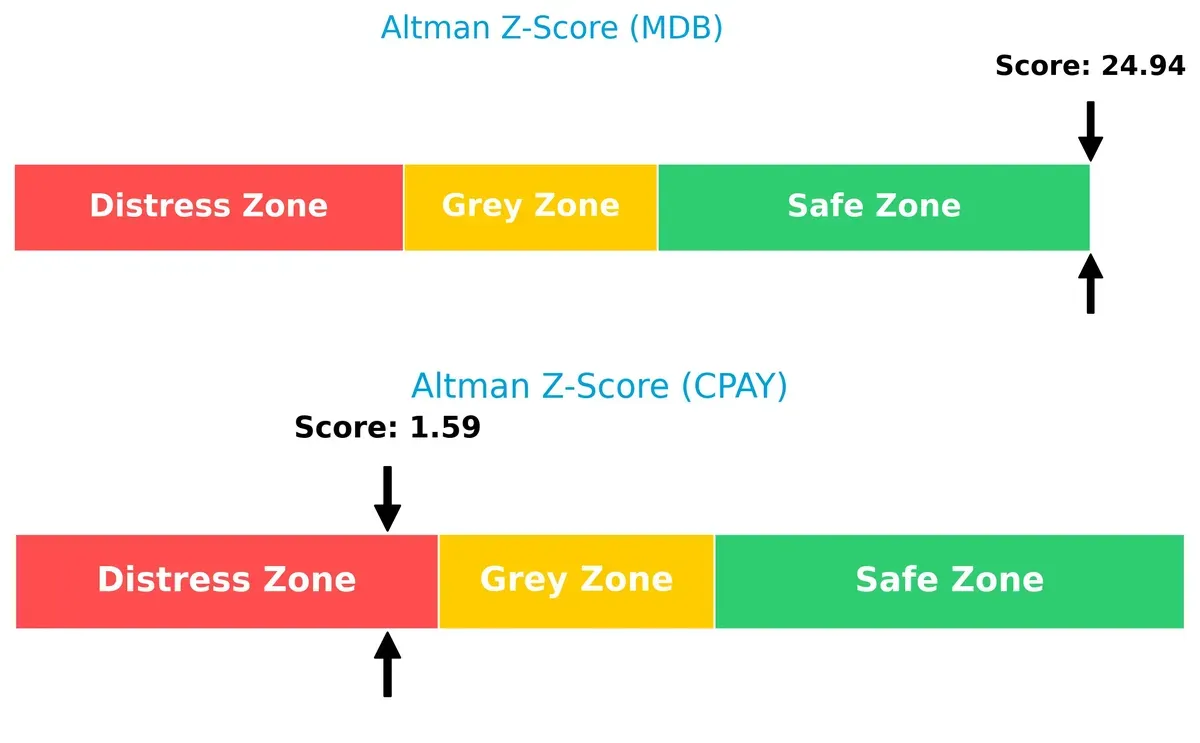

Bankruptcy Risk: Solvency Showdown

MongoDB’s Altman Z-Score (24.9) far exceeds Corpay’s (1.6), implying a vastly stronger solvency position and a lower bankruptcy risk in this economic cycle:

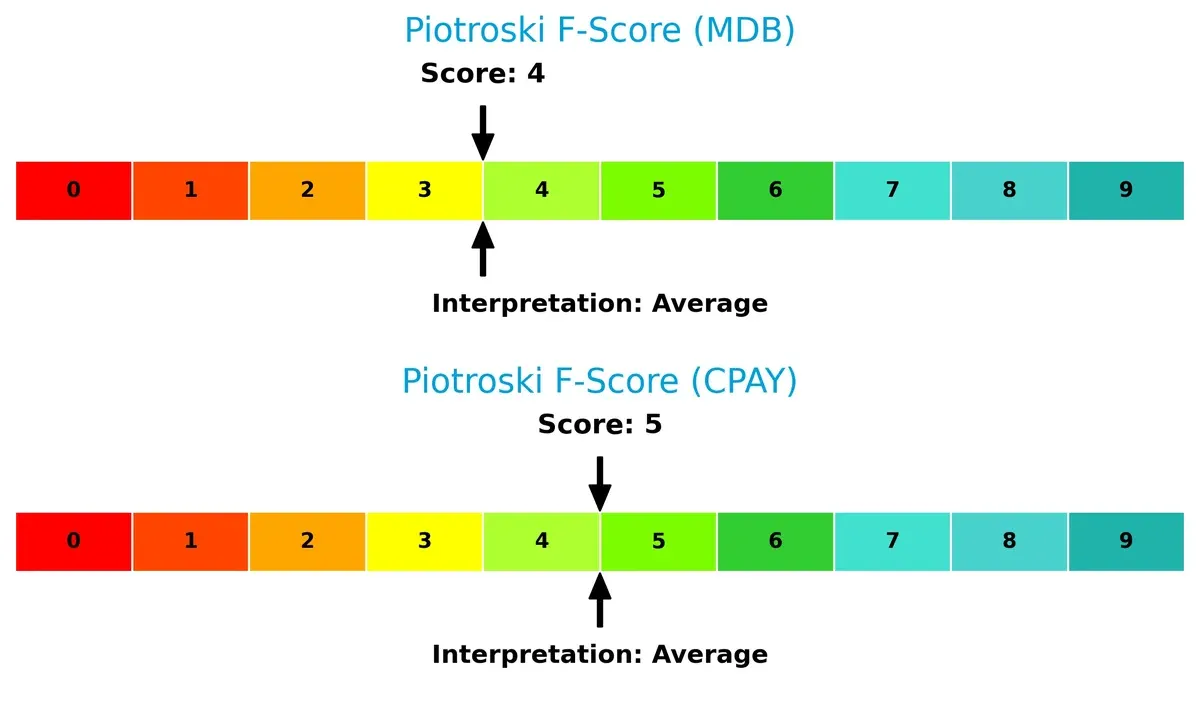

Financial Health: Quality of Operations

Both firms exhibit average Piotroski F-Scores, with Corpay slightly ahead (5 vs. 4). Neither shows peak financial health, signaling potential internal metric weaknesses that investors must monitor closely:

How are the two companies positioned?

This section dissects the operational DNA of MDB and CPAY by comparing their revenue distribution and internal dynamics. The goal is to confront their economic moats and identify which model offers the most resilient competitive advantage today.

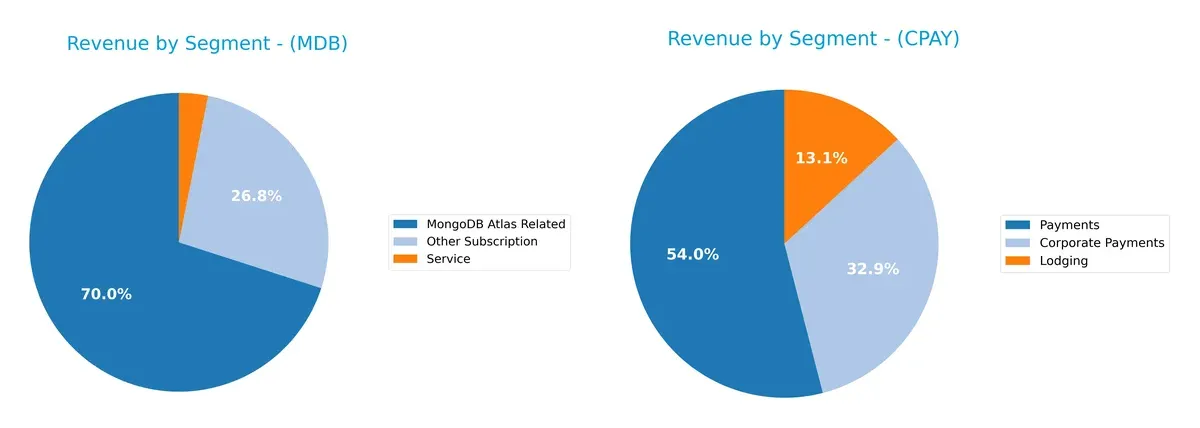

Revenue Segmentation: The Strategic Mix

This visual comparison dissects how MongoDB, Inc. and Corpay, Inc. diversify their income streams and reveals where their primary sector bets lie:

MongoDB anchors revenue in its Atlas cloud platform with $1.4B in 2025, complemented by $539M in other subscriptions, showing moderate diversification. Corpay relies heavily on its Payments segment, which dwarfs others at $2B, followed by Corporate Payments at $1.2B and Lodging at $489M. MongoDB’s focus on cloud services signals ecosystem lock-in, while Corpay’s concentration in payments exposes it to sector-specific risks despite scale.

Strengths and Weaknesses Comparison

This table compares the Strengths and Weaknesses of MongoDB, Inc. (MDB) and Corpay, Inc. (CPAY):

MDB Strengths

- Strong revenue growth in subscription services

- Diverse geographic presence across Americas, Asia Pacific, and EMEA

- Low debt-to-assets ratio (1.06%)

- High fixed asset turnover (24.78)

- Favorable quick ratio (5.2)

CPAY Strengths

- High net margin (23.62%) and ROE (27.55%)

- Favorable WACC (6.26%) supports capital efficiency

- Significant revenue from diverse payment services

- Strong presence in US, UK, and Brazil markets

- Favorable fixed asset turnover (9.59)

MDB Weaknesses

- Negative profitability metrics: net margin (-6.43%), ROE (-4.64%), ROIC (-7.36%)

- High price-to-book ratio (7.32) signals possible overvaluation

- Unfavorable interest coverage (-15.26)

- Unfavorable current ratio (5.2) indicating liquidity concerns

- No dividend yield

CPAY Weaknesses

- Moderate leverage with higher debt-to-equity (2.58)

- Unfavorable asset turnover (0.17) suggests lower operational efficiency

- Slightly unfavorable current ratio (0.98) raises liquidity caution

- Unfavorable price-to-book ratio (5.43)

- No dividend yield

The comparison reveals MDB’s strength in asset efficiency and geographic diversification but significant profitability and liquidity challenges. CPAY excels in profitability and market reach but faces operational efficiency and leverage risks. These factors shape strategic priorities for each company going forward.

The Moat Duel: Analyzing Competitive Defensibility

A structural moat is the only reliable shield protecting long-term profits from relentless competition erosion. Let’s dissect the core moats of two tech firms:

MongoDB, Inc.: Intangible Assets Powering Innovation

MongoDB’s moat stems from proprietary database technology and developer mindshare. Despite a negative ROIC vs. WACC, its rising profitability and 19% revenue growth signal expanding margin control. New cloud offerings could deepen its moat by locking in enterprise clients.

Corpay, Inc.: Cost Advantage Anchored by Scale

Corpay leverages cost-efficient payment processing and broad geographic reach, outperforming MongoDB with a positive ROIC exceeding WACC by 2.5%. Though profitability trends dip, its 43% EBIT margin and diverse payment solutions fortify its competitive position. Expansion in international markets offers growth levers.

Moat Strength Showdown: Innovation Intangibles vs. Scaled Cost Efficiency

Corpay’s cost advantage yields immediate value creation, but MongoDB’s intangible asset moat shows accelerating profitability potential. MongoDB faces a tougher path to value but builds a deeper moat through innovation. I see MongoDB better positioned to defend market share long term with ongoing product evolution.

Which stock offers better returns?

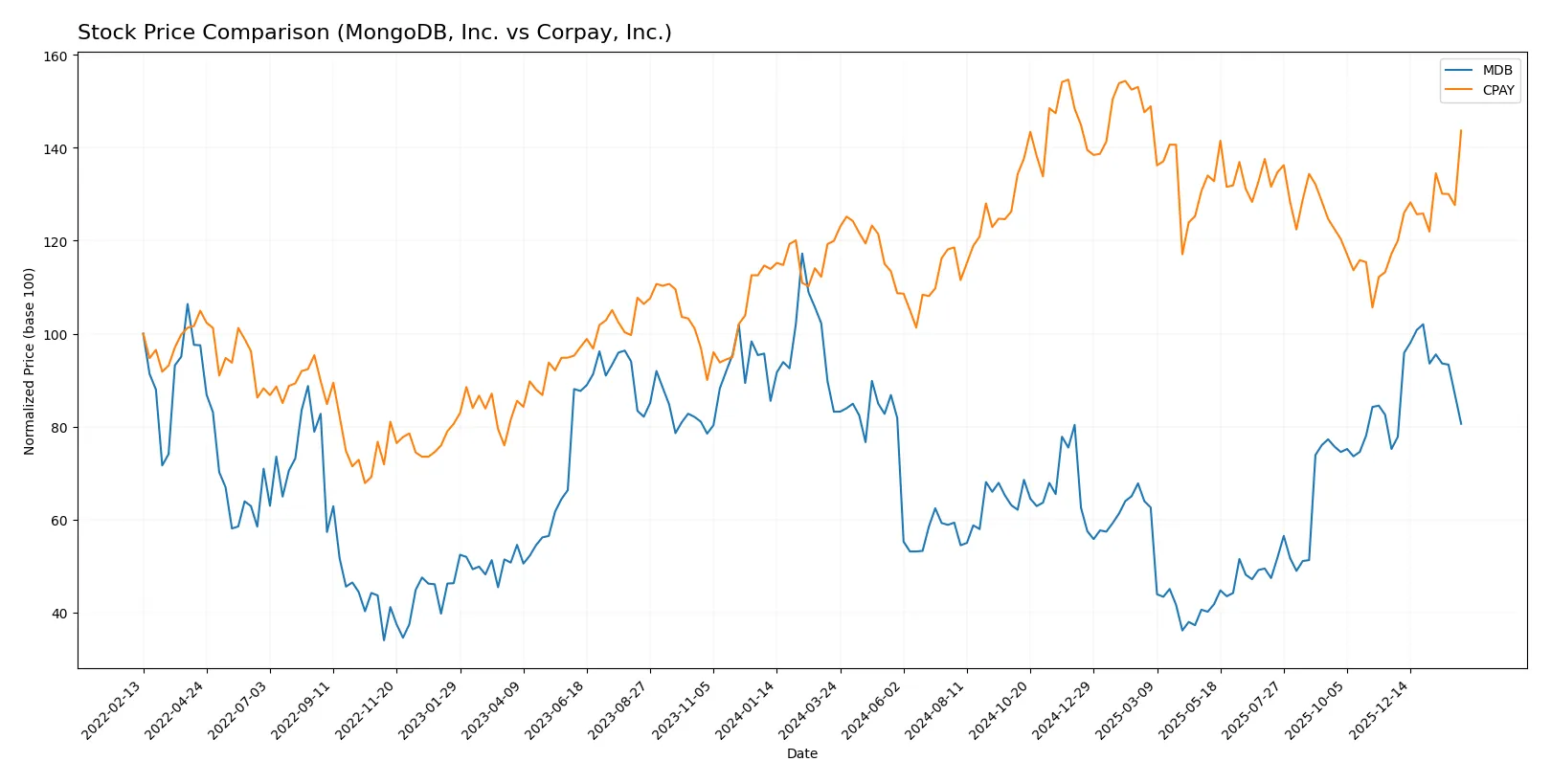

The past year reveals contrasting dynamics: MongoDB, Inc. shows a bearish trend with accelerating decline, while Corpay, Inc. registers a strong bullish acceleration in stock price.

Trend Comparison

MongoDB’s stock declined 3.12% over the last 12 months, marking a bearish trend with accelerating price drop and high volatility, ranging from $154 to $435.85. Corpay’s stock gained 19.8% over the same period, reflecting a bullish trend with acceleration and lower volatility, trading between $249.66 and $381.18. Corpay outperformed MongoDB significantly, delivering the highest market return among the two companies in the past year.

Target Prices

Analysts present a confident target consensus for MongoDB, Inc. and Corpay, Inc.

| Company | Target Low | Target High | Consensus |

|---|---|---|---|

| MongoDB, Inc. | 375 | 500 | 445.2 |

| Corpay, Inc. | 300 | 390 | 359.33 |

The target consensus for MongoDB, Inc. suggests a 29% upside from the current price of $344.35. Corpay, Inc.’s targets imply a modest upside near 1.5% above its $354.19 share price.

Don’t Let Luck Decide Your Entry Point

Optimize your entry points with our advanced ProRealTime indicators. You’ll get efficient buy signals with precise price targets for maximum performance. Start outperforming now!

How do institutions grade them?

Here is a summary of recent institutional grades for MongoDB, Inc. and Corpay, Inc.:

MongoDB, Inc. Grades

The following table lists MongoDB’s recent grades from reputable financial institutions.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Needham | Maintain | Buy | 2026-01-20 |

| Needham | Maintain | Buy | 2026-01-12 |

| Barclays | Maintain | Overweight | 2026-01-12 |

| Truist Securities | Maintain | Buy | 2026-01-07 |

| Needham | Maintain | Buy | 2026-01-06 |

| RBC Capital | Maintain | Outperform | 2026-01-05 |

| Argus Research | Maintain | Buy | 2025-12-04 |

| Goldman Sachs | Maintain | Buy | 2025-12-03 |

| Citigroup | Maintain | Buy | 2025-12-03 |

| Bernstein | Maintain | Outperform | 2025-12-02 |

Corpay, Inc. Grades

Below are Corpay’s recent grades from verified rating agencies.

| Grading Company | Action | New Grade | Date |

|---|---|---|---|

| Mizuho | Maintain | Neutral | 2026-02-06 |

| JP Morgan | Maintain | Overweight | 2026-02-05 |

| RBC Capital | Maintain | Sector Perform | 2026-02-05 |

| Morgan Stanley | Maintain | Overweight | 2026-02-05 |

| Morgan Stanley | Upgrade | Overweight | 2026-01-26 |

| Oppenheimer | Maintain | Outperform | 2026-01-12 |

| Oppenheimer | Upgrade | Outperform | 2025-12-05 |

| UBS | Maintain | Neutral | 2025-11-06 |

| RBC Capital | Maintain | Sector Perform | 2025-11-06 |

| JP Morgan | Maintain | Overweight | 2025-11-06 |

Which company has the best grades?

MongoDB consistently receives strong Buy and Outperform ratings from top firms, signaling broad institutional confidence. Corpay carries mixed ratings, including Neutral and Sector Perform, suggesting more cautious sentiment. Investors may view MongoDB’s superior grades as reflecting greater growth or stability prospects.

Risks specific to each company

The following categories identify critical pressure points and systemic threats facing MongoDB, Inc. and Corpay, Inc. in the 2026 market environment:

1. Market & Competition

MongoDB, Inc.

- Faces intense competition in cloud database services with pressure on innovation and pricing.

Corpay, Inc.

- Operates in crowded payments space, challenged by fintech disruptors and evolving client needs.

2. Capital Structure & Debt

MongoDB, Inc.

- Extremely low debt (D/E 0.01) reduces financial risk; strong balance sheet supports growth.

Corpay, Inc.

- Higher leverage (D/E 2.58) increases financial risk and interest burden despite operational profitability.

3. Stock Volatility

MongoDB, Inc.

- Beta 1.385 indicates above-market volatility, increasing risk during economic downturns.

Corpay, Inc.

- Beta 0.808 shows lower volatility, offering more stability in turbulent markets.

4. Regulatory & Legal

MongoDB, Inc.

- Subject to data privacy and cloud security regulations that may increase compliance costs.

Corpay, Inc.

- Faces regulatory scrutiny in payment processing and cross-border compliance complexities.

5. Supply Chain & Operations

MongoDB, Inc.

- Relies heavily on cloud infrastructure providers, with potential risks in service interruptions.

Corpay, Inc.

- Dependent on global payment networks and technology vendors, vulnerable to operational disruptions.

6. ESG & Climate Transition

MongoDB, Inc.

- ESG risks tied to data center energy use and software sustainability initiatives.

Corpay, Inc.

- Exposure to climate transition through fleet and travel payments; must align with evolving ESG standards.

7. Geopolitical Exposure

MongoDB, Inc.

- Primarily U.S.-based with moderate international exposure, limiting geopolitical risk.

Corpay, Inc.

- Operates internationally, including Brazil and UK, facing currency and geopolitical uncertainties.

Which company shows a better risk-adjusted profile?

MongoDB’s biggest risk is operational losses with negative ROIC and poor profitability metrics despite a fortress-like balance sheet. Corpay’s main threat is high leverage that elevates financial risk amid moderate profitability. MongoDB’s higher stock volatility and weak returns worsen its risk profile. Corpay’s stable earnings and lower volatility make it a better risk-adjusted choice, though its debt load demands caution. Recent data confirm MongoDB’s negative return on equity contrasts sharply with Corpay’s robust 27.55% ROE, justifying concern over MongoDB’s capital efficiency.

Final Verdict: Which stock to choose?

MongoDB’s superpower lies in its rapid revenue and profitability growth, signaling a strong product-market fit and innovation edge. However, its consistent negative returns on invested capital call for vigilance on capital efficiency. It suits investors aiming for aggressive growth with tolerance for operational risks.

Corpay’s strategic moat is its stable cash flow generation backed by recurring revenue and solid profitability metrics. Its value creation surpasses cost of capital, offering better financial stability than MongoDB. It fits well in Growth at a Reasonable Price (GARP) portfolios seeking balance between growth and risk.

If you prioritize rapid expansion and innovation, MongoDB is the compelling choice due to its accelerating income growth despite current capital inefficiencies. However, if you seek better financial stability and consistent value creation, Corpay offers superior risk-adjusted returns and cash flow reliability, albeit with slower growth momentum.

Disclaimer: Investment carries a risk of loss of initial capital. The past performance is not a reliable indicator of future results. Be sure to understand risks before making an investment decision.

Go Further

I encourage you to read the complete analyses of MongoDB, Inc. and Corpay, Inc. to enhance your investment decisions: